LOCO - El Pollo Loco: Patience Required

2023-12-14 06:01:41 ET

Summary

- El Pollo Loco's Q3 results showed barely positive comp sales growth and underperformed my expectations, especially considering ~7% effective pricing.

- On a positive note, the company is taking steps to improve margins and hopes to accelerate unit growth, including the rollout of kiosks and new salsa processing equipment.

- In this update, we'll dig into the Q3 results, industry-wide trends, and whether the stock is worth owning with the potential for higher unit growth on the menu.

Just over two months ago I wrote on El Pollo Loco (LOCO), noting that while the company had called out better traffic trends in Q3, industry-wide traffic was suggesting a high likelihood of deceleration and a reversal of these positive trends. This view that a deceleration looked likely has been confirmed with the release of the Q3 results, with system-wide comp sales coming in barely positive, with the stock significantly underperforming its peer group, [the AdvisorShares Restaurant ETF (EATZ)] since its October lows. On a positive note, October sales have picked up, the company is pulling levers to improve margins to combat the negative effects of AB 1228, and management appears confident that it can accelerate unit growth. In this update we'll dig into the Q3 results, industry-wide trends, and whether the stock is worth owning with higher unit growth on the menu.

{kind=link}

Q3 Results

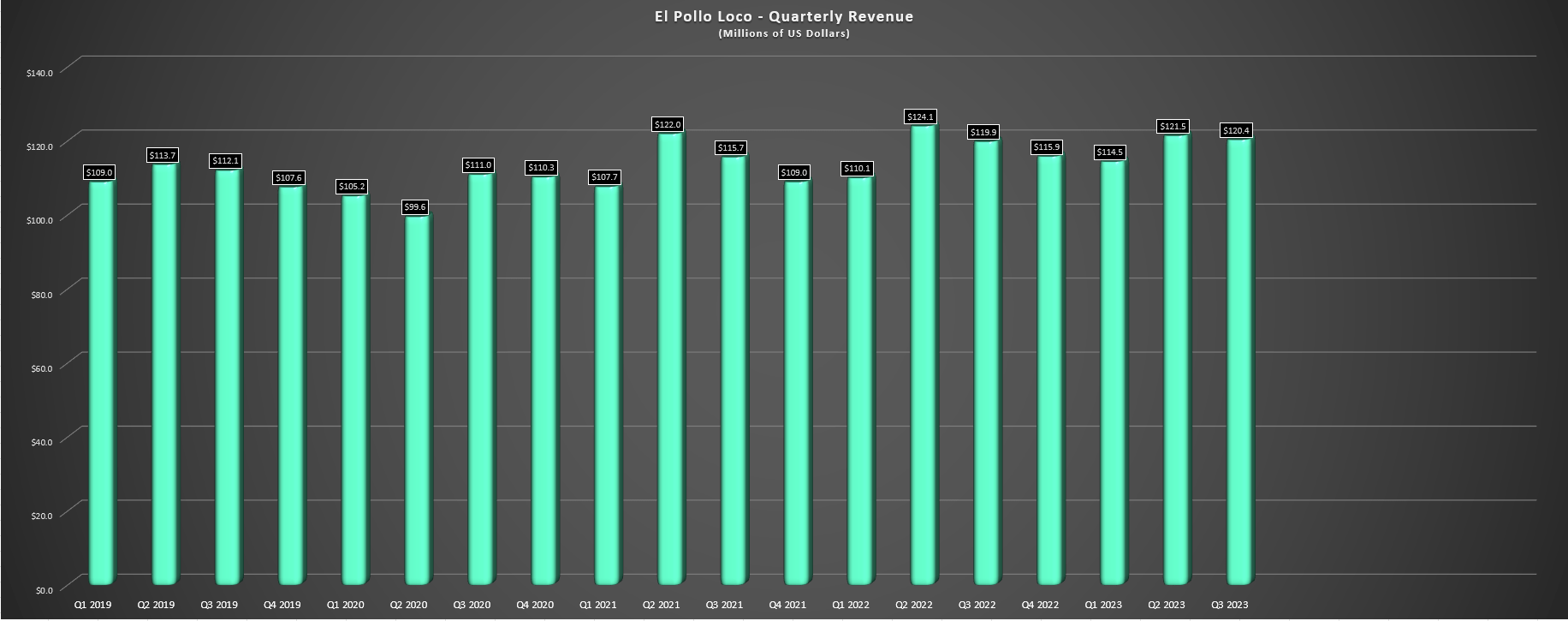

El Pollo Loco released its Q3 results last month, reporting quarterly revenue of $120.4 million, a 0.4% increase from the year-ago period. The lack of revenue growth relative to peers was partially related to company-owned restaurants sold to franchisees which dinged company-operated restaurant revenue (partially offset by new openings and menu price increases), offset by a 7% increase in franchise revenue to $10.3 million. Meanwhile, comp sales came in below my expectations on a system-wide basis at just 0.8% (implying traffic declines relative to ~7% effective pricing), and two-year stacked company-wide comp sales came in at just 3.9%, well below peers like Restaurant Brands International (QSR), Chipotle (CMG) and others that are sitting atop the leaderboards for industry-wide share price performance. Fortunately, traffic did improve in October up from a rough September, but the company will be lapping tougher comps with 2.5% pricing rolling off mid-quarter.

El Pollo Loco Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

Moving over to margins, there wasn't much to write home about here either, with restaurant contribution margins coming in at just 14.4%, up 200 basis points year-over-year but still down nearly 400 basis points from pre-pandemic levels (Q3 2018: 18.3%). The improvement in margins stemmed from leverage on food and paper costs with menu price increases offsetting commodity inflation and slightly lower labor costs with reduced overtime pay offset by higher wages from minimum wage increases in California and "other labor wage increases as a result of competitive pressure". At first glance, this increase in margins might appear positive, but I'm not sure how sustainable menu price increases are with some consumers getting close to being tapped out, and while labor improved 10 basis points, the California fast food minimum wage increase will be rearing its head on April 1st, 2024 (increase to $20.00/hour and well above national average).

Finally, as for the financial results, El Pollo Loco reported adjusted earnings of $6.4 million (excludes $4.9 million gain related to the sale of 17 restaurants), and reported adjusted EBITDA of $15.0 million. Both figures improved year-over-year, and earnings per share [EPS] was also up meaningfully, helped by significant share repurchases year-to-date and 2.5 million shares purchased as part of a purchase agreement for $10.63 per share. Plus, subsequent to quarter-end, the company purchased an additional 1.5 million shares at a price of $8.40 from the same seller (FS Equity Partners V, L.P., and FS Affiliates V, L.P.), with it getting a more attractive this time around. Overall, this reduction in the share count combined with the potential for improved unit growth has helped to stabilize annual earnings per share, with annual EPS set to increase 23% year-over-year based on current estimates, clawing back most of the losses last year.

El Pollo Loco - Annual Earnings Trend - Company Filings, TIKR, Author's Chart

{kind=link}

Recent Developments & Industry Wide Trends

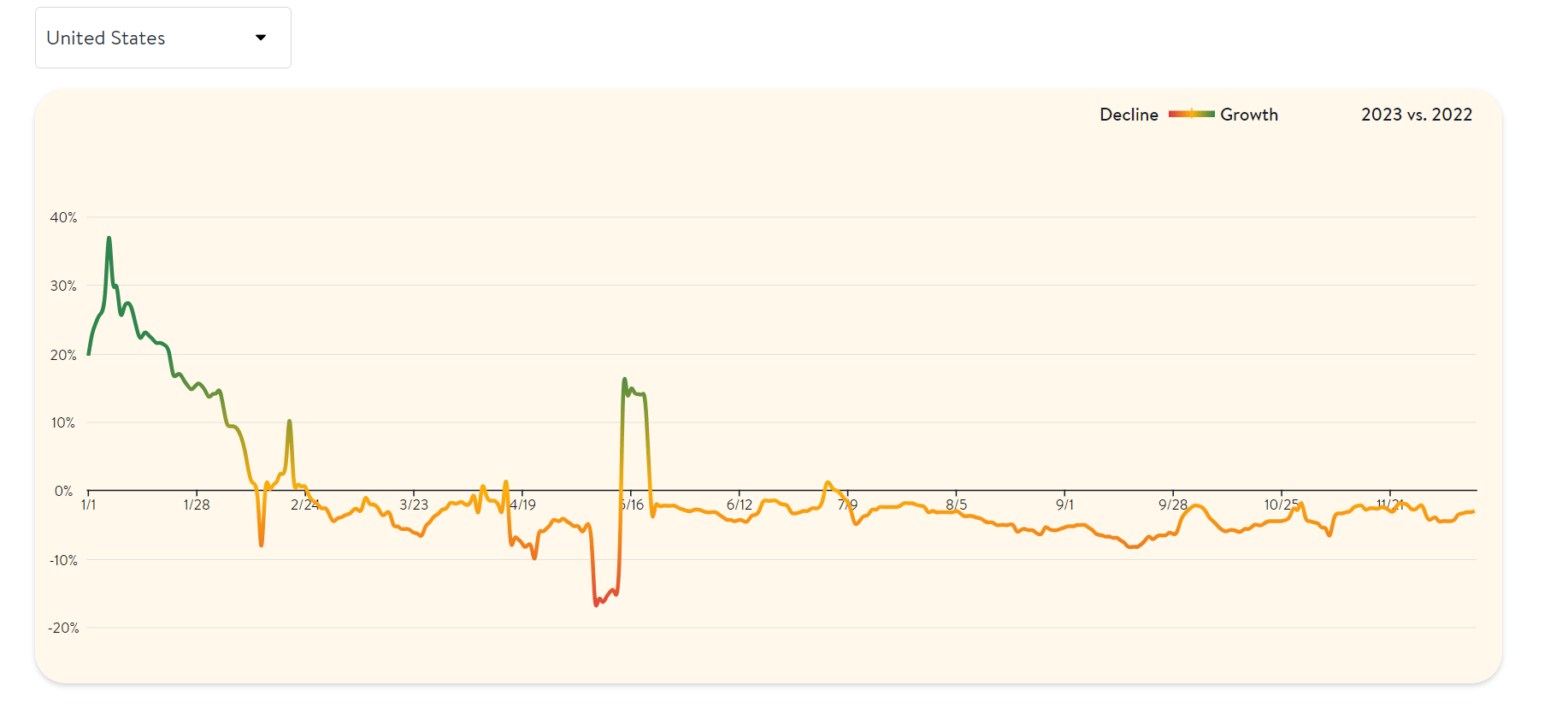

Starting with the negative trends, industry-wide traffic continues to be an issue, with traffic growth remaining negative for over consecutive months with no spikes back into positive territory. This is a significant change of character from February through June (once past the easy Omicron comps) when the trend was lower but there were brief periods of seated diners growth, suggesting that some consumers may finally be seeing the pinch and cutting dine-out occasions or at least reducing their frequency materially. And while this data doesn't correlate perfectly with fast-casual and quick-service brands, we are seeing similar trends across these concepts with quick-service which was holding up the best also dropping into negative territory from a traffic standpoint this fall. The other negative development in the decline in traffic at steakhouses, suggesting that even some more affluent consumers might be pulling back a little and/or trading down.

{kind=link}

The second negative worth discussing is that minimum wages are set to increase to $20.00 per hour for fast food restaurants in California as of April 1st, 2024, a negative development from a wage inflation for El Pollo Loco that has ~80% of its system and ~75% of company-owned restaurants in the state. Among industry peers, this makes El Pollo among the most exposed to this wage pressure which certainly isn't a great position to be in, and while the company did shed 7 company-owned California restaurants with its recent sale of 17 restaurants, the company still has a significant portion of company-owned restaurants that could see a margin hit. To put this concentration of its system in California in perspective, Chipotle has just ~14% of its restaurants in California, a significantly lower number than El Pollo Loco.

The good news is that the company has acknowledged this disadvantage, has noted that it is seeing positive test results from kiosks that have worked well for Shake Shack (SHAK) domestically and Burger King (QSR) both domestically and internationally, and also noted that it's also rolling out new salsa processing equipment. The latter will be easier to use and clean and provide more consistent salsa, while the former has shown a slight increase in average check (consistent with Shake Shack), and could also allow the company to repurpose or reduce labor, which would certainly be a win given the sharp increase to minimum wages coming into effect.

"And given our geographic mix, especially for our company-owned restaurants, we need to grow sales, leverage technologies better, to become more efficient and to help offset some expected incremental costs we anticipate from upcoming legislation changes."

- El Pollo Loco, Q3 2023 Conference Call

As for the kiosks, El Pollo Loco noted in its Q1 results that it had rolled them out across a small portion of the system, and the company has now stated that it will be rolling them out "as quickly as possible" given the encouraging results (reduced labor hours per day). Overall, I would consider this a positive development as it is a way to potentially claw back some lost margins, but the roll-out is being held up short-term by having to procure associated cash machines and it's not clear yet whether this will drive higher margins or simply offset some of the upcoming potential margin hit from minimum wage increases in California. El Pollo Loco initially provided more detail on the kiosk rollout below:

"Yes. So, as part of the tests that we are doing these kiosks, we are also testing the ability to move labor. And a key part of the test that we are finding is the kiosks need to be at the front counter. You don't want to have them elsewhere in the restaurant because we are seeing a much bigger response when you are at the front counter. And we are also finding for our customers at least that you want to have cash machines available so they can use cash. Because again, we are finding where we have cash machines, the usage is much higher. But the bottom line is we are seeing good average check growth really across the board. And certainly, in those restaurants with the high kiosk usage, we are going to be testing, reallocating labor and possibly removing labor."

- El Pollo Loco, Q1 2023 Conference Call

Overall, the company acknowledging that it needs to work on technology and innovation is certainly a step in the right direction, and it's nice to see the company also sharing that it is looking to accelerate unit growth with it confident that it can be a national brand. This view was outlined following its IPO nearly a decade ago and certainly lagged growth estimates, so it will be interesting to see if the company has better execution this time around. All that being said, it's difficult to be gung-ho about owning underperforming restaurant stocks given the erosion in traffic we're seeing industry-wide. And this is especially true with low gas prices (relief for consumers from an expenses standpoint) not leading to any recovery in traffic this time around. Let's look at LOCO's valuation to see whether a margin of safety is in place to suggest there's room for meaningful upside if the turnaround here is successful:

Valuation

El Pollo Loco trades at a market cap of ~$285 million and an enterprise value of ~$540 million, making it one of the lower capitalization names industry-wide, just ahead of other names like Red Robin Gourmet Burgers (RRGB) and Noodles & Company (NDLS). This relatively low capitalization can be attributed to the company's industry-lagging growth vs. fast casual and quick-service peers, with El Pollo Loco seeing limited growth over the past five years, with its system growing by barely 10 restaurants and certainly lagging its stated 2014 plans to grow at 8-10% long term , and the company achieving barely 18% total growth since year-end 2014 (~2% annual growth). Simultaneously, margins have fallen off a cliff and headwinds remain (heavy California weighting with negative impact from AB 1228), with restaurant contribution margins down from ~22% in 2015 to "15-16% range" this year and 15.4% year-to-date.

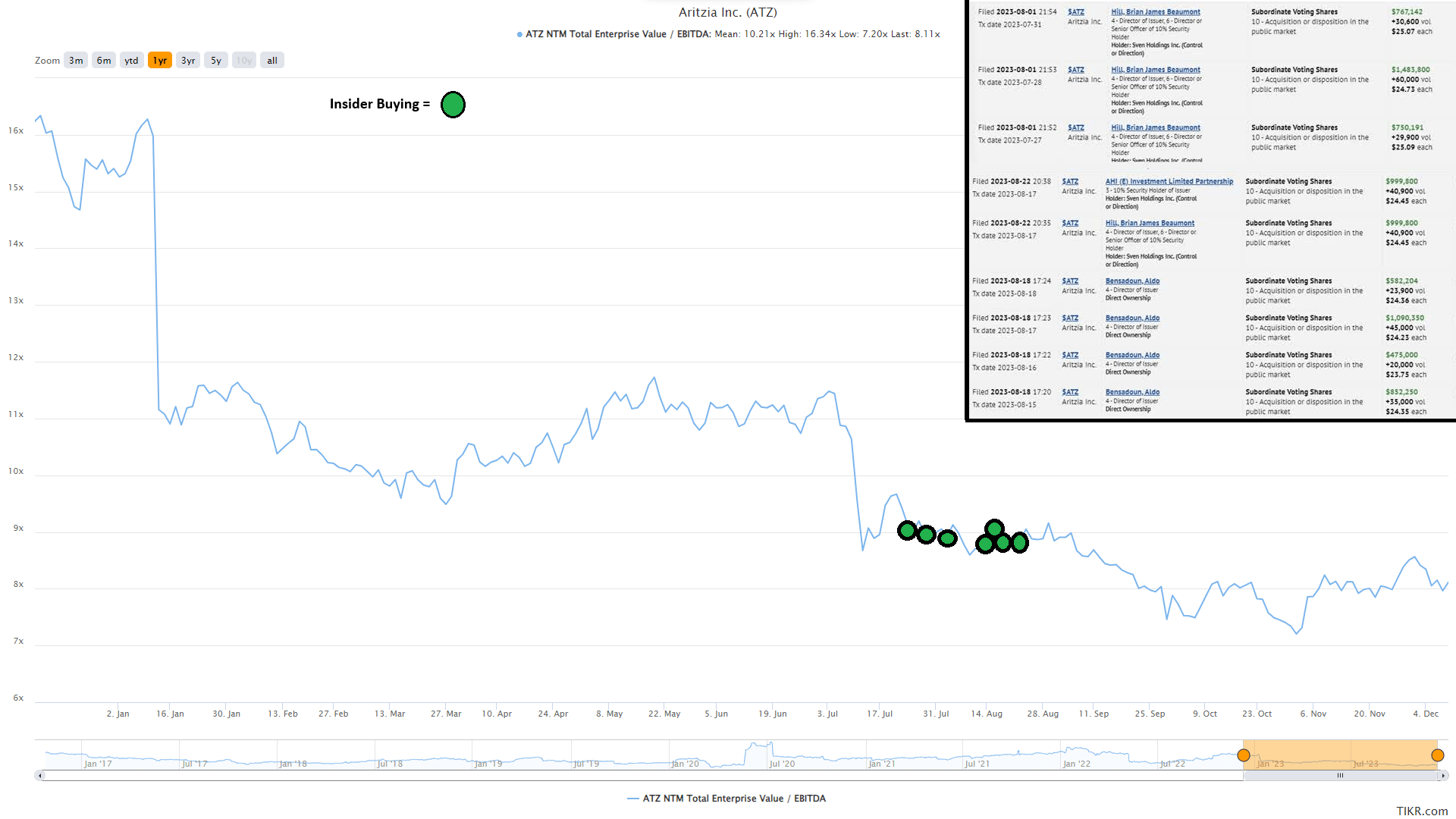

El Pollo Loco - Historical EV/EBITDA Multiple & Current Multiple - TIKR.com

{kind=link}

Based on the company's heavier weighting to California which could push up wage inflation relative to peers and lower unit growth rates (regardless of whether the goal is now acceleration), I believe a more fair multiple for the stock is 10.0x EV/EBITDA in line with some of its other smaller-scale and lower growth peers. Plus, as the chart above shows, despite being down 30% from its 2023 highs, LOCO doesn't trade at much of a discount to its historical multiple. So, even if we assume $58 million in EBITDA in 2024 with the benefit of increased kiosks across the system and assume a lower share count of ~30.5 million shares, I see a fair value for the stock of $10.65. And after applying a 30% discount to estimated fair value to ensure an adequate margin of safety, the stock is still not in a low-risk buy zone despite its underperformance, with an ideal buy zone of $7.50 or lower. Besides, with higher-growth names like Aritzia ( ATZ:CA ) trading at lower multiples with significant insider buying, I continue to see more attractive bets elsewhere in the market today.

{kind=link}

Summary

El Pollo Loco had a disappointing Q3 with industry-lagging comp sales growth and while margins did improve, it was largely due to being up against easy year-over-year comparisons. On a positive note, the company appears to have a plan in place to turn things around, it continues to aggressively buy back shares, and sales did improve in October in line with the industry. However, the stock is staring down AB 1228 which should impact wage inflation next year, and I don't see enough margin of safety for LOCO just yet with it trading only marginally below its historical multiple. Hence, while the ingredients might finally be in place for a potential turnaround, I would need a dip below US$7.50 to become more interested in the stock.

For further details see:

El Pollo Loco: Patience Required