CRSP - Editas Medicine's Pivot: From CRISPR To Programmable Gene Editing

2023-12-28 13:10:55 ET

Summary

- Editas Medicine is transitioning from platform development to establishing itself as a key player in the commercial therapeutics market.

- The company's strategic priorities include fast-tracking the clinical development of EDIT-301, shifting focus to in vivo editing therapies, and expanding business development activities.

- Editas holds an extensive IP portfolio and has granted licenses to companies like Vertex, showcasing the commercial potential of their intellectual property.

Editas Medicine (EDIT), initially a front-runner in the CRISPR technology arena, now navigates a competitive landscape. While CRISPR Therapeutics AG (CRSP) is on the verge of launching its first commercial product and Intellia Therapeutics (NTLA) is at the forefront of in-vivo therapy developments, Editas is carving out its niche. The company is currently transitioning from a primary focus on platform development to establishing itself as a key player in the commercial therapeutics market.

Repositioning

The management at Editas Medicine is strategically steering the company with a few key priorities:

Fast-Tracking EDIT-301 : The first pillar of their strategy is to expedite the clinical development of EDIT-301, a gene-edited medicine aimed at treating severe sickle cell disease and transfusion-dependent beta-thalassemia.

Shift to In Vivo Editing : Secondly, they are recalibrating their research focus toward in vivo editing therapies. This shift from ex vivo (editing outside the organism) to in vivo (editing within the organism) signifies a deeper dive into more complex, yet potentially more scalable gene therapies.

Business Development Expansion: The third pillar involves broadening their business development activities. This includes forming partnerships to enhance their in vivo development pipeline and strategically out-licensing their intellectual property ("IP") and expertise. The goal here is to maximize the application and impact of CRISPR-based medicines.

Earlier this year, Editas made a strategic pivot to position itself as a leader in programmable gene editing. This move is not just about expanding the range of diseases they target but also encompasses advancing the discovery of in vivo editing in hematopoietic stem cells (HSCs) and other tissues.

In addition to these research and development strategies, Editas is keen on leveraging its substantial IP portfolio. The company holds an extensive array of foundational U.S. and international patents in gene editing. Notably, they are the exclusive licensee of the Cas9 patent estate from Harvard University and the Broad Institute. This patent covers the use of Cas9, a crucial enzyme in CRISPR gene editing, for developing human medicines.

The recent licensing deal with Vertex Pharmaceuticals exemplifies the utility and value of Editas's IP. In this agreement, Editas granted Vertex a non-exclusive license for ex vivo Cas9 gene-edited HSC therapies, underscoring the commercial potential of their intellectual property.

EDIT-301

Additionally, the company is also working on their own programs, the most advanced being the EDIT-301.

In this program, Editas has achieved a milestone in patient recruitment. They have enrolled 27 patients with sickle cell disease and eight patients with beta-thalassemia in their RUBY and EdiTHAL studies , respectively. This exceeds their initial target of enrolling 20 patients in the RUBY trial.

One significant regulatory achievement for Editas has been the FDA's grant of a Regenerative Medicine Advanced Therapy ("RMAT") designation for EDIT-301 for the treatment of severe sickle cell disease. This RMAT designation is a notable marker of potential, offering advantages akin to the Fast Track and Breakthrough Therapy programs. These include comprehensive FDA guidance to streamline drug development, an opportunity for a rolling review (permitting Editas to submit sections of their Biologic License Application or BLA as they are completed), and a priority review of the BLA. This expedited process is not only a testament to the treatment's promise but also could considerably speed up the drug's path to market.

New Chief Commercial and Strategy Officer

The management team has actively addressed organizational challenges to enhance its strategic and commercial operations. A key development in this effort was the appointment of Caren Deardorf as the Chief Commercial and Strategy Officer in late September.

Bringing Deardorf on board is a strategic decision, leveraging her vast experience in the commercialization of therapeutics. Deardorf is known for her skill in transforming early discovery and clinical assets into well-defined business strategies. This capability is crucial for Editas as it shifts from a research-focused entity to a company that successfully brings products to market.

Her expertise is not just limited to commercialization but also extends to disciplined portfolio prioritization and value creation. This approach is essential for Editas to maximize the potential of its diverse range of therapies and research projects. Deardorf's experience in leading successful product launches, both in the U.S. and globally, stands out. Her proficiency in this domain suggests that she will be instrumental in successfully introducing Editas' therapies into the market.

In Vivo Therapy Development

A significant challenge for companies trailing in the industry is the recognition that while the ex-vivo approach has been valuable as a proof-of-concept, it may not be the most scalable or sustainable option for a thriving therapeutics industry. Many experts are now seeing in-vivo therapies as the key to scalability .

Understanding this industry shift, Editas Medicine has taken proactive steps. Earlier in the year, the company's drug discovery group initiated lead discovery work on in-vivo therapeutic targets, specifically focusing on hematopoietic stem cells and other tissues. This shift represents a significant expansion of their research, moving beyond the realm of ex-vivo therapies, which involve modifying cells outside the body before reintroduction.

Financials

{kind=link}

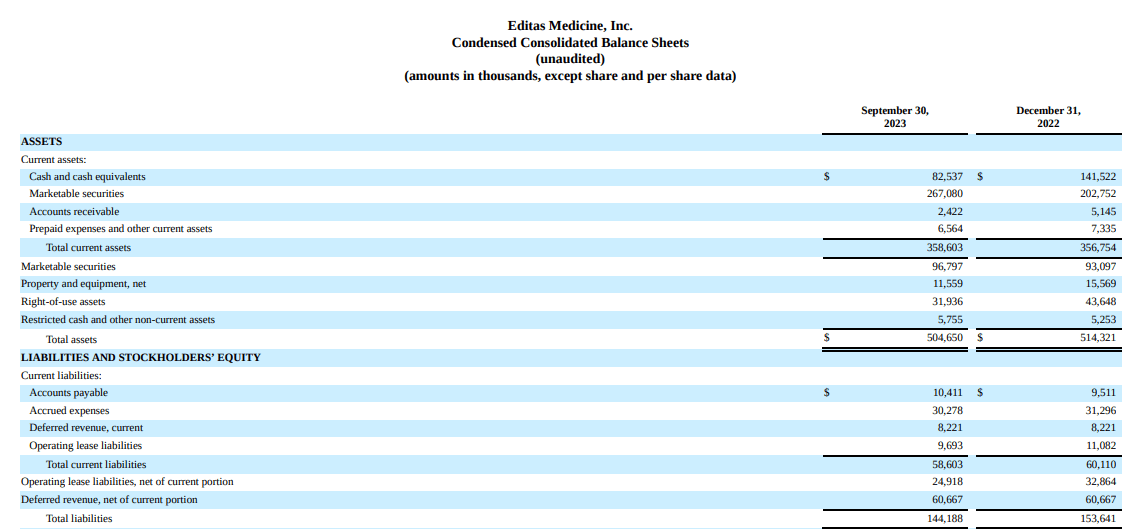

As of September 30, Editas Medicine's financial position included $446 million in cash, cash equivalents, and marketable securities, a slight decrease from the $480 million reported on June 30, 2023. The company's current financial assets are anticipated to support its operating expenses and capital expenditures well into the third quarter of 2025, indicating a two-year financial runway.

For the third quarter of 2023, Editas reported revenue of $5.3 million, largely attributable to the upfront payment received from the non-exclusive Cas9 license agreement with Vor Bio in August 2023.

The company's research and development (R&D) expenses for the quarter remained stable at $41 million, mirroring the expenses from the third quarter of 2022. This consistency in R&D spending is a result of a strategic balance between reduced expenses, driven by a focused shift towards the EDIT-301 program, and increased investment in pre-commercialization activities, such as medical affairs and patient advocacy.

General and administrative (G&A) expenses for the same period were $15 million, showing a reduction from the $16 million incurred in the third quarter of 2022. This decrease can be primarily attributed to lowered headcount expenses, including stock compensation, and a reduction in legal costs.

Valuation & Risks

Based on current financial data, Editas Medicine is estimated to have a cash burn rate of approximately $146 million per year. Note that this figure is primarily based on the current year's financial data, including an estimation for the 4th quarter. Based on trends observed in previous quarters, I expect the figures for the 4th quarter to be slightly lower. If we were to use the trailing twelve-month ("TTM") data, the operating cash flow would be around $152 million. In any case, this rate seems to align with the company's projection of sustaining operations until 2025 with its existing financial resources.

Comparatively, an analysis of CRISPR Therapeutics AG reveals some contrasts. Despite a higher cash burn rate, CRISPR AG benefits from a larger cash reserve, which offers a longer financial runway. Crucially, CRISPR AG is nearing the commercialization of its first therapy. Additionally, its partnership with Vertex, which owns 60% of the program, is a significant factor differentiating it from Editas. This partnership reduces the financial and operational burden on CRISPR AG and aids in the commercial launch.

In contrast, Editas presents a riskier investment option. While there is potential upside due to its intellectual property portfolio and strategic repositioning, its current financial and commercial standing - particularly as it still works toward launching its first product - makes it a less attractive asset. The market has recognized these factors, and this is reflected in Editas's performance relative to its peers.

{kind=link}

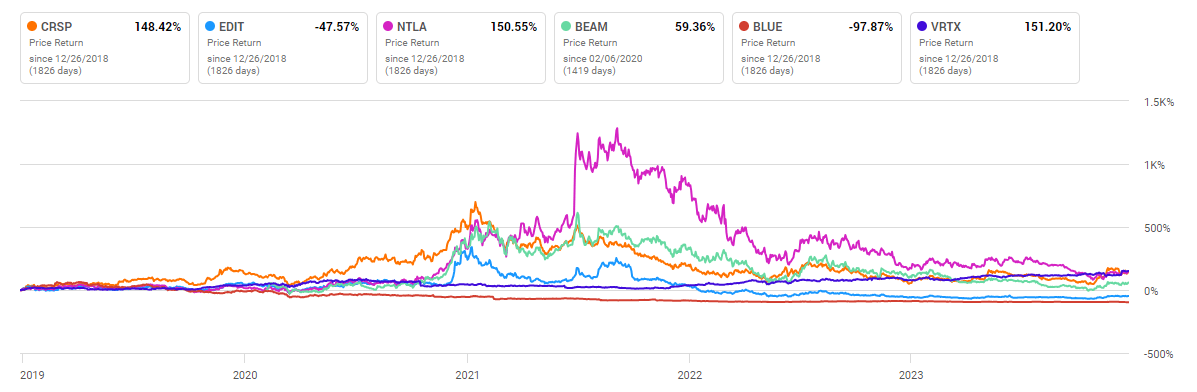

CRISPR AG and Vertex are clear leaders in stock performance, and Intellia, with its promising in-vivo therapies, has also performed well.

{kind=link}

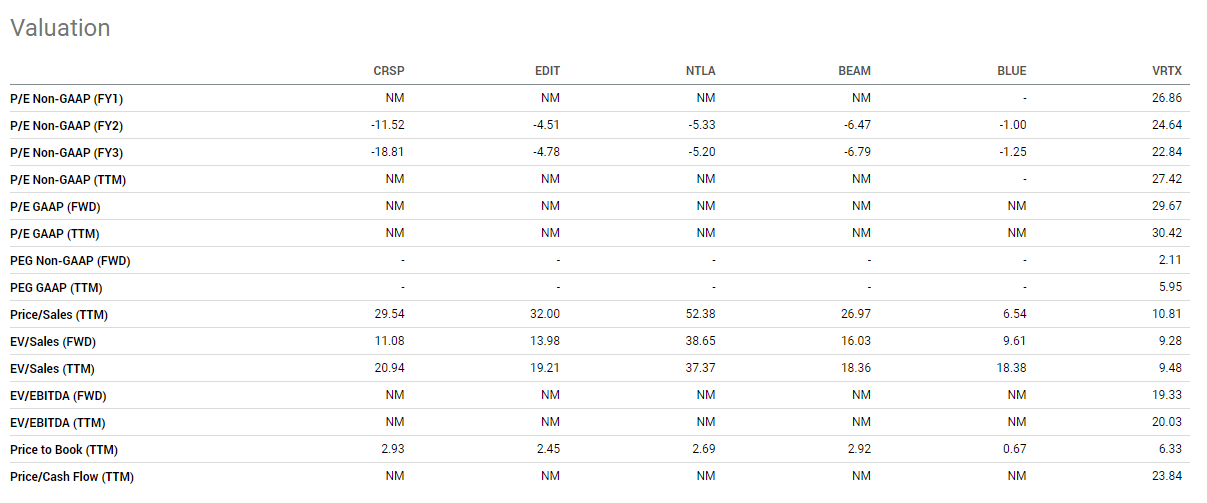

I have previously estimated the total market for sickle cell therapy at around $777 million per year in the medium term, if Editas could capture a quarter of this market through its programs and licensing fees, it would equate to approximately $194 million in revenue. Assuming a highly optimistic 10x sales valuation, this scenario would yield a market capitalization of around $1.9 billion. Considering that Editas currently trades at about $884 million, such an optimistic outcome could potentially see the company's value roughly double in a few years. However, given the high risks involved, the potential reward might not be sufficiently attractive, leading to a decision to remain cautious and stay on the sidelines at this stage.

To justify an investment in this company, a more defined trajectory toward achieving $200 million in annual revenue within the next three years is necessary. Additionally, there's a need to address the dilution risk, which has been a concern since 2019, with the share count increasing by an average of 9% per year.

For a more detailed analysis, consider two scenarios until 2026: a bullish and a bearish one. In the bullish scenario, the company successfully grows its revenues to $200 million per year, with the share count rising to 94 million and achieving a sales multiple close to 10. This figure is aligned with the current multiple of Vertex, a benchmark for an established growth pharmaceutical firm. In contrast, the bearish scenario assumes revenue remains stagnant at the current $25 million, while the share count still increases to 94 million. This dichotomy suggests that, at the current price, the risk of negative returns is disproportionally high.

A reassessment of this investment opportunity might be warranted if there are tangible signs pointing toward the realization of the bullish scenario. Alternatively, a substantial reduction in the current share price could also shift the investment proposition to a more favorable risk-reward balance.

Author's computations

For further details see:

Editas Medicine's Pivot: From CRISPR To Programmable Gene Editing