EW - Edwards Lifesciences: Undervalued With A Substantial Upside Potential

2024-01-09 03:47:30 ET

Summary

- Edwards Lifesciences is down 3.10% over the last year but I am bullish due to its optimistic outlook and growth initiatives.

- The company is committed to its shareholders through EPS growth and share buyback program.

- EW stock is undervalued with a double-digit upside potential, warranting a buy rating.

Investment Thesis

Edwards Lifesciences Corporation ( EW ) is down 3.10% over the last year but I am bullish on the stock given its optimistic outlook for 2024 and beyond which I find very realistic and backed with strong levers. The company has a clear growth strategy , which I am confident will lead to long-term sustainable growth. Based on comparative analysis, EW appears to have higher growth rates and profitability ratios than competitors; something I believe underscores its ability to outperform its peers, some of whom have a larger capacity in terms of growth and profitability than them.

In terms of delivering to shareholders, EW has a 5-year EPS CAGR of 16%, which underscores its ability to create value for shareholders. Aside from that, the company has committed to shareholders through share repurchases, as evidenced by the recent approval of a $1 billion additional share repurchase authorization. In terms of valuation, using a DCF model, I estimate a fair value of around $100, implying a 38% upside potential. This demonstrates that EW is undervalued, providing an appealing entry point for potential investors to invest in this company with massive growth potential supported by its growth strategy.

EW 2024 Outlook And Buyback Plan

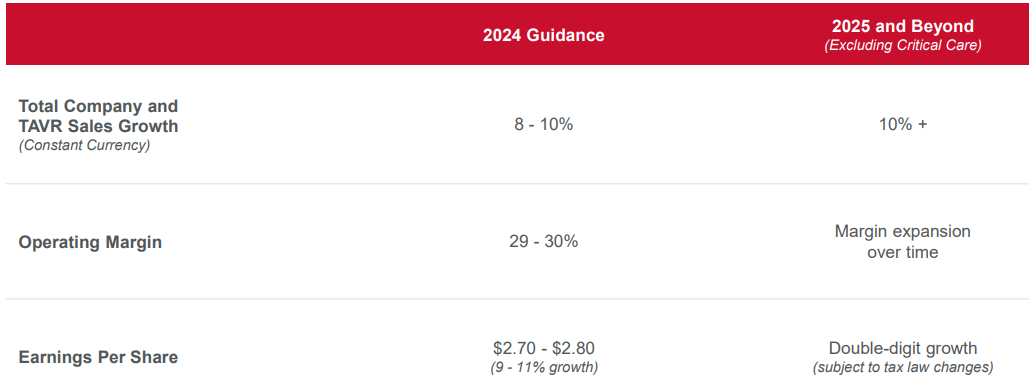

During its most recent investors presentation , EW gave its 2024 and beyond outlook which looks very promising. In the following section, I will attempt to demonstrate how realistic it is, which will justify why it forms the basis of my bullish outlook on this stock. Let us look at the 2024 outlook and my thoughts about it. The company expects to achieve the following goals in 2024:

- Global sales of $6.3-$6.6 billion, representing a constant currency growth of 8%-10%.

- Adjusted earnings per share of $2.70-$2.80, representing a constant currency growth of 9%-11%.

- Continued leadership in the global transcatheter aortic valve replacement [TAVR] market, with expanded opportunities for transcatheter mitral and tricuspid therapies [TMTT] and surgical heart valves.

- Completion of the spin-off of its Critical Care business by the end of 2024, creating an independent company focused on advanced patient monitoring and artificial intelligence solutions.

{kind=link}

EW Investor Presentation 2023

The company also announced plans to buy back $1 billion of its common stock, in addition to the $750 million accelerated share repurchase agreement executed in November 2022. This reflects the company's confidence in its long-term growth prospects and its commitment to return capital to shareholders.

In summary, EW has a strong growth strategy and outlook for 2024, supported by its innovative product portfolio, expanding market opportunities, and spin-off of its Critical Care unit. The company also plans to repurchase $1 billion of its shares, which could enhance its earnings per share and shareholder value. Based on this background, I am optimistic about the company’s share performance in the future as this projected growth backed by the mentioned catalysts will translate to a strong share performance.

Why The 2024 Outlook And Beyond Is Realistic: Growth Initiatives

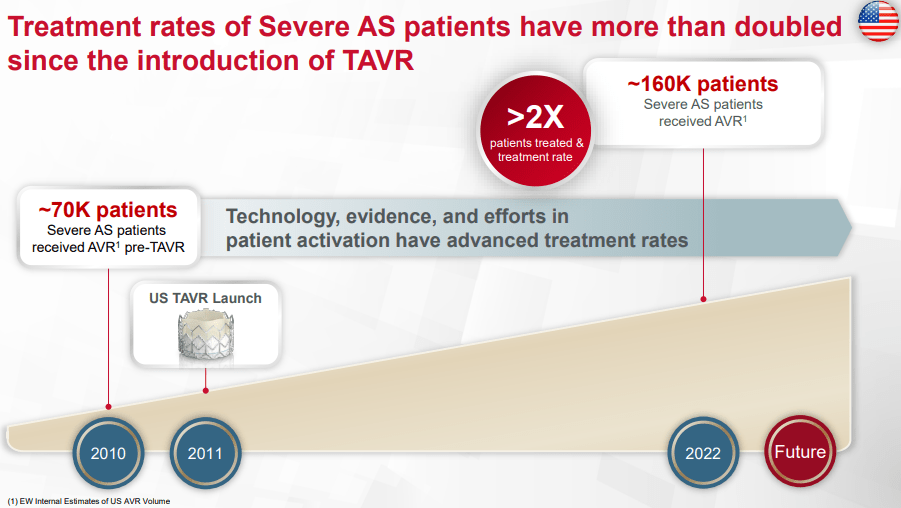

While organizational goals should be realistic and attainable, management can occasionally be overly ambitious and set unrealistic goals. In this section, I'll explain why I think EW's 2024 outlook is realistic. First off, the global TAVR (transcatheter aortic valve replacement) market will continue to expand , driven by increased awareness, patient activation, new technologies, indication expansion, and global adoption. This growth should help EW maintain its leadership position in this market by leveraging its current valve platforms and developing new ones, such as the SAPIEN M3 and the EVOQUE tricuspid valve.

Precedence Research

To demonstrate how the company will benefit from this projected growth through its innovative products, treatment rates for severe AS patients have more than doubled since the introduction of TAVR. This demonstrates that the company is well-positioned to capitalize on projected growth, which I believe will help it meet its financial targets for 2024.

{kind=link}

EW Investor Presentation 2023

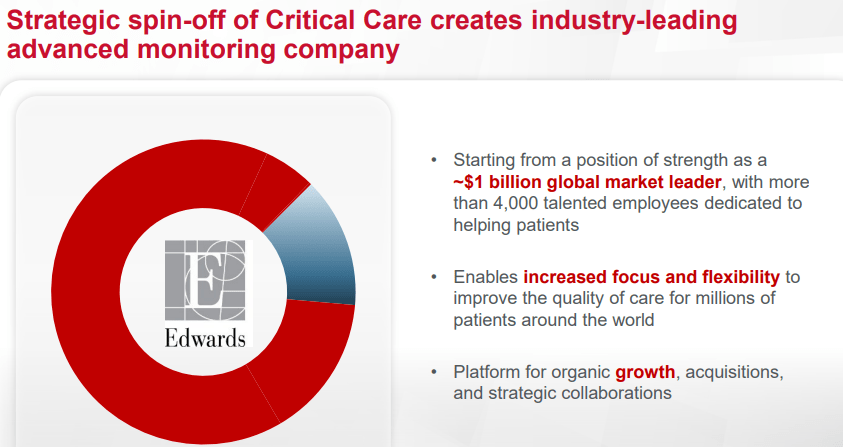

The Critical Care business will be spun off by the end of 2024 , allowing EW to focus on its core cardiac segments while also investing in new areas such as interventional heart failure. The spin-off will also establish a separate entity capable of better meeting the needs of patients and clinicians in the advanced patient monitoring space. The Critical Care business accounts for approximately 16.0% of Edwards' consolidated revenue and is expected to grow in the mid-single digits in constant currency, with sales ranging from $900.0 million to $1.0 billion by 2024. The deal is expected to create an industry-leading advanced monitoring company that I believe will speak authoritatively about EW's leadership position in the industry, attracting more customers while keeping current ones loyal, resulting in an increasing loyal client base and increasing revenues and profit margins.

{kind=link}

EW Investor Presentation 2023

Finally, the company intends to continue investing in R&D, clinical trials, and commercialization to support its pipeline of new products and indications. In 2024, EW plans to spend approximately 17%-18% of its sales on R&D and will conduct several pivotal trials .

Given this background, it is clear that EW's financial projections are supported by strong growth initiatives that will not only strengthen its financial position but also solidify its leading position in some of its key markets, which I anticipate will result in a larger client base and revenue base. Besides the growth initiatives, other aspects point out that the company’s projections are very attainable.

First off, they are in line with the consensus estimates of Wall Street analysts , who expect EW to report sales of $6.47 billion and EPS of $2.7 in 2024. They also reflect the company's historical performance, as EW has consistently delivered an average sales growth rate of 9.95% over the last four years and an average EPS growth rate of 27.58% over the last four years.

Based on this information, I am confident that EW's outlook for 2024 and beyond is both realistic and attainable. It has a strong growth strategy, a strong competitive position, and a robust product pipeline, all of which I believe will contribute to strong long-term growth.

EW Comparative Analysis

Doing a comparative analysis is one way of evaluating how competitive a company is. Here is my comparative analysis of EW. Some of its main competitors are Abbott Laboratories ( ABT ), Medtronic ( MDT ), Boston Scientific ( BSX ), and ICU Medical ( ICUI ). Here are some key points of comparison:

- EW reported revenue growth of 12.27% year on year in the third quarter of 2023, while its competitors' average revenue growth was about 2.89%.

- Edwards had a net margin of 25.99% in the third quarter of 2023, while its competitors' average net margin was 13.98%.

- Edwards has a stock price of $72.85 and a market capitalization of $44.18 billion, while Abbott Laboratories has a stock price of $110.8 and a market capitalization of $192.36 billion, Medtronic has a stock price of $84.57 and a market capitalization of $112.45 billion, Boston Scientific has a stock price of $58.16 and a market capitalization of $85.20 billion, and ICU Medical has a stock price of $97.62 and a market capitalization of $2.35 billion.

YCharts

- Similarly, its revenue and EPS on a TTM basis are shown in the chart below.

YCharts

These figures show that EW has achieved higher growth rates and profitability ratios than some of its competitors, despite having a smaller revenue and market cap. Therefore, EW is a strong and competitive player in the medical device industry. With its innovations and growth initiatives discussed in the preceding sections, I am optimistic about its future growth and competitiveness in this industry.

Valuation

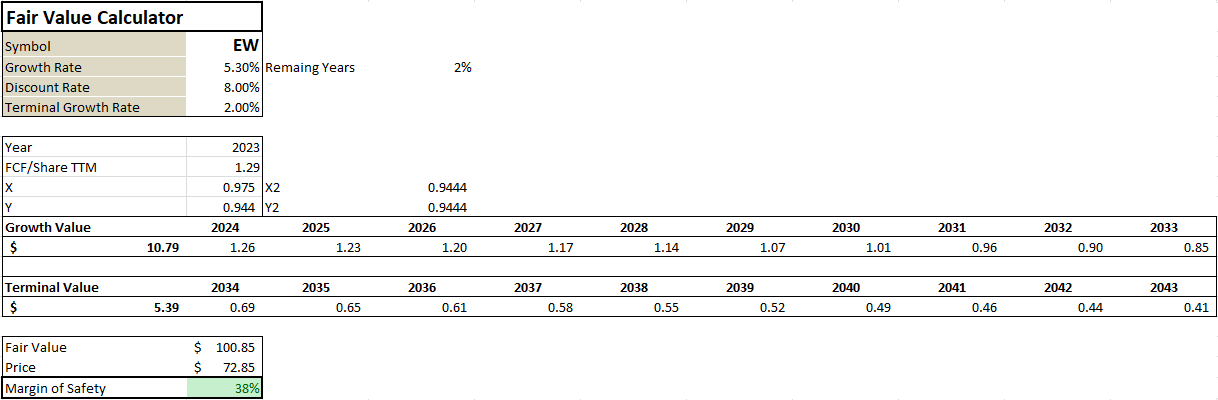

I will use a DCF model to determine the stock's fair value, even though I am aware of its primary drawback, that is, its reliance on assumptions, which I will attempt to mitigate by employing reasonable and, to some extent, conservative assumptions. Below are my model output and assumptions.

{kind=link}

Author's Computations

In my estimation, I used a discount rate of 8% which is the company’s WACC based on my computations. I assumed a growth rate of 5.3% which is very conservative compared to its double-digit free cash flow growth rate over the last five years. I assumed a terminal growth rate of 2% which is also conservative given the potential of the pending growth initiatives which could drive a strong cash flow growth in the future. With these assumptions and using the company’s TTM FCF/share of 1.29 as the base, I arrived at an estimated fair price of $100.85. This signifies that this stock has an upside potential of 38%. I believe the company's strong growth strategy will help this stock capitalize on its upside potential, which I believe potential investors should seek to leverage and maximize their returns.

Risks

Even though I think EW is a good investment, there are risks involved in investing here. One of the major risks is the foreign exchange headwind. The company operates globally and is exposed to fluctuations in currency exchange rates, which can affect its revenue and profitability. According to the company's third-quarter results , unfavorable foreign currency movements reduced its sales by 140bps and its gross profit margins by 410bps, compared to the same period last year. This factor might affect EW's top and bottom lines because the FX environment is expected to be turbulent in 2024 . Prospective investors ought to evaluate the progress of this challenge and any possible risk-hedging measures to be implemented.

Conclusion

To sum up, EW presents a good investment prospect owing to its robust growth strategy and considerable upside potential. The company's robust growth initiatives are supporting its promising future outlook. Its capacity to outperform its rivals in terms of growth and profitability further demonstrates its competitiveness. I recommend this stock to prospective investors at the current price because of its strong growth potential and undervaluation.

For further details see:

Edwards Lifesciences: Undervalued With A Substantial Upside Potential