EDIT - Editas: The Potential Of Gene Editing Technology And The Risks Of A Lackluster Pipeline

Summary

- If EDIT-101 continues to show positive results, it has the potential to become the first-ever gene-editing therapy approved for a genetic disease.

- Editas has established collaborations with leading biopharmaceutical companies, including Bristol Myers Squibb and Juno Therapeutics, to develop innovative gene-editing therapies for a range of diseases.

- Editas Medicine has no approved products in its commercial portfolio. Both EDIT-101 and EDIT-301 are in early to mid-stage development and far from commercialization.

- Editas recently decided to pause enrollment in the BRILLIANCE study for EDIT-101, which has hurt the stock severely.

- Assuming an 11% WACC, a 0% TGR, and using Capital IQ estimates, EDIT's share implies an 80% upside by 2033, according to a DCF valuation.

Editor's note: Seeking Alpha is proud to welcome Adrian Nunez as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Editas Medicine's (EDIT) lead candidate, EDIT-101, is a gene-editing therapy that targets a rare genetic disease called Leber congenital amaurosis 10, which leads to progressive blindness. The interim results of the BRILLIANCE study showed that EDIT-101 was well-tolerated and demonstrated a meaningful improvement in patients' vision, giving investors hope for its potential success.

Despite the positive news from the BRILLIANCE study, Editas' lack of approved products in its commercial portfolio and its heavy reliance on partnerships could hinder the company's ability to generate regular income. This could lead to a prolonged period of no revenue, which will undoubtedly impact its stock price negatively. Additionally, the company's pipeline candidates, EDIT-101 and EDIT-301, are in early to mid-stage development and far from commercialization, leaving them vulnerable to regulatory setbacks or development issues that could harm the company's prospects.

While Editas has a strong cash position with no long-term or short-term debt, the company's collaboration revenues took a hit when AbbVie (ABBV) terminated its strategic alliance with Editas. Finally, assuming an 11% WACC, and 0% TGR, EDIT stock will trade at an 80% upside by 2033, according to my DCF Valuation.

My "hold" recommendation takes all upside and downside risks into consideration.

Company Description

Editas Medicine is a leading biotechnology company focused on developing transformative gene-editing therapies for serious diseases using the revolutionary CRISPR/Cas9 technology. The company is dedicated to discovering, developing, and commercializing gene therapies for patients with rare genetic diseases that have significant unmet medical needs.

January 2023 Company Presentation

Company Presentation

In Editas’ January 2023 Investor Presentation , they updated us on all of their pipeline progress and catalysts. Below, I will analyze key programs as an investor (so keep in mind the picture of their current pipeline). You can learn the definitions of EDIT’s pipeline here: Research and Pipeline | Editas Medicine . Below are my key highlights and takeaways from the presentation:

EDIT-301: EX Vivo Autologous Treatment for Sickle Cell Disease (SCD) :

{kind=link}

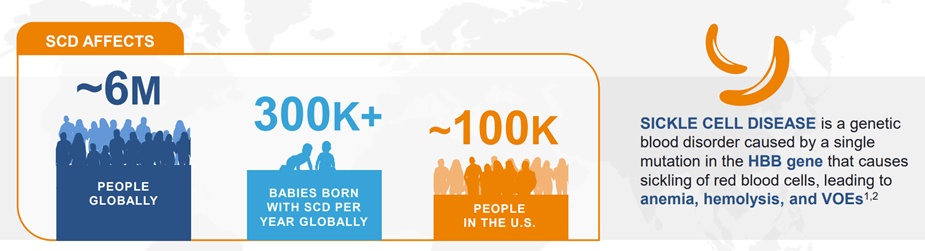

Looking at EDIT’s pipeline, EDIT-301 is one of its most advanced programs, targeting SCD and TDT. Looking at SCD, the company noted that there are ~100 thousand people in the US that are currently suffering from SCD, with ~6 million globally and over 300 thousand babies born with SCD per year. This means that when the product gets commercialized, EDIT will be able to sell to over 6 million people around the world, and with 300 thousand of babies born with SCD annually, EDIT will have a never-ending demand for their SCD treatment.

Another thing to note is that there is no cure for SCD, and there is a high unmet demand, which means this company will have significant benefits when its SCD treatment is commercialized. Right now, the program is in Early-Stage Clinical and still has to pass through Late-Stage, and then it needs to get approved for commercialization.

EDIT-301: EX Vivo Autologous Treatment for Terminal deoxynucleotidyl transferase (TDT):

In Edit’s pipeline, their other top program is TDT, which is a rare genetic disorder that affects the immune system. This disorder affects fewer than 1 in 1 million people worldwide. Currently, there is no cure for TDT, so if EDIT is able to get this program to Late-Stage Clinical and then get approved to commercialize, they would have no competition when it comes to selling their products.

Since TDT is a very rare disorder , the exact estimate of individuals affected by it in the US and globally is not well established. Based on the population of the US, which is roughly 330 million people, this means there may be fewer than 330 individuals in the US with TDT. Globally, the estimated prevalence of TDT would suggest being fewer than 8,000 people worldwide have this disorder. So, not a very high population and demand for a TDT treatment, but would be a nice addition for diversifying EDIT’s product portfolio.

Oncology - T Cells (10 total programs) in IND Enabling phase (pre Early-Stage Clinical):

Company Presentation

As we can see from EDIT’s pipeline above, their third most developed program is the T Cells . The best thing about this program is that Bristol-Myers Squibb fully funds it. T cells are a type of white blood cell that play a crucial role in the immune system. T Cell dysfunction or deficiencies can lead to a variety of disorders, including immunodeficiencies, autoimmune diseases, and certain types of cancer. EDIT’s T Cell program is obviously still well under development, and it is not clear yet how many people the program will target; the goal of the program is to develop gene-edited T Cells for the treatment of various diseases, including cancer and genetic disorders. With this, clinical trials will be necessary to determine the safety and efficacy of the therapy in humans, and regulatory approval will be required before the therapy can be made available to patients.

The same thing goes for EDIT’s second T Cell program, which is still in the pre-clinical stage and is funded by Immatics.

There is a lot of exciting uncertainty around these programs, and I am very excited to see where EDIT can take these programs in the coming years. With that in mind, let’s talk about EDIT’s clinical development objectives for 2023:

Editas Medicine – 2023 Catalysts

{kind=link}

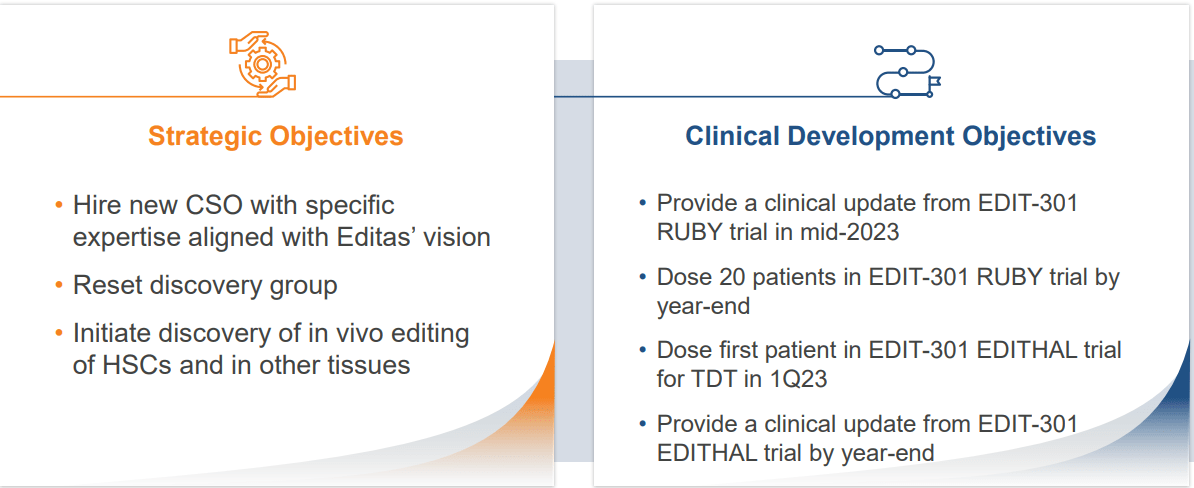

Starting with EDIT’s goal to hire a new Chief Scientific Officer (CSO). This means that EDIT does not currently have someone that is responsible for leading the organization’s research and development efforts. And with EDIT’s objective to reset the discovery group, this, to me, suggests that the company is re-evaluating its research and development plan. This will hopefully allow the company to optimize its R&D investment in the coming years, and I am thrilled to see who they can hire as the new CSO and what their new strategy will be this year.

On EDIT’s “In Vivo HSC Editing”, the program is still in the pre-clinical stage, and the company will initiate discovery for this program in 2023. This program will act as a backbone for the company’s gene editing platforms.

In mid-2023, we are expecting clinical data updates for EDIT-301. As an investor, this means that if we do not get updated on EDIT’s RUBY trial by the end of 3Q in 2023, the share price will be harmed. In contrast, if they update us before their 3Q, this will likely lead to EDIT’s share price rising.

Next, EDIT is planning on dosing 20 patients for their RUBY trial by year-end. This will be a massive update to keep an eye on throughout this year, as this trial will act as a true testament to the progress in EDIT-301. Same goes for the company’s objective to dose their first patient in their TDT treatment. If these trials go well, this will likely move the company’s EDIT-301 programs closer to the Late-Stage Clinical phase, which will be a huge and positive impact on the company’s sentiment going forward. If these trials go south, the company’s share price will follow.

Same thesis goes for the company’s clinical update from EDIT-301 EDITHAL trial by year-end. The company has set critical objectives to keep an eye on for this year, and the results of these clinical and CSO updates will give investors a much better idea of EDIT’s potential in the coming years. With this, there are never any guarantees, and I believe that investing in this company today comes with all the risks that come with clinical data failures (as I mentioned above).

My Investment Approach

I look for undervalued companies with significant potential for the coming years. With that, I also love riskier investments as they provide greater rewards in the long term. Therefore, I aim to hold an investment for anywhere from 3-10 years. I will go through Editas' valuation, January 2023 presentation and catalysts, risks, financial performance, and their intrinsic value for 2033 using a DCF.

Investment Thesis – Reasons To Buy

Editas' lead pipeline candidate; EDIT-101, is a gene-editing therapy designed to treat Leber congenital amaurosis 10 (LCA10), a rare genetic disease that leads to progressive blindness. LCA10 is caused by a mutation in the CEP290 gene, which codes for a protein essential for the health and function of photoreceptor cells in the retina. Currently, there are no approved treatments for LCA10 , and patients have no option but to gradually lose their vision. EDIT-101 uses CRISPR/Cas9 gene-editing technology to precisely edit the mutated CEP290 gene in the patient's retinal cells, restoring the normal function of the protein and thereby halting the progression of the disease.

Editas is currently conducting a Phase 1/2 clinical trial; called BRILLIANCE , to evaluate the safety, tolerability, and efficacy of EDIT-101 in patients with LCA10. In September 2021, the company announced promising interim results from the study, which showed that the treatment was well-tolerated and demonstrated a meaningful improvement in patients' vision. If EDIT-101 continues to show positive results, it has the potential to become the first-ever gene-editing therapy approved for a genetic disease, and a life-changing treatment for patients with LCA10.

Editas has a deep pipeline of gene-editing therapies for a range of genetic diseases; The company is developing EDIT-102 , a CRISPR/Cas9 therapy for treating Usher Syndrome Type 2A, a rare genetic disorder that causes both vision and hearing loss. Editas has completed IND-enabling studies for EDIT-102 and plans to initiate clinical trials in 2022. The company is also developing EDIT-301, a CRISPR/Cas12a therapy for treating sickle cell disease and transfusion-dependent beta-thalassemia. In December 2022, the company announced positive preliminary results from the Phase 1/2 clinical trial of EDIT-301 in sickle cell disease patients. Editas is also advancing a pipeline of gene-edited natural killer (NK) cell therapies for solid tumors.

Editas has established collaborations with leading biopharmaceutical companies; including Bristol Myers Squibb and Juno Therapeutics , to develop innovative gene-editing therapies for a range of diseases. The company's partnership with Juno Therapeutics has provided it with access to cutting-edge gene-editing technology, including CRISPR/Cas9, for developing engineered T-cell therapies for cancer and autoimmune diseases. Editas has also entered into research collaborations and licensing agreements with other biotechnology companies to develop new gene therapies.

Editas has a strong cash position; with cash, cash equivalents, and marketable securities worth $420 million as of September 30, 2022. The company has no long-term or short-term debt, which provides it with the flexibility to invest in its pipeline and pursue new business opportunities. Editas is committed to creating long-term value for its shareholders by advancing its pipeline, expanding its collaborations, and developing innovative gene-editing therapies that have the potential to transform the lives of patients with rare genetic diseases.

In brief, Editas Medicine is a promising investment opportunity for investors seeking exposure to the rapidly growing gene-editing space, with a deep pipeline of innovative therapies and established collaborations with leading biopharmaceutical companies.

Investment Thesis – Reasons To Sell

Lack of Marketed Products: Editas Medicine has no approved products in its commercial portfolio. Without a source of generating regular income, the company's potential sales could suffer in case partnerships do not materialize. Furthermore, the majority of Editas' pipeline candidates are in the early stage or pre-clinical development. There are chances that it will not have a product in the market for years. This lack of commercialization could lead to a prolonged period of no revenue, which will undoubtedly impact its stock price negatively.

Early-Stage Pipeline: Both EDIT-101 and EDIT-301 are in early to mid-stage development and far from commercialization. Development and regulatory setbacks for the pipeline candidates will be a major disappointment for the company, leaving an adverse impact on its shares.

Pipeline Setback: Editas recently decided to pause enrollment in the BRILLIANCE study for EDIT-101, which has hurt the stock severely. The company is actively seeking a collaboration partner to continue the further development of EDIT-101. Such a setback does not bode well for the company.

AbbVie Deal Termination: In August 2020, Editas and Allergan ( now part of AbbVie ) terminated their strategic alliance, which was signed in March 2017. The companies also discontinued the profit-sharing arrangement to split U.S. profit and losses of EDIT-101, originally licensed to Allergan under the same agreement. AbbVie returned the development and commercialization rights of ocular medicines, including EDIT-101, back to Editas. Owing to this, Editas’ collaboration revenues took a nosedive, which does not bode well for the company.

In brief, Editas Medicine's lack of commercialized products, early-stage pipeline, pipeline setback, and termination of a strategic alliance with AbbVie have all hurt the stock's performance. Therefore, I believe that investors should be cautious in shares of Editas Medicine as its potential growth and revenue sources are not guaranteed, and the risks and uncertainties associated with its pipeline candidates outweigh the potential gains.

Editas Medicine - Current Valuation

Editas reported $25.6 million in sales for 2022; with -$197.8 million EBITDA; and -$2.93 diluted EPS. At the time of writing, they are trading at a $682.7 million market cap; a $225.5 million Enterprise Value; and a $10.15 price per share. This means that we can only use EV/Sales to value this company since it has negative earnings. Their EV/Sales comes down to 8.8x, and that is not good in comparison to their sector average of 4.2x.

Editas is also trading at a 1.65x P/B. This to me, does not mean anything because a 1.65x P/B ratio at this stage is neither good nor bad.

The problem with looking at Editas' valuation statistics is that they do not mean anything. This is because Editas is in a pre-clinical phase in its business cycle.

So what does this mean? We are at a higher risk because it is uncertain as to how this market is valuing this company today and where it could value this company in the future.

Another way to look at EDIT’s valuation is with their current cash and fully diluted shares:

{kind=link}

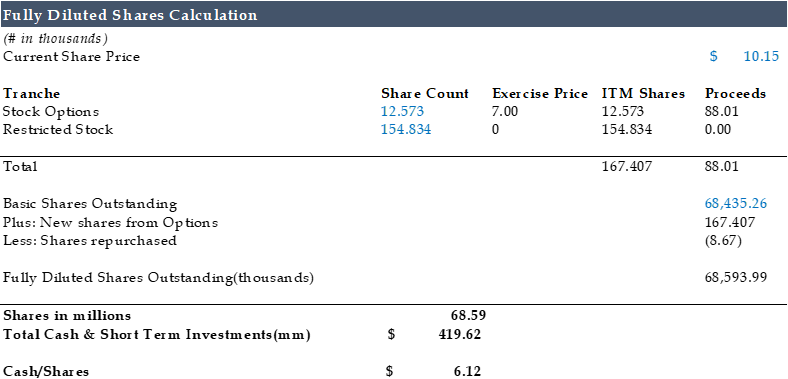

In EDIT’s latest filing, they reported 68.4 million basic shares outstanding, with .17 million In The Money (ITM) Shares. With $88 in proceeds from the stock options, EDIT has 68.59 million fully diluted shares outstanding. EDIT also reported $419.6 million in cash & short-term investments. This means that EDIT has $6.12 in cash & short-term investments per share. With the stock trading at $10.15, I think this reduces a decent amount of the risks that come with buying this company at today’s prices. This is because 60% of EDIT’s equity value is cash and short-term investments.

In brief, EDIT’s valuation metrics are uncertain due to the fact that Editas is still under development and therefore has negative earnings. As for their cash-to-equity, I think this is something moderately attractive, but it does not paint a clear picture of what the market is valuing this company today.

Discounted Cash Flows Analysis 2023-2033

Disclaimer: I used the median estimates from Capital IQ to forecast Editas Revenues, EBIT, taxes, Capex, D&A, and FCF. I assumed an 11.00% WACC and a 0.00% long-term growth rate.

Discounted Cash Flow (Author's Data)

{kind=link}

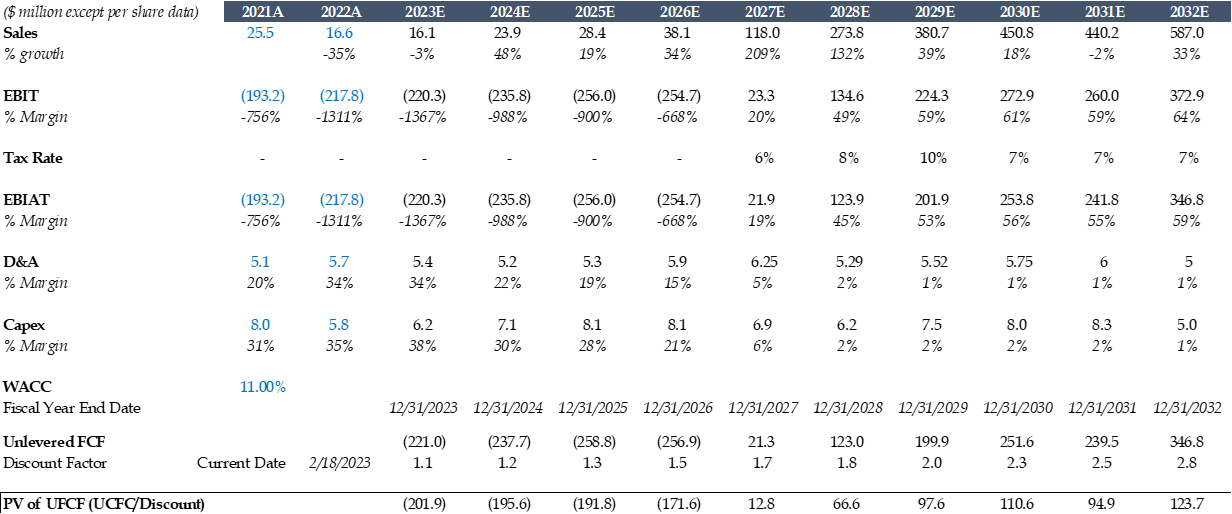

Taking a look at the sales forecasts, the street is pricing in that Editas commercializes its EDIT-303 treatments by 2027, hence the 209% sales growth in 2027. This means that we still have around 4-5 years of clinical data updates until we can see how efficient the management team is when it comes to selling their treatments for SCD and TDT. By 2032, the street prices in $587 million in total sales. This shows a consistent sales increase from the year that Editas commercializes its first pipeline programs. The operating (EBIT) margin in 2032 is roughly 50% which shows significant margin expansion while maintaining significant investments in research and development.

To calculate the UFCF, I used: EBIT*(1-tax rate)+D&A-Capex. Where it forecasts negative free cash flows from 2023 to 2026 as the company continues to develop its pipeline programs. From 2027 to 2032, UFCF is positive, which allows the company to continue to reinvest in the business. The same thing goes for the present value of free cash flows. It is very important to discount the time value of money when forecasting the future value of free cash flow. A dollar today is worth more than a dollar tomorrow.

With this in mind, I used the growth in perpetuity method to arrive at EDIT’s implied share price for 2032:

{kind=link}

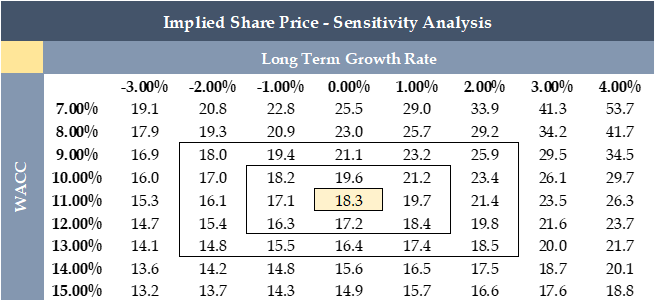

Assuming an 11.00% WACC, and a 0.00% growth rate (same as JP Morgan), EDIT’s implied share price is $18.30 or an 80.25% price appreciation. This is a great appreciation potential. However, this DCF forecasts throughout a decade, and that leaves room for numerous case scenarios. On the sensitivity analysis, we have scenarios with the price ranging from $13.2 to $53.7, where the WACC ranges from 7% to 15%; and the growth rate ranges from -3% to 4%. The growth rate is purely assumptions, and you can base your view on this company with all of these different scenarios.

As for me, a 0.00% growth rate seems appropriate as there are a lot of risks that come with investing in Early-Stage companies. This is because there is a lot of uncertainty with the progress of the pipeline. I believe it is still early to get excited and buy additional shares of this company. Another thing that would improve my sentiment for this company would be the addition of new therapies or partnerships. Diversification is very valuable to me when investing in a biotechnology or pharmaceutical company.

The Last Word

The company's lead candidate, EDIT-101, has demonstrated promising interim results in its ongoing clinical trial for treating Leber congenital amaurosis 10. However, Editas faces significant risks, such as the lack of approved products in its commercial portfolio, a prolonged period of no revenue, and the recent termination of its collaboration with AbbVie. While the company's Q3 2022 earnings beat estimates, its revenue decreased significantly year-over-year. Investors need to weigh these risks against the potential rewards of Editas' pipeline, which has several candidates in early to mid-stage development. Editas' commitment to creating long-term value for its shareholders and its strong cash position with no long-term or short-term debt provides it with the flexibility to invest in its pipeline and pursue new business opportunities. Despite the challenges, I believe Editas is developing a robust pipeline with innovative gene-editing therapies that have the potential to transform the lives of patients with rare genetic diseases, making it a company to watch in the biotech space.

In one sentence: Editas Medicine is poised for long-term growth but lacks clarity for short- to mid-term opportunities.

For further details see:

Editas: The Potential Of Gene Editing Technology And The Risks Of A Lackluster Pipeline