BIIB - Eisai: Looking To Upside Targets Following Leqembi Full Approval

2023-07-09 10:00:00 ET

Summary

- The FDA has approved Eisai Co.'s Leqembi label last week, developed with Biogen, for the potential treatment of adult patients with Alzheimer's Disease.

- The company will lead global development and handle all regulatory submissions for Leqembi, with both parties involved in commercialization and promotion.

- Approval of Leqembi provides a potential medical breakthrough in Alzheimer's Disease treatment, with Medicare's full support expected to boost sales.

- Net-net, reiterate buy on the latest Leqembi updates.

Investment briefing

Following my February publication on Eisai Co., Ltd. ( OTCPK:ESALF ) there have been multiple updates to the investment facts, that must be discussed in full.

Chief among these— t he FDA has fully approved the company's Leqembi label, developed in collaboration with Biogen ( BIIB ), and indicated in the potential treatment of adult patients with Alzheimer's Disease ("AD").

I had extensively covered the impending launch of Leqembi in the last publication, stating, "[t]he U.S. launch of Leqembi in January 2023 is expected to add additional revenue growth drivers for the company". Here I'll focus on the Leqembi updates from the perspective of ESALF investors. But it's essential to know that BIIB is in equal standing to benefit immensely from its full approval and Medicare coverage, as discussed today.

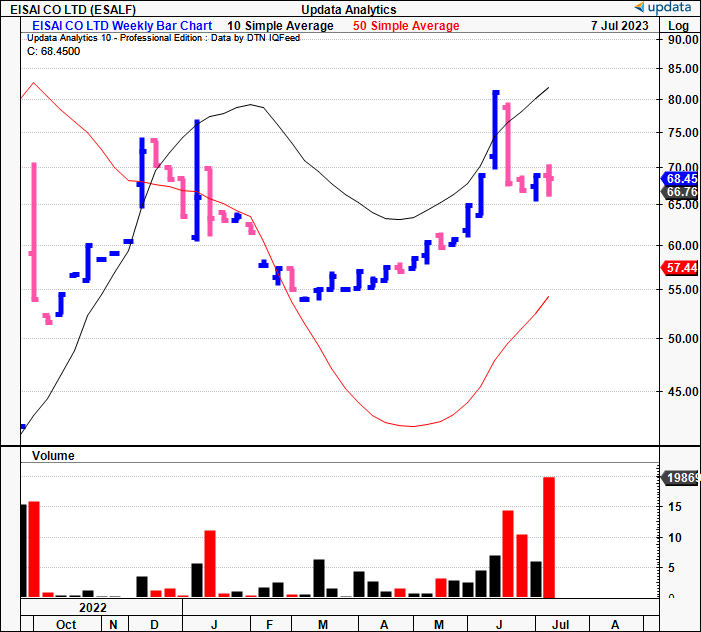

Figure 1. ESAI price evolution, Oct '22–date [weekly bars, log scale]

{kind=link}

Based on the tenets forming my ESALF investment thesis, this is an incredibly important update to the facts. There is loads to unpack here, ranging from the FDA's approval, Leqembi's efficacy, and the deal's economics itself. This report will cover all of the moving parts of the Leqembi updates and links this back to the investment debate for ESALF, ultimately re-affirming the company as a buy in doing so. Net-net, reiterate buy at $79 price target.

Updates to critical investment facts

Leqembi's approval is one meaningful catalyst to move the needle on ESALF's equity stock in my view. If we take a step back, looking at FY'23 YTD, whilst the benchmark indices had rallied some 20-30% by April, ESALF had languished near 52-week lows. However, since the February publication, it has rallied some 26% to the upside, with multiple updates regarding Leqembi along the way. The progression of the approval since February is observed below.

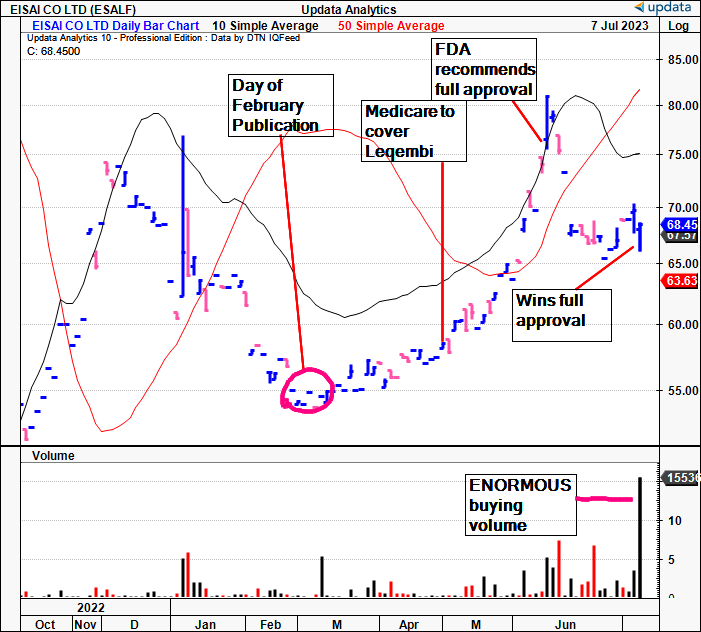

Figure 2. Leqembi FDA pathway from February [daily bars, log scale]

{kind=link}

1. Process to Leqembi full approval

To remind you, Leqembi is an amyloid beta-directed antibody, that actively targets and nullifies the presence of amyloid plaques in the brain. These plaques are the hallmark pathophysiological feature of AD. Therefore, whilst it is not a preventative therapy, the label addresses a critical aspect of the disease's progression.

Clinical updates driving FDA's decision

- As mentioned in the February publication, Leqembi was initially approved under the Accelerated Approval Pathway in January. This came after efficacy data held up well in previous clinical trials— specifically, the reduction of amyloid plaques in the brain, as mentioned earlier. As part of the postmarketing requirements of accelerated approval, the FDA mandated the CLARITY AD trial from ESALF to substantiate the clinical benefits of Leqembi. The Phase 3 RCT enrolled 1,795 patients with AD, with a weighted focus on patients in the mild cognitive impairment or dementia stages of the disease.

- Critically— all of the patients had a confirmed presence of amyloid beta pathology, which may be essential information in the treatment domain once the drug is widely commercial, in my view.

- Participants were randomly assigned in a 1:1 ratio to receive either placebo, or Leqembi, at a dose of 10mg per kilogram, administered once every 2 weeks.

- As to the results, it was shown that Leqembi demonstrated statistically significant reduction in cognitive decline from baseline to 18 months compared to placebo. As a side note, there were differences observed within the secondary endpoints of the study between the groups receiving Leqembi, measured by the:

- Alzheimer's Disease Assessment Scale Cognitive Subscale 14, and

- The Alzheimer's Disease Cooperative Study-Activities of Daily Living Scale for Mild Cognitive Impairment.

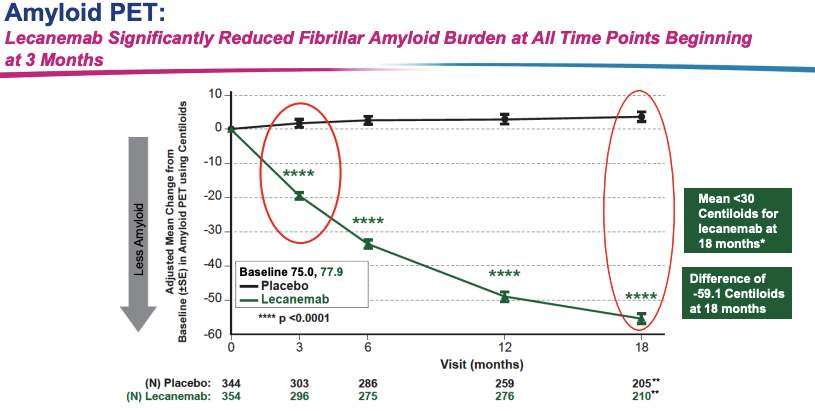

Figure 3. Leqembi impact on Amyloid PET [primary outcome in CLARITY AD trial].

Data: ESALF CLARITY AD Clinical Presentation, retrieved from company website under "Presentations".

{kind=link}

FDA full approval and Medicare coverage

In June , the FDA's Peripheral and Central Nervous System Drugs Advisory Committee ("CNSDAC") unanimously recommended full approval for the supplementary Biologics License Application ("sBLA") for Leqembi. This followed CMS' announcement that all approved AD treatments would receive Medicare reimbursement of up to 80–100% of the treatment's cost.

To me, this is the major growth lever in the Leqembi story. Sales of the drug haven’t been revealed in full per the company. However, Medicare's full support will no doubt be a remedy to pricing and access headwinds in my view. It should be noted that two of ESALF's main competitors in this space —Eli Lilly ( LLY ) and Quanterix ( QTRX )— also benefit from these positive changes. Mainly, however, it is the patients who benefit the most. In terms of creating a patient–focused route to market, this aligns with said principles well.

Moreover, the CMS' vote of approval is clear evidence of the body's view of Leqembi's potential as an AD treatment in my opinion. You see this echoed in the language used by the FDA at the time:

Today’s action is the first verification that a drug targeting the underlying disease process of Alzheimer’s disease has shown clinical benefit in this devastating disease...[t]his confirmatory study verified that it is a safe and effective treatment for patients with Alzheimer’s disease.”

— Teresa Buracchio, Office of Neuroscience, FDA Center for Drug Evaluation and Research.

The subsequent changes to ESALF's guidance following the CMS' approval have yet to be conveyed by management. Comparative examples must therefore be used in order to understand the magnitude of such backing by the CMS [ although, I am waiting on further guidance from management on the same for concrete projections going forward, plus, we need some evidence of how Leqembi's moved since its launch in January ]. Using such a comparative example, Vertex Pharma's ( VRTX ) Trikafta label —indicated for the treatment of cystic fibrosis, another complex disease segment with little-to-no treatment alternatives— immediately springs to mind. Trikafta is now covered under most Medicare (and equivalent) systems throughout most European nations, the U.S., and APAC. It was approved by the FDA in 2019, and by 2020, it had obtained full Medicare coverage [under Parts A–D, with Part D coverage being the most significant for patients].

To date, VRTX has booked ~$17Bn in lifetime Trikafta sales, booking $7.7Bn in FY'22 alone. However, this is only made possible by the fact it is covered under the mentioned Medicare programs— let's not forget, Trikafta costs >$311,000 as a treatment, meaning it's unattainable for most on a standard living wage.

You won't find physicians and specialists prescribing any treatment beyond their patients' realms– it just isn't done. Hence, Medicare's (and equivalent in different jurisdictions) reimbursement of the Leqembi treatment, marketed as Kaftrio in Europe, is quintessential to its rapid uptake in the actual treatment domain. The medication costs ~$26,500 annually, meaning patients would be forking out a maximum of $5,300 per year [at 80% reimbursement, or $441 per month] if not 100% covered. That enormous difference opens the funding window for the entire AD population, and could spike Leqembi sales into perpetuity in my view.

2. Leqembi treatment effects, side effects

The discussion wouldn't be complete without a deep dive into the spectrum of benefits and side effects of the compound. These are well documented, and, noteworthy, is that Leqembi does come with its share of adverse effects.

Side effects

- Headaches, infusion-related reactions, and amyloid-related imaging abnormalities ("ARIA") emerged as the most common side effects associated with Leqembi per the CLARITY trial.

- ARIA —a known class effect of amyloid-targeting antibodies— manifests as transient swelling in specific brain regions, and is only observed from imaging studies. In most cases, this swelling resolves over time— but it may be, and often is, accompanied by small cerebral haemorrhages, otherwise known as brain bleeds.

- While ARIA is frequently asymptomatic, individuals may experience symptoms such as headache, confusion, dizziness, changes in vision, and nausea, in line with the side effects described earlier. In rare instances, ARIA can present as severe and life-threatening.

- Notably, patients receiving Leqembi who are homozygous for the ApoE E4 allele —a critical genetic risk factor in AD— exhibited a higher incidence of ARIA, including symptomatic, serious, and severe cases. That is something to consider when prescribing the treatment, and who may or may not be eligible.

- Accordingly, you'll find on Leqembi's labelling that clinicians are advised to assess the ApoE E4 status of patients before initiating Leqembi treatment.

- Furthermore, precautions are described for patients taking anticoagulants or those with other risk factors for a stroke, given the same reasons.

Contraindications

- Contraindications dictate that Leqembi should not be administered to patients with severe hypersensitivity to lecanemab-irmb [the underlying compound in Leqembi] or any of its inactive ingredients. Naturally, full bloods' are required to test for these kinds of markers in vitro. How else would one know?

- Potential adverse reactions include:

- Severe swelling, and

- Potentially entering anaphylaxis.

- Whilst not necessarily a contraindication, the FDA recommends that Leqembi also "should be initiated in patients with mild cognitive impairment or mild dementia stage of [AD], the population in which treatment was studied in clinical trials. The labelling states that there are no safety or effectiveness data on initiating treatment at earlier or later stages of the disease than were studied."

The list of side effects and precautions is important in the investment debate. In particular, we need an understanding of the AD populous who are not eligible to receive the treatment in order to accurately estimate the size of the total addressable market (“TAM”). On examination, there doesn’t appear to be any indication from ESALF on what it expects in terms of the ineligible segment of AD patients. However, findings by Santiago & Potashkin (2021) found that “…chronic diseases, including diabetes, cardiovascular disease, depression, and inflammatory bowel disease, may be associated with an increased risk of AD in different populations.” Hence, there is a chance the TAM may be restricted on these findings in my view. I’ll be watching the data on this with exquisite focus moving forward, and would encourage you to do the same.

3. Particulars of BIIB collaboration

Based on 1) the market's price response to the updates, and 2) the fundamental changes Leqembi’s approval makes to the AD market, it is of my firm investment opinion that ESALF is a resounding buy.

Market economics

For one, the full approval of Leqembi provides a potential medical breakthrough in an otherwise impossible-to-treat disease segment of AD, where symptoms revolve around either slow or rapid cognitive, and therefore, physical, decline. Patients eventually succumb to the condition.

An estimated 6–7mm adults are in the U.S. diagnosed with AD, with the bolus of patients aged 75 years or older, whereas c.11% are 65 and older. Worldwide, there are an estimated 55mm sufferers, expected to grow to 78mm by 2030. A sub-populous of "early–onset" AD also exists, i.e., those diagnosed before age 50. The AD treatment market is poised for an 8.1% geometric growth into FY'31. Although, with the entrance of new therapies such as Leqembi onto the scene, there is good chance these projections may be revised to the upside in my opinion.

For example, recent research from GlobalData estimates a 20% CAGR into 2030 and reach c.$14Bn by that time. It cites an extensive, 23–long list of pipeline assets due to potentially reach the AD treatment market over the coming years. This is bullish news and supports the buy thesis for ESALF.

BIIB collaboration[s]

As mentioned, the company has collaborated with BIIB to develop and commercialise Leqembi. Now with the full approval on board, the economics of the deal are essential to understand.

Under the co-development and co-promotion agreements for Leqembi, ESALF will spearhead the compound's global development, and handle all the regulatory submissions. Both entities are set to actively engage in the commercialization and promotion in their respective end markets— critically, with ESALF having the final executive orders in the decision-making authority. Expect large marketing efforts from both parties in my view, especially seeing as both ESALF and BIIB have extensively deep, well-formed customer networks, and piles of cash to invest in the same.

As a result, ESALF has chosen to adopt the following accounting procedures to book Leqembi sales going forward:

- Revenue Recognition: Both BIIB and ESALF will record revenue and cost of sales for Leqembi in its approved regions. OpEx associated with Leqembi —and the shared profit paid to BIIB— are to be booked at the SG&A line on ESALF's statements. It will be absolutely essential, therefore, to deconstruct this line for ESALF moving forward. In the event of a "negative shared profit", whereby ESALF instead receives a profit share from BIIB, this will be recognized as a credit to the SG&A line.

- R&D investment: Leqembi will require ongoing refinement and innovation around the core label. All R&D investment capital diverted toward Leqembi is to be shared equally between ESALF and Biogen. Furthermore, expenses related to commercialization in regions without approval will be evenly divided between the pair.

- Milestone payments: ESALF is also to incur milestone payments tied to licensing rights of Leqembi. BIIB shares each of these milestones equally. ESALF will book its milestone portion as an intangible asset. However, I would also point out to you that ESALF will amortize these "intangibles" as a cost of revenue— so adjustments will need to be made to the company's cost structure on reporting to ascertain actual cash values of expenditures and costs.

It's also worth noting that ESALF and BIIB have co-developed BIIB's ADUHELM label, also indicated in the treatment of AD. In January this year, the collaboration agreement underwent fundamental changes. ESALF is to receive a tiered royalty starting at 2% of sales, ratcheting to 8% of turnover once sales surpass $1Bn. You need to know the relevant economics of this collaboration moving forward as well:

- The P&L for ADUHELM is distributed between the two companies. The proportions are determined by the specific regions. For instance, ESALF's potential allocation is as follows: a 45% share for the U.S., 31.5% for Europe, 80% for Japan and Asia (excluding China and South Korea), and, a 50% share for the "rest of the world".

- Furthermore, c.45% share of R&D investment for ADUHELM will be taken on by ESALF.

You might wonder why ESALF would commit to selling BIIB's own AD treatment, as it might cannibalise Leqembi's penetration of the market. However, based on the above economic characteristics of the ADUHELM agreement, in my opinion, it is in ESALF's best interests to move as much of BIIB's label as possible. It assumes no execution risk, instead lets BIIB take on all of that with their own capital. In the end as well, it is the patient who benefits from the broader access to more AD drugs.

In short

To sum it all up, the emergence of drugs like Leqembi represent a medical breakthrough in AD treatment, providing hope to millions of those diagnosed with the condition worldwide. My investment theses focus squarely on these kind of selective opportunities, much like those in the tech or IT spaces focus on groundbreaking software for example. There is a chance to make a meaningful difference to many lives.

In my view, Leqembi's conversion from accelerated approval in January —just 7 months ago— to formal approval is a clear indication of the drug's potential benefits. Safety and efficacy data have held up well to date, and Medicare's support of the label is further evidence of the same. With the backing of the FDA, plus the CMS reimbursement, there is good reason to believe Leqembi sales might benefit in my view. As to the particular numbers— I am waiting on the company's next earnings for more accurate guidance, as we need to see how Leqembi's moved in the market since the January launch. However, it did call for ¥712Bn in total revenue for the FY'23 year in May, a 4.4% YoY decrease, with estimates for ¥39Bn in post-tax earnings, a 31% YoY decline. As to Leqembi’s contribution to these figures, isn’t entirely clear from management.

Hence, I am keeping an extremely close eye on the upcoming numbers from ESALF for better guidance on management's view. It is difficult to project a launch curve post-Medicare announcement without the raw data in front of us. Nevertheless, based on the combination of:

1. Full FDA approval;

2. Economics of the AD treatment market;

3. Reimbursement of Leqembi;

I am bullish on ESALF and retain a buy rating on the company. I had prescribed a $79 price target on the company back in February and I am retaining this figure for now. Confidence in that assumption is bolstered by the culmination of data presented here. This represents another 15% upside from the current market price. The key data to watch out for next? The company's next earnings report in the coming months (there is no set date I can find from the company). Reiterate buy.

For further details see:

Eisai: Looking To Upside Targets Following Leqembi Full Approval