EW - Edward Lifesciences: Still Not A Buy But Getting Closer

2024-01-09 19:06:00 ET

Summary

- Edward Lifesciences is now trading for lower valuation multiples than in the last few quarters.

- The company is continuing to report double-digit growth rates and management is expecting the same growth rates for the years to come.

- The company can now be seen as fairly valued, but it is not yet a bargain.

One of the stocks I was very cautious about in the last few years although we are talking about a great business was Edward Lifesciences ( EW ). In my last three articles I was always rather cautious, rated the stock as a “Hold” and pointed towards the high valuation. I argued that the company is priced for perfection and that high growth rates are already priced in.

In my last article published in June 2023 I stated that Edward Lifesciences is slowly approaching its intrinsic value and in the last six months the stock declined further and lost another 15% (compared to the publication of the article). Right now, the stock is trading 44% below its all-time high (and recently it declined even 53%, which is the steepest decline in Edward Lifesciences’ history).

After losing half of its value, it might seem like Edward Lifesciences is already cheap and one might be tempted to buy the dip already. In my last article I also finished with the following conclusion:

I would still see Edwards Lifesciences as a "Hold". In retrospect one might have purchased EW for $70 back in October or November 2022, but I would still expect the stock to reach at least that level again (and maybe decline even lower). Edwards Lifesciences remains on my watchlist as it is a great business, but still not a great investment.

And in the meantime the stock declined even lower and reached $60 already, so we have to ask the question if buying Edward Lifesciences now is a good idea. To answer this question, we can start by looking at the valuation multiples the stock is currently trading for.

Valuation Multiples

In the last few years, I mostly criticized the extremely high valuation multiples Edward Lifesciences was trading for. While I always acknowledged that we are dealing with a great business, I did not see the stock as a great investment as it was trading for 50-, 60- or 70-times earnings and free cash flow in the past.

When looking at the valuation multiples we can see that the picture improved a little bit. Right now, Edward Lifesciences is trading only for 31 times earnings, which is among the lowest valuation multiples in the last six to seven years and below the 10-year average of 41.37. But we should not ignore that 30 times earnings is still not a low valuation multiple, but one that might be justified for companies being able to grow with a high pace and high levels of consistency.

However, when looking at the price-free-cash-flow ratio, Edward Lifesciences is still trading for a valuation multiple of 57, which is not only above the 10-year average of 47.83, but an extremely high valuation multiple.

At this point we can conclude that Edward Lifesciences is much cheaper than in the last two or three years, but it doesn’t answer the question yet if it is a good investment. We also must look at the fundamental business as there might be reasons for the declining stock price.

Results

Often, a declining stock price is going hand in hand with lower growth rates. But Edward Lifesciences is still growing with a solid pace and current growth rates are in line (or even above) the long-term average. Since the early 2000s, Edward Lifesciences is growing its revenue with about 10% annually. And earnings per share are growing with an even higher pace, although the numbers are fluctuating more wildly.

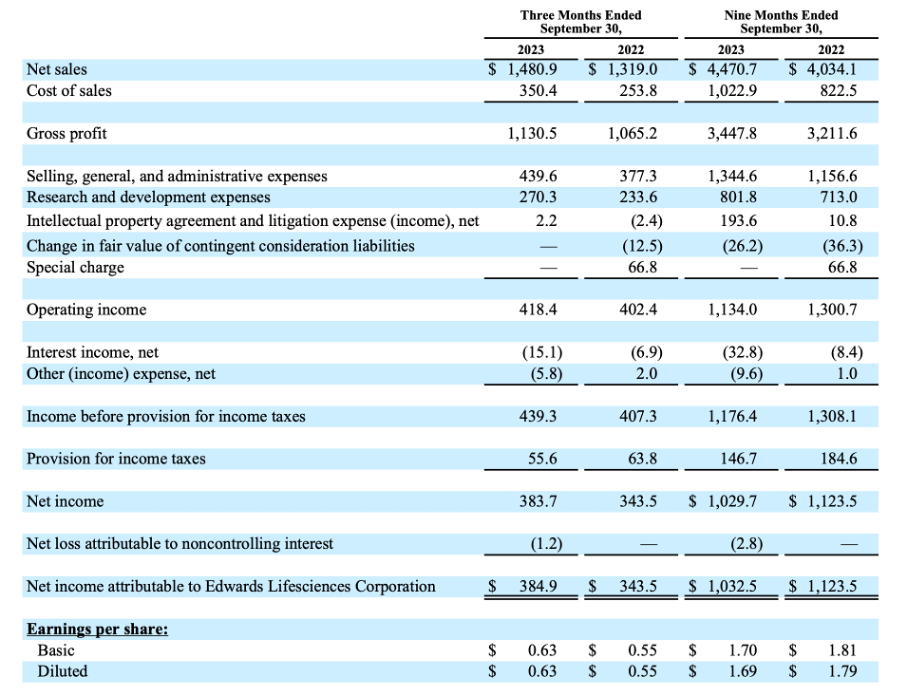

And the results in the third quarter are showing a similar picture as in the last few years. Sales grew 12.3% year-over-year from $1,319 million in Q3/22 to $1,480.9 million in Q3/23. Operating income increased from $402.4 million in the same quarter last year to $418.4 million this quarter – resulting in 4.0% year-over-year growth. And finally, diluted earnings per share increased 14.5% YoY from $0.55 in Q3/22 to $0.63 in Q3/23. And free cash flow – one of the most important metrics – increased from $250 million in the same quarter last year to $356 million this quarter – resulting in 42.4% YoY growth.

{kind=link}

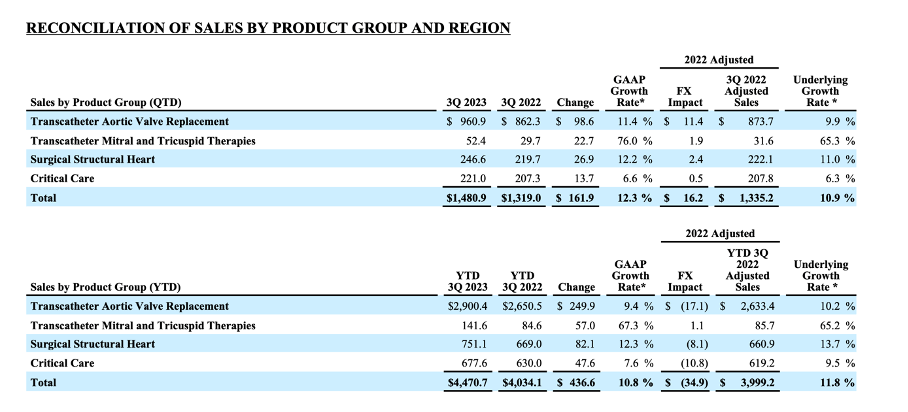

When looking at the four different product categories all are contributing to growth. Nevertheless, Transcatheter Aortic Value Replacement ( TAVR ) is still the most important segment and generated $960.9 million in revenue in Q3/23. This is resulting in 11.4% YoY growth for the segment. The second most important segment – at least from a revenue perspective is Surgical Structural Hearth, which generated $246.6 million in revenue. This is resulting in 12.2% year-over-year growth for the segment. However, the highest growth rate was reported by the Transcatheter Mitral and Tricuspid Therapies (TMTT) segment, which generated only $52.4 million but grew 76.0% YoY.

{kind=link}

Critical Care Spin-Off

You might have realized that I left out the fourth segment – Critical Care. This segment generated $221.0 million in revenue and could grow 6.6% year-over-year. In the recent past, management announced it is planning to spin off its critical care business, but the separation of the business is not expected before the start of 2025. Therefore, this won’t have any impact on 2024 results, and we can expect more information about the industry-leading company Edward Lifesciences wants to create in mid-2024.

During the last earnings call , management commented about the Critical Care business and its potential in the years ahead:

In Critical Care, third quarter sales of $221 million increased 6%, driven by a smart recovery portfolio, with strong adoption of our Acumen IQ sensors, equipped with the high potential prediction index algorithm. We remain confident in our pipeline of critical care innovation, as we continue to shift our focus to smart recovery technologies, designed to help clinicians make better decision and get patient home to their family faster.

Growth

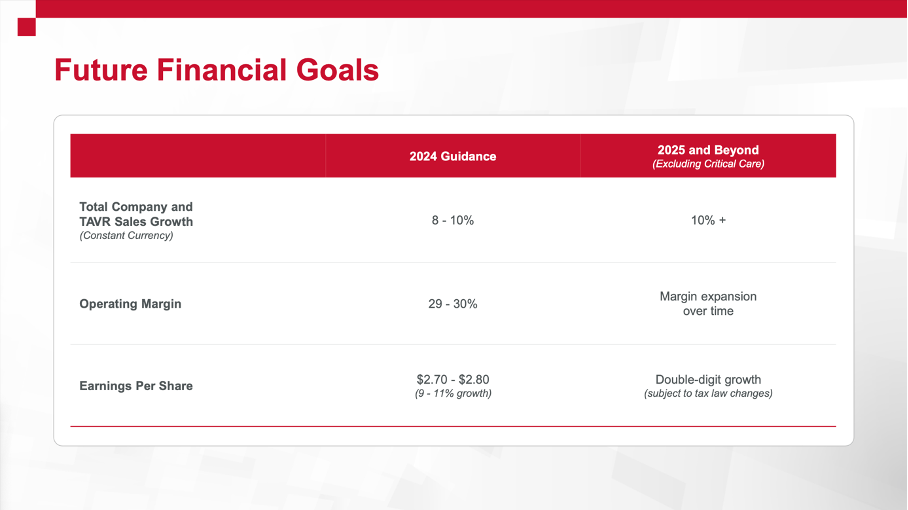

We mentioned above that Edward Lifesciences is continuing to grow with a high pace and is still reporting mostly double-digit growth rates. But the important question at this point is: Can Edward Lifesciences also continue growing with a high pace in the years to come. And when looking at the company’s guidance we can be optimistic for 2024.

{kind=link}

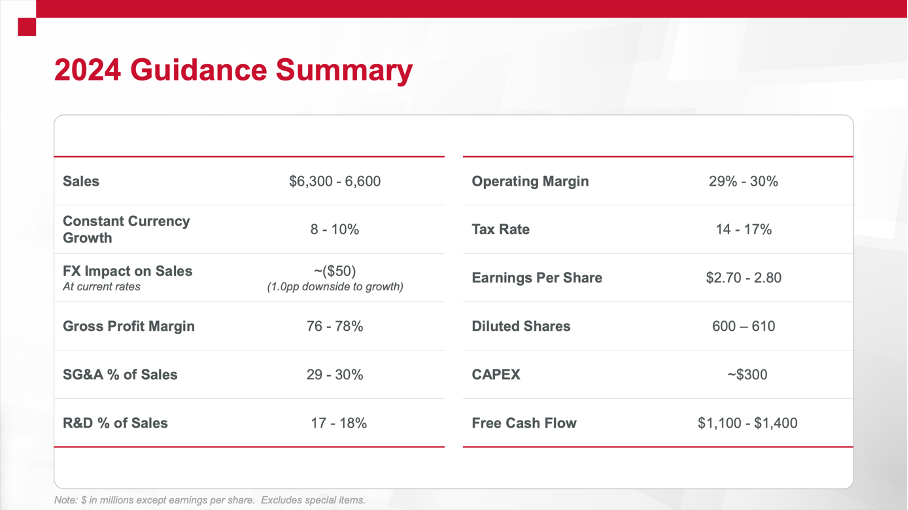

Not only is Edward Lifesciences expecting sales to grow about 8% to 10% in constant currencies, it is expecting earnings per share to be in the range of $2.70 to $2.80. And especially free cash flow will recover again and be in a range between $1,100 and $1,400. This is by the way bringing the P/FCF ratio down to 35 (when taking the midpoint of the guidance and using the current stock price).

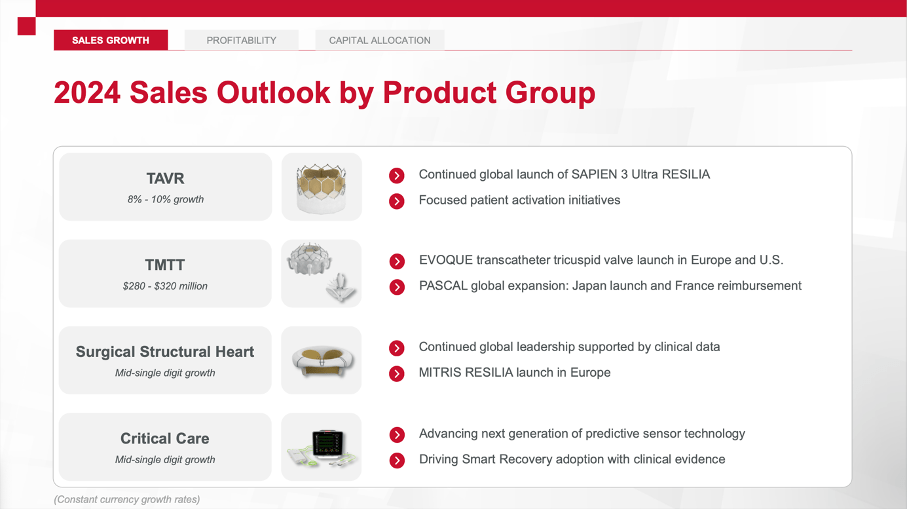

When looking at the different segments (or different product groups) all four segments will continue to contribute to growth. While Critical Care and Surgical Structural Heart are expected to grow in the mid-single digits in 2024, the other two segments – TAVR and TMTT – will be the drivers of growth. TAVR will grow between 8% and 10% but as it is the biggest segment it will continue a huge part to overall growth. And sales for the TMTT segment are expected to be between $280 million and $320 million. Compared to expected sales of $180 million to $200 million in 2023, this is resulting in 40% to almost 80% growth year-over-year.

{kind=link}

Recently the company achieved several milestones for its TMTT segment that should drive growth in the coming year. During the last earnings call, management stated:

In the last several weeks, we achieved four important milestones in support of our commitment to patient-focused innovation. First, CE Mark approval for EVOQUE tricuspid valve replacement system. Second, CE Mark approval for the MITRIS RESILIA surgical mitral valve. Third, PASCAL Precision approval in Japan. Finally, the competition of the enrollment in the first-ever pivotal trial for any transfemoral mitral replacement therapy the ENCIRCLE trial for SAPIEN M3.

But management is not only optimistic for 2024 but also for the years following. Overall, the company is expecting sales in constant currency to grow at least 10% annually and in combination with an expanding operating margin over time, earnings per share should grow at least in the double digits.

{kind=link}

In my last article I already wrote about the growth potential of Edward Lifesciences in the years to come:

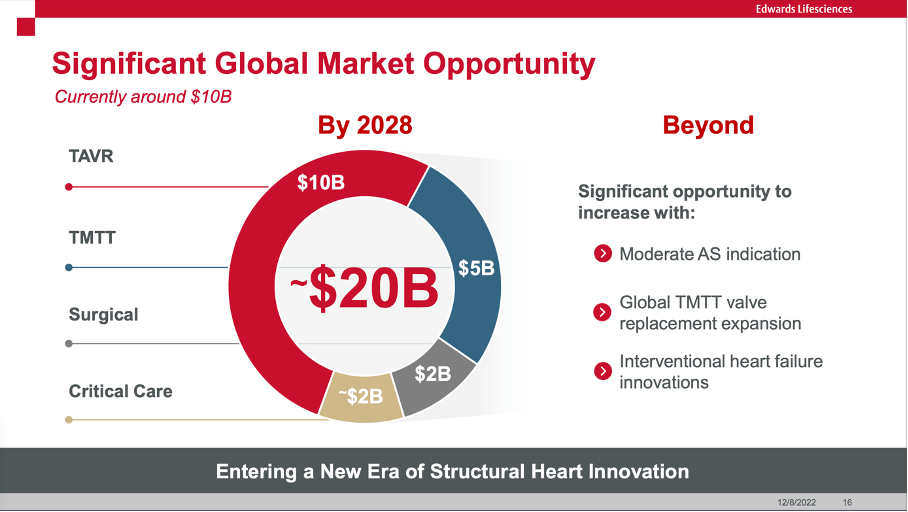

The company's global market opportunity is currently around $10 billion and will double in the next five years to reach a TAM around $20 billion in 2028. Especially TAVR - the most important market for Edwards Lifesciences (65% of its revenue in fiscal 2022) - will reach a global market size of $10 billion.

{kind=link}

And during the last earnings call, the company reaffirmed it is still expecting the global TAVR opportunity to exceed $10 billion by 2028 and this is not only the most important market for Edward Lifesciences, but also a market in which it has a dominant position.

Intrinsic Value Calculation

I already mentioned above that Edward Lifesciences is now trading for a lower P/E ratio, and I also mentioned that using the expected free cash flow for 2024 leads to a more reasonable forward P/FCF ratio for Edward Lifesciences. And we can draw the conclusion that Edward Lifesciences seems to be cheaper than in the last few years and is most likely a better investment than in 2022 or 2021. Nevertheless, we still don’t know if we can see the stock as undervalued or not.

To determine a fair, intrinsic value for the stock we can use a discount cash flow calculation. As always, we assume a 10% discount rate and calculate with 609.5 million outstanding shares. As basis for our calculation and the estimated free cash flow for 2024, we can take the midpoint of the company’s own guidance ($1,250 million). And for the next ten years, we can assume 10% growth (as management is expecting at least double-digit bottom-line growth) followed by 6% growth till perpetuity. When using these assumptions, we get an intrinsic value of $68.07, and the stock is almost fairly valued.

At this point we can certainly make the argument that Edward Lifesciences might also grow with a higher pace in the years to come. Although analysts are expecting “only” a CAGR of 10.38% in the next six years, in the last ten years operating income grew with a CAGR of 15.92% and earnings per share increased with a CAGR of 19.43%. And it seems at least reasonable to expect similar growth rates for the years to come. And although the argument that growth slows down over time when a business gets more mature seems reasonable, we can also argue for Edward Lifesciences being able to grow at a similar pace (it has now for quite some time). Additionally, Edward Lifesciences will most likely continue to buy back shares (although this is not so effective due to the high share price) and will focus on improving its margins – like it has done in the past.

{kind=link}

Despite these arguments for an even higher growth rate, I will stick to 10% growth annually. We should also not ignore the risk for a recession in the years to come – and despite Edward Lifesciences being rather recession-resilient we might see contracting margins and lower free cash flow for several quarters (or maybe even a few years).

Conclusion

At this point I would argue that Edward Lifesciences is still a “Hold” as it seems to be trading more or less for its intrinsic value. I would neither describe Edward Lifesciences as overvalued nor as bargain at this point but I don’t know if one should already invest (I won’t).

Keeping in mind that Edward Lifesciences can be seen as a recession-resilient business one might open a position at this point. But we should be prepared for even lower stock prices – or for Edward Lifesciences trading at similar prices for quite some time. We can only make the case for Edward Lifesciences being fairly valued – I don’t see any reasons why the stock should trade much higher in the next few quarters.

For further details see:

Edward Lifesciences: Still Not A Buy But Getting Closer