ESTC - Elastic: Downgrading To Neutral On Valuation

2024-01-16 13:49:40 ET

Summary

- Elastic, an infrastructure software company, has rallied on the back of the generative AI boom.

- The company is making the case that search is integral to powering contextual generative AI applications.

- So far, we haven't seen a meaningful acceleration in Elastic's revenue, though the consensus is calling for one point of y/y acceleration in FY25.

- Given the recent sharp rally in Elastic stock, I'm recommending locking in profits here and waiting until the low $90s to buy back in.

The markets have soared over the past couple of months, but now is hardly the time to get complacent. I continue to hold firm to the view that 2024 will be a stock picker's market, and active investing and careful stock assessment will be the way to win this year as I expect major indices to trade sideways.

In particular, we should pay careful attention to recent winners, and Elastic N.V. ( ESTC ) is a big one. This infrastructure software company, known for its enterprise search applications, enjoyed late tailwinds from the Generative AI boom which has helped to juice its recent top-line results. Over the past twelve months, shares of Elastic have more than doubled; so far this year in January, it has even extended gains and risen ~5% while the S&P 500 has roughly flatlined.

Generative AI is a big opportunity, but also already embedded into Elastic's valuation now

I last wrote a bullish note on Elastic when the stock was trading in the mid-$70s in early November. At the time, I had called out the company's steady top-line trends, its consistent upward march in profit margins, and an attractive valuation as core reasons to be bullish on the company. With the stock now trading above $110, however, it's a great time to re-assess this call: and owing to Elastic's much richer valuation, I'm now pegging my rating on the stock at neutral.

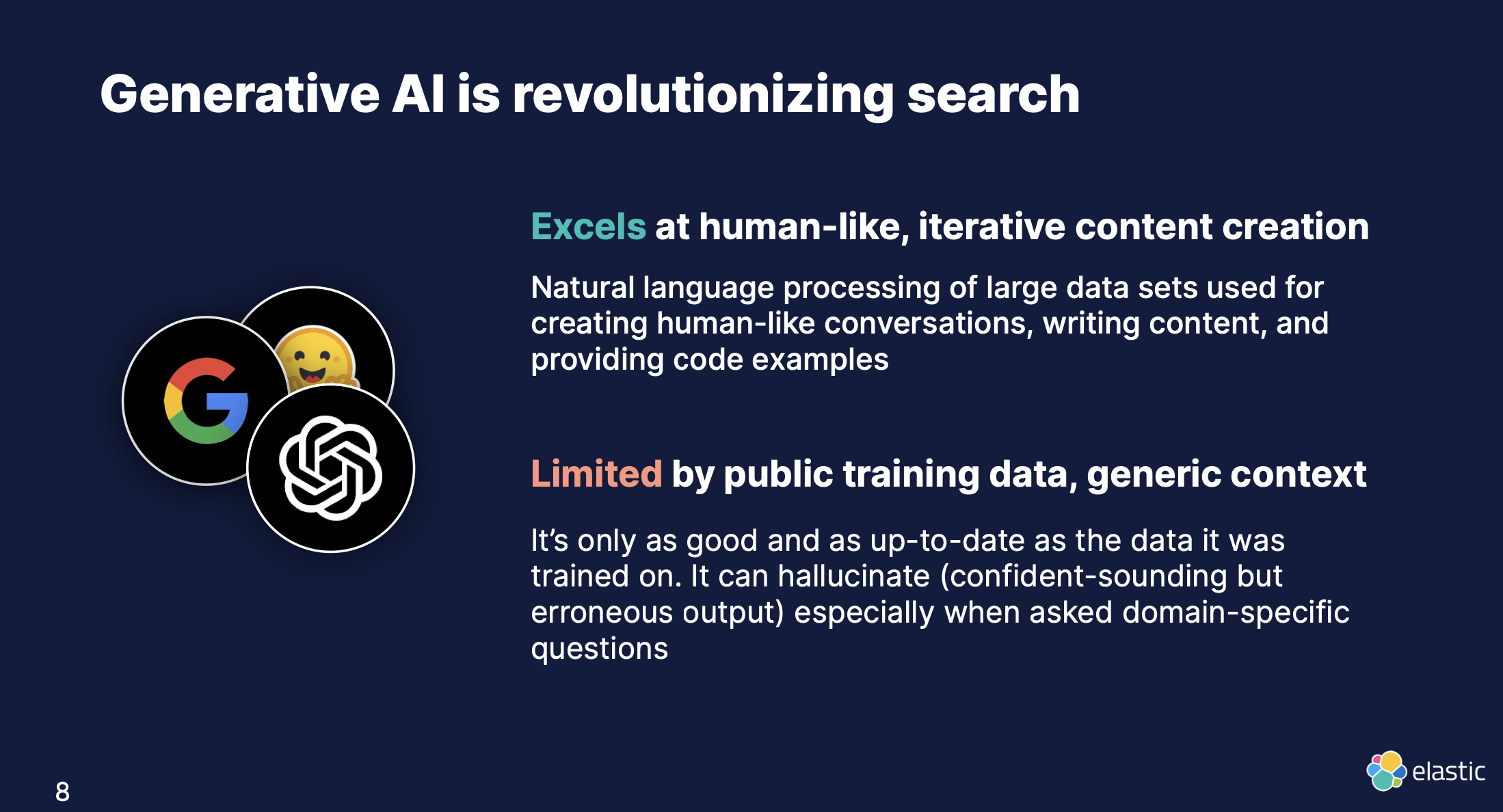

The recent optimism on Elastic is driven by generative AI - though the stock tailwinds happened much later than the first wave. The slide below, taken from Elastic's recent Q2 earnings deck, showcases how generative AI interacts with Elastic's core search functionality:

{kind=link}

Search, according to Elastic, helps to create new contextual generative AI applications. AI struggles in domain-specific queries, helping developers to narrow queries and integrate well into large language models. Customer interest in GenAI-related use cases for Elastic has picked up, which investors are hoping will generate a re-acceleration in growth.

Beyond generative AI, here's a refresher on some of my other core bull case drivers for Elastic:

- Many use cases supporting a large global TAM on one platform - Elastic's core platform supports a variety of use cases and one that has been adopted by major corporations. It estimates its global TAM at $78 billion, suggesting only ~1% current penetration. This TAM has grown significantly versus $45 billion at the time of Elastic's IPO in 2018.

- Purely recurring, high-margin software product - 90%+ of Elastic's revenue comes from subscriptions, meaning the company has very high revenue visibility. It has net revenue expansion rates of ~120%, meaning the majority of its customers upsell dramatically (versus ~110% net expansion rates for most other software companies). On top of that, Elastic's revenue comes in at a high-70s (%) gross margin. The math on this works out like a charm: as more and more Elastic customers renew and expand, Elastic can take advantage of its huge gross margin to scale profitably, given that renewal deals to existing customers cost far less in terms of sales dollars to achieve.

But the reality is: so much of this strength in GenAI opportunity, in my view, is already baked into Elastic's share price after the recent rally. At current share prices just north of $110, Elastic trades at a market cap of $11.15 billion. After we net off the $966.4 million of cash and $568.1 million of debt off Elastic's most recent balance sheet, the company's resulting enterprise value is $10.75 billion.

Meanwhile, for the upcoming fiscal year FY25 (the year for Elastic ending in April 2024), Wall Street analysts are pegging Elastic's revenue at $1.48 billion, or 18% y/y (already representing 1% of top-line acceleration versus current revenue trends, a nod to GenAI opportunity). This puts Elastic's valuation at 7.3x EV/FY25 revenue. It's not a crazy double-digit revenue multiple, but it's also not too far off from a more pure-play AI stock like C3.ai, with similar current growth rates but (arguably) much heavier and more direct future tailwinds from GenAI demand.

To me, there's not much room for Elastic to glide much higher this year, unless its revenue growth suddenly re-accelerates meaningfully above 20% y/y again. Given the sharp rally over the past few months, I'd prefer to lock in gains here and move to the sidelines.

Q2 download

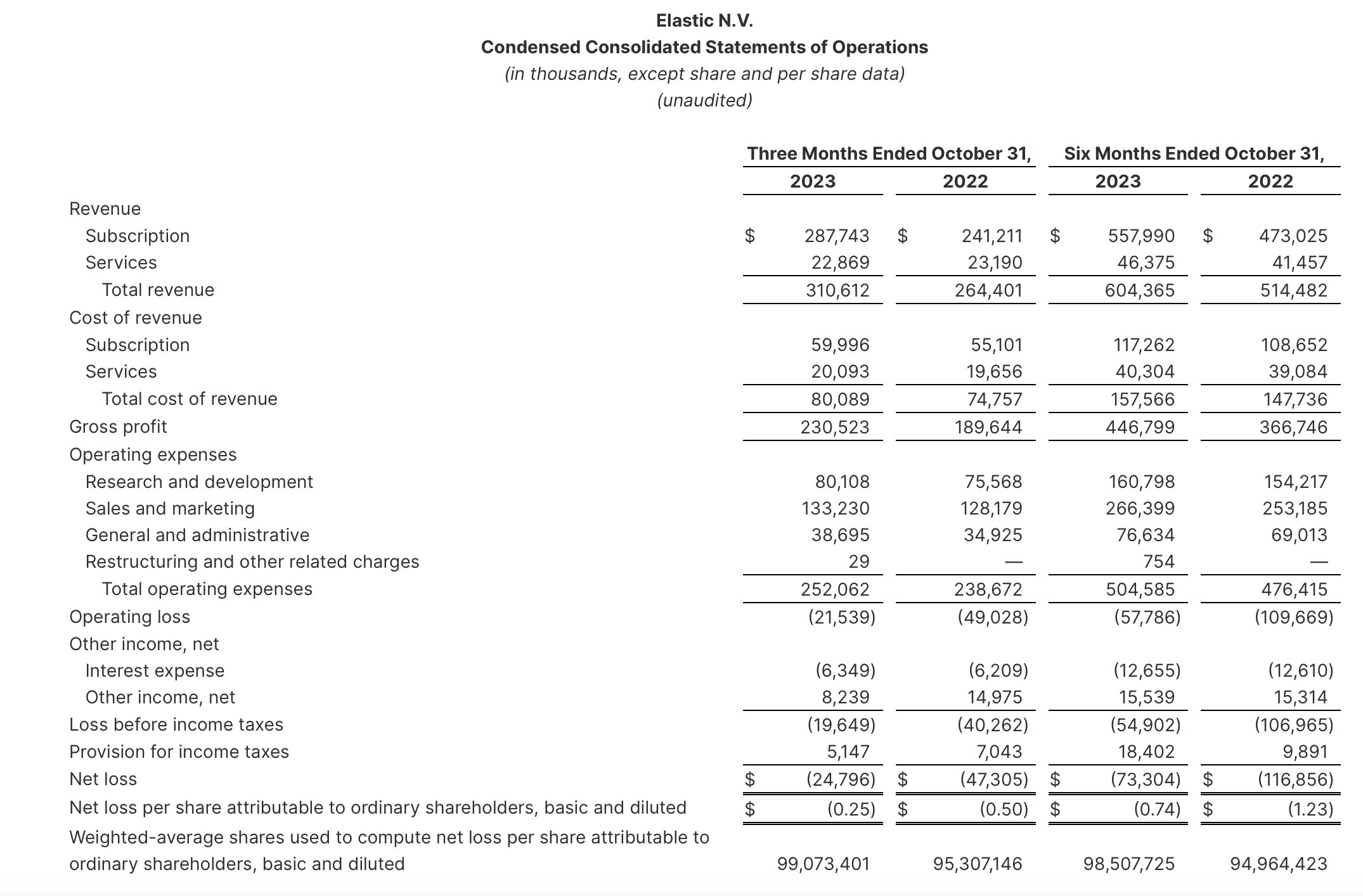

Let's now go through Elastic's most recent quarterly results in greater detail. The fiscal Q2 (October quarter) earnings summary is shown below:

{kind=link}

Revenue grew 17% y/y to $310.6 million, slightly ahead of Wall Street's expectations of $304.0 million (+15% y/y).

{kind=link}

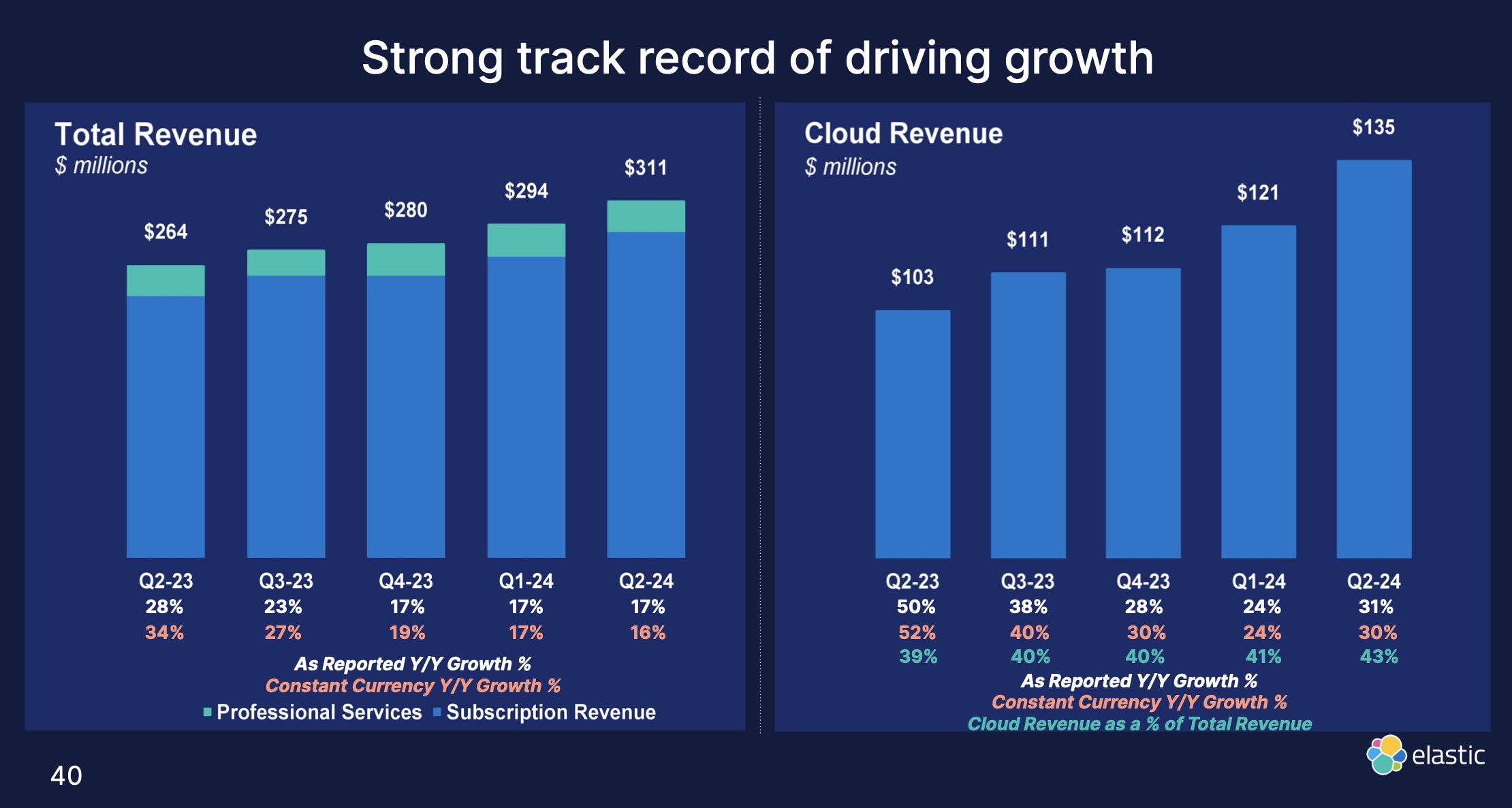

Note, as shown in the chart above, that on a constant currency basis revenue growth actually decelerated one point versus 17% y/y growth in Q1, which in turn decelerated from 19% and 27% growth in the quarters prior. So in actuality, even though management has nodded to more customer interest in Generative AI, these deals have not yet moved the needle from a top-line perspective. We do note, however, that Elastic's transition to Elastic Cloud continues, and cloud revenue growth did accelerate to 30% y/y on a constant-currency basis, as cloud revenue share increased 4 points y/y to 43% of overall revenue.

Here is some helpful commentary from CEO Ash Kulkarni's remarks on the Q2 earnings call , detailing sales momentum and the impact of Generative AI on the company's deal flow:

Generative AI is driving a resurgence of interest in search as customers use semantic search, vector search and hybrid search to ground large language models with their private business context and ESRE provides the most comprehensive and enterprise-ready platform for these use cases. While it will take some time for generative AI spend to become a significant driver of our revenue, we are very excited about the long-term opportunity [...]

In Q2, we saw a significant increase in the use of ESRE. ESRE includes a built-in vector database, the ability to bring in your own machine learning models and also ELSER, which is our own proprietary machine learning model for semantic search. This quarter, we saw a rapid adoption of ELSER, which we first released with ESRE launch.

With ELSER, customers are able to quickly implement semantic search without any model training to power generative AI use cases. With the release of the even more efficient ELSER Model 2 earlier this month, we expect to see this momentum continue."

The company also reported a 110% net revenue retention rate, indicating the average customer is upgrading its usage of Elastic by 10%. On a geographic basis, the company notes strong momentum in EMEA, while many customers as well are showcasing interest in consolidating under one Elastic platform to serve a multitude of different use cases.

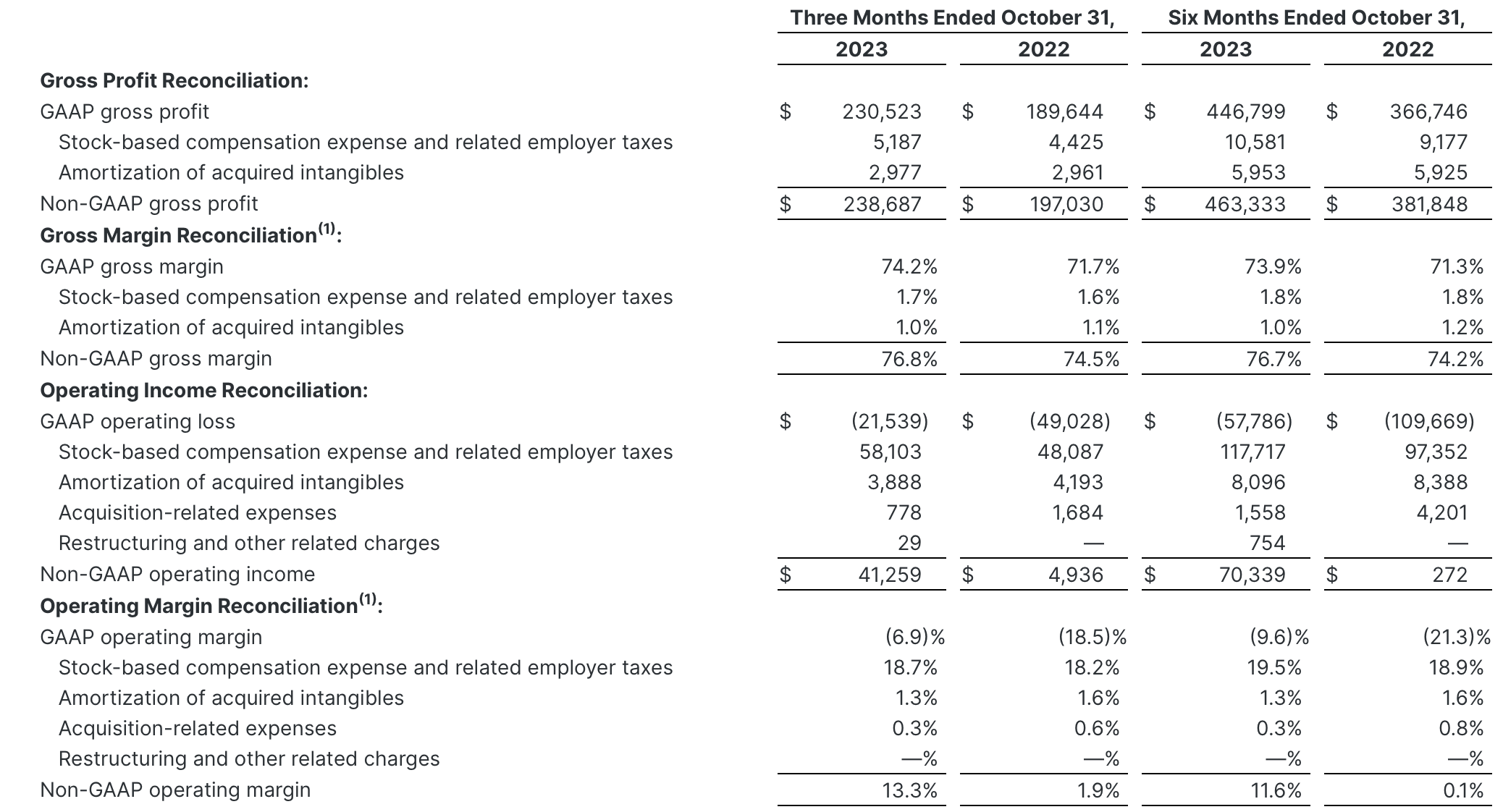

From a profitability standpoint, Elastic continued to show an impressive y/y expansion in pro forma operating margins, up to 13.3% - 11 points better than the prior year.

{kind=link}

The company continues to expect margin expansion in FY25, noting that it expects revenue growth will outstrip opex investment growth.

Key takeaways

There is no doubt that Elastic continues to execute well amid a groundswell of additional interest in Generative AI, but I do believe that investors will have a chance to re-invest in this stock at a better price. I'd be willing to dive back into this name if Elastic came down to 6x EV/FY25 revenue, representing a $93 price target and ~16% downside from current levels.

For further details see:

Elastic: Downgrading To Neutral On Valuation