LOCO - El Pollo Loco: Foggy H2 Outlook With Weak Industry-Wide Traffic

2023-10-04 00:30:55 ET

Summary

- El Pollo Loco's stock is resting near 52-week lows after a weaker Q2 reported than I expected.

- While the company called out better trends to start Q3, decelerating industry-wide traffic may have weakened post-July, giving little visibility into a Q3 beat.

- In this update, we'll look at industry-wide trends, LOCO's positioning geographically in states with steadily rising minimum wage & whether the stock offers a margin of safety.

Roughly one year ago , I wrote on El Pollo Loco ( LOCO ), noting that with the company committing to buybacks and a special dividend, the stock offered a decent reward/risk if it dropped below $10.00. After briefly dipping below $10.00 in early January, the stock enjoyed a ~30% rally but has since given up all of its gains and has found itself near new 52-week lows. However, while disappointing, much of this decline looks justified, with the company reporting anemic comp sales growth in Q2, even if adjusting for tough comparisons following its successful Beef Birria launch in the prior year quarter. In this update, we'll dig into recent results, industry-wide trends, and whether the stock is offering a margin of safety.

{kind=link}

Recent Results & Upcoming Q3 Results

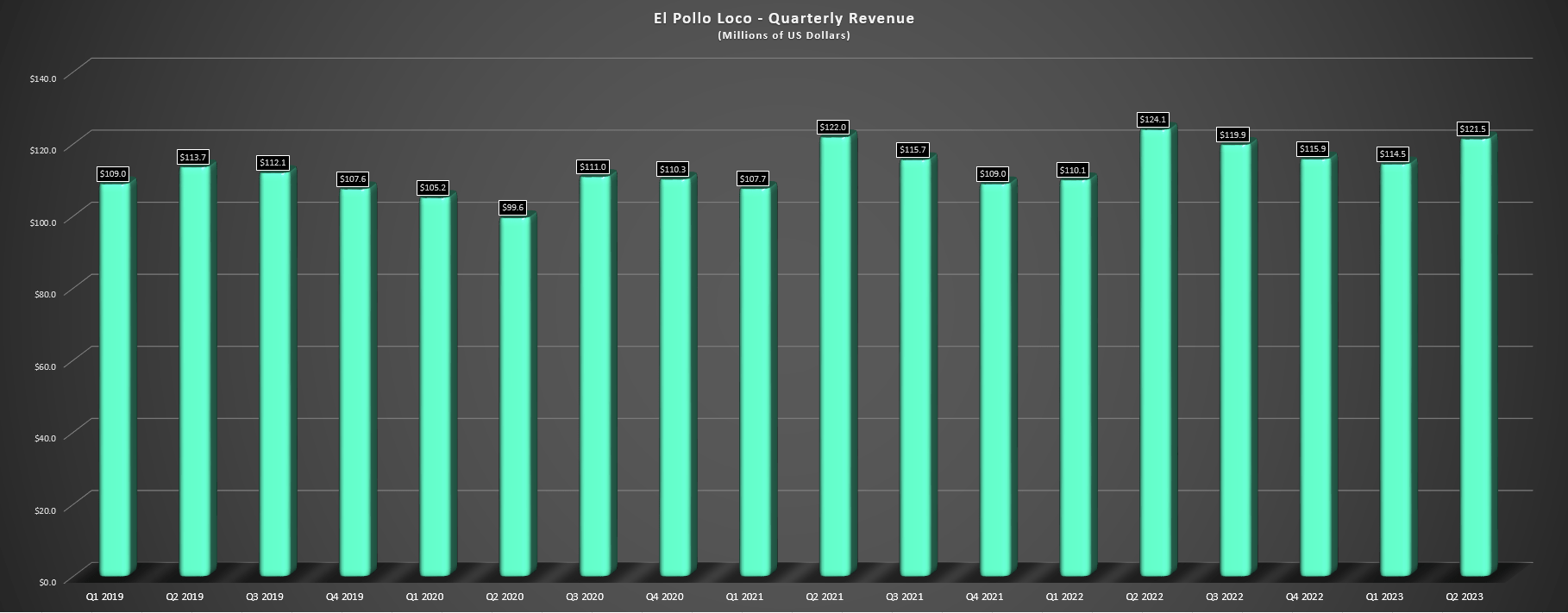

El Pollo Loco released its Q2 results in August, reporting a 2% decline in revenue growth ($121.5 million vs. $124.1 million), negative comp sales growth despite menu pricing of ~9.0%, implying a sharp decline in traffic. And while the company deserves a minor pass because of having to lap difficult comparisons from its Beef Birria LTO, which was a hit and helped to drive 7.5% comp sales growth in Q2 2022, the results were still below my expectations, especially given the level of effective pricing. Meanwhile, from revenue and system-wide sales standpoint, system-wide sales sunk on the back of fewer transactions partially offset by higher check, while revenue slid as well, which was partially related to company-owned restaurants sold in the period, a minor headwind.

El Pollo Loco - Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

As for restaurant revenue, the company reported a 2.3% decline in company-owned comparable restaurant sales to $103.9 million, with a 4.5% decline in transitions offset by a 2.3% increase in check due to menu pricing and less company-owned restaurants, with four sold in the period. Unfortunately, the results weren't much better for its franchise business, with franchise revenue up to $10.1 million on the back of eight franchise restaurant openings and four restaurants sold to existing franchisees, but partially offset by a 4.1% comp sales decline. This represented the second consecutive comp sales decline for its franchised restaurants, and comp sales significantly underperformed other brands like Chipotle ( CMG ) with high single digit comparable sales.

When questioned about the difficult results, the company noted that its Beef Birria fell relatively flat on the second attempt and that it saw some pullback in frequency from lower end consumers as well as check, which certainly is not ideal. The silver lining is that the company did note that things were trending a little better in Q3 from a quarter-to-date basis as of its early August Q2 Conference Call, with better results at lunch and dinner. However, OpenTable stats suggest that traffic got worse at least for seated diners over the quarter, with traffic appearing to peak in late July to early August before rolling back into sharply negative territory. So, although the company was cautiously upbeat on Q3, it's hard to get a clear read through into how the rest of the quarter went when traffic appeared to have trailed off in August and September across most segments.

{kind=link}

Finally, from a margin standpoint, El Pollo Loco enjoyed lower food & paper costs (27.4% vs. 29.8%), with help from its high single-digit pricing in the period. That said, labor costs remained elevated at 31.1% (+10 basis points year-over-year) and occupancy and other costs also crept up (+ 30 basis points year-over-year), a drag on the higher contribution margin from lower food and paper costs. Unfortunately, less overtime pay was mostly offset by the impact of minimum wage increases in California (higher wage rates), wage increases due to competitive pressure, and also higher costs due to improved management staffing. The result was that margins improved year-over-year to 16.9% with restaurant contribution of $17.6 million, but this is still well below pre-COVID-19 levels.

Recent Developments

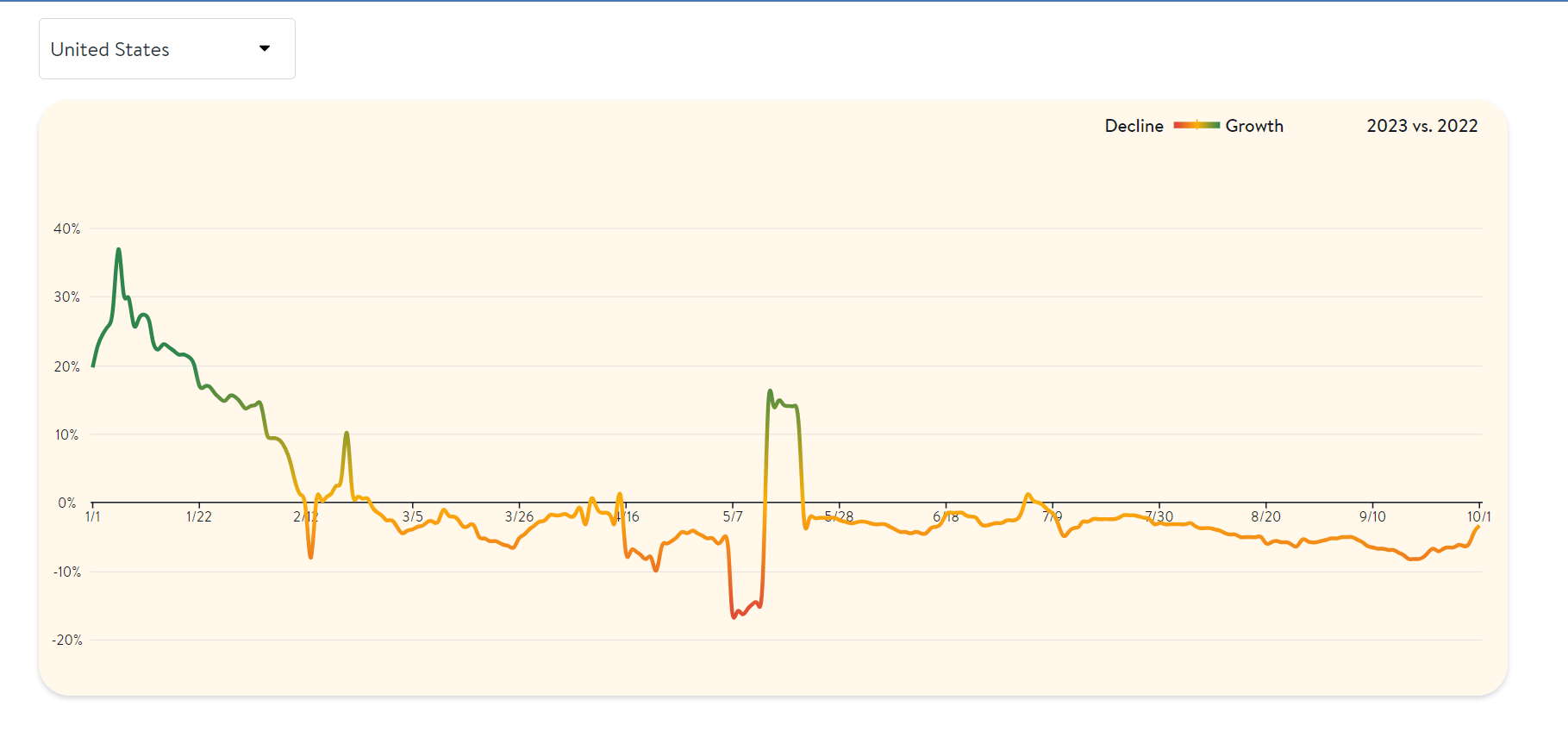

While it's been a tough year for traffic already for most restaurant brands, the recent rise in gas prices hasn't helped (Q3/Q4 2023 vs. Q2 2023), with this placing a further pinch on already light wallets as consumers deal with rising grocery prices, rising mortgage/rent payments, and rising utility costs. And while El Pollo Loco is fortunately positioned in the quick-service and fast casual space with a lower average ticket, the comp traffic declines have affected nearly all brands. We can see this in stats from Black Box Intelligence August comp traffic, which was negative yet again at 2.9%, with exceptions being Italian (cuisine) and quick-service (segment) which performed the best.

Black Box Intelligence August Comp Sales Data - Black Box Intelligence

{kind=link}

Unfortunately, this slowdown has been present at casual dining as well, and Darden ( DRI ) has noted some potential signs of check management , something the industry seemed to evade despite things getting tight last year as well. As noted earlier, this makes it tough to be overly optimistic about the second half of the company's Q3 results and certainly Q4 with consumers now contending with higher gas prices that have stabilized at a higher level since Q2. Hence, I think it's difficult to have much confidence in a beat on sales or earnings for El Pollo Loco when it reports its Q3 results in November, with estimates currently sitting at ~$121.0 million and $0.19, implying barely 1% revenue growth year-over-year.

However, while there's less visibility into the top line due to waning consumer confidence, it's not easy to be bullish about the company's bottom line either if one takes a medium-term view. This is because the company already warned in its 2022 Annual Report that it could be impacted by California's proposed FAST Act which could lead to dramatically higher labor costs. Since voted in, the most recent development is that fast food workers' minimum wage will increase to $20.00 next year in California. Plus, Nevada's minimum wage is also set to jump ~20% next year, another key market for El Pollo Loco. So, while some other restaurants have been able to see margin improvement with some commodity deflation, any benefit on the commodity side could be eroded by continued wage pressure in El Pollo Loco's top markets.

On a positive note, quick-service and fast-casual brands have the option to lean into automation, and self-serve kiosks that El Pollo Loco has deployed at some of its system is a way to help reduce labor costs. If this proves successful, this could help to remove some labor from restaurants where usage is high. That said, although this a proactive measure that could help lift margins, the fact is that its competitors are getting stronger and also have the muscle to invest in automation like Chipotle ( CMG ) and Del Taco ( JACK ). So with tough competition that is better capitalized and a tough macro environment with the potential for rising costs, I'm not sure that El Pollo Loco will be able to justify its previous multiples when sub 16% restaurant margins look like the new normal if labor pressures persist.

Valuation

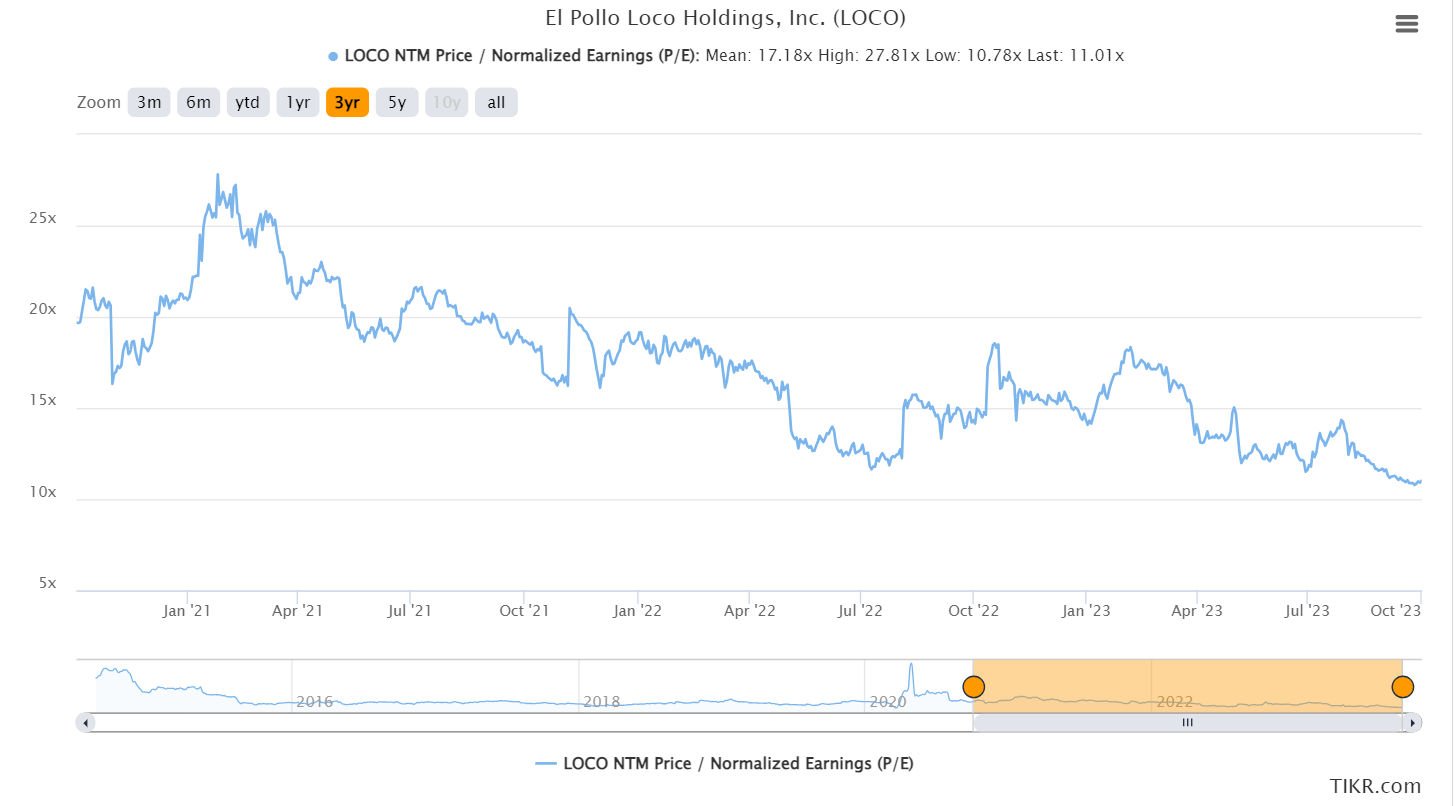

Based on ~36 million shares and a share price of $9.00, El Pollo Loco trades at a market cap of ~$300 million and an enterprise value of ~$565 million, making it one of the lowest capitalization stocks in the industry. This has left the stock hugging the lower rail of its historical range from an earnings multiple standpoint over the past three years, with the stock currently trading at just ~10.7x FY2024 earnings estimates and just ~8.8x EV/EBITDA, a discount to most of its fast-casual peers that trade at over 10.0x EV/EBITDA and over 15.0x earnings. That said, the current environment is not like the last three, and arguably not like the last decade either, with rates surging to multi-decade highs, and it being a long and brutal winter for micro-cap stocks, evidenced by the iShares MicroCap ETF ( IWC ) not taking part whatsoever in the year-to-date rally. So, adjusting this for environment, it's not that surprising that El Pollo Loco trades at such a deep discount to its 3-year average (~17x earnings).

El Pollo Loco - Earnings Multiple & Historical Earnings Multiple - TIKR.com

{kind=link}

Adding insult to injury, El Pollo Loco's results this year have been below my expectations, and the margin outlook isn't great given the continued pressure on wages in its core markets. In fact, the company's top two markets (California and Nevada) will see significant minimum wage increases next year for fast-food restaurants, with Governor Gavin Newsom signing legislation to solidify an increase to $20.00 per hour , a ~20% hike from current levels next April. Meanwhile, Nevada's minimum wage will increase to $12.00 as of July 2024. Given that ~71% of El Pollo Loco's revenue came from the Greater LA area and over 80% of El Pollo Loco's system was based in these two states, the continued pressure on wages certainly isn't an ideal development, and it makes El Pollo poorly positioned relative to some of its industry peers with a less chunky West Coast weighting.

Given this unfavorable geographical weighting, the multiple compression we've seen in small-caps and the company's relatively low unit growth rate, I think a more conservative multiple for El Pollo Loco is 12.5x, well below its mean multiple of 17.0x over the past few years. If we apply this multiple to FY2024 earnings estimates of $0.85, this translates to a fair value for the stock of $10.65 pointing to a 17% upside from current levels. While this upside might interest some investors, I am looking for a minimum 35% discount to fair value to justify starting new positions in sub $1.0 billion companies to ensure a margin of safety. After applying this discount, LOCO's ideal buy zone doesn't come in until $7.00 or lower, suggesting the stock is still not in a low-risk buy zone despite its recent underperformance.

Summary

El Pollo Loco may have enjoyed a bump in margins in Q2, but restaurant margins are down over 300 basis points since Q2 2019 and it's hard to be optimistic about the company's ability to claw back margins with minimum wage increases in its core markets. Plus, with less room to keep raising menu prices given the pullback we've already seen in traffic industry-wide, the setup is not ideal short term. It's possible I could be overly worried about the margin impact of steady labor increases in key markets, and El Pollo Loco may innovate through automation and menu to grow traffic and reduce costs to reduce this impact. Still, with no clear margin of safety for the stock at current levels, I don't see any way to justify paying up for the stock above $9.00 here.

For further details see:

El Pollo Loco: Foggy H2 Outlook With Weak Industry-Wide Traffic