EDPFY - EDP - Energias de Portugal: Undervalued Electric Utility Capitalizing On The Green Transition

2023-08-20 00:50:09 ET

Summary

- EDP is a leading Portuguese electric utility company with an attractive earnings and dividends growth profile.

- The company is investing heavily in the green transition, aiming to add 4.5 GW/year of renewable capacity and reach a total of 50 GW of RES capacity by 2030.

- As a result of temporary share price weakness caused by concerns over leverage and RES earnings, an appealing buying opportunity has emerged.

We present our note on EDP – Energias de Portugal (EDPFY), Portugal’s leading electric utility company. EDP offers an attractive earnings and dividends growth profile, combined with value crystallization through asset rotations in hydro, thermal, and renewables. Concerns over rising leverage and downward earnings revisions in renewables have put pressure on the share price, creating an appealing buying opportunity. We will provide an overview of the business, an analysis of asset rotations and the leverage situation, as well as our valuation and investment recommendation.

Introduction To EDP

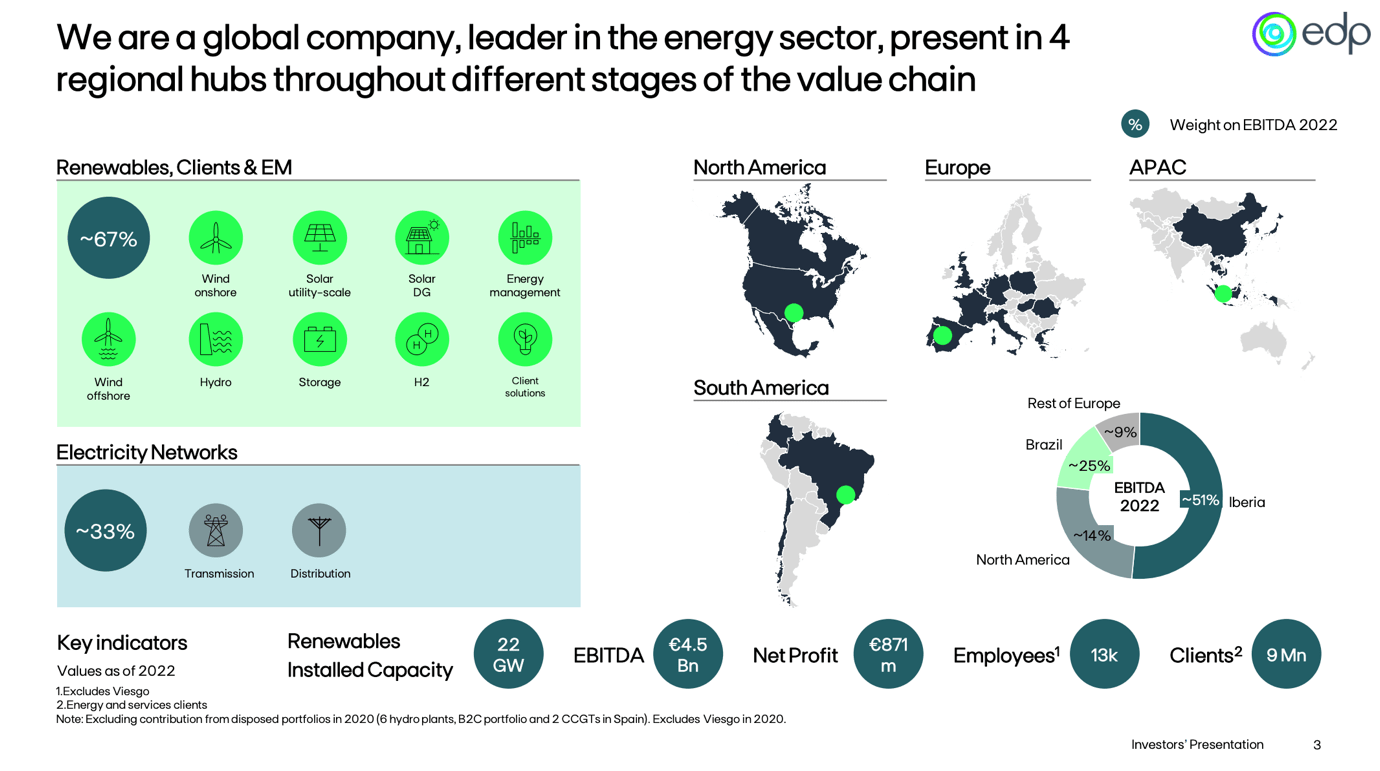

EDP is a Portuguese electric utility company headquartered in Lisbon. It is present in 4 regional hubs in Europe, North America, South America, and APAC, in different stages in the value chain. Renewables, Clients, and EM including wind, solar, hydro, storage, hydrogen, and client solutions generate 67% of EBITDA, while Electricity Network which includes transmission and distribution generates 33% of group EBITDA. EDP owns a 71% stake in EDPR (EDP Renovaveis) and is in the process of acquiring minorities in EDP Brazil. The company is listed on the Euronext Lisbon and has a current market capitalization of €17.3 billion.

{kind=link}

Investing In The Green Transition

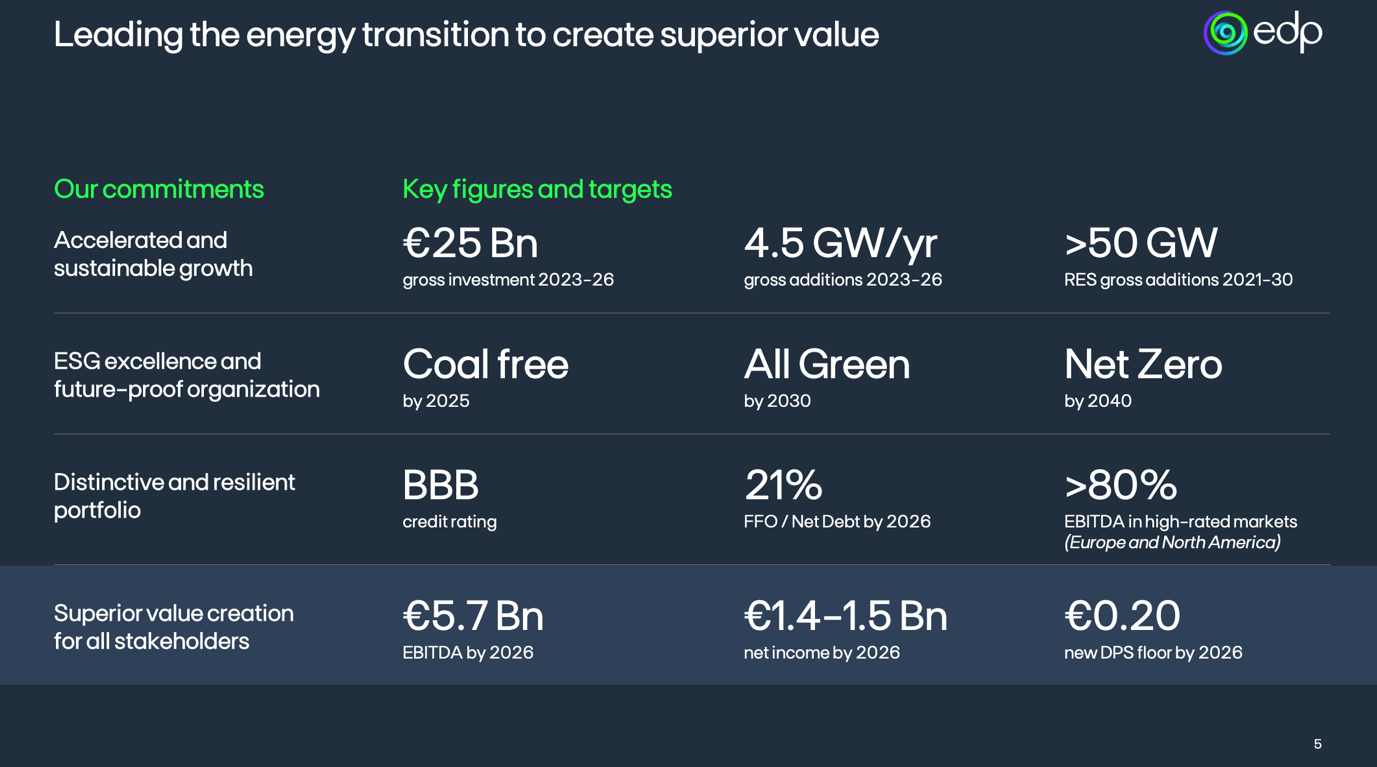

The company is positioned as a top global green transition player. EDP currently has ca. 22 GW of installed renewable capacity and it is aiming for 4.5 GW/year of gross additions between 2023 and 2026, investing €21 billion in this timeframe, out of which 40% will be invested in onshore wind, 40% in utility-scale solar, and the rest in hydrogen, storage, and solar distributed generation. Until 2030, EDP aims to be fully green and to add a total of 50 GW of RES capacity.

Moreover, by FY2026 EDP aims to invest ca. €3.2 billion in Networks in Portugal, Spain, and Brazil, reaching a regulated asset base level of €6.6 billion, with high visibility and considerable inflation protection.

50% of the total investment plan of €25 billion is secured while the rest is in the pipeline. The company targets an EBITDA of €5.7 billion and net profit of €1.4-1.5 billion in FY2026 vs. an EBITDA of €4.5 billion and net profit €871 million in FY2023 respectively. By FY2026, 80% of EBITDA should be achieved in high-rated markets i.e., Europe and North America. EDP remains committed to a disciplined investment framework oriented towards strong shareholder returns through the cycle. This is reflected on achieved targets of IRR being 200 bps higher than WACC or 1.4x higher.

{kind=link}

Q2 Results

H1 results were solid with EBITDA and Net Income prints beating consensus estimates. Meanwhile, guidance on EBITDA of €5 billion and net income of €1.1 billion for this year was upheld. The results were impacted by increased hydro production and lower sourcing costs as well as negatively affected by lower load factors in North American wind and higher taxes in two European countries: Poland and Romania. Moreover, EDP announced it has achieved 95% ownership of EDP Brazil and is moving forward with the squeeze-out. In addition, two rotation deals have been announced with 257 MW of assets getting sold in Spain and 301 MW of assets in Poland , at an average of ca. €1.7 million per MW, implying significant value creation.

Asset Rotation

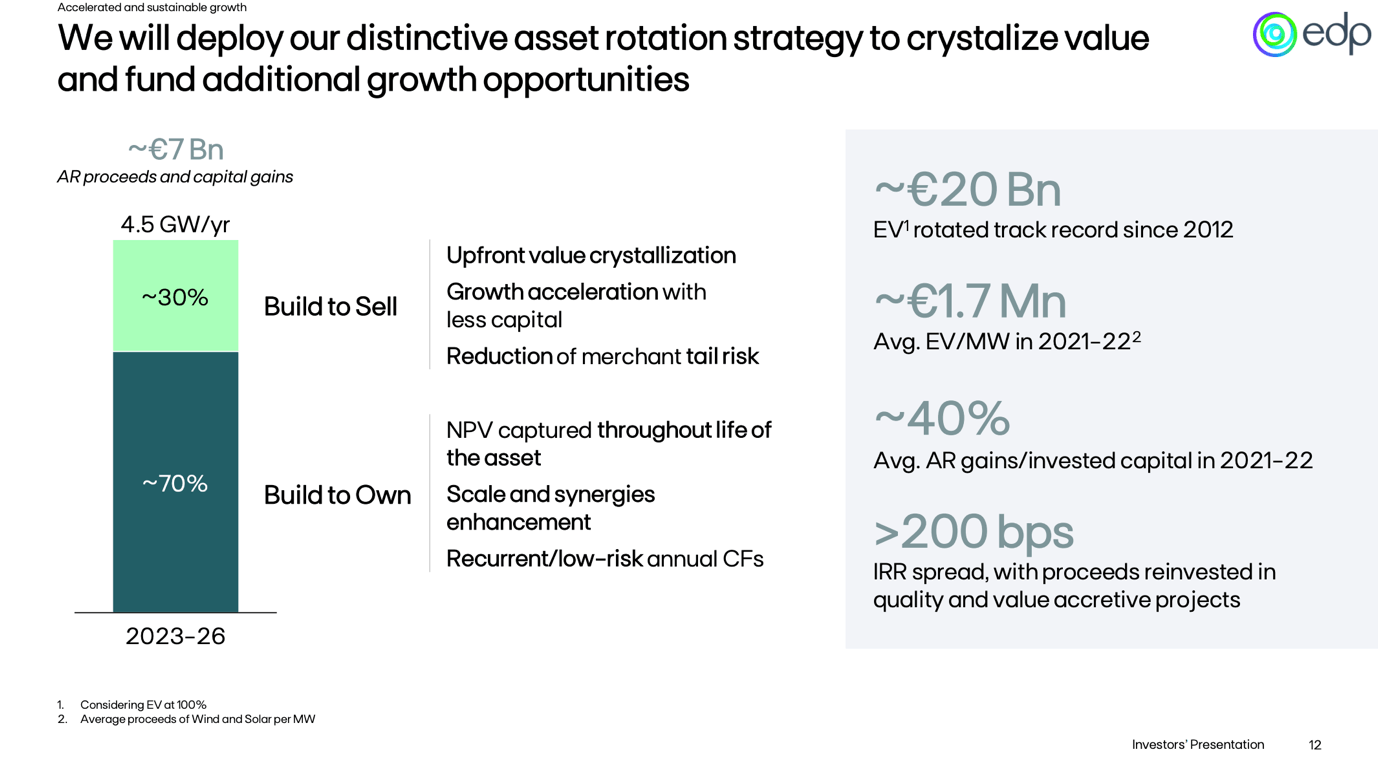

EDP additionally creates value for shareholders through asset rotations in various areas. Considering at 100% of enterprise value, EDP has rotated ca. €20 billion of assets since 2012. The average enterprise value per MW rotated in 2021 and 2022 has been €1.7 million, with 40% gains over invested capital, and an IRR 200 basis points above the respective WACC. Out of the 4.5 GW yearly capacity additions built until 2026, 30% i.e., 1.5 GW per year will be built to sell, providing upfront value crystallization and less capital-intensive growth. We prefer this mixed approach in comparison to a 100% build-to-own approach.

{kind=link}

Share Price Weakness

Over the last couple of months, the share price has been weak as a result of market concerns over renewables earnings downgrades and leverage. The negative revisions are mostly related to one-offs hence we find the impact disproportionate and not justified. Moreover, given the net profit guidance of €1.1 billion for the FY, we believe there is some upside that is not priced due to the EDP Brazil minorities squeeze-out and the current state of hydro reservoirs. In addition, we believe concerns over net debt should ease as EDP has announced it will be securitizing some receivables and disposing of some assets in Brazil, pushing leverage down to around €15 billion as per the consensus. Moreover, as new RES assets are commissioned and start generating cash flow, EDP should achieve a 21% FFO / Net Debt Ratio by FY2026, rapidly delivering.

Investment Thesis And Valuation

We forecast an EBITDA of €5.7 billion in FY2026e in line with the company guidance and sell-side consensus, and €1.4 billion of net profit in FY2026e at the lower end of the company’s guidance. The long-term sector average PE ratio has hovered around 14x, but this does not take into account the higher EPS growth. We believe there should be a sizeable premium for the growth and quality of the RES portfolio, for the value creation through asset rotation, as well as the solid fundamentals of the networks business. We apply a target forward PE ratio of 18x to reflect the premium, arriving at a target market capitalization in FY2025 of €25.2 billion. Discounting at a cost of equity of 8% we arrive at a target market capitalization of €21.6 billion, implying 23% upside, and a share price of €5.1 per share, or $5.6 per share. We would also like to point out that the company has guided to a dividend floor of €0.20 per share by 2026, which implies a nearly 5% yield at current share price levels.

Risks

Downside risks include but are not limited to an increase in bond yields especially given the long duration of the portfolio, lower electricity prices, hedging risks, regulatory risk in networks, higher than expected taxation and/or windfall taxes, permitting delays in renewables, operational issues leading to lower than expected capacity additions, value destructive M&A, suboptimal allocation of capital in RES, etc.

Conclusion

We recommend building a long position in EDP shares, given the earnings growth, the appealing valuation as a result of temporary weaknesses, portfolio quality and optimization, and growing capital returns. We think EDP has one of the most attractive risk/reward profiles in the sector.

For further details see:

EDP - Energias de Portugal: Undervalued Electric Utility Capitalizing On The Green Transition