EFT - EFT: This 8.04%-Yielding Debt Fund Is A Winner For Income Investors Today

Summary

- Eaton Vance Floating Rate Income Trust invests in a portfolio of floating-rate securities in an effort to give its investors a high current income.

- Floating-rating securities have a marked advantage over ordinary bonds in markets like we are in today.

- The closed-end fund should prove to be a reasonably solid holding for the near term until the Federal Reserve finally pivots.

- The CEF's distribution should be reasonably secure, and this is one of the few Eaton Vance funds to hike its payout recently.

- The fund is currently trading at an attractive valuation.

Without a doubt, one of the biggest problems facing Americans today is the incredibly high inflation that has been pervading the economy. There has not been a single month over the past year in which inflation was less than 6.5% year-over-year and in most months, it was substantially higher. This has had a huge impact on the poor and the middle class, many of whom are now taking on second jobs or entering the gig economy simply to make ends meet.

In fact, according to a recent Prudential Pulse survey , approximately 81% of Generation Z members and 77% of Millennials have either taken on second jobs or entered the gig economy just to earn the extra money that they need to feed themselves and heat their homes. This is not surprising, considering that inflation has been most prominent in food and energy, as anyone that has paid their electric bill or gone to the grocery store lately can attest.

Fortunately, as investors, we can put our money to work for us instead of needing to sacrifice more of our precious time earning money just to pay the bills. One of the best ways that we can do this is by purchasing shares of a closed-end fund that specializes in the generation of income. These funds are nice because they provide easy access to a diversified, professionally-managed portfolio that can usually deliver a higher yield than anything else in the market. In fact, in many cases, these funds can boast yields that are higher than any of the underlying assets possesses. This is exactly the kind of thing that anyone investing for income can appreciate.

In this article, we will discuss the Eaton Vance Floating Rate Income Trust ( EFT ), which is one fund that investors can use for this purpose. As of the time of writing, the fund boasts an 8.04% yield, which is certainly sufficient to boost anyone’s income. Indeed, this would result in a $1 million investment paying $80,400 annually, which is more than most full-time jobs. Fortunately, you do not have to pay through the nose for this income, as the fund is currently trading at a very attractive price relative to its assets. As such, let us investigate and see if this fund could deserve a place in your portfolio.

About The Fund

According to the fund’s webpage , the Eaton Vance Floating-Rate Income Trust has the stated objective of providing its investors with a high level of current income. This is not surprising for a fixed-income fund as fixed-income securities provide nearly all of their returns to investors through direct payments. The potential for capital gains from these securities is quite limited because they do not have a link to the growth and prosperity of the issuing company. After all, a company will not increase the amount that it pays its creditors simply because its profits improve.

The market price of fixed-income securities is largely dictated by interest rates. Basically, when interest rates increase, the market price of bonds will go down. This is because the yield of newly issued bonds will go up in such an environment and nobody will buy an existing bond with a lower interest rate instead of a new identical one with a higher yield. Thus, the price of existing bonds must go down so that they deliver the same yield-to-maturity as a newly-issued bond with identical characteristics.

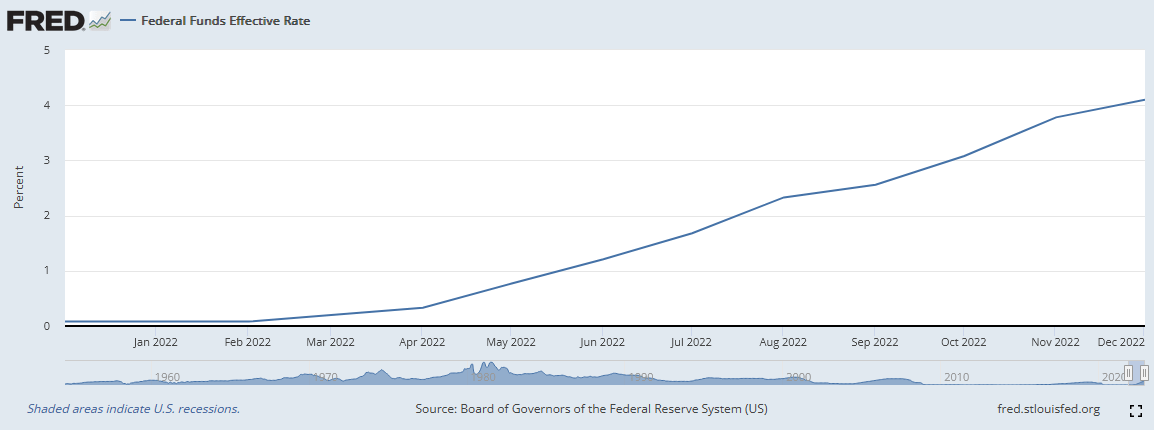

As everyone reading this is no doubt well aware, the Federal Reserve has been raising interest rates over the past year in an effort to combat inflation. As we can see here, the effective federal funds rate (the rate that commercial banks charge each other for overnight loans) went from 0.08% a year ago to 4.10% today:

{kind=link}

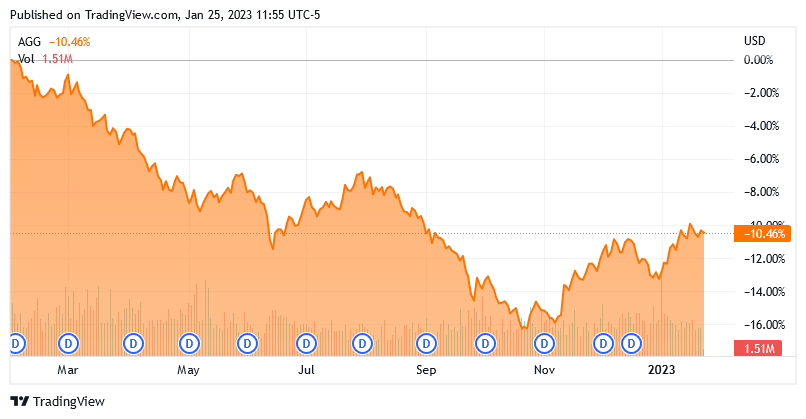

This has had the effect of suppressing bond prices due to their inverse correlation with interest rates, as just discussed. Over the past year, the Bloomberg U.S. Aggregate Bond Index ( AGG ) has declined 10.46%:

{kind=link}

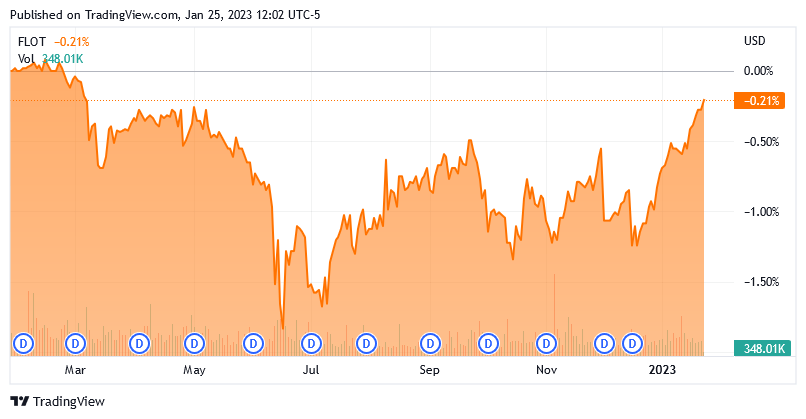

This is how the Eaton Vance Floating-Rate Income Trust is unique. This fund does not invest in traditional fixed-rate bonds. Rather, the fund buys fixed-income securities that have a floating interest rate. Think of these like credit cards or adjustable-rate mortgages. Basically, when the interest rate in the economy increases, the interest rate paid by the issuer of these securities also increases. This overcomes most of the problems of holding bonds in a rising-rate regime as these securities should hold their value reasonably well. This is immediately evident in the fact that the Bloomberg U.S. Floating Rate Note <5 Years Index ( FLOT ) is basically flat over the past year:

{kind=link}

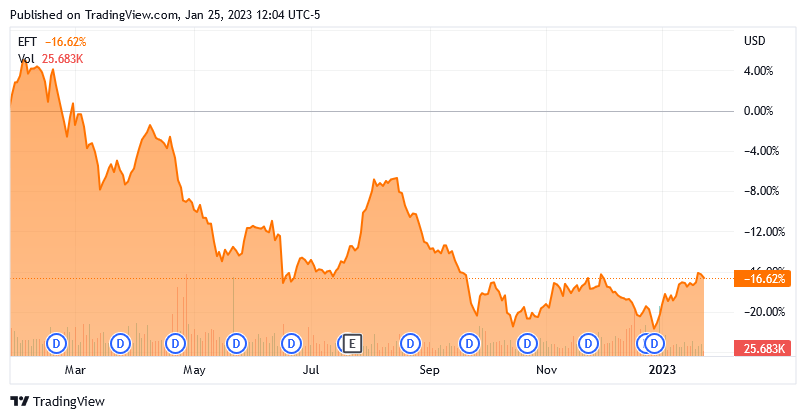

Unfortunately, the Eaton Vance fund has not performed anywhere near as well. The fund is actually down 16.62% over the same period:

{kind=link}

Although the Eaton Vance fund does have a substantially higher yield than the index, this is not nearly enough to make up the difference. This is admittedly a bit difficult to understand unless the fund is either not investing in floating-rate securities like it claims to be or it is over-distributing. We should investigate further in order to try to explain the performance discrepancy.

Floating-rate debt securities are typically issued by companies that have a great deal of debt or somewhat volatile revenue. In short, these securities are typically issued by companies that cannot obtain more traditional debt financing. This is something that may concern more risk-averse investors because companies like this tend to be more likely to default on their obligations. That is a risk that extends to the fund because any losses that the fund suffers will end up adversely affecting investors in the fund.

As such, we want to investigate the possibility that the fund will actually lose money due to defaults. There are a few major rating agencies that make this an easy process though as they assign letter grades to most debt issues that ostensibly inform investors of the risk that the issuing company will default on its debt obligation. Here is a broad overview of the credit ratings that have been assigned to the securities in the fund’s portfolio:

Eaton Vance

An investment-grade security is anything rated BBB or above. As we can see, that is only 1.1% of the portfolio. The overwhelming majority of the securities in this fund are rated either BB or B, as these two ratings are assigned to 86.0% of the portfolio. It may be comforting to learn that these securities are not at a particularly high risk of loss due to default. According to the official bond ratings scale , companies with these ratings have the sufficient financial strength to cover their debt obligations and should be able to weather a short-term economic downturn with minimal difficulty.

These firms may, admittedly, be vulnerable to a long-term economic shock but such an event has not occurred since the Great Depression. Thus, we can be fairly confident that the default risk here is fairly low despite the fact that the fund is invested in speculative-grade securities.

Another way that the fund can protect us against the risk of principal loss is by investing in a large number of assets. This is because having a large number of positions should ensure that no individual issuer makes up a noticeable proportion of the portfolio. Thus, if any individual company were to default, we would not notice it when looking at the portfolio in aggregate. The fund currently holds positions in 512 securities, which should give it the kind of diversification that is needed to protect itself adequately. This does, in fact, appear to be the case as there is no position in the fund that accounts for more than 1.02% of its assets:

Eaton Vance

Although 1.02% seems like a lot, the truth is that every asset in the fund has a yield that is currently significantly above that. Thus, the only thing that a 1.02% loss would do is offset a bit of the fund’s interest income. It is nothing that is really worth worrying about. Thus, risk-averse investors should be reasonably satisfied that their money is reasonably safe with this fund. With that said, the fund is still vulnerable to losses if a large number of companies default all at once but in such a situation, the country will have far bigger problems than just a few investors losing some money due to debt defaults.

Leverage

In the introduction, I stated that closed-end funds like the Eaton Vance Floating-Rate Income Trust have the ability to generate yields that are significantly higher than any of the underlying assets possess. One of the ways in which this is accomplished is through the use of leverage. In short, the fund is borrowing money and then using that borrowed money to purchase floating-rate securities. As long as the yield of the purchased assets is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the overall portfolio yield. As the fund is capable of borrowing at institutional rates, which are significantly lower than retail rates, this will usually be the case.

However, the use of leverage is a double-edged sword. This is because it boosts both gains and losses. As such, I generally do not like to see a fund’s leverage above a third as a percentage of its assets because that exposes us to too much risk. Unfortunately, this fund fails that requirement as its levered assets comprise 37.54% of the portfolio as of the time of writing. That is significantly above the level that we usually like to see. However, as this fund invests mostly in reasonably safe assets, it is probably okay at the current level. We will want to keep an eye on this though as we do not want the fund’s leverage to increase much beyond the current level.

Distribution Analysis

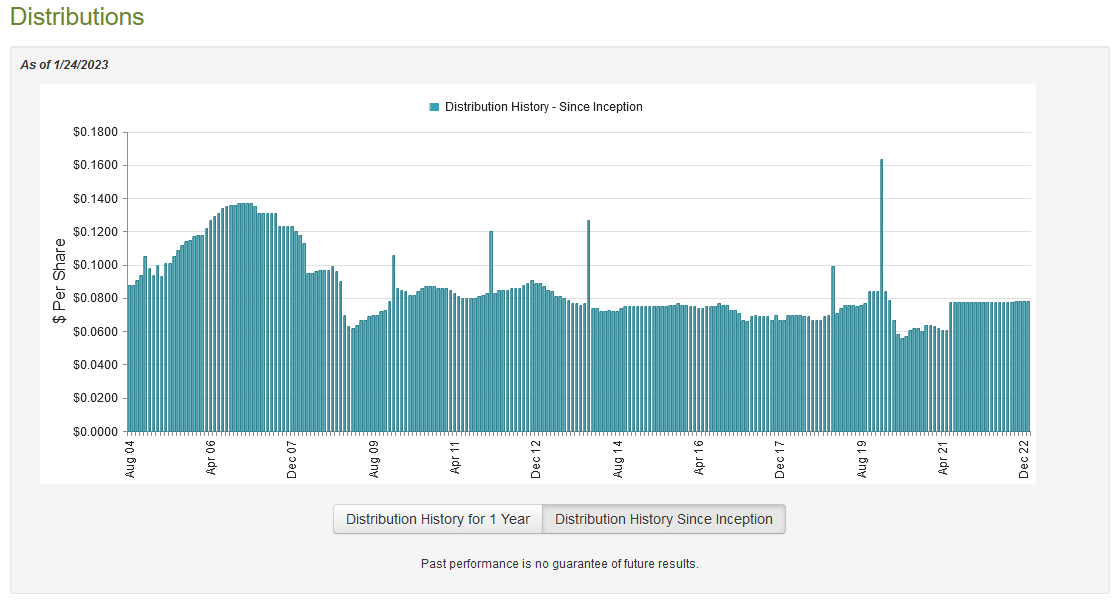

As stated earlier in this article, the primary objective of the Eaton Vance Floating-Rate Income Trust is to provide its investors with a high level of current income. In order to achieve this objective, the fund invests in floating-rate securities that tend to have a fairly high yield, particularly today. It then applies leverage to boost the yield further. As such, we might assume that this fund will boast a fairly high distribution yield. This is certainly true as it pays out a monthly distribution of $0.078 per share ($0.936 per share annually), which gives it an 8.04% yield at the current price. The fund’s distribution has varied quite a bit over the years, although this is one of the only Eaton Vance funds that increased its distribution back in October:

{kind=link}

The fund’s distribution tends to vary with interest rates. As befits a floating-rate fund, it seems to increase the distribution when interest rates are high and decrease it when interest rates are low, but it is certainly not a perfect correlation. The fact that the fund’s distribution tends to vary over time is something that may be problematic to those investors that are looking for a safe and secure source of income to use to pay their bills. However, as an opportunistic position into rising interest rates, it makes a lot of sense. This is, indeed, how I am profiting from a similar floating-rate fund, the Apollo Tactical Income Fund ( AIF ), in my own portfolio today.

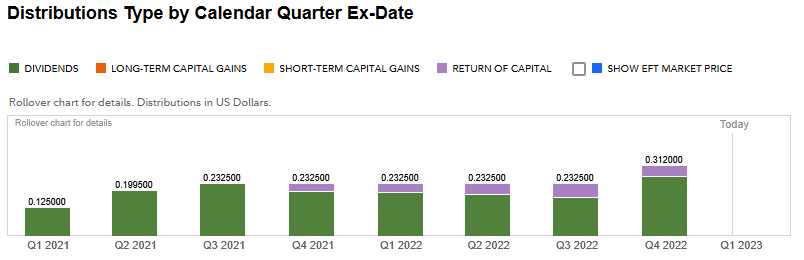

It may be somewhat comforting that the fund’s distributions are mostly classified as dividend income, although there is some return of capital in the recent ones:

{kind=link}

A return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period and thus may be somewhat concerning. However, the majority of the fund’s distributions are classified as dividend income, which is generally the most sustainable source of funding for distribution since they are simply the fund paying out the interest that it receives from the investments in its portfolio. However, as I pointed out in a previous article , it is possible for these distributions to be misclassified. As such, we should investigate exactly how the fund is paying its distributions in order to determine how sustainable they are likely to be.

Unfortunately, we do not have a particularly recent document to consult for this purpose. The fund’s most recent financial report corresponds to the full-year period that ended on May 31, 2022. As such, it will not give us any real insight into how well the fund performed over the past six months or so. This is disappointing as nearly all of Eaton Vance’s other closed-end funds have released a more recent report.

Nonetheless, this report will still give us a good idea of how well the fund performed in the Federal Reserve’s shift from a loose monetary policy to a tight one. That is an event that had a significant impact on the fund over the past twelve months so it is nice to get a little insight into that. During the full-year period, the Eaton Vance Floating-Rate Income Trust received a total of $714,307 in dividends and another $30,542,985 in interest from the assets in its portfolio.

This gives the fund a total income of $31,257,292 during the period. The fund paid its expenses out of this amount, leaving it with $21,665,970 available for the shareholders. This was almost enough to cover the $24,895,091 that it paid out during the period. The fact that the fund got pretty close to covering its distribution is very nice to see, although it would have been better to see it all covered.

The fund does have other ways to earn the money that it needs to make the distributions, however. One of these methods is through capital gains. Unfortunately, the fund failed at this task during the year. It did manage to achieve net realized gains of $4,304,314 during the period but this was offset by $38,809,832 net unrealized losses. The fund’s assets declined by $195,294,810 during the period after accounting for all inflows and outflows.

That is somewhat misleading though since the fund spent a net of $153,904,061 repurchasing its own shares during the period. Overall, it did manage to cover its distribution through net investment income and net realized gains, although the net unrealized losses are still an issue. Regardless, this one can probably maintain its distribution at the current level since its income probably went up during the second half of 2022 as the yields on its assets adjusted upward.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Eaton Vance Floating-Rate Income Trust, the usual way to value it is by looking at the fund’s net asset value. A fund’s net asset value is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy shares of a fund when we can get them for a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of January 24, 2023 (the most recent date for which data is available as of the time of writing), the Eaton Vance Floating-Rate Income Trust has a net asset value of $12.98 per share but the shares currently trade for $11.58 each. This gives the fund’s shares a 10.79% discount to net asset value at the current price. This is not as good as the 11.42% discount that the shares have averaged over the past month but it is still a reasonable price to pay. Overall, the price is acceptable here.

Conclusion

In conclusion, the Eaton Vance Floating-Rate Income Trust may be worth purchasing today. The fund is one of the few fixed-income funds that actually benefit from rising interest rates and it recently increased its distribution to prove it. The fund currently boasts a reasonably attractive 8.04% yield that it can probably sustain and trades at a discount to the net asset value. Overall, Eaton Vance Floating Rate Income Trust could be a winner today.

For further details see:

EFT: This 8.04%-Yielding Debt Fund Is A Winner For Income Investors Today