ESALF - Eisai: Growth In Japan Markets Leqembi The Main Long-Term Growth Driver

Summary

- Growth in Japan markets the standout for the period, with growth across all core segments.

- Leqembi gaining substantial traction in regulatory approvals in key global markets.

- Hence therein lies a strong investment opportunity with ESALF for those seeking exposure to breakthrough Alzheimer's treatments.

- Net-net, rate buy at $79 target.

Investment Summary

As the year progresses we've garnered coverage over several Japanese-based pharmaceuticals names, each with varying outlooks for the coming periods. You can check out the recent publications on Takeda Pharma ( TAK ) and Astellas Pharma ( ALPMY ) here:

- Takeda: Momentum Building Around Core Offerings, Rate Buy

- Astellas: Balanced Investment Debate After Q3 Numbers

Extending the coverage, I'm back to scrutinize Eisai Co., Ltd.'s ( ESALF ) Q3 FY22' results after the company posted relatively flat top-line growth period across its global markets. ESALF has been building momentum around its core Alzheimer's Disease ("AD") segment, alongside its pharmaceutical assets over the past 12 months. Chief to the investment debate, however, is the company's Leqembi label, that has garnered substantial regulatory momentum for the treatment of AD. In particular, its collaboration with Biogen ( BIIB ), through the phase 3 CLARITY trial, that investigated Leqembi in Alzheimer's, met its primary and secondary outcomes back in September. This has led to an expedited approval process in the U.S. and EU. The pair have since advised a 50% profit sharing deal where ESALF will continue developing Lecanemab and BIIB will assume manufacturing responsibilities. For more on the study, I'd encourage investors to Seeking Alpha contributor Keith Williams coverage, who conducts a deep dive of the trial, the results, and what to expect looking forward [see: here ].

Turning back to the quarter, there's a large amount of data to unpack from the numbers, and the company's expectations looking forward. [Just as a side note, the company reports in JPY, however, for the convenience of readers, I'll be talking in US dollar terms, where 1 USD = JPY 143.65 at the time of writing] . Looking at the numbers, the standout across ESALF's performance from Q1–Q3 has been growth in its Japanese markets, and this is a factor that must be considered in the investment debate as well. Moreover, with a number of key inflection points on the horizon, building momentum around its Leqembi segment, we rate ESALF a buy at a $79 initial target.

Q3 results analytics

1. Operating results were flat, coupled with free cash outflows

ESALF reported a ~500bps YoY decline in turnover to ~$4Bn. The downside was largely attributed to an upfront payment of $368.8mm from Bristol Myers Squibb ( BMY ), booked in the previous fiscal year, under strategic collaboration for its antibody drug conjugate MORAb-202. It also lost some leverage at the SG&A line, chiefly due to the headwinds with the JPY/USD cross rate, in addition to the shared profit paid to Merck ( MRK ) following Lenvima's revenue growth. However, these collaborations enabled ESALF to pare back its R&D margin, thanks to synergies obtained through its partnership model. Moving down the P&L, we'd note that operating profit pulled in tighter by ~$138.2mm YoY, and it pulled this down to earnings of $303.8mm, down ~45% YoY, despite recognizing a $173mm tax credit thanks to its transfer of paid in capital from a U.S. subsidiary. Turning to cash flows, ESALF's net CFFO realized an outflow of $191.8mm, related principally to the payment of accounts payable to its various partners. It also increased its investing activities, with another outflow of $150.1mm, attributed to CapEx, purchases of additional financial assets, and investments in property, plant and equipment. On this, it increased its debt position by $401mm, and returned $340mm in capital to shareholders via its dividend. Net-net, it burnt through $309mm over its first 3-quarters. Subsequently, by the end of the period, cash and cash equivalents stood at $1.99Bn. Moreover, it realized a free cash flow outflow of $341.4mm.

Fig. (1)

Note: Results are listed in JPY. (Data: ESALF Investor Presentation, see: "Revenue by Reporting Segment" pp. 19)

{kind=link}

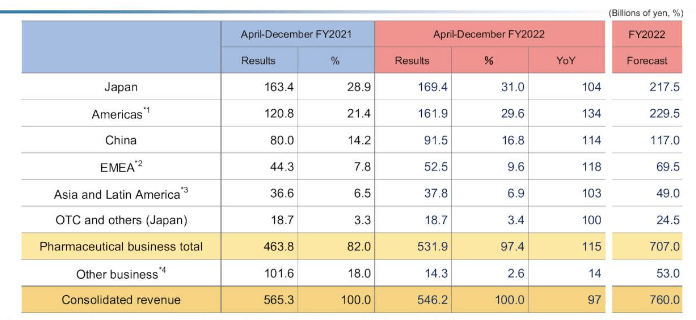

2. Japanese pharma business outperforming

Analysis of the pharmaceutical business in Japan reveals total revenue reached $1.26Bn, up by 103.7% YoY. Subsequently, the divisional earnings grew by 120% YoY, reaching $420mm. Among the products, Dayvigo [indicated in neurology] achieved a notable 210% YoY growth route, and clipped revenue of $134mm. Fycompa, another neurology product, also demonstrated growth with revenue of $35mm, up by 115.9% YoY. Turnover from its oncology products also exhibited a robust growth profile, with its Lenvima and Halaven labels each up >100%, generating revenue of $79mm and $48mm respectively. Meanwhile, its Humira label, contributed $279mm to the top line, up 96.7% YoY. Additionally upsides were observed in its Goofice, and Jyseleca segments, indicated for treatment of constipation and chronic inflammation, respectively.

Looking forward to its full-year results for FY22' [corresponding to March 2023'] the total revenue in its Japanese markets are expected to reach $1.2Bn, up by 134.0% YoY, with on a net profit of $735mm, up by 146.7% YoY. Overall, the company's performance in the Japanese pharmaceutical market indicates a positive growth trajectory, making it an attractive investment opportunity for investors seeking exposure to the industry.

Fig. (2)

Note: Results are listed in JPY. (Data: ESALF Investor Presentation, pp. 22)

{kind=link}

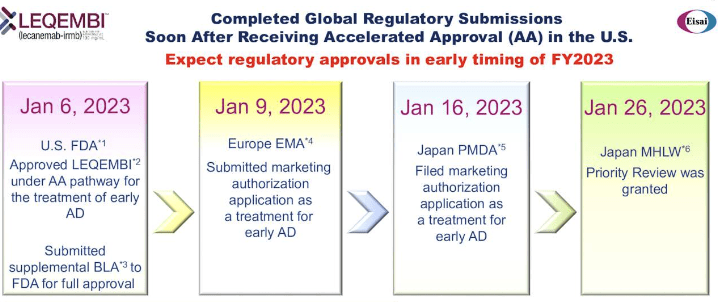

3. The U.S. launch of Leqembi in January 2023 is expected to add additional revenue growth drivers for the company.

Regarding Leqembi, the company's AD label, it's worth reminding readers that the results of the Clarity AD phase 3 study with BIIB [listed earlier] met its primary and key secondary endpoints with statistical significance. Importantly, this included an amyloid-related imaging abnormality ("ARIA") expression profile the fell within range expectations. This development paved the way for the initiation of an biologics license application ("BLA") submission to the National Medical Products Administration ("NMPA") in China back in December. Furthermore, based on the data from the Phase 2 study, that demonstrated Leqembi's ability to reduce the accumulation of amyloid beta ("AB") plaques in the brain – a defining feature of AD – the FDA granted the compound breakthrough therapy designation, and fast track designation for AD treatment in the U.S., subsequently a supplemental BLA was submitted for traditional approval.

Fig. (3)

Data: ESALF Investor Presentation, pp.9

{kind=link}

The company also submitted a marketing authorization application to the European Medicines Agency ("EMA"). It was in January 2023. Subsequently, ESALF, has pushed ahead with regulatory approval in Japan. This in itself can be a challenge, as governmental approval is usually required in the process. Alas, it submitted a marketing authorization application was submitted to the Pharmaceuticals and Medical Devices Agency ("PMDA"). Next step is the review by the Japanese Ministry of Health, Labour, and Welfare. Moreover, its AHEAD 3-45 phase 3 study is currently underway in the U.S., Japan, and Europe. It is evaluating Leqembi's potential for preclinical AD [otherwise known as asymptomatic AD]. As a potential catalyst, it has been selected by the Alzheimer's Clinical Trials Consortium ("ACTC") for evaluation.

Risks to thesis

There are several notable risks associated with the buy thesis that investors should be acutely aware of. Namely, the ongoing regulatory status of Leqembi springs to mind, seeing as it still has a ways to go before reaching critical mass via a full approval, beyond the BLA and the breakthrough therapy designation. Should any kinks arise along the way, this could present a material risk in the medium-term. Further to this, there's risk it may not achieve regulatory status in Japan, and this must be factored into the investment debate as well. In that vein, it would be unwise to ignore the broader macroeconomic picture, seeing the February pullback in broad equities, and the central bank tightening regimes in major global markets. A further hiking cycle from any of the company's major geographical regions could present as a risk to growth for the company. It is essential that investors recognize these risks in their investment reasoning, as mentioned.

Valuation and conclusion

The stock is trading at a substantial premium at 54x trailing P/E, more than double the industry at ~25x. It is also priced at 2.8x book value, and when looking at growth of its book value per share, it has decreased by 760bps YoY to $20.56. The potential on Leqembi is central to the debate however. With only two other major providers [Roche, and Eli Lilly, see: here , pp. 28] as major competitors to the label, and both facing challenges from the FDA, this is an upside factor to ESALF's case. Utilizing management's full-year EPS forecasts of $1.47, at the 54x multiple, derives a price target of $79.

It's important to note that ESALF's developments are significant advancement within the AD populous, as Leqembi's approval for the treatment of Alzheimer's disease marks a crucial milestone, along with other advancing labels within the space. All of these respective developments have the potential to address a wide unmet medical need for patients suffering from the condition. Further, the global market for AD treatment is expected to grow at CAGR 16.2% into FY30', reaching $13Bn by that time. Therefore, we suggest Leqembi is a promising investment opportunity for those investors looking to gain exposure to treatments providing a medical breakthrough in complex disease segments, further supporting the buy thesis. Hence, looking at the culmination of data, we rate ESALF stock a buy.

For further details see:

Eisai: Growth In Japan Markets, Leqembi The Main Long-Term Growth Driver