ESTC - Elastic: Rating Upgrade As I Believe Valuation Will Catch Up To Peers' Level

2023-09-03 09:05:23 ET

Summary

- I upgrade my rating to buy for Elastic stock as I expect valuation to catch up to peers' levels.

- Elastic reported strong 1Q24 earnings with a 17% YoY revenue increase and 10% EBIT margin.

- Generative AI and consolidation trend are expected to drive growth for Elastic in the future.

Overview

My recommendation for Elastic (ESTC) is a buy rating, as I expect valuation to catch up to peers’ levels. I believe the current discount that ESTC is trading at is not justified as the growth profiles between ESTC and peers are similar. I am positive that growth can continue at this momentum as ESTC continues to invest in its generative AI offering and also reap the benefits of the consolidation trend. Note that I previously gave a hold rating to ESTC as I saw the upside to the current share price as unattractive, but I have changed my view after the 1Q24 earnings.

Business

ESTC specializes in IT and data analysis services, providing a range of offerings such as surveillance, security analysis, enterprise search, cloud computing, and open-source application performance monitoring solutions. The business has 1 key reporting segment: IT services with a breakdown of Subscription and Professional Services, representing 92% and 8% of revenue respectively.

Recent results & updates

In 1Q24 , total revenue experienced a 17% year-over-year increase in constant currency, surpassing the management's projected growth of 14% by 300 basis points. As a result of this revenue growth and effective expense management, pro-forma [PF] EBIT margin reached 10%, which was 400 basis points higher than the guidance provided. This combination of better-than-expected revenue and margin performance resulted in an EPS beat, with PF EPS reaching $0.25. Overall, ESTC has reported a strong start to the year.

Diving deeper, the robust revenue performance was driven by both the self-managed subscription segment and Cloud. To provide context, subscription revenue grew by 16%, with self-managed subscription revenue showing a year-over-year growth of 11%, marking a 1 percentage point acceleration compared to the previous quarter. While some investors might be disappointed by the deceleration in cloud revenue growth to 24% for the current quarter, it's important to note that ESTC achieved a 24% growth rate on top of the impressive 30% growth seen in the previous quarter. This indicates a consistent growth trajectory, and there is an expectation that this level of growth will continue, as management specifically mentioned an improvement in cloud consumption patterns in the first quarter of 2024. Moreover, management also observed signs of stabilization in the consumption optimization trend and the overall macroeconomic climate.

“And although we saw some positive signs of customers ramping here in Q1, it's conceivable that consumption may fluctuate in the near term. So we just think it's best to consider that possibility in our guidance.” from: 1Q2024 earnings call

In my opinion, generative AI is going to be a major factor in the growth of the ESTC business. This was also the primary focus of the earnings call (1Q24 transcript search results for AI-related keywords reveal 19 occurrences). Management claims that they are experiencing a surge in interest in and use of vector databases and generative AI. In particular, they stressed that the C-suite is actively involved in discussions about generative AI and that its use is widespread. Seeing heavy participation from the C-Suite in these discussions gives me confidence that the ESTC product is gaining traction. Nonetheless, I gathered from management's comments that the general tone of customer conversations in August has been similar to 1Q24, suggesting that underlying customers may still be wary of investing today. However, I see the initial achievements as quite encouraging, particularly because management has disclosed that there are hundreds of paying customers leveraging ESRE for vector search functionalities. This figure encompasses both new and current clients and is on the rise. Furthermore, the company is stepping up its commitment to Gen-AI by allocating more resources to research and development as well as marketing efforts.

Outside of AI, I think the organic growth story of ESTC is still solid, as management has noted that businesses are consolidating workloads in favor of ESTC as they become more cost-conscious. That means two things:

- ESTC is the vendor of choice for the underlying companies, which speaks well of ESTC's value proposition across other solutions that customers are using.

- ESTC ARPU could go higher as the consolidation trend continues.

Valuation and risk

Author's valuation model

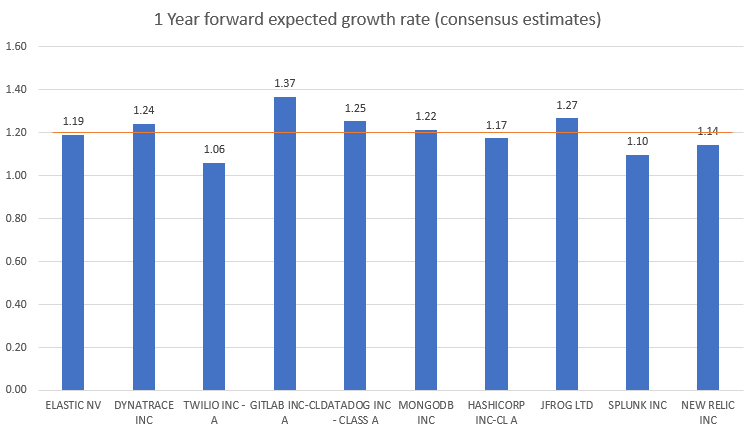

According to my model, ESTC is valued at $98.40 in FY24, representing a 40% increase. This target price has increased from my previous model as I expect FY24 to grow slightly faster, reflecting the FY24 guidance, and also multiples to trade up to 5.5x forward revenue. The average forward revenue that peers are trading at today is 5.5x forward revenue, which is at a premium to ESTC today. I believe the discount is not justified as ESTC has historically traded at a 1x ratio. Moreover, the growth profiles of ESTC and peers are roughly similar today.

Bloomberg

{kind=link}

I reiterate my thoughts on ESTC risk that as one of the key players in the search industry, ESTC has established a dominant position due to the limited presence of strong competitors. If ESTC were to decide to update their technology and add Elastic-like features, however, they would be up against stiff competition from the likes of Microsoft (with their FAST search), Oracle (with their Endeca), and Micro Focus (with their Autonomy). By bundling them with other customer engagement solutions, these mega-vendors can afford to offer steep discounts or even give these tools away for free.

Summary

I upgrade my rating to a Buy for ESTC due to my belief that its valuation will eventually align with industry peers. The current trading discount does not seem justified, considering the similar growth trajectories between ESTC and its competitors. The recent 1Q24 earnings report revealed a strong start to the year, with a 17% year-over-year revenue increase, surpassing guidance by 300 basis points, resulting in a 10% EBIT margin. Notably, both self-managed subscriptions and Cloud revenue contributed to this growth. As for risk, my view remains the same where ESTC would always be under the threat of larger players bundling products to offer similar services/solutions at a cheaper rate. For instance, Microsoft ( MSFT ) with its FAST search.

For further details see:

Elastic: Rating Upgrade As I Believe Valuation Will Catch Up To Peers' Level