ESTC - Elastic: A Solid Buy For The Age Of Data Despite Premium Valuation

2023-11-29 05:02:39 ET

Summary

- Elastic offers unique tools for modern data management, making it pivotal in fast data discovery for AI applications.

- The company demonstrates consistent double-digit revenue growth and positive cash flow, showcasing financial resilience.

- ESTC's premium valuation may be justified by its remarkable growth rates, margin expansions, and promising prospects in the AI domain.

Elastic N.V. ( ESTC ) often finds itself sidelined in discussions surrounding AI-centric stocks, yet its significance in the realm of data and AI applications is profound. Despite sporting a comparatively higher valuation, Elastic consistently demonstrates strong execution, surpassing analysts' expectations in both EPS and revenue. The initial valuation multiples might seem substantial, but the company's robust growth rates and promising future prospects make it a compelling investment choice in today's market. As an investor, recognizing Elastic's pivotal role amidst these technological landscapes underscores its potential value, despite the apparent premium.

Elastic's unique offering enables modern AI and data analytics stack

Elastic stands out in the tech landscape for its distinctive offerings that cater to modern data solutions. With products like Elasticsearch, Kibana, and Logstash, it provides an ecosystem that enables companies to manage and derive insights from vast volumes of data.

For instance, Elasticsearch, its flagship product, offers powerful search and analytics capabilities, allowing businesses to efficiently navigate and explore their data in real-time. Kibana complements this by offering visualization tools, enabling users to create insightful dashboards and reports. Additionally, Logstash serves as an essential component, facilitating the collection and processing of data from various sources.

In the era of burgeoning AI applications, Elastic's tools are well-positioned to capitalize on the AI boom. Fast data discovery is crucial in the AI landscape, and Elastic's solutions address this need. Leveraging its capabilities, organizations can swiftly access and process data, a fundamental requirement for training and deploying AI models. Elastic's technology aids in rapid data retrieval and analysis, making it an integral part of the infrastructure for companies delving into AI-driven insights and decision-making.

Elastic's uniqueness lies not only in its innovative product offerings but also in its widespread adoption across a vast array of companies. With a staggering customer base of over 58,000, (including giants like Microsoft ( MSFT ) or Amazon ( AMZN )) Elastic has solidified its position as a go-to solution for diverse data-related needs. This extensive adoption not only showcases the product's versatility but also creates a significant barrier to entry for potential competitors, fostering a loyal customer base and enabling Elastic to retain its pricing power, which in turn should help the company increase its profitability.

Elastic demonstrates stellar financial execution

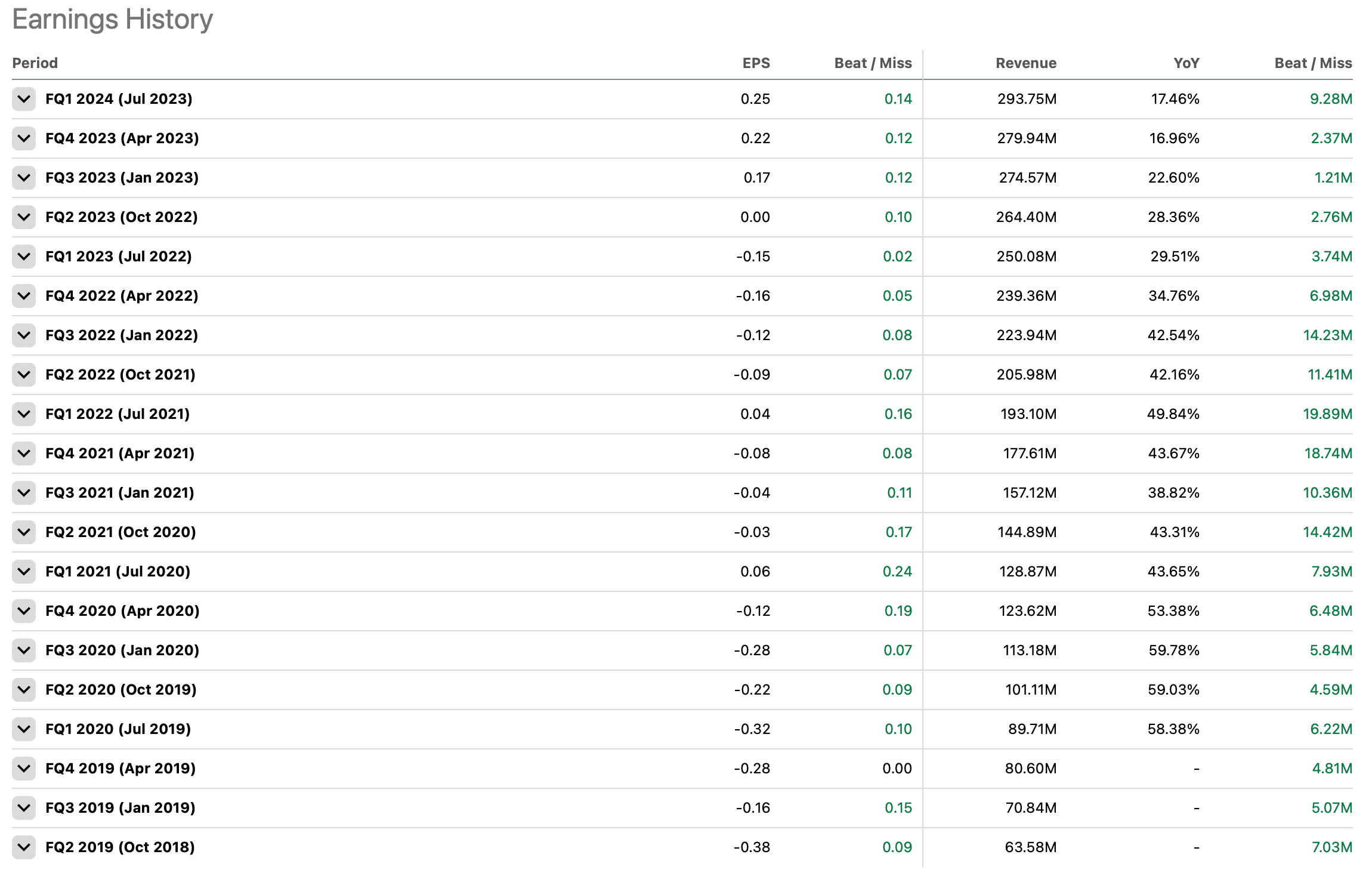

When it comes to financial execution, Elastic has shown notable strength in recent quarters.

For instance, in FQ1 2024, (the quarter ending in July 2023 and reported at the end of August) Elastic achieved a notable 17.5% year-over-year revenue growth and a significant improvement in EPS, reaching $0.25 on a non-GAAP basis. With this, the company exceeded analysts' expectations by a solid margin. Remarkably, the company has consistently surpassed anticipated outcomes in every single quarter since going public in 2018, based on data from Seeking Alpha.

{kind=link}

Elastic's financial performance reflects a positive trajectory across various metrics. Over the past five years, the company has consistently achieved double-digit revenue growth, signaling a steady expansion. A substantial portion of its revenue is attributed to subscriptions, boasting an impressive gross margin of nearly 80%. Importantly, this surge in revenue has not been mirrored by a proportional increase in the cost of revenue, emphasizing the company's efficient cost management strategies.

Moreover, Elastic demonstrates a consistent commitment to R&D spending, maintaining a sufficient budget for enhancing and innovating its solutions without a significant need for escalating expenses over time. For instance, in FQ1 2024, R&D expenses went up by a mere 3%.

Notably, the company maintains positive cash flow from operations, as certain expenses tied to stock-based compensation weigh on the GAAP profitability figure. This helps Elastic keep a stellar balance sheet, with more than $950 million in cash and marketable securities and only $568 million in long-term debt, which significantly reduces financial risk for the stock.

Valuation is steep, but it might be justified by performance and future growth prospects

Regarding valuation, the situation might not seem clear initially, as ESTC's valuation multiples appear expensive. ETSC trades at an approximately 70 P/E ratio, based on EPS projections for FY 2024 (ending April 2024), and a 51 P/E for FY 2025 earnings. These multiples are uncommon in the current market, even among software and AI companies.

However, Elastic's premium valuation seems justifiable considering several key aspects. First, while the company's Price-to-Sales (P/S) ratio stands at 6, which might seem relatively high, it's not excessively inflated within the industry, especially considering Elastic's ongoing improvements in profitability margins. This progress underscores the company's ability to generate more earnings from its revenue over time, indicating a positive trajectory in terms of financial health.

Furthermore, Elastic's expected EPS growth is staggering, with forecasts indicating a substantial uptick. Projections suggest an impressive 335% EPS growth in FY 2024, followed by a continued strong growth rate ranging between 36-37% in FY 25 and beyond. Even in the long term, an average EPS growth rate of 30-40% over the next decade is anticipated, especially given Elastic's extensive involvement in AI-related ventures.

Considering such high EPS growth rates, the Price/Earnings to Growth ((PEG)) ratio, which ideally hovers around 1, isn't remarkably high, currently resting at approximately 1.5 based on EPS growth projections. Given Elastic's consistent history of surpassing EPS expectations significantly, the actual PEG ratio might be even lower, substantiating the argument for its premium valuation.

What to watch for in the upcoming reports

Investors should remain vigilant regarding Elastic's future performance despite its positive trajectory. A few critical points warrant close observation in the upcoming reports.

Firstly, Elastic's progression toward achieving GAAP profitability is a crucial metric to watch. The company has showcased commendable improvements in its margins, but the persistent high stock-based compensation hampers its path toward consistent GAAP positive income.

Secondly, tracking the revenue growth pattern is vital. Although Elastic maintains a robust revenue growth rate, approximately 17%, with a similar outlook for FY 2024, it's noteworthy that this growth has slightly decelerated from the higher rates of 30-50% seen previously.

Lastly, monitoring the net expansion rate is essential. While Elastic currently boasts an impressive rate of 113%, which reflects healthy client retention and growth, observing trends in this metric over time is crucial. Similarly by revenue nature companies like Twilio ( TWLO ) have witnessed a decline in this rate, indicating potential shifts in client behaviors or market dynamics that could affect Elastic's growth in the long run. Therefore, keeping an eye on these indicators will provide investors with a comprehensive understanding of Elastic's ongoing performance and future prospects.

Key takeaways

Elastic stands as a unique player in the tech landscape, offering indispensable tools for modern data management. As AI applications burgeon, Elastic's role becomes pivotal in fast data discovery, crucial for AI's success. Its tools expedite data access and processing, making Elastic indispensable for AI-driven insights and decision-making.

Financially, Elastic demonstrates consistent double-digit revenue growth, primarily driven by subscriptions with impressive gross margins. While high stock-based compensation affects GAAP profitability, the company maintains positive cash flow, showcasing financial resilience.

Elastic trades at a premium valuation with a P/E ratio of 70, seemingly high in comparison to the market. However, this valuation might be substantiated by the company's remarkable growth rates, margin expansions, and promising prospects in the AI domain. Despite the seemingly steep valuation, Elastic's trajectory suggests a robust investment opportunity.

For further details see:

Elastic: A Solid Buy For The Age Of Data Despite Premium Valuation