BSX - Edwards Lifesciences: Rising Dominance In Structural Heart Disease

2023-08-21 07:01:11 ET

Summary

- Edwards Lifesciences is the global leader in medical devices for structural heart disease and critical care monitoring.

- Their Transcatheter Aortic Valve Replacement technology dominates the market and is expected to continue its leading position.

- EW's growth is driven by the under-penetrated TAVR market and advancements in surgical structural heart and critical care therapies.

Edwards Lifesciences ( EW ) is the global leader in medical devices for structural heart disease and critical care monitoring. Their products are used to replace or repair a patient's diseased or defective heart valve. The Edwards SAPIEN family of valves is the best transcatheter aortic valve replacement product on the market.

Edwards's Transcatheter Aortic Valve Replacement ((TAVR)) has dominated the market along with Medtronic (MDT) for a long time, and I expect Edwards' leading market position to continue in the near future. Edwards has heavily invested in R&D, creating a deep "moat" in the structural heart disease industry. I believe Edwards can become the dominant player in the structural heart disease medical device field.

Business Overview

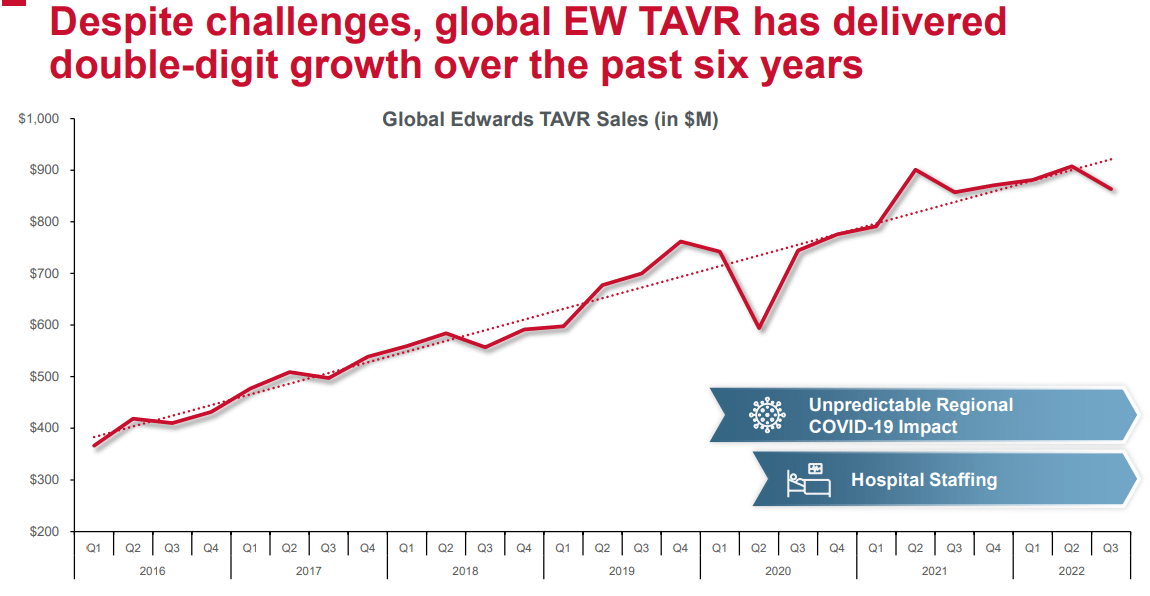

Leading Transcatheter Aortic Valve Replacement Technology: Transcatheter aortic valve replacement products represented 65% of total revenue in FY22. The Edwards SAPIEN family of valves possesses the best technology in the market. Despite COVID-19 challenges and hospital staff issues, Edwards's Transcatheter Aortic Valve Replacement business has experienced double-digit growth over the past six years.

2022 Edwards Investor Presentation

{kind=link}

The TAVR market is dominated by only two main players: Edwards and Medtronic. Boston Scientific ( BSX ) shut down their Lotus Edge transcatheter aortic valve replacement program in 2020. Edwards and Medtronic have dominated the market for almost a decade. As their scale grows, it becomes challenging for new players to enter this market.

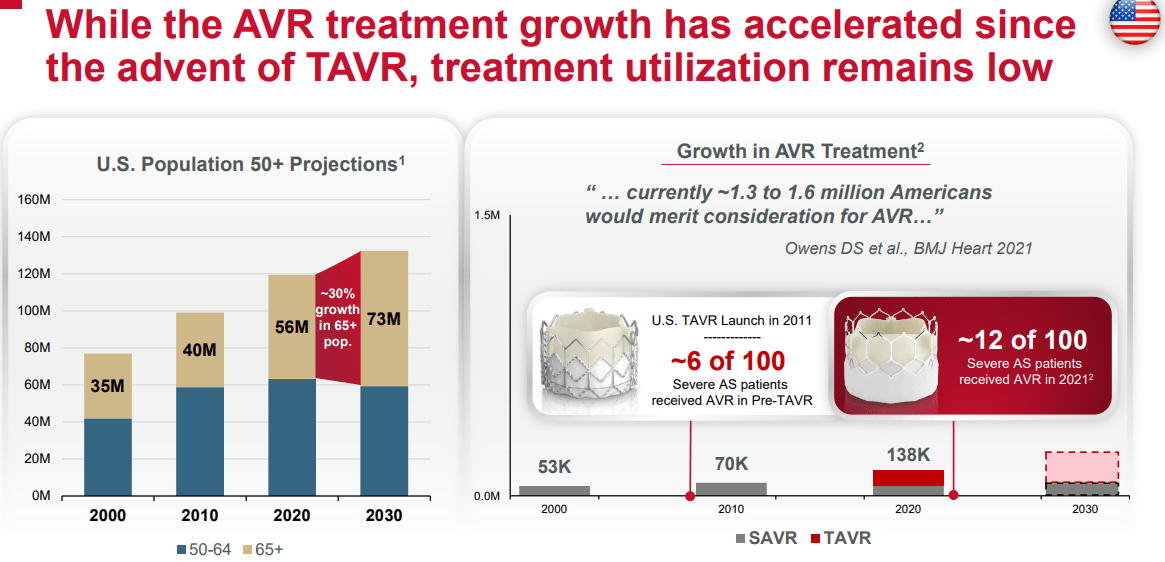

Additionally, I believe the TAVR market is underpenetrated, with significant growth potential ahead. As indicated by Edwards in their investor presentation , only 12 out of 100 aortic stenosis ((AS)) patients received Aortic Valve Replacement ((AVR)) in 2021.

2022 Edwards Investor Presentation

{kind=link}

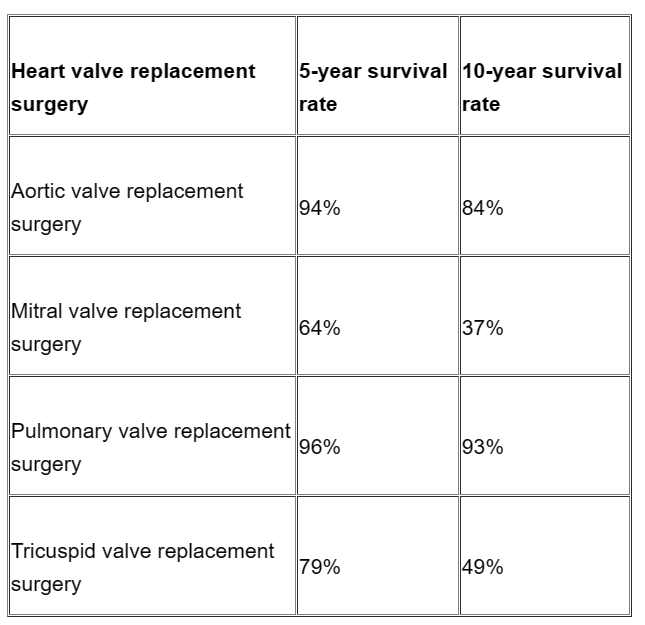

According to the article titled " Survival Rate of Heart Valve Replacement Surgery " on MedicineNet, the 5-year and 10-year survival rates after Aortic valve replacement surgery are the highest among all types of heart valve replacement surgeries. I believe that Edwards's TAVR technology will gain more popularity among patients with structural heart diseases, as TAVR is superior to other types of surgeries. It enables patients to have a longer lifespan and a better quality of life. The potential growth in penetration could fuel Edwards's business expansion over the next decade, in my opinion.

"Survival Rate of Heart Valve Replacement Surgery " on MedicineNet

{kind=link}

Transcatheter Mitral and Tricuspid Therapies: The Transcatheter Mitral and Tricuspid Therapies (TMTT) business provides transcatheter treatments for mitral and tricuspid valve diseases. Their transcatheter products are commercially available in Europe for mitral and tricuspid valve repair. The FDA approved the company's PASCAL Precision transcatheter valve repair system in 2022. Edwards indicates that their PASCAL Precision system can deliver faster procedures with enhanced patient outcomes.

Moreover, Edwards is conducting TRISCEND II trial , introducing new products designed to treat Tricuspid regurgitation. Edwards aims for U.S. approval around the end of 2024.

In my view, these products, in conjunction with Edwards's TAVR technology, could offer a comprehensive solution for patients with structural heart diseases. While TMTT currently constitutes a small portion of total revenue, it expands Edwards's range of product solutions. Edwards's salesforce can leverage all these product offerings to enhance sales productivity in hospitals.

Surgical Structural Heart: This business represented around 17% of total revenue in FY22. Their newest MITRIS RESILIA valve is available in the US and Japan. Edwards anticipates robust demand for surgical structural heart therapies. As disclosed in their 2022 Investor Presentation , Edwards expects the surgical structural heart market to reach $2 billion by 2028. The surgical structural heart market is driven by the surge in the number of people suffering from structural heart diseases. Additionally, advancements in diagnosis allow people to detect structural heart diseases earlier, enabling timely surgery.

Critical Care: Critical Care constitutes around 16% of total revenue. They manufacture hemodynamic monitoring systems used to measure a patient's heart function and fluid status in surgical and intensive care settings. This business growth is tied to hospital procedure volume and capital spending budgets. Edwards primarily competes against ICU Medical ( ICUI ) and PULSION Medical Systems. Similar to Edwards's TAVR solutions, these critical care solutions can assist hospitals and ICUs in offering comprehensive care to patients with structural heart diseases.

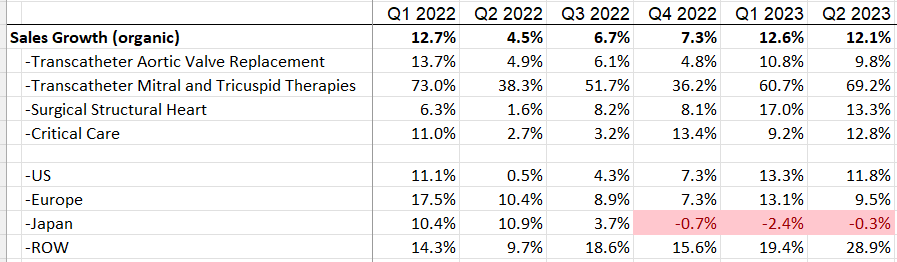

Putting all the pieces today, as depicted in the table below, Edwards has a strong history of organic growth, with TAVR contributing significantly.

{kind=link}

Rising Dominance In Structural Heart Disease

I envision Edwards emerging as the dominant player in the medical device field specializing in structural heart diseases. This thesis is based on several key factors:

Heavy R&D Investment in Structural Heart Diseases: Edwards has been spending more than 17% of total revenue in R&D in the past. They have been successfully developed several pioneer breakthrough technologies in structural heart diseases space. For instance, they launched SAPIEN in 2011, then SAPIEN XT in 2014, SAPIEN 3 in 2015, SAPIEN 3 Ultra in 2019, SAPIEN 3 Ultra RESILIA in 2022, and nowadays the next-generation SAPIEN X4. I believe these technology innovations are the DNA of Edwards, and I expect they continue to invest heavily in R&D to optimize their SAPIEN platform.

According to my research, most developed medical device companies are spending around 6% of total revenue in R&D. As such, Edwards is a outlier and it is a truly innovated growth company.

International Market Penetration: Presently, Edwards primarily operates within the United States, with nearly 60% of its total sales originating from this region. To extend its reach on an international scale, the company must focus on enhancing regulatory approvals, broadening global training initiatives, strengthening its sales force, and expanding manufacturing capabilities. Notably, the unique nature of structural heart disease devices necessitates extensive pre-training for surgeons and nurses. Consequently, the sales cycle for these devices tends to be more protracted compared to other commonplace medical devices.

Edwards has already implemented a high-touch service model in the United States, Japan, and select European countries. I anticipate this approach will extend to new regions in the future, contributing to the company's geographic diversification. This expansion could open doors to a substantial market opportunity as they navigate the global landscape.

Comprehensive Solutions for Structural Heart Diseases: Edwards' contribution to patients with structural heart diseases extends beyond TAVR products. The company is actively involved in producing Transcatheter Mitral and Tricuspid Therapies, as well as surgical structural heart and surgical heart monitoring systems. This comprehensive range of products offers hospitals and ICUs a comprehensive solution, essentially functioning as a one-stop shop for their needs.

This holistic product approach not only addresses a wider range of medical issues but also fosters customer loyalty and retention. By offering a diverse portfolio of products that cater to various aspects of structural heart diseases, Edwards establishes a stronger bond with its customers. This strategy enhances the company's customer relationships by providing them with comprehensive solutions and strengthening their reliance on Edwards' products and services.

Recent Quarterly Result And Outlook

In Q2 FY23 , Edwards delivered 12.1% organic revenue growth and 0.8% adjusted operating income growth.

{kind=link}

As revealed in their earnings call, their adjusted gross profit margin was 77.7% in Q2 FY22, compared to 80.5% in the same period last year. This reduction was driven by foreign exchange.

On the balance sheet, they held $1.5 billion in cash as of June 30th, 2023. Their balance sheet appears very solid.

Edwards has been repurchasing shares in recent years, buying back $1.7 billion in FY22, with approximately $650 million remaining under the current share repurchase authorization.

FY23 Guidance:

Revenue Growth in constant currency: 10%-13%, versus previous guidance of 10% to 12%

Adjusted EPS: between $2.50 and $2.60

Adjusted free cash flow: between $1.0 billion and $1.4 billion

Diluted shares outstanding: between 610 million and 615 million

Tax Rate: 13% to 17%

Valuation

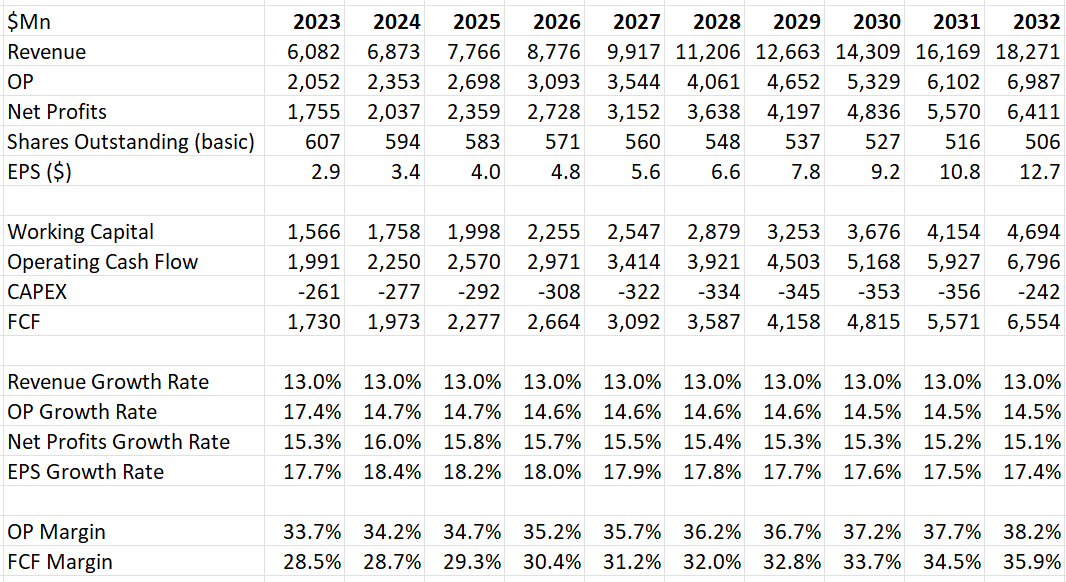

Sales Growth: I assume all growth comes from organic sources, with no contribution from acquisitions. In the model, I assume 13% revenue growth, primarily driven by procedure volume growth, new product launches, and penetration growth.

Operating Margin: I assume around 50bps of annual margin expansion. Their operating margin is expected to reach 38.2% in FY32 in my model.

Tax Rate: 15% in the model, in line with their guidance.

CAPEX: Edwards has been spending around $300 million annually. I don't expect their spending pattern to change significantly over the next decade.

With these assumptions, the model's financial summary can be found in the table below.

Edwards DCF Model, Author's Calculation

{kind=link}

To calculate the discount rate ((WACC)), I am using the following assumptions:

Beta: 1.02. Data Source: Yahoo Finance five-year monthly beta .

Risk-Free Rate of Return: 4.2%. I am using 10-year US government bond yield .

Expected Market Return Premium: 7%. I am using the same assumption across my models.

Cost of debt: 10%. I am using the same assumption across my models.

With these inputs, the cost of equity stands at 11.3%, and the WACC is estimated at 11.1% in the model.

Applying the discount rate, the present value of the free cash flow from the flow is calculated to be $48 billion in the model. That is the enterprise value of Edwards. Adjusting their debt and cash balance, the fair value is estimated to be $86 per share in the model.

Investment Risks

Competition from Abbott's Portico Product: The FDA approved Abbott's ( ABT ) Portico , the transcatheter aortic valve replacements in September 2021. Abbott officially joined Medtronic and Edwards in TAVR market.

According to Evaluate , Abbott's Portico meets noninferiority criteria, but safety appears doubtful. It's premature to determine if Abbott's TAVR product poses a substantial threat to existing players. Both Edwards and Medtronic TAVR products have been in the market for a long time, and I think they possess significant first-mover advantages in terms of technology and safety assurance.

Fluctuation in Procedure Volumes: Edwards's growth relies largely on procedure volumes. Hospital staffing shortages negatively impacted procedure volumes. However, hospital staffing has improved recently. In Q2 FY23 , Edwards observed a more stable hospital staffing environment in both the US and internationally. Their global TAVR grew 10% in constant currency in Q2 FY23 due to improving procedure volumes. Edwards also noted an increase in patients coming to hospitals and, importantly, in diagnoses, a leading indicator.

High R&D Expenses: Edwards has heavily invested in R&D, with R&D expenses accounting for over 17% of total revenue. In FY23, they anticipate R&D to be 17% to 18% of sales to support TAVR and TMTT new technologies. I expect their R&D expenses to remain high over the next few years. Despite the high R&D ratio, Edwards maintains an industry-leading operating margin, achieving 32.3% in FY22 and 32.5% in FY23.

Conclusion

I believe Edwards Lifesciences will continue to dominate market positions alongside Medtronic in the near future, although Abbott's Portico could capture a small share. Edwards's growth is primarily driven by global procedure volume growth and the market penetration of Aortic Valve Replacement surgeries. I trust Edwards can become the dominate player in the overall structural heart medical device filed. Considering the valuation, I assign a "Strong Buy" rating to Edwards Lifesciences.

For further details see:

Edwards Lifesciences: Rising Dominance In Structural Heart Disease