ESTC - Elastic's Bullish Turn: Anticipate 65% YoY Profitability Surge In 2025

2024-01-12 05:09:49 ET

Summary

- Elastic's significant strides in profitability improvement, with an estimated 65% year-over-year increase to approximately $230 million in fiscal 2025, form a compelling basis for a bullish outlook.

- Despite facing challenges like slowing revenue growth rates, ESTC's innovative adeptness in optimizing deployments for existing customers positions it well.

- While the stock's multiple has compressed over time, the low expectations embedded in the share price create an opportunity for upward movement.

Investment Thesis

Elastic ( ESTC ) specializes in search analytics, offering a platform that allows businesses to swiftly search and analyze extensive datasets in real time.

The stock had gone largely nowhere for a prologue period post-pandemic. But of late, on the back of its strong improvements in profitability, the stock is now once more attractive.

According to my estimates, in fiscal 2025 (starting in May 2024) Elastic's underlying profitability will meaningfully increase by approximately 65% y/y to around $230 million.

This leaves this stock priced at approximately 48x forward non-GAAP operating margins, which for a SaaS business is an attractive buy.

Rapid Recap

In my previous analysis, back in September , I said:

I find it challenging to feel bullish about the company, especially considering its current valuation, which is valued at +60x this year's EPS.

Further, the company's revenue growth rates are now below 20% CAGR, and its recent success seems to stem partially from cannibalizing its legacy on-premise offering rather than substantial organic growth.

Author's work on ESTC

In hindsight, this was categorically the wrong call to make. I hadn't expected Elastic to make so much progress on its underlying profitability. Therefore, I now revise my rating to a bullish call.

Elastic's Near-Term Prospects

Elastic is a tech company that provides a search analytics platform. Essentially, they help businesses quickly find valuable information from vast amounts of data in real-time. Whether it's searching a website, identifying security threats, or powering generative AI applications, Elastic's platform is designed to make data exploration and analysis efficient and effective. Their solutions, like Elasticsearch Relevance Engine and Elastic Cloud, enable users to manage and search through data seamlessly, making Elastic a go-to choice for companies looking to seeking to mine data for various purposes.

Elastic's near-term prospects appear promising. The company showcased robust growth in Elastic Cloud, up 31% y/y as of its latest fiscal Q2 2024 results.

Notably, Elastic's focus on generative AI applications, leveraging technologies like Elasticsearch Relevance Engine ("ESRE"), has garnered significant attention from customers.

The recent multiyear marketplace deal with DocuSign ( DOCU ) and the adoption of Elastic's capabilities by a leading video-sharing platform underscore the growing demand for Elastic's search analytics platform. The company's emphasis on consolidating customers onto the Elastic platform for various use cases, such as observability and security, resulted in key wins and demonstrated its ability to replace incumbent solutions.

Additionally, Elastic's innovative product developments, like the Elasticsearch Query Language (ES|QL) and advancements in generative AI, position it favorably to capitalize on emerging market trends. Furthermore, strategic collaborations with major cloud hyperscalers, such as Amazon Web Services and Google Cloud, underscore Elastic's commitment to expanding its global reach, providing a solid foundation for future growth.

However, Elastic also faces challenges. While the company has demonstrated strong growth, there's a need to monitor and adapt to evolving geopolitical environments. Elastic acknowledges the continued importance of cost-consciousness and spend management among customers, indicating a landscape where organizations are careful with their budgets.

Though the company has succeeded in optimizing Elastic deployments for existing customers, sustaining and expanding these optimization efforts will be crucial as the market evolves.

Additionally, Elastic's entrance into the serverless offerings arena, marked by the acquisition of Opster, introduces the challenge of seamlessly integrating and leveraging Opster's monitoring and troubleshooting capabilities to enhance Elastic's platform resilience.

Furthermore, as Elastic places a strategic focus on generative AI, it acknowledges that its revenue from that segment will take time to grow. The company must navigate this transitional period and effectively communicate the value proposition of generative AI to its customer base.

With this background in mind, let's discuss its financials.

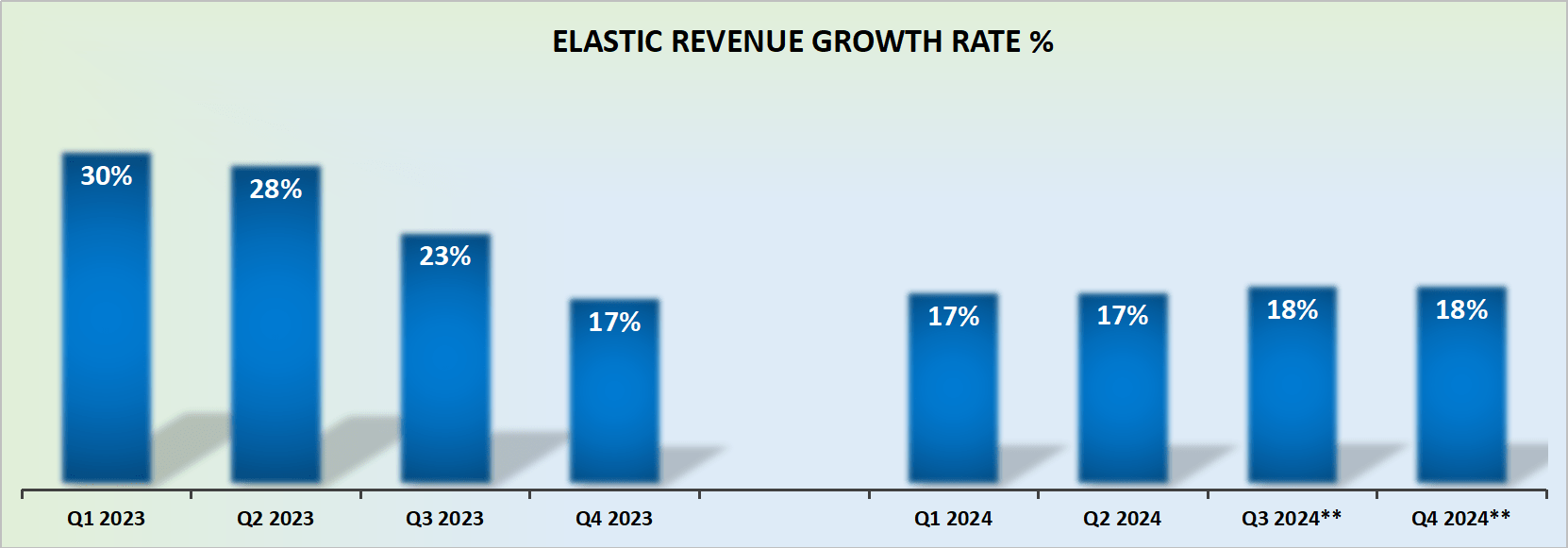

Revenue Growth Rates Are Now Sub-20% CAGR

{kind=link}

Allow me to get to one aspect that significantly overhangs Elastic. The business' growth rates are now slowing down. Surely, growing at just under 20% isn't all that slow, now is it? Well, here's the problem, Elastic has a market cap of about $11 billion. It's considered a mid-cap from a tech investors' perspective.

And what this further implies, is that for a tech investor, the stock is either a rapidly growing entity or it's starting to mature. Tech investors are extremely picky, given that the industry has a long history of rapid disruption.

Consequently, tech businesses that start to be considered sub-20% growers are often viewed as not being able to deliver "premium growth". Premium growth generally means companies that can be expected to consistently deliver +20% CAGR. And when that is an underlying expectation their multiple starts to rapidly compress. Unless the business can find another way to attract investors to the stock. And that's what we discuss next.

ESTC Stock Valuation -- 48x Forward Non-GAAP Operating Profits

For the most part, Elastic has seen the multiple on its stock compress with time. This echoes my assertion above, that the business is no longer viewed as a premium growth company.

However, given that its expectations become so muted, any good news coming from the company, together with the low expectations embedded in the share price, and the stock was primed to move higher.

More specifically, what's happened here is that previously, Elastic guided for its operating margin for fiscal Q2 2024 to be 10% at the high end. But when the results for fiscal Q2 2024 were actually reported, Elastic's non-GAAP operating margin reached 13%.

Consequently, investors are hoping that management is simply being prudent with its profitability guidance and that in fact, the business has now reached a point where getting close to 13% non-GAAP operating margins can be expected on a sustainable basis.

And then, where the real bull case starts to be reflected is in the possibility that as Elastic's growth rates mature, this business could in fiscal 2025 (starting in May 2024), be counted on to deliver around 15% non-GAAP operating margins.

As a reference point, if we assume that next year Elastic's growth rates for the most part match the growth rates from fiscal 2024, this would see its revenues growing by 18% y/y to approximately $1.5 billion.

And then, if we presume that Elastic can deliver a 15% non-GAAP operating margin, this would imply that in fiscal 2025 its non-GAAP operating profits could reach approximately $230 million.

This would compare with the approximate $140 million expected in fiscal 2024. More specifically, investors are hoping that in fiscal 2025, its underlying profitability could increase by close to 65% y/y.

Given this potential, this would go a long way to support its stock, leaving the stock priced at 48x forward non-GAAP operating profits, with the expectation that the company is now at a point in time where it can start to ooze with profitability.

The Bottom Line

My earlier skepticism about Elastic's prospects has proven to be misguided, as the company has demonstrated substantial improvements in profitability. The shift to a bullish outlook is supported by the anticipation of a meaningful increase in underlying profitability, approximately 65% year-over-year, reaching around $230 million in fiscal 2025.

Despite challenges such as slowing revenue growth rates and the need to navigate a transitional period in generative AI, Elastic's innovative product developments and resilience in optimizing deployments for existing customers position it favorably.

While the stock's multiple has compressed over time, the low expectations embedded in the share price create an opportunity for upward movement, especially if Elastic can consistently deliver on its non-GAAP operating margin targets.

In sum, there's a lot to like in this stock.

For further details see:

Elastic's Bullish Turn: Anticipate 65% YoY Profitability Surge In 2025