MDT - Edwards Lifesciences: Slowly Approaching Its Intrinsic Value

2023-06-12 23:39:04 ET

Summary

- Edwards Lifesciences is still reporting solid top-line growth in Q1/23 but the bottom line declined and fiscal 2022 also saw low growth rates.

- Aside from actual growth rates in the last few quarters, Edwards Lifesciences is a high-quality business with a wide economic moat based on patents and switching costs.

- For the years to come, analysts as well as management are expecting double-digit growth rates again.

- Even when considering double-digit growth rates, EW stock still seems to be a bit overvalued and not a good investment.

So far, I covered Edwards Lifesciences ( EW ) twice on Seeking Alpha - and in both cases I was rather cautious about the stock as an investment. My first article was published in April 2021 - and since then the stock declined slightly about 1.5%. My second article was published in June 2022 and during the last year the stock lost about 14% in value.

And while the stock was struggling in the last 1.5 years, the performance during the last 10 years was great. We certainly must acknowledge that the stock performance of EW was great, and it was a great investment. Between 2013 and late 2021, the stock could increase its value about 13 times. But we should point out that a big part of the performance also stemmed from valuation multiples expansion: the price-sales ratio increased from 3.5 to 16.25 and the price-earnings ratio increased from 12 to 78.

In the last few quarters, valuation multiples "normalized" again, and the stock is trading for more reasonable multiples (we will get to this). But this process of lower multiples also led to a declining stock price. The question we must answer now is if Edwards Lifesciences is a good investment and if the still growing business will be enough to offset potentially further declining valuation multiples (as the trend might continue).

Quarterly Results

To answer the question, we first have to look at the last results to see if Edwards Lifesciences can continue to grow and if it can continue to grow with a high pace (as it has in the past). When looking at the first quarter results for fiscal 2023, we can see sales increasing from $1,341 million in Q1/22 to $1,460 million in Q1/23 - resulting in 8.9% year-over-year growth. And while Edwards Lifesciences could report solid top line growth, operating income declined from $438.8 million in the same quarter last year to $388.4 million this quarter - a decline of 11.5% YoY. And finally, diluted earnings per share also declined 5.1% YoY from $0.59 in Q1/22 to $0.56 in Q1/23.

Edwards Lifesciences 2022 Investor Conference Prese

{kind=link}

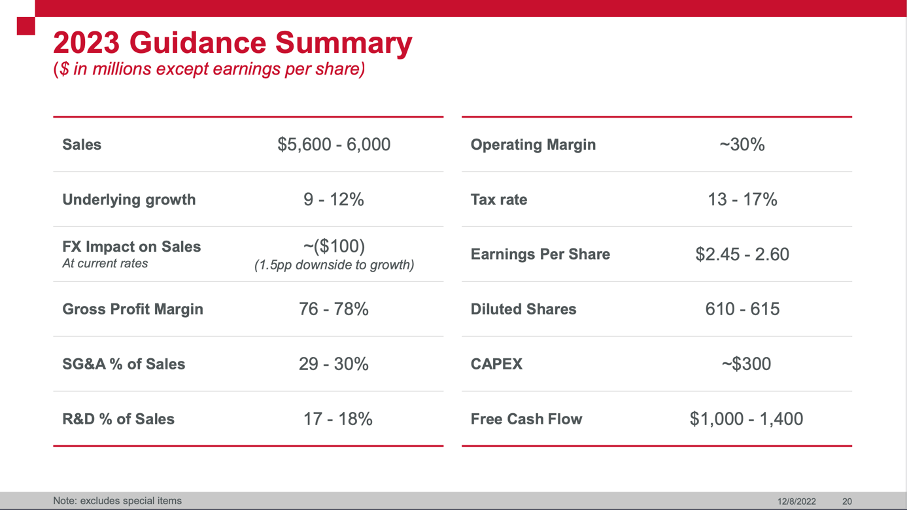

Edwards Lifesciences already issued a solid guidance for fiscal 2023 during its 2022 Investor Conference last December. During the last earnings call, the company raised its guidance again and is now expecting its sales for fiscal 2023 to be at the high end of its $5.6 to $6.0 billion range (resulting in 10% to 12% underlying growth). Adjusted earnings per share are now also expected to be in a range between $2.48 and $2.60 - compared to $2.44 in diluted earnings per share in fiscal 2022 it would result in 1.5% to 6.5% year-over-year growth for the bottom line.

Long-term Growth

While we don't want to bash Edwards Lifesciences for its results, the growth rates in the last few quarters were rather mediocre - especially compared to the last ten years. In fiscal 2022, revenue increased only about 3% and earnings per share about 2.5% year-over-year.

Edwards Lifesciences Annual Report 2022

{kind=link}

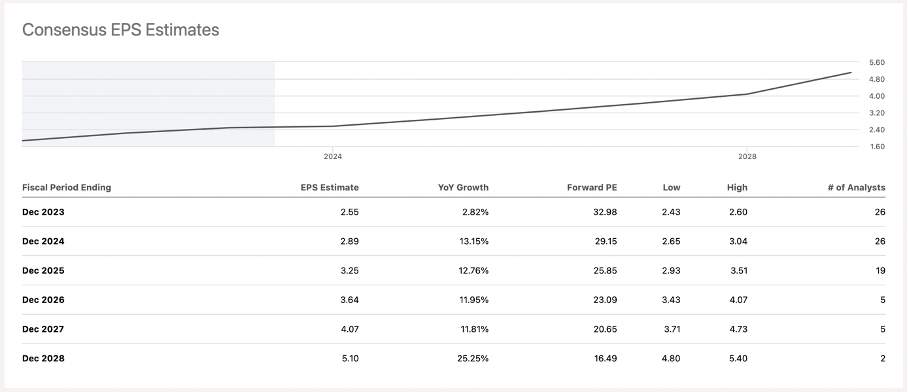

Compared to growth rates in the last decade (revenue increased with a CAGR of 10.98% and earnings per share increased with a CAGR of 19.43%) these growth rates are rather disappointing. However, analysts are expecting double-digit growth rates for fiscal 2024 and the following years again.

EPS consensus estimates for Edwards Lifesciences (Seeking Alpha)

{kind=link}

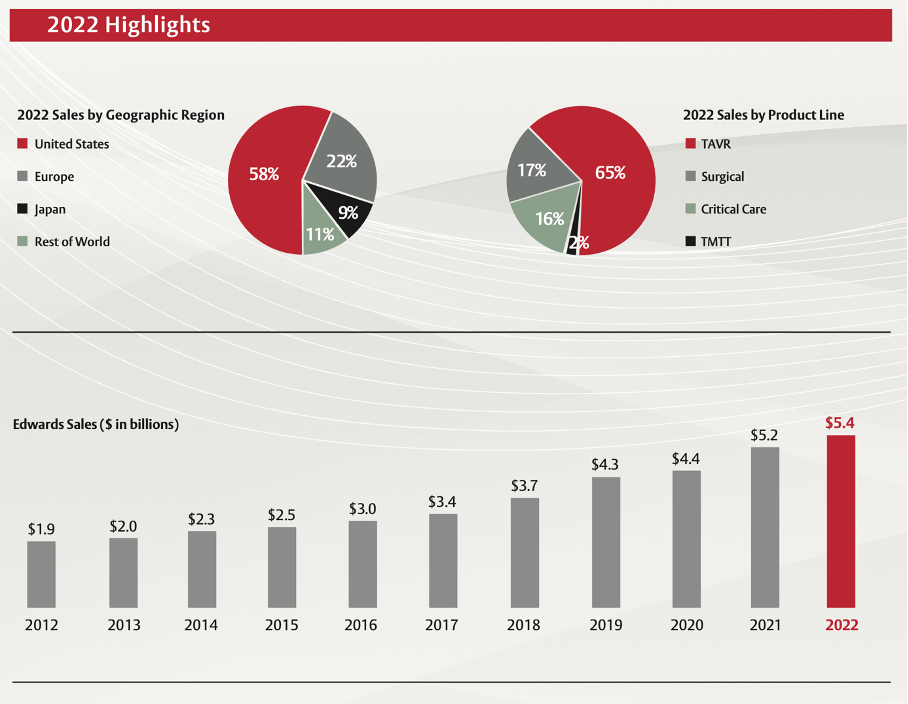

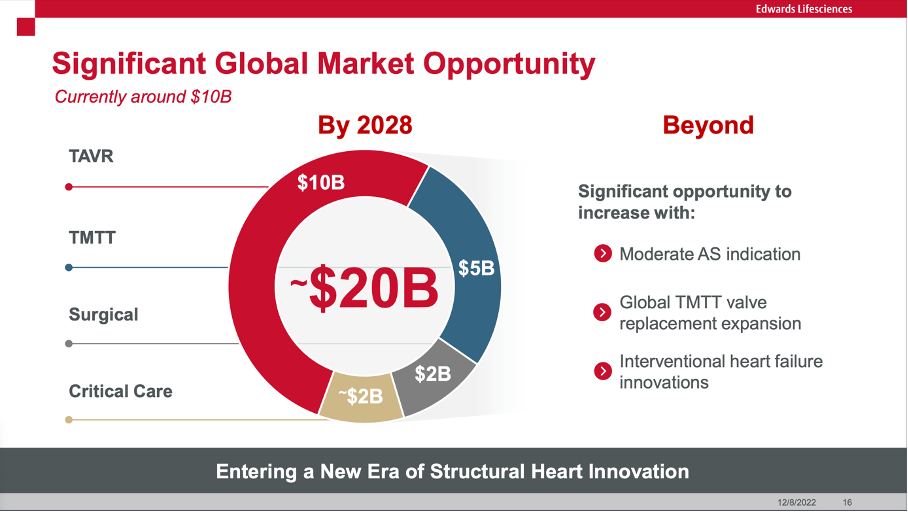

And as I have pointed out in previous articles, Edwards Lifesciences certainly has the potential to grow as the underlying market will continue to grow at a high pace. The company's global market opportunity is currently around $10 billion and will double in the next five years to reach a TAM around $20 billion in 2028. Especially TAVR - the most important market for Edwards Lifesciences (65% of its revenue in fiscal 2022) - will reach a global market size of $10 billion.

Edwards Lifesciences 2022 Investor Conference Prese

{kind=link}

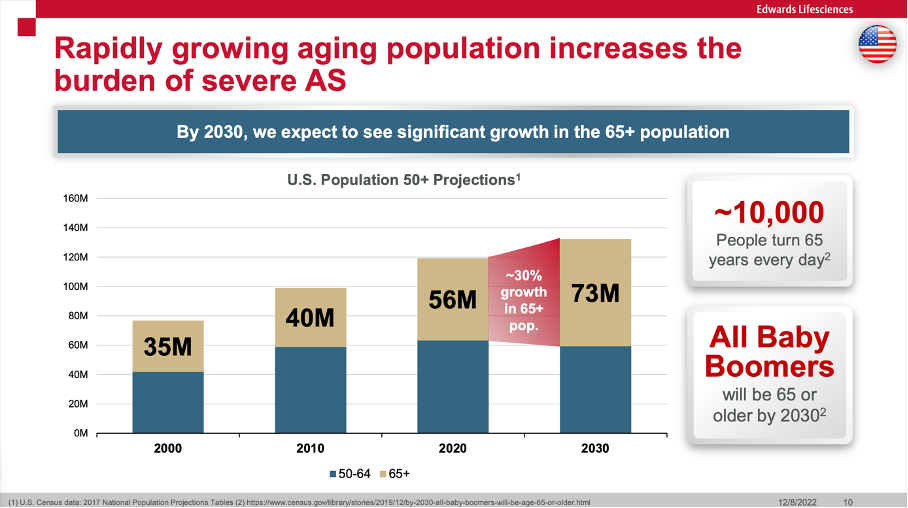

One megatrend that might drive growth for Edwards Lifesciences - similar to many other healthcare, pharmaceutical and medical device companies - is the rapidly growing aging population in the United States. And we are looking especially at the United States as Edwards Lifesciences generated 58% of its fiscal 2022 sales there.

Edwards Lifesciences 2022 Investor Conference Prese

{kind=link}

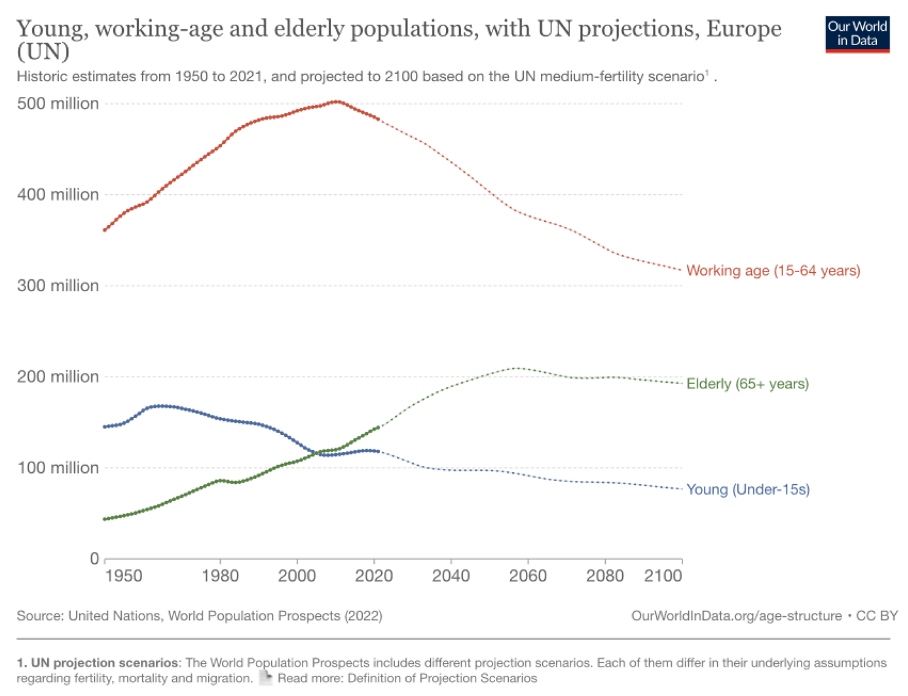

But of course, the elderly population increasing is not a just a trend visible in the United States - it is visible in most developed economies. And especially in Europe (22% of total sales in 2022) the picture is similar. For the next few decades, the number of older people will continue to increase in Europe.

{kind=link}

Hospital Staffing

And while the growing elderly population will most likely lead to higher demand for pharmaceuticals as well as medical devices (and lead to growing revenue for Edwards Lifesciences), the demographic shift that will occur in the coming decades is also posing a risk for the company. In the last few quarters, the healthcare staffing was one of the issues discussed during the earnings call and also reason for the mediocre results in 2022. During the last earnings call management was more optimistic that healthcare staffing (especially hospital staffing levels) was improving again, and management is expecting the situation to continue improving throughout the rest of the year.

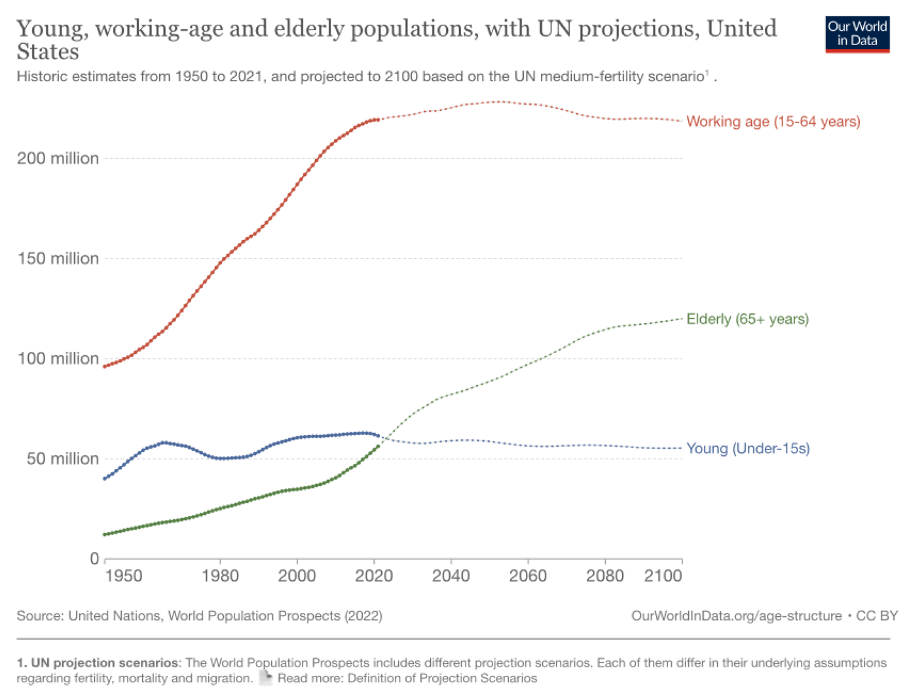

When taking the long-term view however, we are potentially looking at a severe problem. Especially in Europe, hospital staffing issues might become a major issue. When looking at the chart above we can see that the working age population in Europe will decline steeply until 2100. When looking at the same data for the United States, the picture is a bit better as the working age population in the United States will continue to increase slightly in the next few decades and then more or less stagnate at a high level.

{kind=link}

And the combination of a stagnating (or declining working age population) and an increasing elderly population is creating a huge problem that might also affect Edwards Lifesciences. An increasing elderly population will need more care and more operations but with a declining working age population the necessary staff in hospitals or nursing homes might not be found - creasing a huge problem. On the other hand, hospital staffing issues seem not to be a new problem as there was a shortage in the 1940s as well as the 1990s (thanks to Horizon Capital for bringing this to my attention).

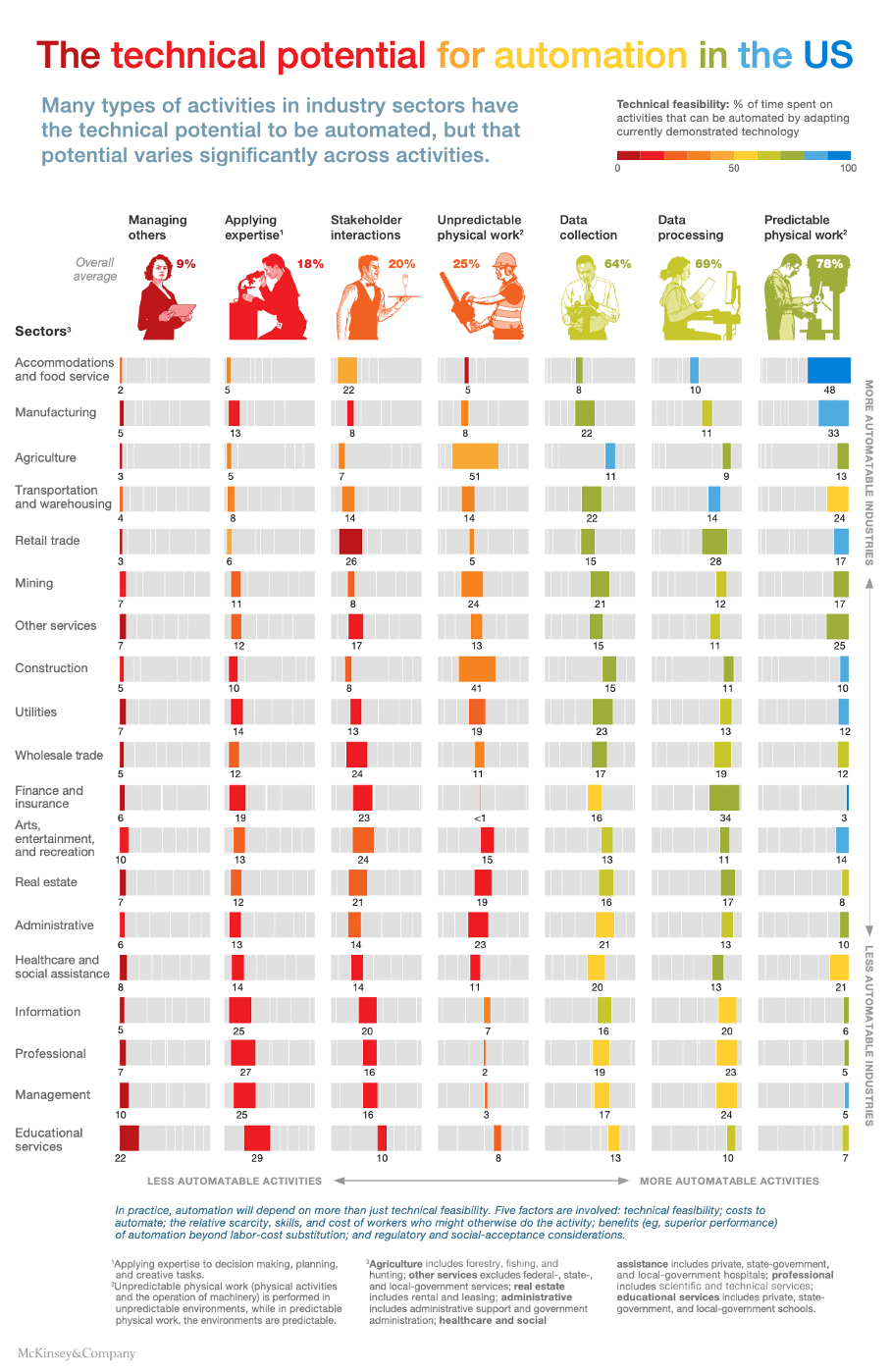

But we should not ignore this problem - especially as there seem to be only very few solutions to this problem. While automation and artificial intelligence (one of the current hypes and a subtopic of automation) will lead to shifts in the labor market we can't imagine right now, jobs in hospitals and nursing homes are among those that are hard to replace by automation. Jobs in the healthcare sector are demanding emotional intelligence and are a combination of many non-routine tasks - and these are the skills which are hardest to automate at this point.

{kind=link}

With all the information we have today, we are most likely looking at a challenge that can only be solved by making these jobs more attractive (better payment might be part of the solution).

Economic Moat

Now after that digression about automation and the labor market, let's return to the topic at hand - Edwards Lifesciences. After talking about the company's growth potential in the years to come and risks the hospital staffing problems might cause, let's look at another risk the company is facing - the competition. And especially in a market promising high growth rates, competition is a huge challenge as such markets will usually attract new competitors.

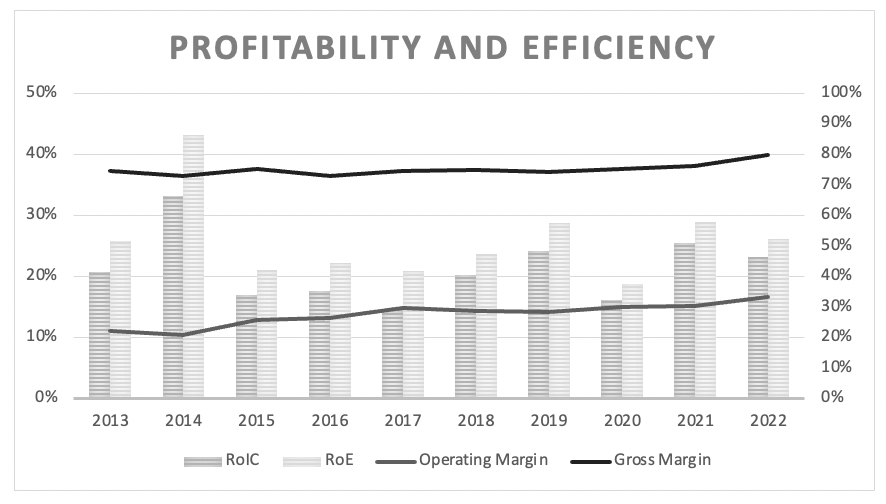

But as I have already mentioned in my first article about Edwards Lifesciences, the company has a wide economic moat around its business, and we therefore can expect the company being able to hold competitors at bay. When talking about economic moats, we can look at some metrics that usually indicate an economic moat around a business. For starters, we can look at the gross and operating margin: both should either be consistent over the years or - even better - improve over time. In case of Edwards Lifesciences, we see high levels of consistency and improving margins in the last few years, which is a first hint for a wide economic moat.

Edwards Lifesciences: Margins and Profitability (Author's work)

{kind=link}

A second important metric to look at is the return on invested capital. Companies with a wide economic moat around the business should be able to consistently report an RoIC of at least 10%. Edwards Lifesciences is reporting an RoIC of 21.23% on average during the last ten years - clearly indicating an economic moat.

When trying to identify the source for the company's economic moat we can mention the patents as well as switching costs. While I could not find any information about patents in the last Annual Report, the company seems to have about 1,500 patents and is filing about 50 to 100 new patents each year. And while patents are not the best source of economic moat a company can have, I still see Edwards Lifesciences in a great position for two reasons. First, Edwards Lifesciences has a huge number of patents and is therefore limiting the risks associated with patent loss. Second, the company is spending huge amounts on research and development and will most likely be able to replace expiring patents. When comparing the amounts Edwards Lifesciences is spending on research and development (as % of total sales) to the company's peers - Medtronic plc ( MDT ), Abbott Laboratories ( ABT ) or Boston Scientific Corporation ( BSX ) - we get impressive numbers.

| Company | 2018 | 2019 | 2020 | 2021 | 2022 | 5-year average |

|---|---|---|---|---|---|---|

| Edwards Lifesciences | ||||||

| 16.71% | ||||||

| 17.31% | ||||||

| 17.34% | ||||||

| 17.26% | ||||||

| 17.56% | ||||||

| 17.24% | ||||||

| Medtronic | ||||||

| 7.63% | ||||||

| 8.06% | ||||||

| 8.28% | ||||||

| 8.67% | ||||||

| 8.62% | ||||||

| 8.25% | ||||||

| Abbott Laboratories | ||||||

| 7.52% | ||||||

| 7.65% | ||||||

| 6.83% | ||||||

| 6.36% | ||||||

| 6.62% | ||||||

| 7.00% | ||||||

| Boston Scientific | ||||||

| 11.33% | ||||||

| 10.94% | ||||||

| 11.53% | ||||||

| 10.13% | ||||||

| 10.43% | ||||||

| 10.87% |

Aside from the patents, switching costs are a second source for a competitive advantage the company has. In my first article I wrote:

For the medical professionals, there is often a steep learning curve involved. All people involved in the procedure have to learn to use the products and once they are trained on using Edwards Lifesciences' products (and maybe are convinced these are the best), they might be hesitant to switch.

Of course, the other major competitors mentioned above see similar tendencies and can create similar switching costs. However, when looking at the different numbers and metrics, neither Medtronic nor Abbott Laboratories seems to be able to match Edwards Lifesciences."

And the combination of these two - patents and switching costs - are generating an economic moat around the business that is difficult to match for competitors.

Share Buybacks

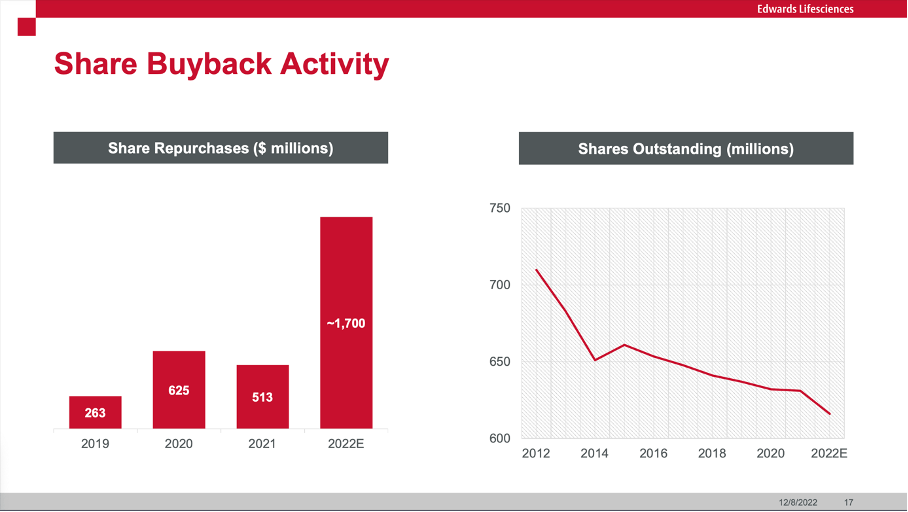

We should also mention share buybacks, which have always played a role for Edwards Lifesciences although the company never repurchased shares aggressively. However, in fiscal 2022 the picture changed, and management spent $1,727 million on share buybacks. This is worth mentioning for two reasons. First, the amount is a multiple of the sums the company spent in the past few years. Second, the cash spent on buybacks was almost twice the free cash flow Edwards Lifesciences generated in fiscal 2022 ($973.6 million) and therefore the company had to use cash on its balance sheet.

Edwards Lifesciences 2022 Investor Conference Prese

{kind=link}

The aggressive share buybacks in 2022 might underline that management saw its stock being undervalued in 2022. In the first quarter of fiscal 2023 the amount spent was lower again, but Edwards Lifesciences still repurchased shares worth $249 million. And while about $650 million are remaining under the current share repurchase authorization, we must expect the company to slow its buybacks down again. During the last earnings call, management estimated the number of diluted outstanding shares for 2023 to be between 610 million and 615 million (at the end of the first quarter, the number was 610.9 million).

Intrinsic Value Calculation

In the past, the main reason not to buy Edwards Lifesciences was the valuation and the fact that the stock price was not justified by fundamentals (in my opinion). The fundamental business (high growth rates in the past, expected double-digit growth rates in the future and a wide economic moat) would justify an investment, but the high valuation multiples the stock was trading for made me cautious to invest money in Edwards Lifesciences.

When looking at the price-earnings ratio, we see a constantly declining P/E ratio in the last few years. In 2021, the ratio peaked at 78 and is constantly declining and now the stock is trading for 35 times earnings. This is below the 5-year average of 50.21 and could be justified for a high-quality business.

However, when looking at the - in my opinion more important - price-free-cash-flow ratio, the picture is a little different. We also saw extremely high P/FCF ratios in 2020 and 2021 and the valuation multiples declining in the following quarters. While the P/E ratio continued to decline, the P/FCF ratio was stagnating in the last few months and although the stock is trading slightly below the 5-year average of 56.81, a P/FCF ratio of 53 still seems excessive and not justified.

While it seems like Edwards Lifesciences got "cheaper" in the last two or three years, I would still be cautious if the stock is a good investment. And as always, we are using a discount cash flow calculation to determine an intrinsic value, a fair price I would be willing to pay for the stock. In my last article I calculated an intrinsic value of $86.46 in a rather bullish scenario and hence the stock would be more or less fairly valued at the time of writing.

This intrinsic value was calculated about a year ago - and is clearly demanding an update. As always, we calculate with a discount rate of 10% and the number of diluted outstanding shares is 610.9 million. As basis, we could use the free cash flow of the last four quarters which was $1,005.6 million. And when assuming 6% growth in ten years from now till perpetuity, Edwards Lifesciences must grow its free cash flow more than 16% annually for the next ten years to be fairly valued. And although the company could grow its bottom line with a CAGR of 19.43% in the last ten years, I would classify these assumptions as too optimistic (analysts are also more pessimistic - see above).

However, we can be a little more optimistic about the free cash flow we take as basis. A realistic assumption would be the midpoint of the company's own fiscal 2023 guidance - $1,200 million (see above). When calculating with this amount - and all other assumptions remain the same - the company must grow its free cash flow between 13% and 14% in the next ten years to be fairly valued. And while these growth rates seem achievable for the business, I would still be rather cautious and see Edwards Lifesciences as fairly valued at best (rather a bit overvalued).

Conclusion

I would still see Edwards Lifesciences as a "Hold". In retrospect one might have purchased EW for $70 back in October or November 2022, but I would still expect the stock to reach at least that level again (and maybe decline even lower). Edwards Lifesciences remains on my watchlist as it is a great business, but still not a great investment.

For further details see:

Edwards Lifesciences: Slowly Approaching Its Intrinsic Value