EIX - Edison International: Reasonable Results But Some Risks Here

2023-07-31 13:13:08 ET

Summary

- Edison International reported Q2 results that generally showed its financial stability over time.

- The population of the company's service territory is declining, which is exerting adverse impacts on its revenues.

- The company is positioned to deliver a 9% to 11% total average annual return to its investors through 2028 assuming it achieves its growth projections.

- The company has a fairly high leverage, which poses some risks to investors.

- The current stock price looks a bit high, so it might be best to wait until it declines before buying in.

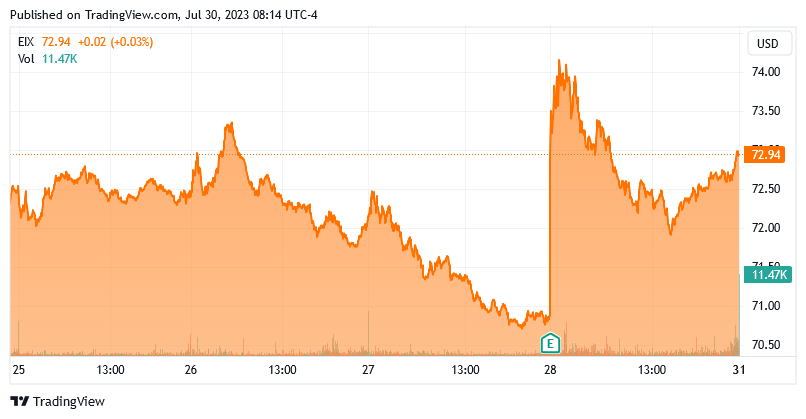

On Thursday, July 27, 2023, California-based regulated electric utility Edison International ( EIX ) announced its second quarter 2023 earnings results. At first glance, these results appeared to be mixed, as the company missed the expectations of its analysts in terms of top-line revenue, but it still managed an earnings beat. The market certainly seemed to appreciate the earnings results, despite the revenue miss, as the stock price jumped in the trading session that followed the announcement:

{kind=link}

The utility sector has long been appreciated by conservative risk-averse investors, such as retirees, for its general stability and dependable growth. We do not see that here though, as Edison International's revenues were down year-over-year, although earnings were up fairly substantially. The company provided guidance that suggests that it will continue to deliver more growth over the remainder of this year and it does seem likely to deliver it.

One big problem here, though, is that the company is located in California and the demographics of California are not particularly favorable for utilities. Edison International will probably be able to overcome this and still deliver growth, but that does not mean that investors are getting a good deal. The company appears to be very expensive relative to its peers, so it might be best to sit on the sidelines and wait for a better entry point.

Earnings Results Analysis

As my long-time readers are likely well aware, it is my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Edison International's second-quarter 2023 earnings results:

- Edison International brought in total revenue of $3.964 billion during the second quarter of 2023. This represents a 1.10% decline over the $4.008 billion that the company brought in during the prior-year quarter.

- The company reported an operating income of $724 million in the reporting period. This compares quite favorably to the $504 million that the company earned during the year-ago quarter.

- Edison International's regulated electric utility Southern California Edison completed covering 5,000 miles of bare electric wire with a covered conductor. The company claims that this will reduce the risk of catastrophic wildfire damage by 85%.

- The company reported an operating cash flow of $802.0 million in the most recent quarter. This represents a 79.82% increase over the $446.0 million that the company generated in the equivalent quarter of last year.

- Edison International reported a net income of $354 million in the second quarter of 2023. This represents a 46.89% increase over the $241 million that it reported in the second quarter of 2022.

It seems certain that the first thing that anyone reading these highlights will notice is that Edison International's revenue went down compared to the prior-year quarter. The company did not actually provide any reason for this, but there are quite a few possibilities. One is that the Edison Energy business unit had lower revenues than during the year-ago quarter. Edison Energy is a business that advises industrial, commercial, and other institutional customers on ways to reduce their energy usage. This is not a regulated utility business, so it does not enjoy the same stable revenues and cash flows that the utility business would, which means that it is somewhat more vulnerable to fluctuations in the business cycle.

Curiously, Edison International said absolutely nothing about the performance of this business unit in its conference call . In fact, the income statements and balance sheets that the company provided in its earnings report do not break down the revenue earned by its different business units, so we do not know if weakness with the non-utility business was a reason for the revenue decline or not. However, given the fairly small proportional size of the revenue decline, it could have been caused by just about anything.

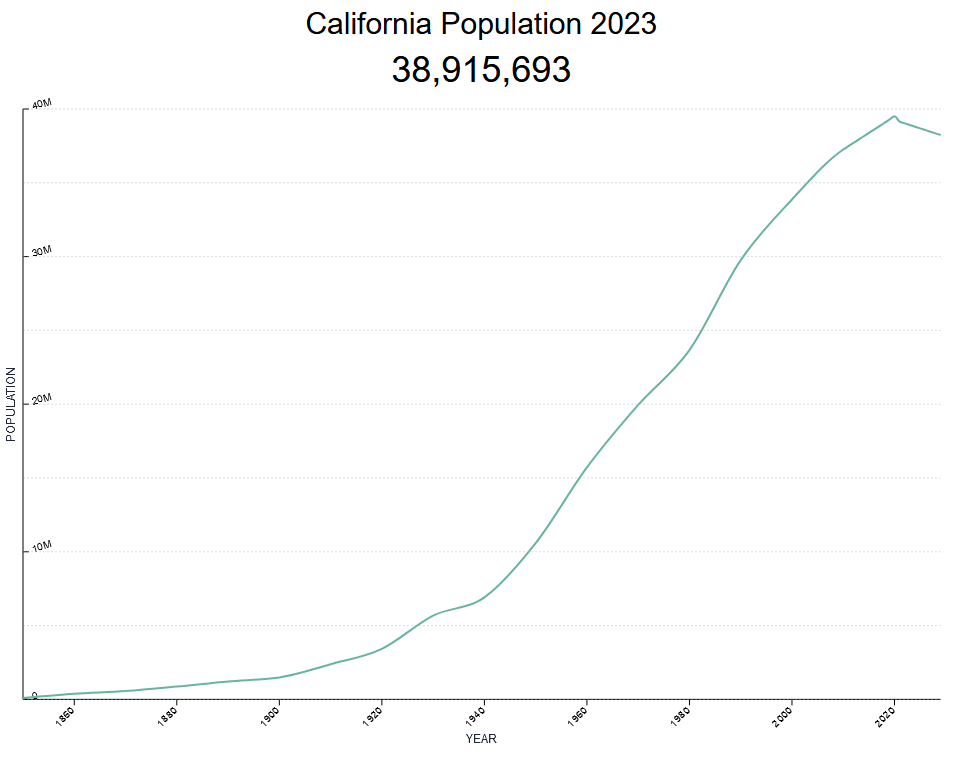

In the introduction to this article, I mentioned that Edison International has to contend with some demographic problems due to the fact that it operates in California. This comes mainly from the fact that California's population is declining. As we can see here, the state's population peaked in 2020 and then began to decline:

{kind=link}

This is at least partly due to the pandemic. As everyone reading this is no doubt well aware, the COVID-19 pandemic led to a significant increase in remote work. Employees no longer have to commute to their offices anymore, so there is no reason why they necessarily have to live close to their workplace. As a result, people are able to live wherever they choose, and by and large, they are opting not to live in California. In 2020, the state actually lost a seat in the House of Representatives due to its poor demographic trends. KTLA, a local television station in Las Angeles, makes note of this as well. There is also some anecdotal evidence, such as a shortage of Uhaul trucks available for people trying to move out of California. In short, while there may be some politicians and people on social media trying to argue the opposite, most evidence does point to people opting to leave California in favor of other states.

This matters for Edison International due to the fact that it is a utility. As a utility, it is a monopoly that is confined by government regulations to operating in only one specific area. In this case, that service territory is most of Southern California:

{kind=link}

This is basically the Los Angeles metropolitan area and San Bernadino County, which includes a lot of areas that are widely known in the public consciousness due to the enormous number of television shows and movies set in this area. It is also one of the most populated areas of the nation, although as just mentioned the population appears to be declining. With that said Edison International's web page claims that it serves about fifteen million customers, which makes it one of the largest utilities in the country. It did not provide an exact figure in its most recent earnings report, however. As the population of this region is declining, the company's customer count is probably also declining. This means that it has fewer people paying their electric bills every month, which has an adverse impact on its revenue.

Thus, all else being equal, we could expect the company's revenues to decline over time. That would have an adverse impact on profits because lower revenue means that less money is available to cover the company's costs and make its way down to cash flows and profits.

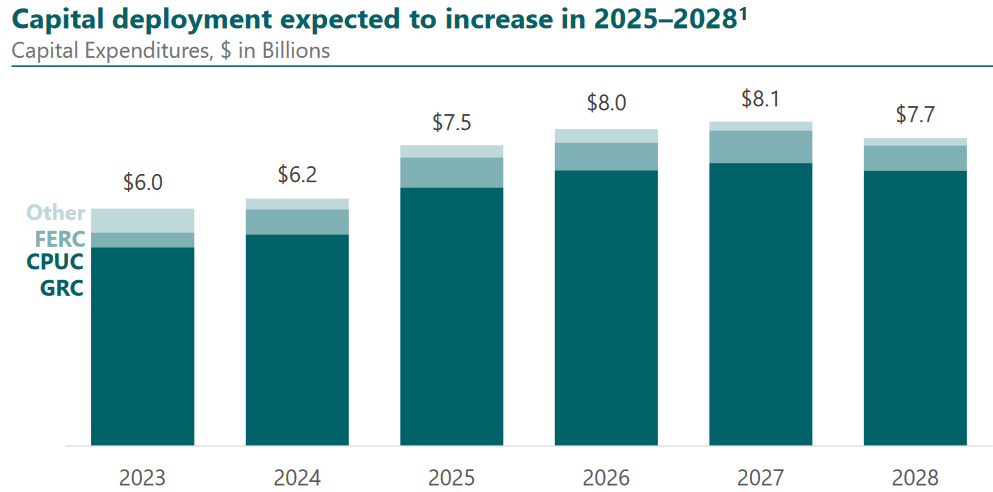

However, Edison International does have ways that it can offset the impact of a declining customer base and still generate growth. One of these is through growing its rate base. The rate base is the value of the company's assets upon which regulators allow the company to earn a specified rate of return. As this rate of return is a percentage, any increase in the rate base allows the company to positively adjust the prices that it charges its customers in order to earn that specified rate of return. The usual way that a company will grow its rate base is by investing money into upgrading, modernizing, or possibly expanding its utility-grade infrastructure. This is exactly what Edison International is planning to do. In its earnings conference call, the company outlined a plan to invest $38 billion to $43 billion over the 2023 to 2028 period into growing its rate base:

{kind=link}

This is fairly nice to see as this is a bit longer than the capital investment programs that have been provided by most of the company's peers. In fact, the best that we have seen from pretty much any other company in the sector is a plan for the 2023 to 2027 period. Edison International is thus providing us with an additional year relative to its peers. This is nice because of the visibility that it provides us into the company's forward performance. After all, as investors, we are forward-looking and like to be able to make predictions about where a company will be five or ten years from now. The more information that we have about its capital spending plans, the easier it is to make such predictions. The fact that Edison International is providing such a long projection horizon to its shareholders is thus rather shareholder-friendly.

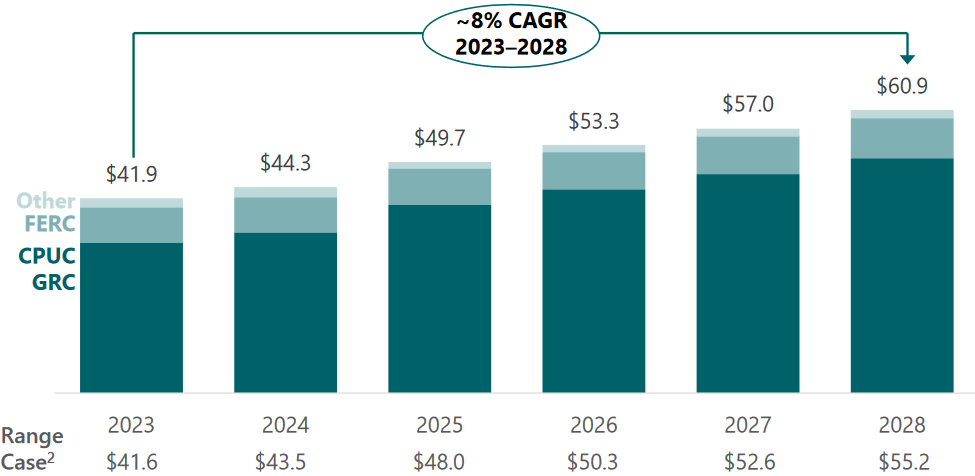

The company's planned capital investment program should allow it to grow its rate base at an 8% compound annual growth rate over the 2023 through 2028 period:

{kind=link}

This is sufficient to allow the company to grow its earnings per share at a 5% to 7% rate over the period. At this point, some readers might point out that this projected growth rate is less than the projected growth rate of the rate base. One of the biggest reasons for this is that Edison International needs to finance its growth through the issuance of common equity and debt. This is fairly common for a utility, but it does have a negative impact on the company's earnings per share growth. The reason for this should be fairly obvious, as the issuance of new common equity dilutes the shareholders since the company's earnings have to be divided among more shares. In addition, the debt issuances will require the company to pay interest, which will offset some of the net income growth. However, a 5% to 7% earnings per share growth rate is still in line with what most other utilities should be able to deliver over the period. When we combine this with Edison International's 4.04% dividend yield, the company should be able to deliver a 9% to 11% average annual total return over the period. This is a very reasonable return for a conservative utility stock.

Financial Considerations

It is always important to review the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. That can cause a company's interest expenses to go up following the rollover because new debt is issued with an interest rate that corresponds to the market rate at the time of issuance. As of the time of writing, interest rates are at the highest level that we have seen since 2007 so this is a very real risk today. In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company's cash flows to decline could push it into financial distress if it has too much debt. While utilities like Edison International usually have fairly stable cash flows over time, there have been bankruptcies in the sector before so this is a risk that we should not ignore.

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio basically tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company's equity can cover its debt obligations in the event of a liquidation or bankruptcy event, which is arguably more important.

As of June 30, 2023, Edison International had a net debt of $34.516 billion compared to total shareholders' equity of $17.694 billion. This gives the company a net debt-to-equity ratio of 1.95 today. Here is how that compares to some of the company's peers:

| Company |

| Net Debt-to-Equity Ratio |

| Edison International |

| 1.95 |

| CMS Energy ( CMS ) |

| 1.91 |

| CenterPoint Energy ( CNP ) |

| 1.57 |

| DTE Energy ( DTE ) |

| 1.89 |

| PG&E Corporation ( PCG ) |

| 2.29 |

As we can see here, Edison International appears to be more reliant on debt to finance its obligations than many of its peers. In fact, the only company here that uses leverage to a greater degree is fellow California utility PG&E Corporation. If we were to include peers from more locations around the nation (two of these are California utilities and two are Michigan utilities) then we would see that Edison International appears very heavily levered compared to the sector. This is immediately apparent from looking at my past articles on other companies. However, Edison International is one of the only companies in the sector that has reported its second-quarter earnings and I do not feel comfortable comparing it directly to companies that have not yet reported. However, this does not change the fact that Edison International has a higher debt load than we really want to see and this poses a risk that no investor should ignore.

Dividend Analysis

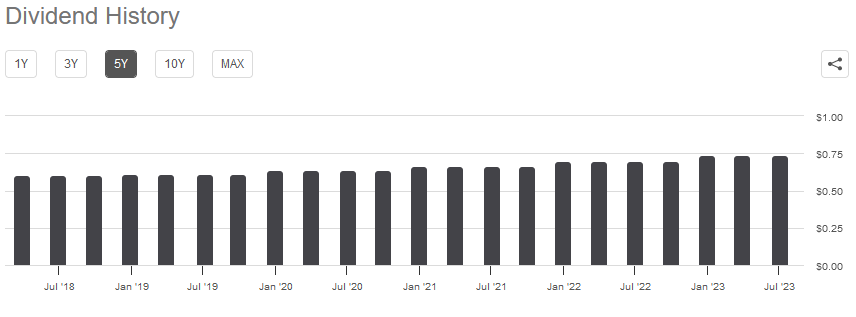

One of the biggest reasons that we purchase utilities is that these companies tend to have higher dividend yields than companies in many other sectors. This comes from the simple fact that utilities tend to be fairly slow-growth entities so they cannot be depended on for the enormous capital gains that we see in the technology sector, for example. Thus, a utility will pay out a significant portion of its profits to its shareholders in order to provide them with an acceptable return. When we combine this with the fact that the market does not usually assign high earnings multiples to utility companies, the dividend ends up being a substantial percentage of the share price. Edison International is no exception to this as the stock yields 4.04% as of the time of writing, which is substantially above the 1.43% yield of the S&P 500 Index ( SPY ). Edison International also has a long history of raising its dividend on an annual basis:

{kind=link}

The fact that the company increases its dividend each and every year is something that is very nice to see during periods of inflation, such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it feel as though a person is getting poorer and poorer with the passage of time, which is especially problematic for those that are depending on their portfolios for the income that they need to survive. The fact that the company increases the amount that it pays out helps to offset this effect and ensures that the dividend maintains its purchasing power over time.

As is always the case though, it is critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut since such an event would reduce our incomes and almost certainly cause the stock price to decline. Let us investigate this and determine if it could be a possibility here.

The usual way that we judge a company's ability to maintain its dividend is by looking at its free cash flow. The free cash flow is the amount of cash that was generated by the company's ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is therefore the money that can be used for things such as reducing debt, buying back stock, or paying dividends. During the second quarter of 2023, Edison International had a negative levered free cash flow of $941.5 million. Obviously, this is not enough to pay any dividends yet the company still paid out $278.0 million in dividends during the quarter. At first glance, this is likely to be quite concerning since the company is not generating nearly enough free cash flow to finance its payouts.

However, it is not atypical for a utility to finance its capital expenditures through the issuance of both debt and equity. We discussed this earlier in this article. The company will then finance its dividends out of operating cash flow. The reason that this is done is that utilities tend to have enormous capital expenditures due to the high cost of constructing and maintaining utility-grade infrastructure over a wide geographic area. These costs are sufficient to preclude ever paying a dividend if it was financed out of free cash flow. During the second quarter of 2023, Edison International reported an operating cash flow of $802.0 million. That was easily enough to cover the $278.0 million that was paid out in dividends with quite a bit of money left over that can be used for other tasks. Overall, the company's dividend is probably reasonably safe.

Valuation

It is critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility, one way to value it is by looking at the price-to-earnings growth ratio. This ratio is a modified version of the familiar price-to-earnings ratio that takes a company's earnings per share per growth into account. A price-to-earnings ratio of less than 1.0 indicates that a stock may be undervalued relative to its earnings per share growth and vice versa. However, it is incredibly rare for a utility stock to be undervalued by this metric in the current richly-valued market. As such, the best way to use this ratio is to compare Edison International to its peers in order to see which stock offers the most attractive relative valuation.

According to Zacks Investment Research , Edison International will grow its earnings per share at a 3.69% rate over the next three to five years. This is a lot less than we projected earlier based on the company's rate base growth. Edison International has a price-to-earnings growth ratio of 4.19 at the current price assuming that earnings per share growth. Here is how the company compares to its peer group:

| Company |

| PEG Ratio |

| Edison International |

| 4.19 |

| CMS Energy |

| 2.52 |

| CenterPoint Energy |

| 2.69 |

| DTE Energy |

| 3.07 |

| PG&E Corporation |

| 5.82 |

As we can see here, Edison International appears to be fairly expensive relative to its peers. However, this assumes that the Zacks estimate of 3.69% earnings per share growth is correct. If we use management's 5% earnings per share growth estimate, the company has a price-to-earnings growth ratio of 3.09 today, which still makes it look expensive. Overall, the only real conclusion that we can draw here is that the stock has gotten a bit ahead of itself and needs to come down a bit before we buy it.

Conclusion

In conclusion, Edison International posted reasonable Q2 results that generally show its stability over time. This is a characteristic that it shares with most other companies in the sector. However, the company has some challenges ahead of it considering that the population in its service area is declining. Edison International also appears to be a bit riskier than some of its peers in terms of both leverage and valuation. While there are some nice things here, it may be best to wait for a better price before buying in considering the risks.

For further details see:

Edison International: Reasonable Results, But Some Risks Here