ESALF - Eisai: Lumpy Rollout Of Leqembi Economic Value Hard To Ascertain (Rating Downgrade)

2023-09-22 16:01:40 ET

Summary

- Eisai Co., Ltd. has experienced a sharp decline amid lumpy progress with its Alzheimer's disease drug, Leqembi.

- Q1 FY'23 numbers show modest growth in ESALF's pharmaceutical business, but revenue and operating income have decreased over time.

- ESALF's ability to create economic value is questionable, with a high cash conversion cycle, low return on investment, and tight margins.

- Net-net, revise to hold.

Investment updates

Since the July publication, Eisai Co., Ltd. ( ESALF ) ( ESAIY ) hasn't caught a bid, having sold off sharply to the downside instead. Whilst unpleasant, 1) I accept this is the nature of markets, and 2) the analysis presented here today corroborates the market's viewpoint.

ESALF's latest numbers weren't convincing, despite its progress with Leqembi - the medical breakthrough in Alzheimer's Disease. The last publication dealt with Leqembi in extensive detail, so for a dive into the pharmacology and market opportunity of the label, I'd encourage you to check it out by clicking here. At this point, the economic value created from ESALF's growth model is lacking. Plenty of investment has been put to work into expanding the business, and it now has multiple commercial labels out in the field collecting cash flows. This report will unpack all of these factors for the benefit of investors. Net-net, I am paring my rating on ESALF to hold for the reasons presented here today.

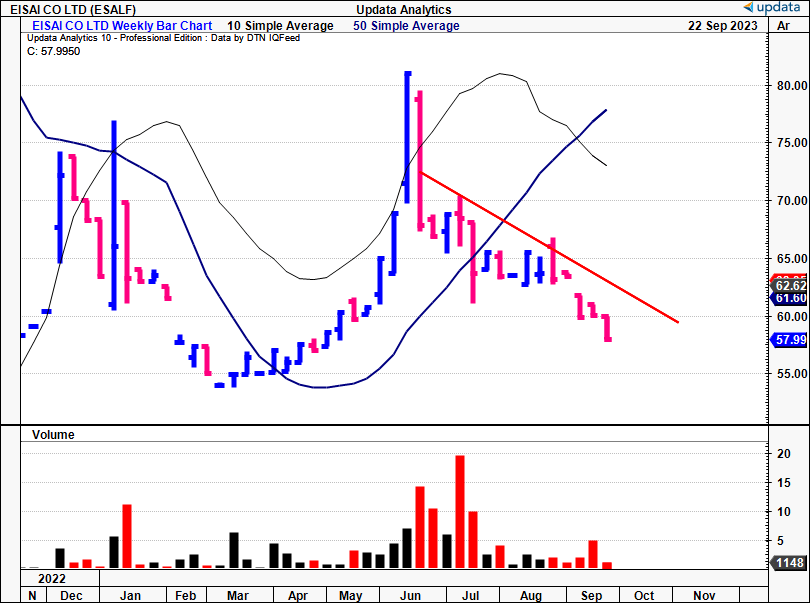

Figure 1. ESALF price action throughout '23. Tremendous rally in first half, second half price action hasn't followed suit.

{kind=link}

Critical updates to investment thesis - latest numbers, economic value

1. Q1 FY'23 insights

Two essential points: ESALF reported its Q1 numbers for its fiscal '23, corresponding to Q2 CY 2022. I'll talk in terms of Q1 from here for consistency. Second, ESALF reports in JPY. All figures presented in this report are presented in USD, at the exchange rate of 1 USD = 148.34 JPY, unless otherwise stipulated.

While ESALF's pharmaceutical business exhibited reasonable growth in Q1 , this wasn't so much organic, as it was from the upfront payment it booked to transfer future economic rights related to Elacestrant (see: Figure 4). Top-line sales were $1.36Bn for the quarter, up ~7% YoY, on an operating income of $180.4mm.

In terms of revenue from its global labels, the growth percentages were nothing to write home about in my view. Specifically, the key contributors were:

- Lenvima put up Q1 sales of $477mm, up 6.7% YoY. You can see the breakdown of Lenvima sales in Figure 2(a).

- Halaven (indicated as an anticancer agent) pulled in $64.1mm, down 14% YoY.

- Dayvigo did $63.4mm in sales, a 44.6% growth rate.

- Fycompa (its anti-epileptic agent) sales were $54.7mm, a decrease of 18% YoY. Commercial rights for Fycompa in the U.S. were transferred in January this year.

As to the geographical breakdown, the company clipped equally mixed results across its regional segments. While revenues in Japan grew by a modest 160bps YoY to $434.8mm, earnings decreased by 1.1% to ~$154mm. On the other hand, its Americas footprint (U.S. and LatAm) proved to be a bright spot, growing 2.4% YoY to do $366.1mm of business, on earnings growth of 14.4% to ~$241.5mm.

However, like many global players this year, the company faced challenges growing its business in China. Revenues declined by 9.1% to c.$213.2mm on a 10.2% decline in earnings to ~$125.5mm. Meanwhile, in EMEA, revenues were up 3.4% to $126mm, on earnings of $68mm.

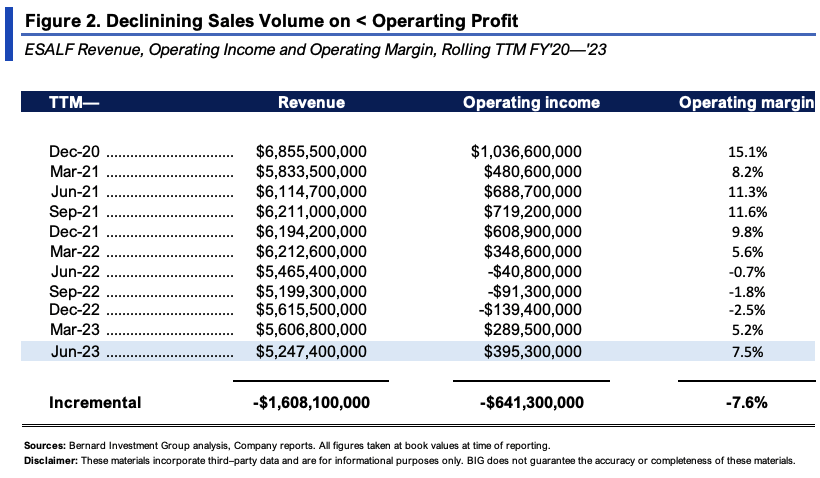

Another point I'd highlight here: ESALF's revenue and operating income have decreased at a noticeable clip each period in the last few years. Figure 2 outlines this in greater detail, on a rolling TTM basis since 2020. Over this time, TTM sales have decreased from $6.85Bn to $5.25Bn, a $1.6Bn loss. Meanwhile, operating income is down $641.3mm over this time, and operating margins have compressed by nearly 8 percentage points. This is potentially a red flag, and definitely not supportive of a company with many strong labels on the market.

{kind=link}

Figure 2(a)

Source: ESLAF Q1 FY'23 Investor Presentation

As to Leqembi , ESALF's and Biogen ( BIIB )'s breakthrough drug indicated to treat Alzheimer's disease ("AD"), there's been no major updates from the last publication. That in itself is an investment update. As a reminder, the label received approval from the FDA earlier this year. The drug is designed to slow the cognitive and functional decline in adults with AD, especially those with mild cognitive impairment or mild dementia-which is important, as you're getting patients at an earlier stage of the disease this way. Leqembi's approval was based on the results of the Clarity AD trial, which showed significant improvements in both cognition and daily function.

The thing is, it's essential for ESALF and BIIB to start getting Leqembi out to the market. Five U.S. health systems have put the drug onto their registrars, and more importantly, research from GlobalData Healthcare submitted the duo could recognize $12-$13Bn in sales off the drug by 2028, all going according to plan. ESALF is said to expect at least $7Bn of this. But there's no movement just yet, and we're yet to see the market's uptake of the drug. Furthermore, Bloomberg reports it is " facing a rocky rollout as doctors grapple with logistical issues, insurance uncertainties and complicated safety testing requirements".

ESALF is currently exploring new dosing regimens and working on developing a more convenient formulation of the treatment. Applications have been submitted for Leqembi's use in early AD treatment in various regions, and some jurisdictions have granted priority review to expedite the evaluation process. Furthermore, Leqembi is being evaluated for preclinical AD in the AHEAD 3-45 Phase III study , designed to test its effectiveness in slowing the progression of AD in patients with early cognitive impairment. The study is still ongoing, and the results are yet to be published.

2. Economic analysis of performance

Several tension points are observed when examining the company's ability to create economic value downstream.

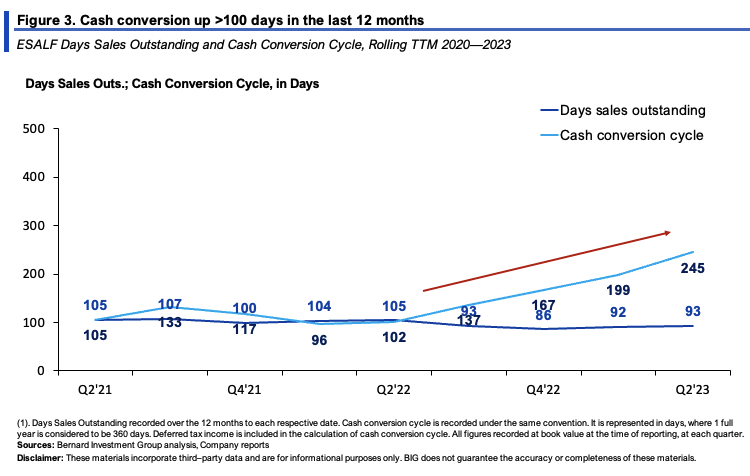

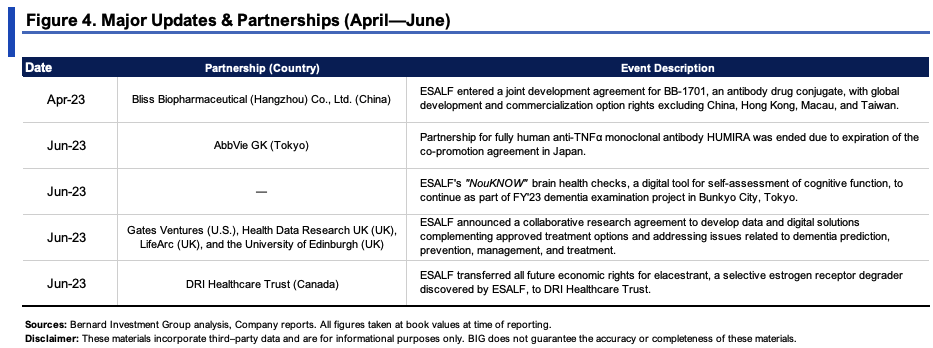

One, the company has less cash tied up in NWC, but the efficiency of this is far less apparent. The cash conversion cycle ("CCC") has increased by more than 100 days over the past 12 months, blowing out to 245 days. Said differently, each $1 put towards NWC is being recycled back to cash in 245 days, up from ~100-110 days in the past. This, as DSO has remained flat. The cause? The massive Leqembi inventory buildup is related to the points raised earlier. This is even more interesting, seeing the number of partnerships it entered into, as seen in Figure 4.

{kind=link}

{kind=link}

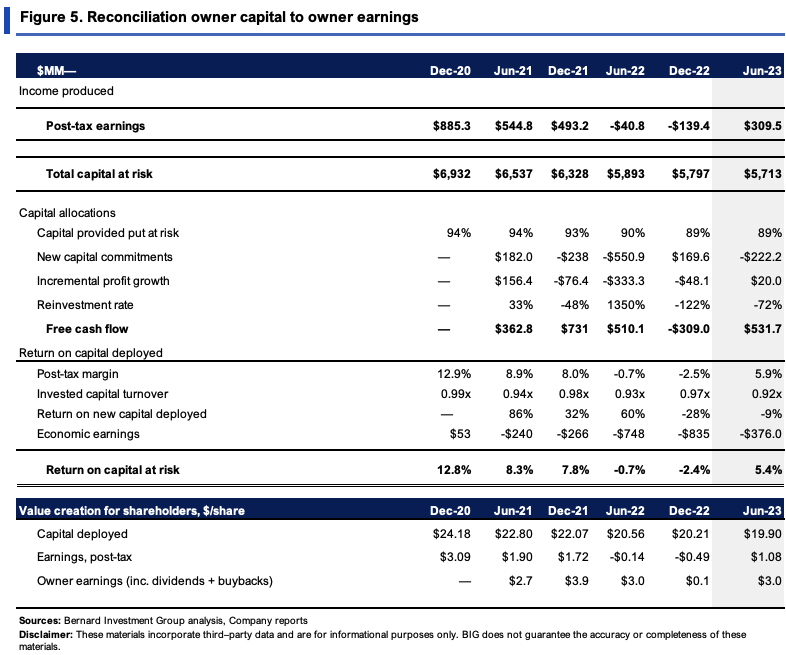

Two, ESALF's capital intensity is apparent in Figure 5. It has leaned up in terms of capital at risk, with $5.7Bn or $19.90/share employed into the business as I write. This produced $1.08/share in trailing NOPAT last period, just a 5.4% return on investment. Going back to 2020, there's been no major difference on this, in fact, the rate on capital has been declining on aggregate the entire time.

Three, driving the soft result are ESALF's post-tax margins, just 6% last period. This is not the norm for most pharma players. Typically, it is the post-tax margins where pharmaceutical companies actually excel in , given the strength of their patents, low fixed asset intensity, and high product sales. Capital turnover isn't always the best because capital usually doesn't produce the profits for pharma companies. For ESALF, both margins and capital turnover are unreasonably tight, leading to sub-standard returns on capital. This is a risk in my view.

{kind=link}

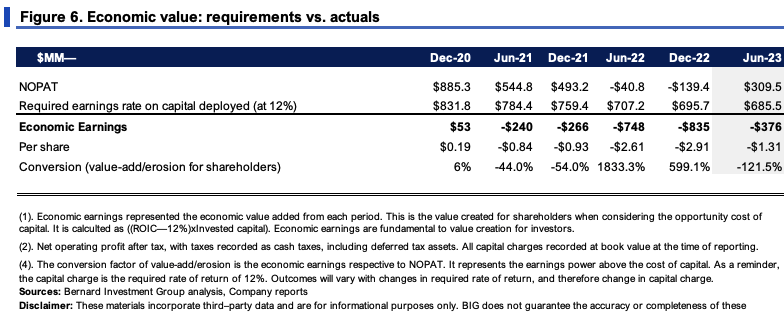

Four, the above points mean ESALF isn't creating meaningful value for shareholders. The lack of economic value this presents for investors is quantified in Figure 6, showing what the company should have produced on its capital invested at a 12% hurdle rate. The 12% is relevant as it represents long-term market averages. Any NOPAT above the 12% charge on ESALF's invested capital is economic earnings, anything below, economic losses. You can see persistent economic losses over the testing period, thrown off by ESALF's operating numbers. As you may guess, economic profits are the preferred option.

{kind=link}

Valuation and conclusion

The stock sells at high premiums of 48.7x earnings and 43.6x forward EBIT, 70% and 171% premiums to the sector respectively. I find it difficult to see ESALF moving into these kinds of valuations, let alone trading at higher multiples from here, given what's been presented today. The dividend yield is at 2% as I write this, and isn't enough to overcome these challenges. At a 43.6x forward multiple, this implies that consensus expects ~$379mm at the current market cap. ESALF also sells at 3.4x forward sales, and consensus expects $4.95Bn at the top this year. Assigning the 3.4x multiple to this derives a market value of ~$16.6Bn, in line with the company's current value. To me, this suggests the bulk of growth expectations have been well captured in ESALF's current market cap, supporting a hold rating.

In short, ESALF's Leqembi label has the potential to be a large catalyst downstream. But we've no market data to work with just yet. Instead, at the company level, it's been a series of downsides in turnover and operating margin, carrying through to a series of economic losses for shareholders. The question of opportunity cost immediately presents itself here. In my view, there are more selective opportunities available to position against right now. Hence, I'm paring back my rating on ESALF to a hold.

For further details see:

Eisai: Lumpy Rollout Of Leqembi, Economic Value Hard To Ascertain (Rating Downgrade)