GOCO - eHealth Inc.: A Buy And Hold Idea With 50% Upside Potential

2023-03-09 13:51:04 ET

Summary

- This is an in-depth piece on eHealth, and its two main peers - GoHealth and SelectQuote.

- EHTH reported fantastic results for Q4 FY 2022 and offered really solid FY 2023 guidance. The company is making all of the right business moves. This should create a tailwind.

- Perhaps, most importantly, the industry appears to have gotten religion! And with EHTH shares trading at only 41% of book value, they look compelling.

Today, I write to share my Buy and Hold thesis on eHealth, Inc. ( EHTH ). EHTH is a name that has been on my radar, for quite some time. However, it wasn't until the morning of January 25, 2023, where I invested any capital and got long the stock. What got me off the sidelines and comfortable enough to commit capital here was the company's January 24, 2023 pre-announced and then its actual February 28, 2023 Q4 FY 2022 earnings release and conference call, which included FY 2023 guidance. These two events give me comfort that this stock is undervalued, with the stock trading just shy of $10 per share. Moreover, I would argue the shares are well positioned for another leg up, over the next twelve months, as the market works out all the good stuff taking place in this business and industry.

Let's get started.

Why eHealth shares could have another leg up

Quick company background

eHealth is an online private health insurance marketplace. Through its call centers staffed with knowledge agents, its online service platform, and recent technological advancements, which now offer a hybrid enrollment process, with live chat and co-browsing, the company guides its customers - mostly the Medicare population - through enrollment. These plans are very complex and vary by state, so the onboarding process and experience is very important.

The company has extensive relationships with over 200 insurance carriers and offering consumers a broad selection of thousands of Medicare Advantage, Medicare Supplement, Medicare Part D prescription drug, individual, family, small business, and other ancillary health insurance products.

As of FY 2022, the company operates two segments: Medicare and Individual, Family and Small Business. The Medicare business represented 89% of FY 2022 revenue.

The company generates revenue via commission payments paid by health insurance carriers. eHealth service is free to consumers, as a broker, and the company undertakes no underwriting risks.

eHealth very much reminds me of Intuit Inc.'s ( INTU ) TurboTax business.

Peak Valuation of 2019

Before we talk about the present day, let's go back in time, and look at peak valuations, for this sector.

EHTH's two major peers are GoHealth, Inc. ( GOCO ) and SelectQuote, Inc. ( SLQT ).

In the first chart enclosed below, the top portion of the chart captures the enterprise value of all three. In the bottom section of the chart, graphed over the same time period, you can see the blended 24-month EBITDA. So, as I understand it, Bloomberg takes 12 months of actuals and then incorporates forward estimates, of EBITDA, for the subsequent 12 months, hence the 'Blended 24 Months'.

Please note, at the pinnacle, these stocks were trading at EV/ Forward Adj. EBITDA of 11X to 12X!!!

You might have also worked out, at the valuation apex, EHTH's enterprise value was north of $3 billion, SLQT's was north of $5 billion, and GOCO's was north of $7 billion!

{kind=link}

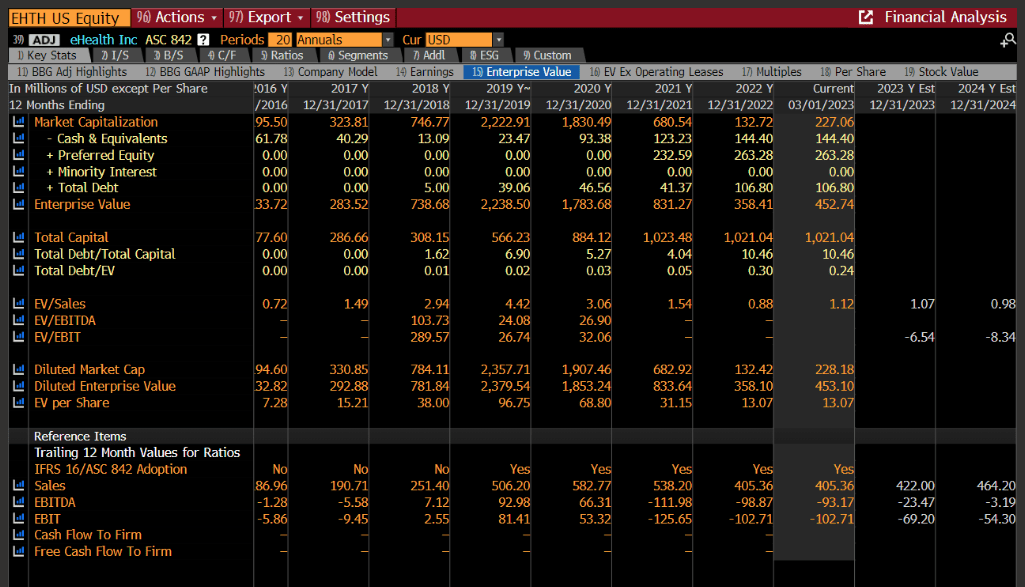

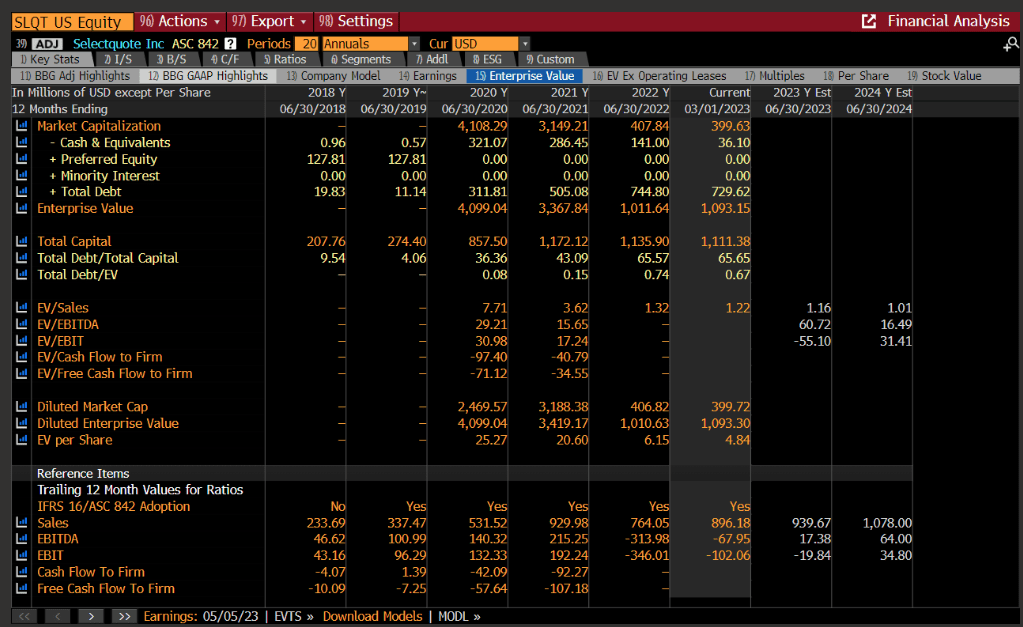

Fast forward to today, and as of last night's closing bell (March 8, 2023) here are the enterprise values of the group:

- EHTH - $451 million : $266 million market capitalization (27.6 million shares x $9.64). $144.4 million of cash, $263.3 million of 8% Convertible Preferred stock (with a stock price of $79.59 per share), and $66.1 million of long term debt. So, including the Convertible Preferred, we are looking at an enterprise value of $451 million.

- SLQT - $1.08 billion : $444.6 million market capitalization (166.5 million shares x $2.67). $36 million of cash and $670 million of long term debt. This translates into a $1.05 billion enterprise value.

- GOCO - $913 million : $419.2 million market capitalization (22 million shares x $19.10). $215 million of cash, $660.4 million of long term debt, and $48.4 million of Preferred stock. This translates into a $913 million enterprise value.

Next, and I think Bloomberg was pulling EBITDA data, as of 12/31/22, before the January 24, 2023, big pre-announcement, across the board, by all three companies would make the SEC filings. The reason I say this is because EHTH only filed its 10-K, on March 1, 2023

EHTH

{kind=link}

SLQT

{kind=link}

GOCO

{kind=link}

Executive Summary

It is really easy to get lost in the weeds, as this is a fairly complex business. As I did all the synthesizing, for you, let's cut to the chase. I will spare readers some of the excruciating details.

On September 23, 2021, EHTH hired its new CEO, Fran Soistman. EHTH's board knew the business and equity was hurdling towards oblivion and they smartly brought in a professional. That said, the 2021 annual enrollment period, for FY 2022, was already sunk, as Soistman couldn't turn a battle ship, on a dime.

{kind=link}

So, Soistman inherited the sins of his predecessor, and as you can imagine, FY 2021 results were really bad.

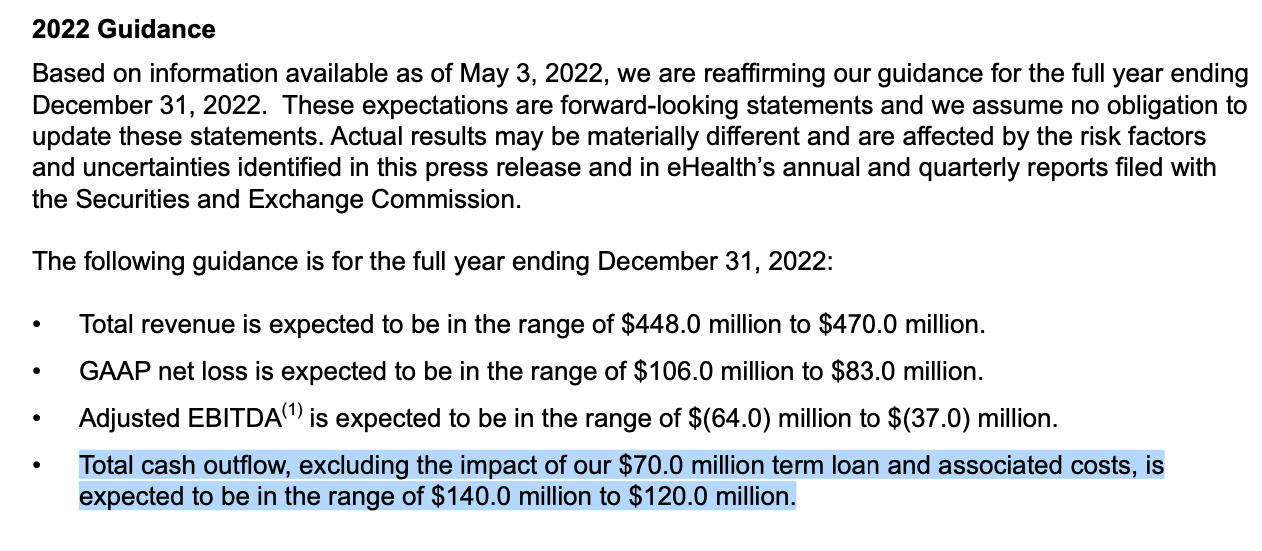

Here is May 3, 2022 guidance:

{kind=link}

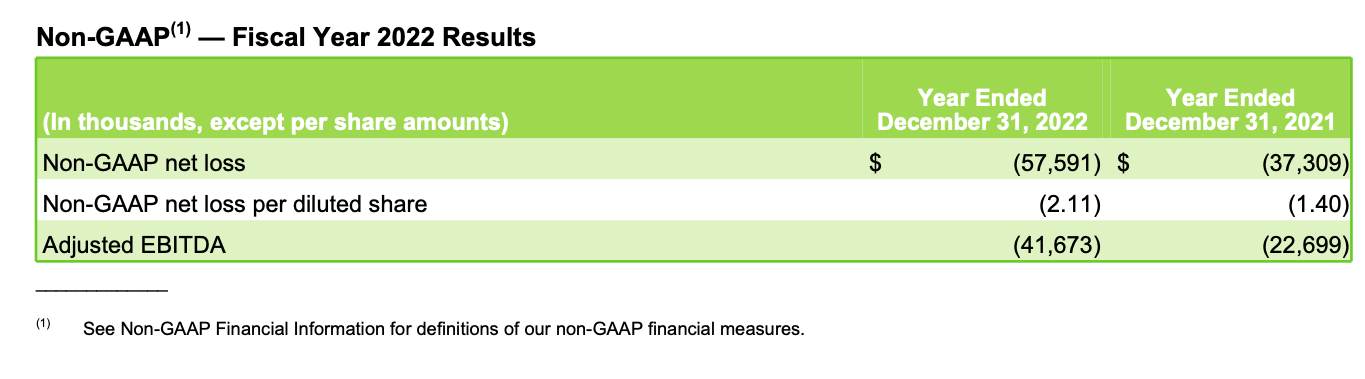

Here is what Soistman delivered:

Adj. EBITDA of negative $41.7 million is towards the high end of guidance.

{kind=link}

Net Cash Outflows of negative $26.9 million, markedly better than the May 3, 2022 guidance of negative $130 million!!

{kind=link}

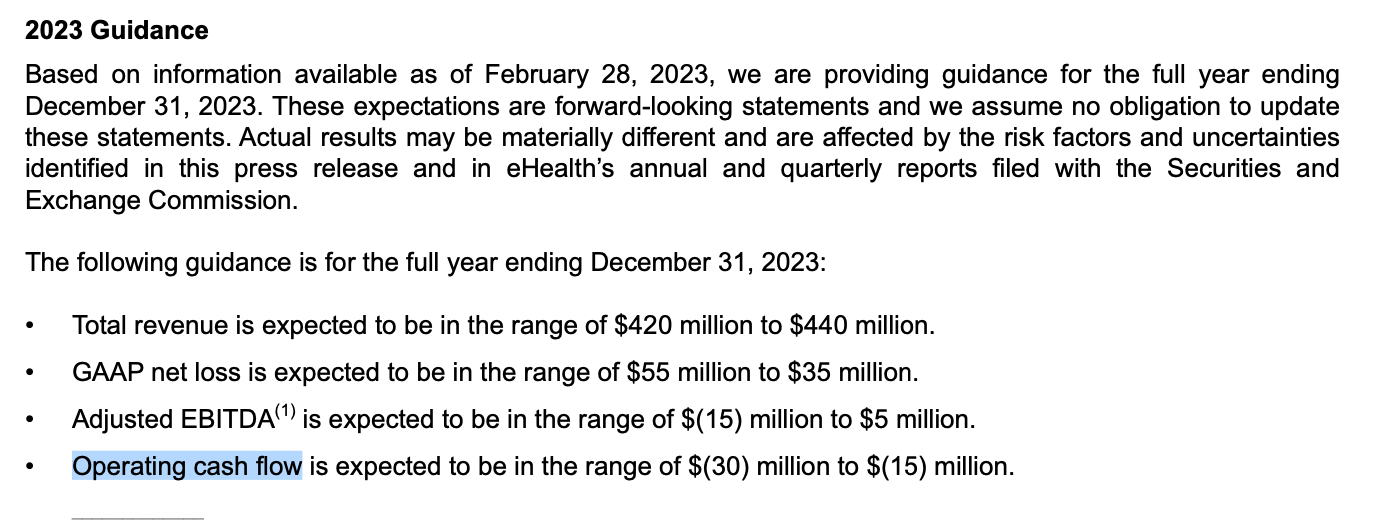

FY 2023 Guidance

So Adj. EBITDA of negative $5 million (mid-point) and negative operating cash flow of $22.5 million (mid-point).

{kind=link}

However, if you listened to the February 28, 2023 conference call, please note:

Given that the majority of initial commissions associated with AEP sales come in during the first quarter, our Q1 2023 cash collections will reflect the reduced enrollment volumes from its last AEP.

At the same time, the cash benefit of the investment we will be making this year to resume enrollment growth this coming AEP will not be felt until Q1 of 2024. In fact, on a trailing 12-month basis, ending March 31, 2024, we expect to be right around breakeven on an operating cash flow basis.

You really need to understand these nuances.

Secondly, and more importantly from Soistman's excellent stewardship, turning this battleship around , is the Industry Got Religion!!!

See Soistman's comments, from the Q4 FY 2022 conference call, from February 28, 2023:

It's important to note that over the past several months, we have observed trends suggesting that our industry peers are taking similar actions in terms of prioritizing sustainable profitability versus growth at all costs. In fact, we believe that the Medicare distribution market has reached an inflection point with brokers refocusing their effort and resources on enrollment margins and member retention.

In addition to bringing a more rational approach to demand generation, which benefits all players in the industry, we see this trend as having a positive effect on consumers as brokers place increased emphasis on the overall customer enrollment experience, including plan fit and a long-term member retention.

Now, given the bizarre price action, in EHTH shares, on February 28, 2023, I went back and read SLQT's February 7, 2023 conference call and GOCO's November 2022 call (they report on March 16, 2023).

Sure enough, the commentary, from both companies exactly echoes Soistman's observations on quality over chasing volume, and a focus on profitability vs. revenue growth.

GOCO's commentary on getting Religion (November 10, 2022):

Exhibit A

I'll now turn to our strategic initiatives. Last quarter, we made a calculated decision to emphasize quality and invest in Encompass. Our shift to focusing on more experienced, high-quality sales agents rather than volume of agent is already proving beneficial.

Last year, this time, just under 13% of our agents had been at GoHealth for at least 1 AEP. This year, just over 94% of agents have been here for at least 1 AEP, and they're delivering the improved quality we were targeting. While it's still early in AEP, our conversion rate is ahead of expectations. With our seasoned agents and new model, October conversion has improved 70% year-over-year. This increased efficiency and a higher rate of conversion in turn makes our marketing spend go even further by making the most of each and every lease.

Exhibit B

I'll now provide further detail on each of these objectives. First, we will continue building out our unified omnichannel marketing engine. Last year, we significantly improved our lead quality and lowered our acquisition costs by narrowing down our marketing channels and campaigns to pursue only the highest ROI initiatives. This year, we see an opportunity to start diversifying our channel mix through a disciplined test-based approach, out of the strong leadership of our CMO, Michelle Barbeau, our reengineered marketing initiatives will be increasingly driven by audience segmentation and targeting, leveraging differentiated messages that highlights what's unique about eHealth and extending touch points with non-converting website visitors as well as our existing customers.

Exhibit C

One of the keys to our branding strategy is to create a lasting awareness of who eHealth is and what we do with the ultimate goal of long-term customer loyalty. The retention effort continues during the enrollment process by providing an excellent customer experience and optimal plan matching through enhanced recommendation analytics tools and carries on post enrollment through continued engagement using a data-driven approach, targeting the optimal times to engage our existing customers.

The success of these initiatives will be measured by our ability to keep our beneficiaries in the eHealth advisory ecosystem even as they switch plans or carriers based on changes to the personal needs or plan design. In aggregate, this new retention strategy will bring a more thoughtful approach to building a year-round personalized relationship with our beneficiaries, focusing on high impact rather than higher volume customer communications.

SLQT's commentary on getting Religion (February 7, 2023):

Exhibit A

As we noted in that release and will speak to today, the most important takeaway is the tangible reinforcement we have observed in our strategic redesign. We firmly belief SelectQuote has optimized their senior segment to drive the right balance of profitability, cash efficiency and growth. Better yet, we believe the strategy is repeatable in a range of future Medicare Advantage seasons.

Exhibit B

We also continue to see improving trends on both policy approval rates and early life retention results, which we largely attribute to the enhancements we made to our sales and marketing strategy in the spring of 2022. Put simply, we’re increasingly confident in the visibility of policyholder persistency and our booked LTVs , which is another key requirement in our mission to deliver predictable profit and growth for our shareholders.

Exhibit C

Again, to be clear, the improvement was predominantly driven by agent mix and lead quality compared to the plan design features in this AEP versus last, and while we focused on better quality this AEP, we believe there is still a significantly large market to grow our business in the future. This was evident even this AEP as our tenured agents drove higher close rates, which created more policy volume than expected on our budgeted marketing and lead spend.

Now if we move down the page, you can see a significant reduction in our marketing cost per approved policy, which were down 50%. Much of this improvement is explained by the close rates of our agents, but SelectQuote also prioritized the most optimal marketing channels based on lead quality and cost. The end result was a strong senior EBITDA margin of 37% for the quarter and significantly improved cash efficiency in the policies book compared to recent years. Ryan will present views on each of those KPIs later in our remarks. Put bluntly, a strategic focus on operating leverage was exactly what our senior business needed, and we’re thrilled with the execution of our teams in the season thus far.

Other Nuances:

From SelectQuote's conference call and slide deck:

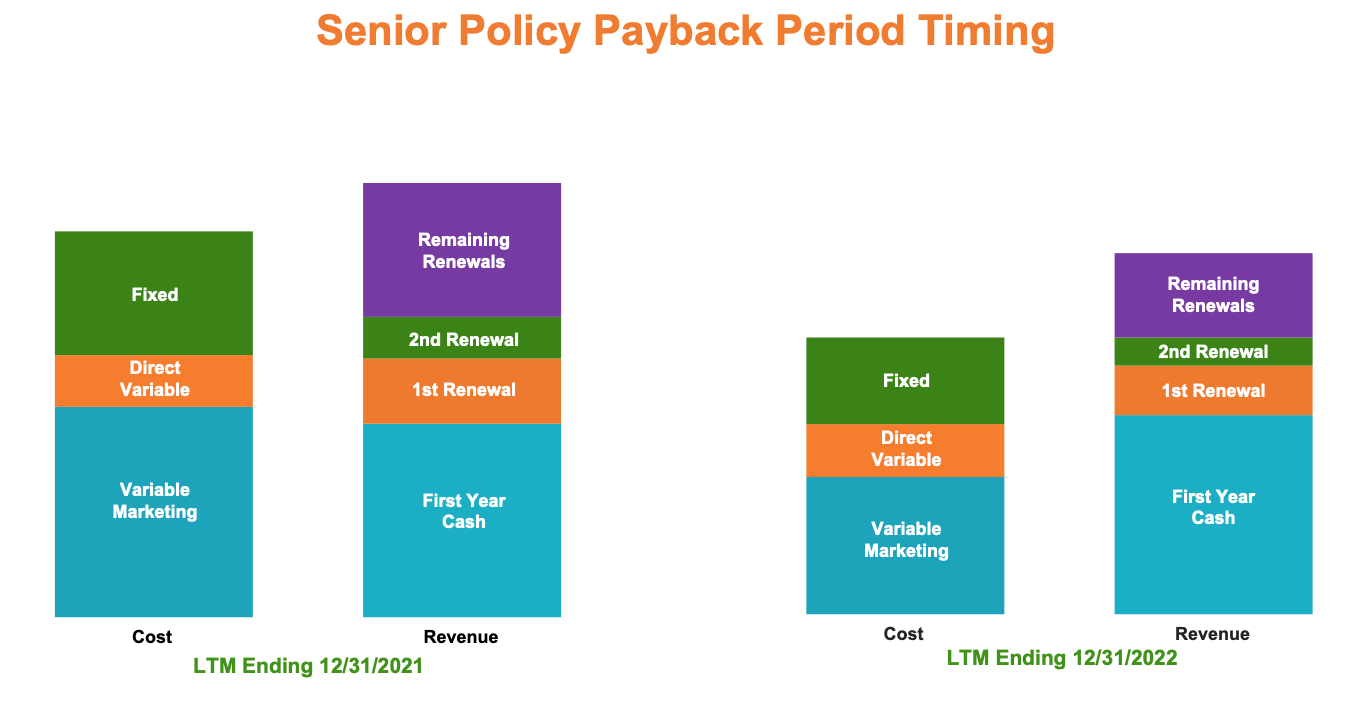

If we now flip to Slide 10, let me provide one last piece of context about the strategic redesign of our senior MA business and our improvement in cash efficiency. In these charts, we break down the components and timing of the cost to produce policies and the same for the cash timing of the resulting revenues. As you can see in the stacked bars at left, it took the first year and first renewal just to cover the variable cost to produce those policies, then it took the second renewal and a significant portion of the remaining tail of renewals to cover our fixed costs.

Slide 10:

{kind=link}

Lastly, the final piece of the puzzle you need to understand is constrained lifetime value (LTVs).

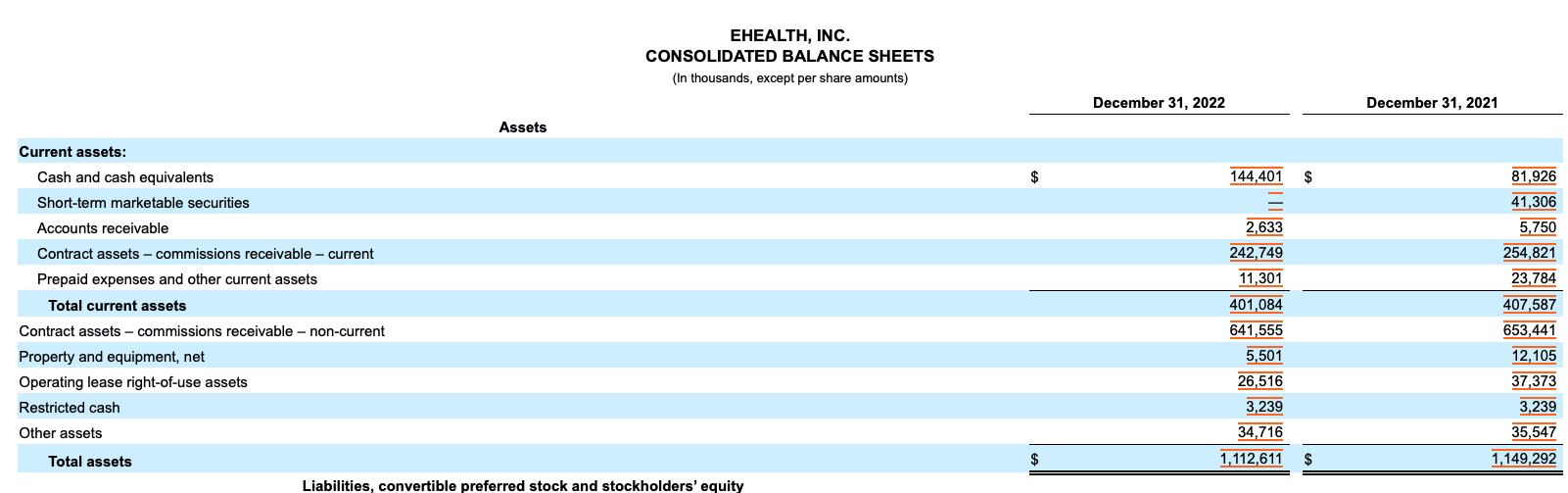

If you look at EHTH's balance sheet, you see the majority of the book value or assets are 'Contract assets - commissions receivable - noncurrent'.

This is another phrase for LTVs.

{kind=link}

When I dug through the 10-K, you can boil down the LTVs to the following two key items:

- The duration or how long a person stays with eHealth (called persistency)

- Commissions (paid by the carriers, should be fixed, for a specific cohort, but could theoretically change going forward)

Per EHTH's 10-K, the initial cost to underwrite a new policy is $888, consisting of the fixed costs of onboarding a new member as well as the estimated variable marketing costs.

{kind=link}

And per EHTH's 10-K,

The estimated average plan duration used to calculate Medicare health insurance plan LTVs historically has been approximately 3-5 years, while the estimated average plan duration used to calculate the LTV for major medical individual and family health insurance plans historically has been approximately 1.5 to 2 years. To the extent we make changes to the assumptions we use to calculate constrained LTVs, we recognize any material impact of the changes to commission revenue in the reporting period in which the change is made, including revisions of estimated lifetime commissions either below or in excess of previously estimated constrained LTV recognized as revenue.

In other words, you have to spend money upfront, to attract the new members. However, the payoff, is based on the retention of the customer, as they stay enrolled with EHTH, for many years. Again, this is largely a function of the quality of the customer experience.

So qualitatively, see these nuances from EHTH's February 28, 2023 conference call:

As a reminder, CTMs reflect beneficiary complaints filed directly with CMS. Since implementing a host of enrollment quality-related initiatives in the third quarter of 2021, eHealth has observed a 50% decrease in its CTM rates from 2021 to the most recent AEP based on preliminary data available to date. We also continue to receive positive anecdotal feedback from carriers, including from one of our largest carrier partners who share that our enrollment quality metrics are in line with their own internal sales channel.

We are steadily moving towards our goal of becoming the gold standard in enrollment quality within our sector, while also achieving and exceeding our financial targets. Last month, we released our preliminary fourth quarter and fiscal year 2022 results, which came in above annual guidance ranges that we provided earlier in the year. Today, we will share more detail about our fourth quarter financial and operating performance and the key drivers behind our effective AEP execution.

Feature enhancements during onboarding:

Co-browsing and chat capabilities:

To better bridge our online and telesales experiences. Last year, we introduced co-browsing and chat capabilities. The online chat tool, in particular, had a pronounced positive impact during the AEP on conversion rates for the online visitors to used it. It also positively impacted approval rate and initial retention for these enrollments based on data we have to date.

In addition to creating a positive user experience, chat also effectively leverages time and capacity of our benefit advisers as one person can manage multiple chats simultaneously. As a testament to the success of these initiatives, our fourth quarter telephonic conversion rates increased approximately 25% compared to Q4 of 2021. This represents a meaningful operating lever given the significant call volume we received in Q4.

One other Devil's Advocate Point

On the EHTH Q&A portion of the call, EHTH bear, and Deutsche Bank analyst, George Hill, asked this question about cash flow and raising capital.

Soistman gave a very standard and generic answer, but gave no concrete indication that EHTH needs to raise additional equity capital, at this time.

My guess is the algos picked up on the phrase ' the company will need to raise capital' and that is the only logical explanation for the February 28th stock action. Again, on February 28, 2023, EHTH shares opened up, out of the gate, +10%, and reversed from $9.78 and closed at $7.36, down 16.7%, on the day.

{kind=link}

EHTH Q4 FY 2022 Conference Call

If you are actually paying attention, Citigroup's analyst asked the same question on SLQT's conference call:

SLQT's Q4 FY 2022 Conference Call

Putting It All Together

The market in general, and notably small caps, especially sub $500 million market capitalization stocks, are often manic. They tend to dramatically over shoot and under shoot, in both directions. It is crystal clear, at least to me, that EHTH is inflecting and the industry has got religion! Given these events, I would argue that EHTH's stock could have another leg up. Given the net book value of EHTH's balance was $23.55 per share, as of December 31, 2022, I would argue $15, or more than 50% upside, from yesterday's closing price (of $9.64), is warranted. The only negative here, and this isn't new, is EHTH's preferred has a 35% change of control premium.

In closing, Soistman and team have gone a great job here and have moved the business in the right direction. Only three or four months ago, Mr. Market was pricing these equities (EHTH, SLQT, and GOCO) for bankruptcy. Those fears haven't materialized and I would argue both eHealth and the industry are inflecting. Moreover, there are strong demographic tailwinds, with so many new baby boomers turning 65 each day. This is a demographics trend that has another five to eight years behind it.

Appendix

I originally wrote up EHTH to my marketplace group.

Initially, on the morning of January 25, 2023, when shares opened at $6.25, I suggested tactically buying some shares. I then provided a follow up piece, published (originally) on March 2, 2023, with shares opening that morning at $7.90 and suggested that the stock could still double from that point.

{kind=link}

Second Wind Capital archives

For further details see:

eHealth, Inc.: A Buy And Hold Idea With 50% Upside Potential