EW - Edwards Lifesciences: Valuation Seems Still Too Elevated

2023-06-12 17:55:23 ET

Summary

- Edwards Lifesciences is now down over 35% from its all-time high.

- The company should continue to benefit from the market expansion of TAVR amid the growing aging population and increasing life expectancy.

- The latest earnings were mixed as top-line growth improved while the bottom line remains very weak.

- Despite the drop, the current valuation is still meaningfully elevated compared to other healthcare equipment companies.

- I rate the company as a hold.

Investment Thesis

Edwards Lifesciences ( EW ) has been an outstanding compounder in the past decade, with shares up over 620% during the period. The company continues to benefit from the rapidly expanding TAVR market amid the growing aging population and increasing life expectancy.

However, it has been underperforming since last year as the valuation seemed extended while growth was impacted by hospital constraints. Despite the 30%+ drop from its all-time high, I still do not think the current price looks attractive. The valuation is a huge concern as multiples remain meaningfully elevated compared to peers. Sales growth has improved but is still not strong enough to justify the valuation. I do not see much upside potential in the near term therefore I rate the company as a hold for now.

The Leader In TAVR

Edwards Lifesciences is a leading global healthcare equipment and technology company that specializes in structural heart disease and critical care. Roughly 65% of the company's revenue is generated from TAVR (Transcatheter Aortic Valve Replacement) products, which is its major focus. According to its FY23 sales estimate, it currently has a dominating 63.9% market share. The leading position and branding give the company a strong moat as the industry has extremely high regulatory and R&D (research and development) barriers.

TAVR is a rapidly expanding market. According to Strategic Market Research , the global market size of TAVR is forecasted to grow from $5.63 billion in 2023 to $13.4 billion in 2030, representing a strong CAGR (compounded annual growth rate) of 13.1%. The growing aging population and the increasing life expectancy continue to be major drivers for market expansion.

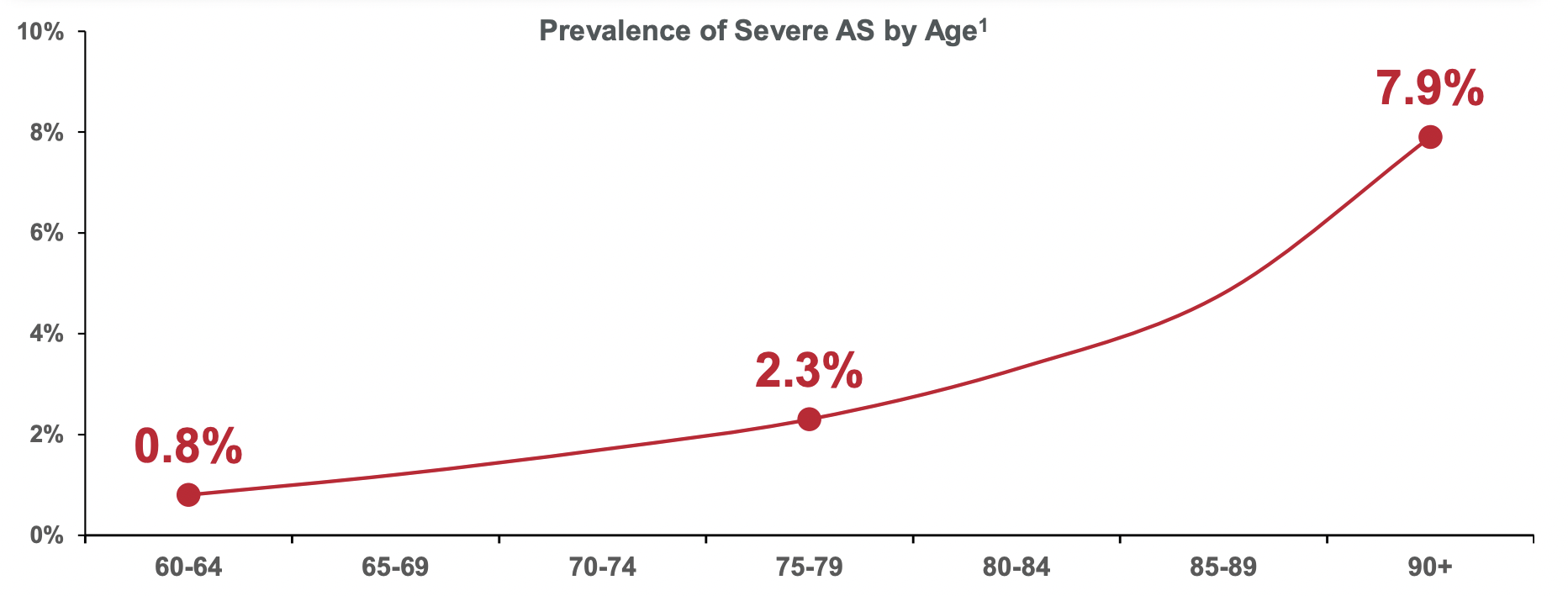

For instance, the percentage of the world's population over 60 years old is expected to grow from 12% in 2015 to 22% in 2050, according to the World Health Organization. This trend will likely increase the number of severe aortic stenosis patients as the disease's prevalence is highly correlated with age. According to the company , its prevalence among people at age 60-64 is only 0.8% but the figure jumps substantially to 7.9% for people at age 90 or over, as shown in the chart below. Considering the backdrop, the demand for AVR treatment should continue to increase over time.

{kind=link}

Edwards Lifesciences

Mixed Financials

Edwards Lifesciences' latest earnings finally showed some improvements in top-line growth, as hospital constraints eased. The company reported revenue of $1.46 billion, up 8.8% YoY (year over year) compared to $1.34 billion. The TAVR segment grew 7.6% from $881.3 million to $947.9 million, accounting for 65% of total revenue. The growth was largely driven by the increase in procedure volume globally, as hospital staffing levels improved. The remaining segments increased 11.3% from $459.9 million to $511.7 million, mainly driven by the strength in the surgical structure heart segment.

Michael Mussallem, CEO, on easing hospital constraints

As we indicated, we believe that first quarter trends were lifted by improved hospital staffing levels. Results were also lifted by a catch-up in procedure volumes early in the quarter following the holiday season slowdown.

The bottom line was weak as spending surged. SG&A (selling, general, and administrative) expenses increased 17.8% from $370.3 million to $436.3 million, largely attributed to costs around personnel. R&D expenses also increased 14.3% from $228.6 million to $261.2 million, due to a higher number of clinical trial activities. The elevated spending resulted in the adjusted operating income dropping 2.4% YoY from $444.7 million to $434.1 million. The adjusted operating margin declined 350 basis points from 33.2% to 29.7%. The diluted EPS was $0.62 compared to $0.60, up 3.3% YoY as it benefited from the drop in the number of shares outstanding amid buybacks.

Lofty Valuation

Despite being down over 35% from its all-time high, Edwards Lifesciences' valuation continues to be a major issue in my opinion. The company is still trading at an fwd PE ratio of 33x, which is pretty expensive by all standards. As shown in the chart below, the current multiple remains elevated compared to other leading healthcare equipment companies such as Abbott Laboratories ( ABT ), Boston Scientific ( BSX ), and Mettler-Toledo ( MTD ).

For instance, the peer group's average fwd PE ratio of 26.3x represents a meaningful discount of 25.3%. The company's latest revenue growth of 9% and EPS growth of 3% is also quite low for such a lofty valuation. I simply do not see the opportunity for multiple expansions unless the company can substantially accelerate its growth rates in the near term.

Investors Takeaway

Edwards Lifesciences is the clear leader in the fast-growing TAVR market with a strong moat, but I do not think the company currently presents a compelling investment case. Revenue growth has rebounded from 1.4% in Q4 last year to 8.8% in the latest quarter but this is still below the company's historical average growth rates of mid-double digits. The bottom line was particularly weak as spending outpaced growth. Considering its financials, the elevated valuation seems unjustified and should limit its upside potential. I do not think the current risk-to-reward is favorable and I rate the company as a hold.

For further details see:

Edwards Lifesciences: Valuation Seems Still Too Elevated