FCT - EFR: Hedge Your Interest-Rate Risk At A Discount

2023-12-13 23:16:56 ET

Summary

- Eaton Vance Senior Floating-Rate Trust offers a current yield of 11.54%, in line with other funds investing in floating-rate senior loans.

- The fund has performed better than typical bond funds, with only a 1.56% decline over the past three years compared to a 17.91% decline in the Bloomberg US Aggregate Bond Index.

- EFR primarily invests in senior floating-rate loans, which have stable prices and can provide a reasonable level of income to investors.

- The fund is fully covering its distribution with NII, so it is not unnecessarily depleting its assets.

- Eaton Vance Senior Floating-Rate Trust is currently trading at a discount on net asset value.

The Eaton Vance Senior Floating-Rate Trust ( EFR ) is a closed-end fund that income-focused investors can employ in pursuit of their goals. The fund would appear to do this job quite admirably, as its 11.54% current yield is in line with other funds that primarily invest in floating-rate senior loans. For example, consider the following yields that are currently being offered by the fund's peers:

| Fund |

| Current Distribution Yield |

| Eaton Vance Senior Floating-Rate Trust |

| 11.54% |

| Apollo Senior Floating Rate Fund ( AFT ) |

| 12.35% |

| Eaton Vance Floating Rate Income Fund ( EFT ) |

| 11.51% |

| Blackstone Long-Short Credit Income ( BGX ) |

| 11.67% |

| First Trust Senior Floating Rate Income Fund II ( FCT ) |

| 11.87% |

This is something that income investors should appreciate. After all, all of these funds are investing in very similar assets so a fund possessing an especially high or an especially low yield could be a sign that the market either perceives a high level of risk with respect to the fund or has greatly overvalued it. As we can see, this does not appear to be the case with this fund today.

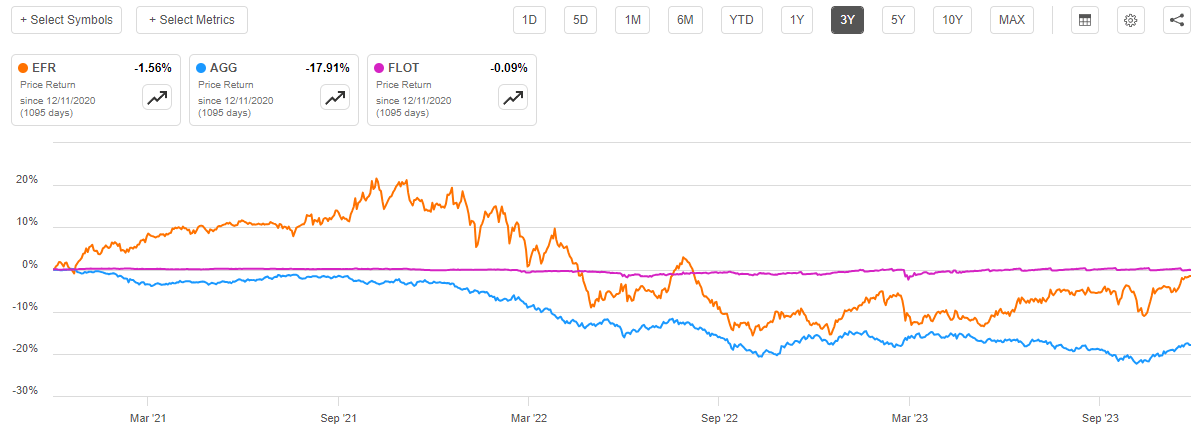

As everyone reading this is no doubt well aware, the past few years have been very challenging for bonds and other fixed-income investments. After all, bond prices tend to move inversely to interest rates, and interest rates have risen over the past three years. The Eaton Vance Senior Floating-Rate Trust has held up much better than a typical bond fund, though. As we can see here, the fund's shares have only declined by 1.56% over the past three years. That is substantially better than the 17.91% decline of the Bloomberg US Aggregate Bond Index (iShares Core U.S. Aggregate Bond ETF ( AGG )) over the same period, but it has unfortunately not been as good as the American floating-rate index (iShares Floating Rate Bond ETF ( FLOT )), which has been almost perfectly flat:

{kind=link}

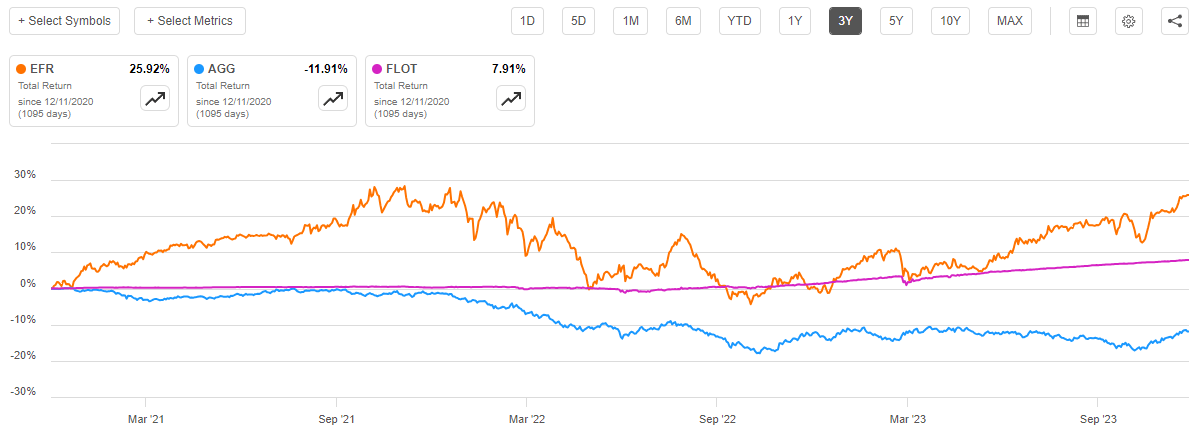

As I have pointed out before though, bonds and other fixed-income securities tend to deliver the overwhelming majority of their total returns in the form of direct payments to investors. After all, these securities do not have any net capital gains over their lifetimes. This is especially true with bonds held by a closed-end fund, as closed-end funds themselves typically pay out all of their investment profits to the shareholders in the form of distributions. As such, we should look at the performance of these funds after accounting for the impact that the distributions have on overall returns. It is certainly possible that a large enough distribution can completely offset share price declines. This chart does exactly that:

{kind=link}

This is mostly what we expected to see. In short, the Eaton Vance Senior Floating-Rate Trust completely dominated both the aggregate bond index and the American floating-rate index. This is largely because of its much higher yield compared to either of these indices, along with the fact that the prices of the securities that are held by the fund do not really change much when interest rates do.

About The Fund

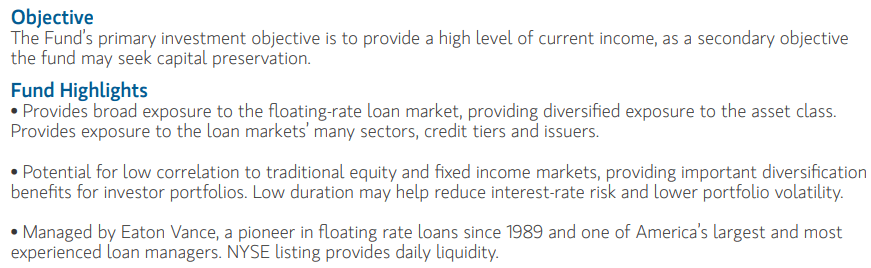

According to the fund's webpage , the Eaton Vance Senior Floating-Rate Trust has the primary objective of providing its investors with a high level of current income. This makes sense when we consider the fund's strategy, which is unfortunately not described on the website. The fund's fact sheet includes this information, however:

{kind=link}

In short, the fund seeks to achieve its objectives by investing its assets into senior floating-rate loans, which are sometimes called "leveraged loans." Fidelity Investments includes an excellent definition of these securities on its website :

Leveraged loans - also known as floating-rate loans or bank loans - are loans made by banks or other financial institutions that are then sold to investors. Companies may use the money they get to refinance their debt, fund mergers and acquisitions, or finance projects. The companies that receive these loans typically have credit ratings that are below investment grade. These loans usually have a term of between 5 to 7 years, though the borrower can repay them at any time. They are secured by collateral such as the borrower's real estate and equipment, as well as intellectual property including brands, trademarks, and customer lists.

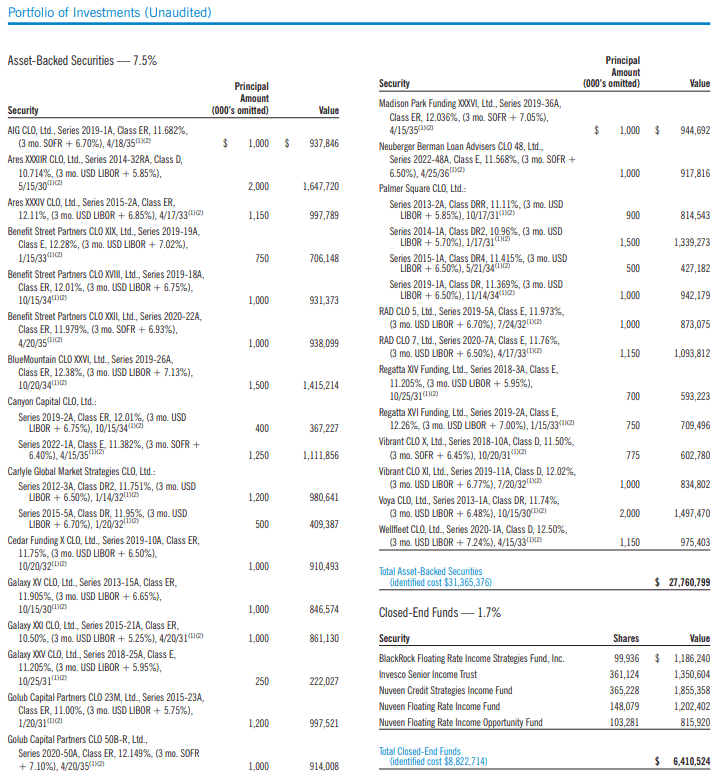

In other words, these are essentially junk bonds with coupons that deliver a payment to the investor that varies based on some interest-rate benchmark. A look at the first page of the fund's semi-annual report that details its current holdings reveals securities whose coupon rate varies based on LIBOR or SOFR:

{kind=link}

I have occasionally seen securities that have coupon yields based on the ten-year U.S. Treasury rate as well. There are none of those shown in this screenshot, however, and LIBOR or SOFR is much more common anyway because these are both short-term interest rate benchmarks. The variable rates paid by floating-rate securities are normally based on short-term interest rates, such as the overnight rate.

As of the time of writing, the 3 mo. LIBOR is at 5.63% and the SOFR is at 5.33874%. As such, we can very quickly see that many of the securities shown above will have current coupon rates that are well above 10%. This is obviously a very big change from two years ago when the Federal Reserve kept interest rates at 0% or very close to it. It is also something that income-focused investors should appreciate, as today's interest rates allow these securities to boast yields that can actually result in investors receiving a reasonable level of income from the assets in their portfolios. After all, a 10% yield of a $1 million portfolio is $100,000 per year, and that is enough to live a reasonably comfortable lifestyle in some parts of the United States.

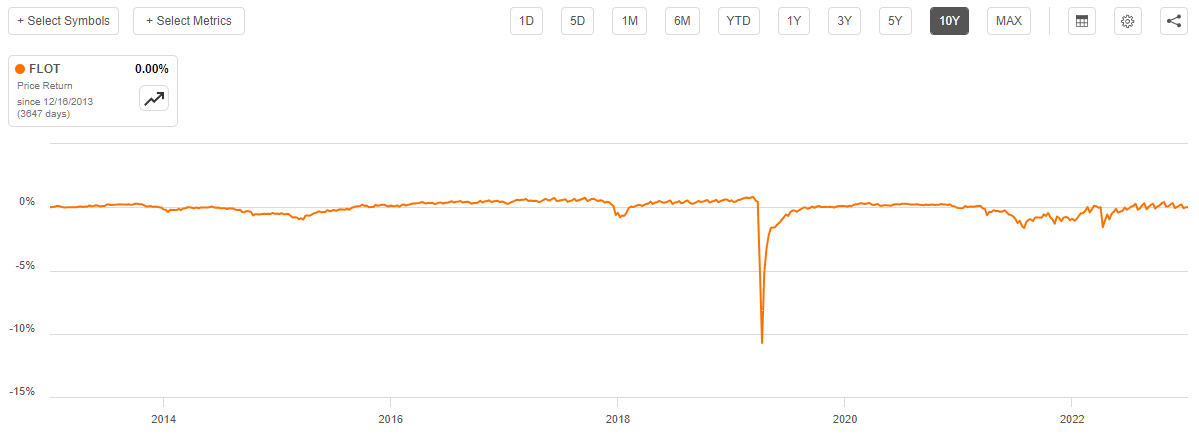

One of the biggest advantages of floating-rate loans can be found in the fact that their prices tend to be remarkably stable over time. As we saw earlier in this article, the floating rate note index has been almost perfectly flat over the past three years despite the rapid increase in interest rates that we saw in 2022 and the first half of 2023. This extends out to include the past ten years:

{kind=link}

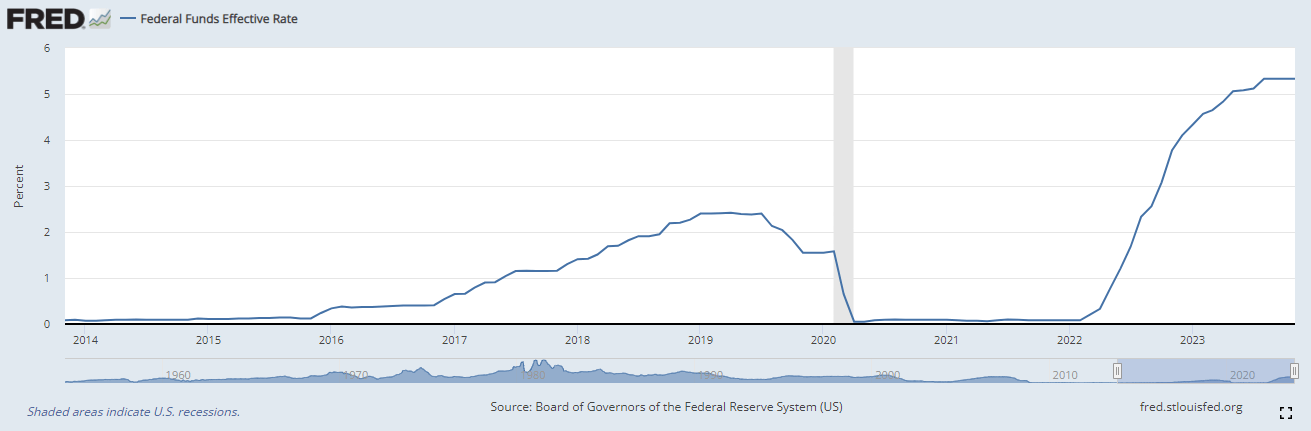

While interest rates were generally low over this period, there were some changes. In particular, the nation's central bank tried to raise interest rates in 2018 in response to the economy beginning to heat up. Interest rates were not at 0% prior to the COVID-19 pandemic, after all. We can see this simply by looking at a chart of the effective Federal Funds rate over the same period:

{kind=link}

As we can see, interest rates generally increased over the 2015 to 2019 period, and again in 2022. Despite this, the floating rate note index was flat, other than a very brief shock in 2020 right when the pandemic broke out. At that time, investors were basically just panic-dumping everything due to the uncertainty about COVID-19. This steep decline corrected itself very rapidly, however. The takeaway here is that floating-rate securities tend to be very stable in price regardless of interest rate movements. That should extend to the securities in the Eaton Vance Senior Floating-Rate Trust, and it is in fact one of the biggest reasons why this fund's share price did not decline nearly as much as the Bloomberg U.S. Aggregate Bond Index over the past three years.

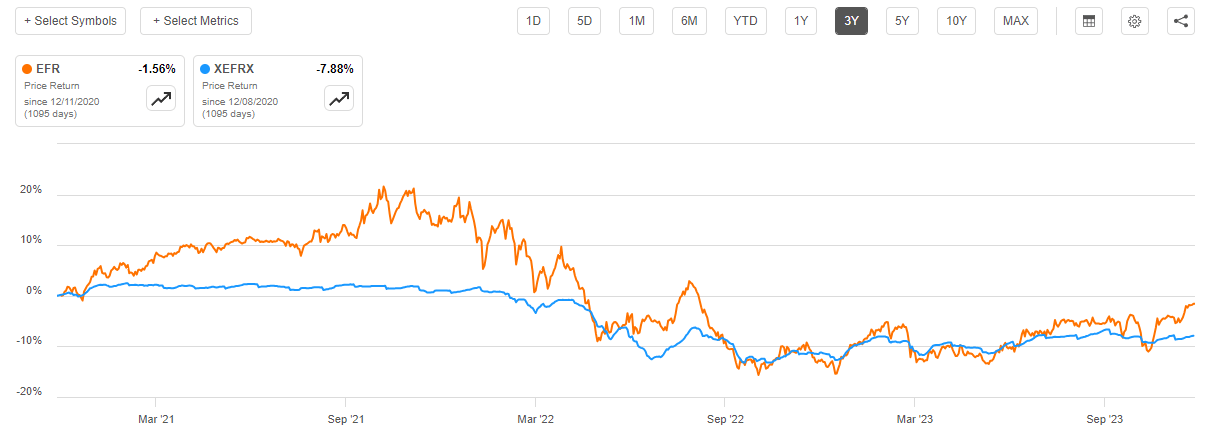

With that said though, the fund's net asset value per share has not held up nearly as much. As we can see here, the fund's net asset value per share declined by 7.88% over the past three years:

{kind=link}

This is certainly concerning, as it could suggest that the fund has been making larger distributions than it can actually afford. In fact, that is the only explanation that I can actually come up with, as the securities in the portfolio should have held up reasonably well. The fund's leverage might have also caused some losses, which we will discuss later in this article. Overall, though, this fund's net asset value did hold up much better than the aggregate bond index, so the thesis is still generally sound. In short, the fund should be able to act as a hedge against rising interest rates.

It may be more important to have that hedge against rising interest rates than some market participants seem to believe. As I pointed out in a recent article , there is no guarantee that the Federal Reserve will cut interest rates next year. In fact, I have seen a number of reports from independent analysts and central bank watchers over the past week or two that strongly suggest that the market is wrong about the magnitude of interest rate cuts next year. That was the case in the first half of 2023 as well, and we all remember what happened to the stock and bond markets over the summer. As such, it might be a good idea to include something in your income portfolios that exhibits a certain amount of neutrality with respect to interest rates. This fund appears to be one option, as it has already been shown that it can deliver a reasonable performance during periods of rising interest rates.

As mentioned earlier, senior loans are essentially junk bonds with floating coupon rates. The securities held by these funds are backed by companies that may not have the best credit ratings or the strongest balance sheets. This is something that might be concerning to those investors who are highly risk averse. After all, such companies are generally considered to be much more likely to default than an investment-grade company. Fortunately, this fund appears to be taking precautions against the losses that could accompany such an event.

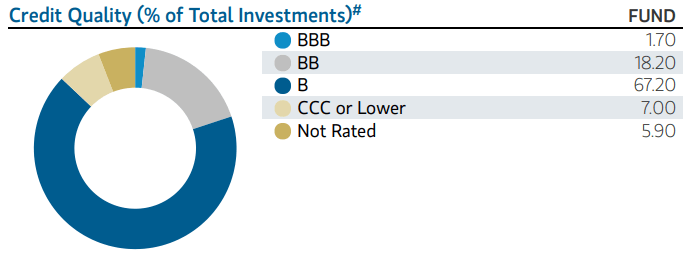

Let us have a look at the credit ratings of the securities that are currently held by the Eaton Vance Senior Floating-Rate Trust. Here is a high-level summary:

{kind=link}

An investment-grade security is anything rated BBB or higher. As we can clearly see, that only describes 1.70% of the assets in the fund. The remainder of the securities are speculative-grade assets. However, 85.40% of the securities carry either a BB or B rating. These are the two highest possible credit ratings for junk bonds. According to the official bond ratings scale , companies whose securities carry one of these two ratings currently have the financial capacity to carry their existing debt even in the event of a short-term economic shock. As such, while these securities certainly carry a higher risk of losses due to default than an investment-grade firm, the risk is probably not worth overly worrying about. This is especially true when we consider that this fund's portfolio consists of securities from 340 issuers and no single issuer accounts for more than 1.15% of the fund. As such, even if a single issuer were to default, it is unlikely that it would have a noticeable impact on the fund's assets.

Therefore, this fund should prove to be a reasonably safe investment over the next year or two regardless of whatever happens in the broader economy.

Leverage

As is the case with most closed-end funds, the Eaton Vance Senior Floating-Rate Trust employs leverage as a method of boosting the effective yield that it receives from its portfolio. I explained how this works in a number of previous articles. To paraphrase myself:

Basically, the fund borrows money and then uses this borrowed money to purchase bonds and other income-producing assets. As long as the yield that the fund receives from the purchased asset is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that a fund is not employing too much debt since that would expose us to an excessive level of risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Eaton Vance Senior Floating-Rate Trust has leveraged assets comprising 34.11% of its total portfolio. This is obviously slightly above the one-third level that I would really like to see. However, in this case, it is probably okay. After all, the real problem with leverage is that assets can decline in price, but leverage does not, so it amplifies the losses. However, the securities that this fund is investing in tend to remain fairly stable regardless of the broader macroeconomic conditions. As such, the fund can probably carry a higher level of leverage than could a common equity fund or similar. We probably do not have to worry too much about this fund, especially since its leverage is not very much different than other floating-rate loan funds.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Eaton Vance Senior Floating-Rate Trust is to provide its investors with a very high level of current income. In order to achieve this goal, the fund invests in a portfolio that primarily consists of floating-rate leveraged loans. As we have seen, some of these securities have coupon yields that are well into the double digits based on the current LIBOR and SOFR benchmarks. The fund collects the coupon payments that it receives from these securities, and even employs leverage to allow it to collect payments from more securities than it can control simply through the use of its own equity. The fund pools all of this money together and then pays it out to its shareholders net of its expenses. As the fund's assets are currently boasting fairly attractive yields, we can assume that this fund's shares will also boast a fairly high yield.

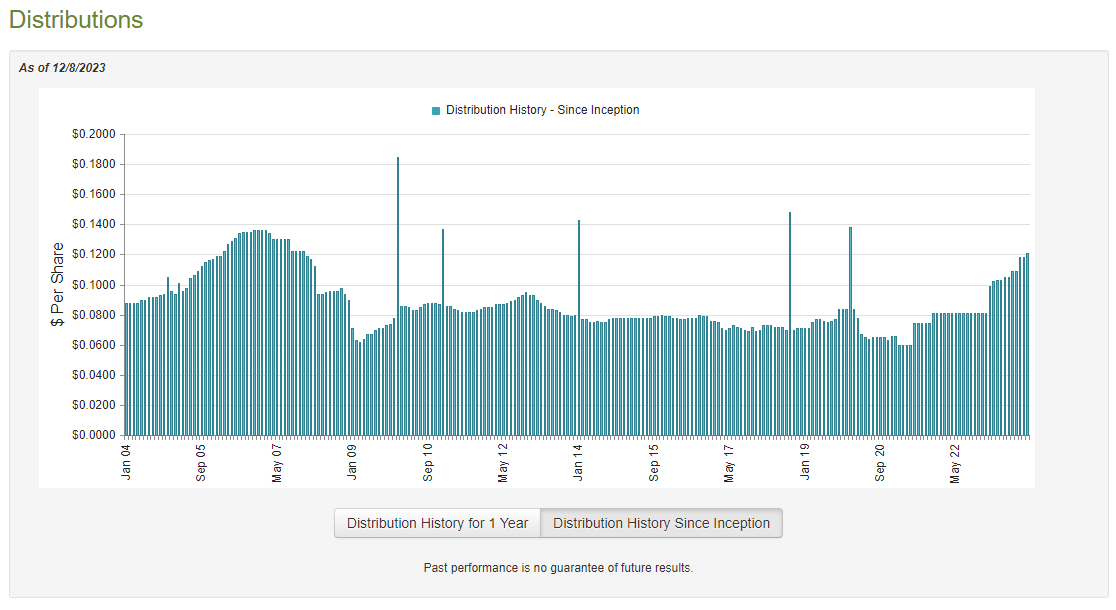

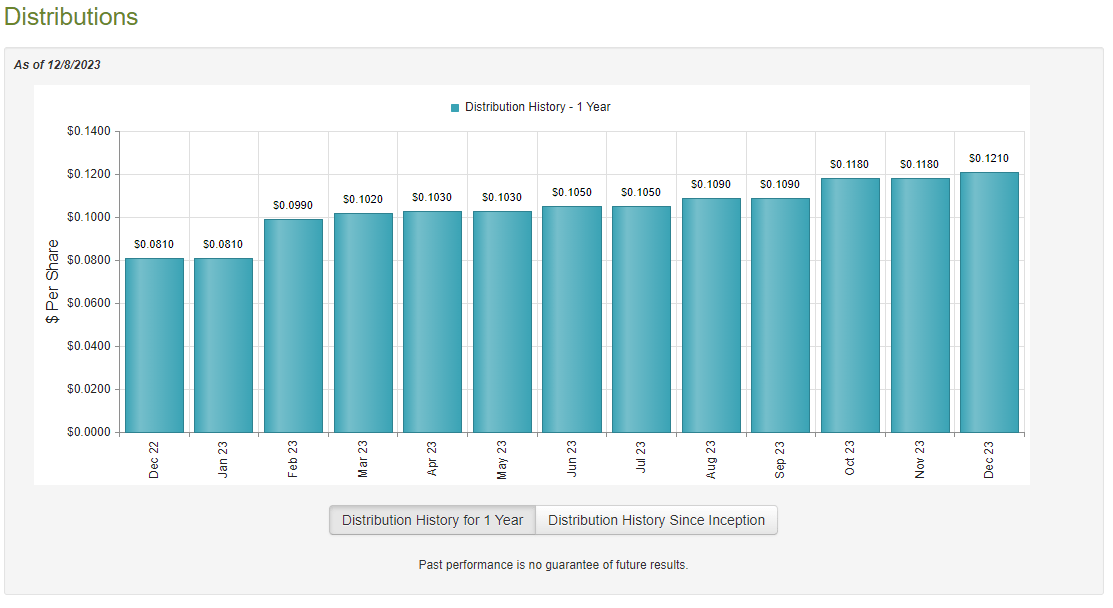

This is certainly the case as the Eaton Vance Senior Floating-Rate Trust currently pays a monthly distribution of $0.1210 per share ($1.452 per share annually), which gives it an 11.54% yield at the current share price. As was mentioned in the introduction, this is comparable to the yields of many peer funds right now. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years. In fact, as we can see here, the fund's distribution has varied significantly over time:

{kind=link}

The fact that the fund's distribution has been increased and decreased numerous times over the years will likely prove to be something of a turn-off for those investors who are seeking to receive a consistent and secure income from the assets in their portfolios. However, if we consider the nature of the assets in this fund then the distribution history makes a great deal of sense. After all, senior loans tend to be very stable in terms of price so the return that they deliver depends on the coupon yield, which in turn depends on the level of interest rates. The fund increases its distribution when interest rates are rising and reduces it when interest rates decline. The fund has raised its distribution seven times over the past twelve months for this reason:

{kind=link}

This contributes to our overall thesis of this fund being a hedge against rising rates. After all, since both stocks and traditional fixed-rate bonds seem to decline when interest rates go up, this fund is one of the few things that can benefit from rising interest rates.

As is always the case though, we should have a look at the fund's finances to ensure that it can actually afford the distribution that it is paying out. After all, we do not want the fund to be over-distributing and destroying its net asset value in the process. That is not sustainable over any sort of extended period.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report is its semi-annual report that corresponds to the six-month period that ended on April 30, 2023. This document was linked earlier in this article. The fact that this is the newest financial report currently available is a bit disappointing, as it will not provide us with any information about the fund's performance over the past seven months. However, it should still give us a good idea of how well the fund performed in November and December of last year, which were somewhat challenging months for many asset classes. It will also show us how well the fund did in the first four months of this year, which was something of a loose money environment as investors rushed to snap up bonds in anticipation of a pivot by the Federal Reserve.

During the six-month period, the Eaton Vance Senior Floating-Rate Trust received $553,180 in dividends and $25,293,040 in interest from the assets in its portfolio. This gives the fund a total investment income of $25,846,220 during the period. The fund paid its expenses out of this amount, which left it with $19,858,777 available for shareholders. That was more than sufficient to cover the $15,958,642 that the fund paid out in distributions over the period.

The same thing happened during the preceding full-year period. During the full-year period that ended on October 31, 2022, the fund had a net investment income of $26,681,859 and paid out $25,476,811 in distributions.

It therefore appears that this fund is simply paying out its net investment income to the shareholders. This is exactly what we want to see a debt fund do. The fund does not appear to be over-distributing, although it will probably have to cut its distribution if short-term interest rates start to decline. That would almost certainly be the result if the market is correct about an impending pivot by the Federal Reserve.

Valuation

As of December 8, 2023 (the most recent date for which data is currently available), the Eaton Vance Senior Floating-Rate Trust has a net asset value of $12.98 per share but the shares trade for $12.58 each. This gives the fund's shares a 3.08% discount on net asset value at the current price. That is a reasonable discount, although not quite as good as the 4.33% discount that the shares have averaged over the past month. As such, it might be possible to get a better price by waiting a bit, but I will admit that I am not sure that it will make a huge difference in your overall return if you do wait for a better entry point. As long as you are buying the fund at a discount, it is probably fine.

Conclusion

In conclusion, the Eaton Vance Senior Floating-Rate Trust appears to be a reasonable way to hedge interest rate risk. That is something that could be important right now as there is no guarantee that the central bank will actually cut the Federal Funds rate to the degree that the market expects, and it could be a good idea to hold something that will benefit if rates remain higher than the market is currently pricing. This fund is one way to protect yourself against this risk. The fund's finances appear to be very strong, as it is simply paying its distribution out of net investment income. The fact that this fund is trading for a discount further strengthens the thesis.

For further details see:

EFR: Hedge Your Interest-Rate Risk At A Discount