EIDO - EIDO: Robust Outlook Intact For Indonesian Equities

2023-05-17 05:53:53 ET

Summary

- Indonesia has sustained one of the highest economic growth rates in Southeast Asia despite a weaker commodity and global trade backdrop.

- Domestic consumption has emerged as a key growth driver, alongside China reopening-led tourism rebound.

- While the iShares MSCI Indonesia ETF has outperformed YTD, valuations remain undemanding relative to the underlying growth potential.

Indonesia has traditionally been a play on the commodities cycle. But this time around, a weaker commodity price backdrop hasn't put the brakes on the economy - a result of the transition toward higher-value downstream products (e.g., the boost in processed nickel products following the government's metal downstreaming policy). In line with this view, the country's trade balance has been resilient to start the year, with export revenue growth even accelerating to +$23.5bn in March (vs. +$21bn in Feb) and the trade balance remaining in surplus despite a commodity-driven terms-of-trade headwind this year. Also helping is China's post-reopening momentum, which bodes well for exports and tourism going forward.

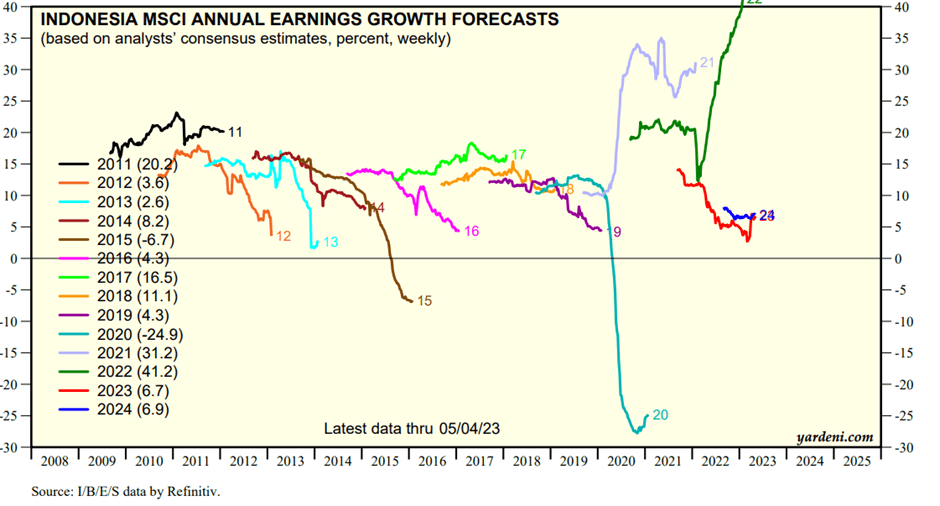

Perhaps the biggest tailwind for the near-term outlook, though, is the strong consumption story domestically (despite the monetary tightening), as well as a potential rate cut pivot and an H2 political spending boost ahead of next February's election. So even with real GDP growth already running at +5.0% YoY in Q1, there remains ample room for corporate earnings improvement later in the year. While some of the positives I cited in my prior coverage have likely been priced in following the iShares MSCI Indonesia ETF's ( EIDO ) YTD rally, the valuation remains very reasonable at ~4x earnings relative to the MSCI Indonesia's high-single-digits % earnings growth outlook .

Fund Overview - A Low-Cost, Financials-Heavy Indonesian ETF

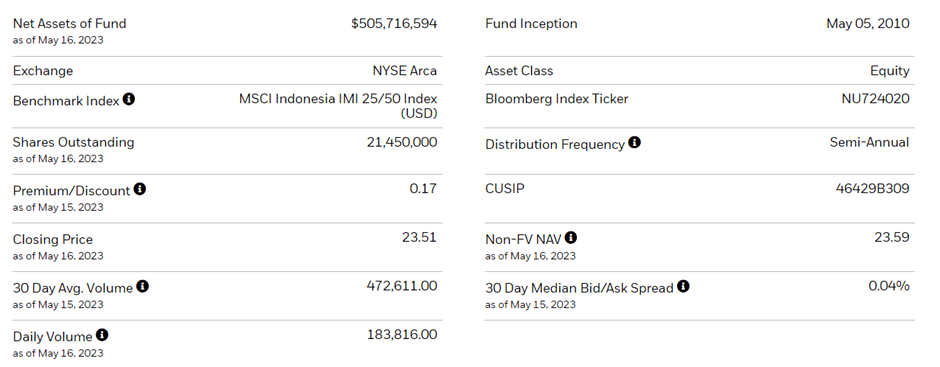

The US-listed iShares MSCI Indonesia ETF tracks, before fees and expenses, the performance of the market cap-weighted MSCI Indonesia IMI 25/50 Index, which comprises ~99% of the Indonesian free float-adjusted market cap. The ETF has seen a significant increase in its net asset base at $506m (up from ~$449m prior) and maintains a highly competitive ~0.6% expense ratio despite being one of the few single-country Indonesian options available to US investors. A summary of key facts about the ETF is listed in the graphic below:

{kind=link}

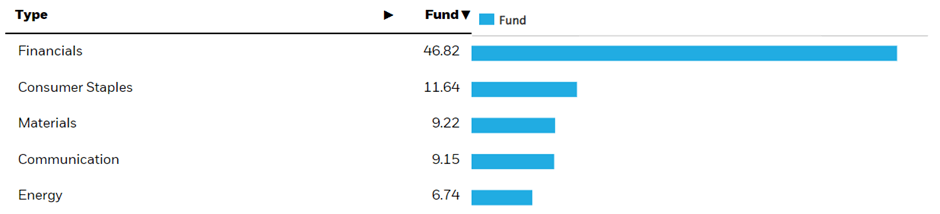

In line with comparable Southeast Asian ETFs, EIDO is heavily concentrated on the financials sector (particularly banks). Following a strong Q1 for the sector, the allocation has now risen to 46.8% (vs. ~46% prior), widening the gap relative to the iShares MSCI Malaysia ETF's ( EWM ) ~39% allocation. The rest of the portfolio composition is mostly unchanged, though the weightage for EIDO's top sectors has increased. Consumer staples remains at 11.6% (unchanged), followed by materials (lower at 9.2%), communication (lower at 9.2%), and energy (unchanged). With the top five accounting for ~84% of the total portfolio, EIDO remains a heavily concentrated fund from a sector perspective.

{kind=link}

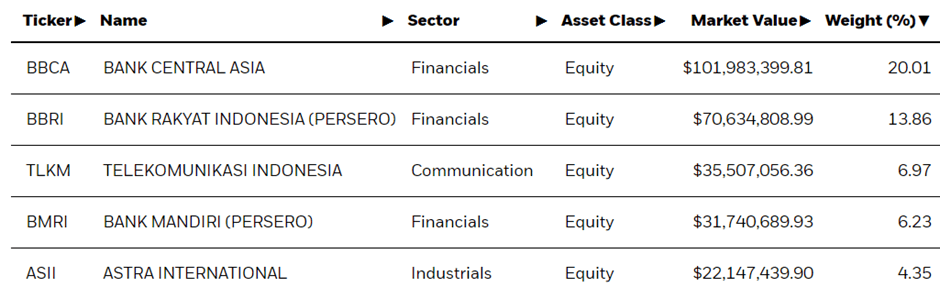

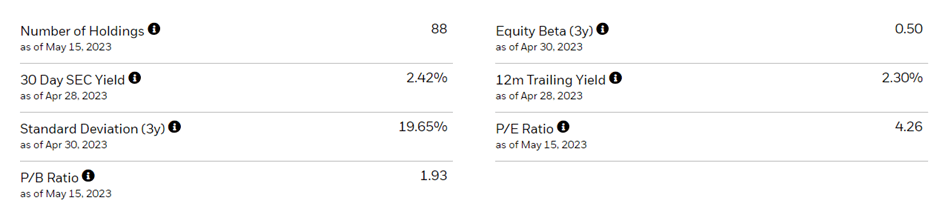

The size of the portfolio is consistent with prior reporting at 88 holdings, as well as the single-stock portfolio composition. That said, the appreciation in Indonesia's leading private banks post-Q1 has led to their increased portfolio weightage. The largest two single-stock holdings, PT Bank Central Asia Tbk ( PBCRF ) and PT Bank Rakyat Indonesia Tbk ( BKRKY ), for instance, are now up to 20.0% and 13.9%, respectively. In comparison, telco PT Telkom Indonesia ( TLK ) has slightly declined as a % of EIDO at 7.0%, while PT Bank Mandiri Tbk ( PPERF ) remains unchanged at 6.2%. Indonesian conglomerate Astra International ( PTAIF ) was a relative gainer in the top five at 4.4%, as a surprisingly resilient consumer led to its Q1 outperformance. All in all, the top five holdings account for a larger ~51% share of the overall portfolio, placing EIDO at the upper end of comparable Southeast Asian ETFs from a single-stock concentration standpoint.

{kind=link}

Fund Performance - Capital Returns Outpace Southeast Asian Peers

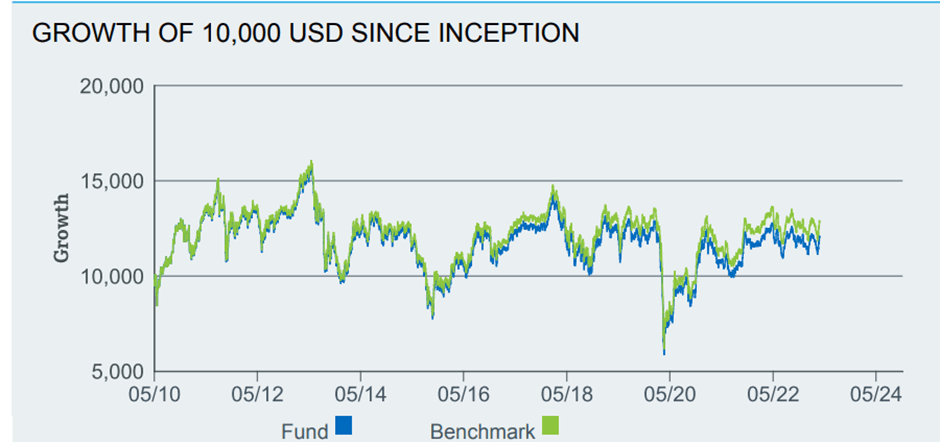

On a YTD basis, the ETF has appreciated by +4.9% (+5.9% in NAV terms), but the long-term compounding remains unremarkable at +1.5% (in market price and NAV terms) since its inception in 2010. The fund's performance has, however, outpaced comparable Southeast Asian ETFs like the iShares MSCI Philippines ETF ( EPHE ) and the iShares MSCI Malaysia ETF across short and long-term time frames. On three and five-year timelines, for instance, EIDO has returned +18.6% and -0.8%, respectively (vs. +6.6% and -3.9% for EPHE and +2.7% and -5.8% for EWM). Zooming out over the last decade, their returns converge closely, though EIDO still comes out ahead at -2.3% (vs. -3.2% for EPHE and -3.0% for EWM). Performance has also tracked the benchmark MSCI Indonesia IMI 25/50 Index well after accounting for fees, so the fund's tracking error is low.

{kind=link}

The fund also offers a solid distribution (semi-annual payout), with the trailing twelve-month yield at 2.3% (2.4% on a 30-day basis). While EIDO's yield pales in comparison to EWM (a similarly financials/bank-heavy portfolio), it runs ~1%pt higher than EPHE despite also offering a superior capital growth record. Where the EIDO portfolio shines, however, is on its defensiveness (equity beta of 0.5 vs. the S&P 500 (SPY)) and its valuation at ~4x P/E. Given the relatively higher earnings growth sustained by Indonesian large-caps (+7% in 2023/2024 per consensus estimates) and the slew of positive earnings revisions seen in recent months, EIDO arguably has the greatest re-rating potential in Southeast Asia.

{kind=link}

Domestic Resilience Sets Foundation for the Next Leg of Growth

Indonesia's Q1 growth showed surprising resilience in the face of a global slowdown, as increased domestic demand strength drove headline GDP growth to +5.0% in Q1 (+3.4%pts domestic demand contribution vs. +3.0%pts in Q4). Meanwhile, net exports were also a positive contributor, adding +2.1%pts to Q1 growth (decelerating from +2.2%pts in the previous quarter), as a foreign tourist rebound offset most of the weakness on the goods side. In line with the GDP print, Indonesian consumer companies also saw their pricing power remain intact in Q1 - a positive surprise given the fuel price hike implemented last year. And as political campaigning ramps up in H2, the best-in-class consumer franchises in the EIDO portfolio remain well-positioned to capitalize.

{kind=link}

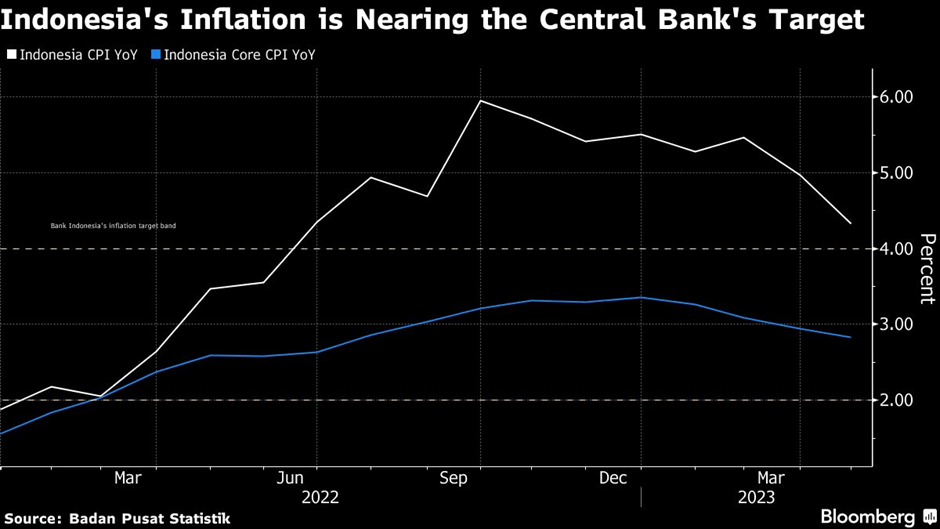

A key contributor to the recent household strength is the fading inflationary impulse - headline consumer inflation further decelerated to +4.3% YoY in April (vs. the central bank's 2-4% target range), helped by lower food prices and a favorable base effect for key items like cooking oil. With the sharp disinflation coinciding with IDR stability and a likely end to the Fed rate hike cycle over the next month, Indonesia could soon see a rate cut pivot as well. While potentially a headwind for bank margins, the major Indonesian banks within the EIDO portfolio have more than enough offsetting growth levers. As Q1 showed, the big banks are actively gaining deposit share via more expansive transactional franchises while also penetrating the more profitable micro/ultra-micro loans segment. Also helpful are their improved asset qualities post-restructuring (e.g., Bank Rakyat's corporate loan restructuring in Q4), providing them with access to cheaper credit and structurally higher ROEs from here.

{kind=link}

Robust Outlook Intact for Indonesian Equities

Indonesia's move to diversify its commodity dependence means the 'long Indonesia' thesis remains valid. Case in point - even with a broadly weaker backdrop for global commodities, the economic data out of Indonesia has been strong, showing its sensitivity to the commodities cycle has been significantly reduced. There's also a strong domestic consumption story developing here, with private consumption emerging as the key GDP growth driver in Q1 and election-related spending set to provide further support as the election season kicks off in H2. Plus, China's post-reopening outbound tourism recovery has yet to move into full swing, presenting incremental upside to earnings growth for the EIDO portfolio. Yet, at ~4x earnings relative to a high-single-digits % earnings growth outlook for Indonesian large-caps, EIDO seems very cheaply priced. Alongside a sustained current account surplus and sizeable FX reserves, as well as the prospect of a rate cut pivot later this year, EIDO investors should also be protected on the FX side.

{kind=link}

For further details see:

EIDO: Robust Outlook Intact For Indonesian Equities