EGO - Eldorado Gold: Too Far Too Fast

Summary

- Eldorado Gold suffered one of the largest drawdowns among its peers over the past two years, sliding 65% from its Q3 2020 highs.

- The weakness in the stock can be attributed to inflationary pressures which severely impacted its margins and declining output with difficult comps relative to a huge year in 2020.

- Fortunately, Eldorado is in a much better position today, with Skouries green-lighted and the company lapping much easier comps after failing to meet production guidance in 2022.

- However, while a better 2023, a strong gold price and the Skouries financing package are positive developments, the stock is quite extended short-term, suggesting an elevated to risk to paying up for EGO here.

2022 was a challenging year for the Gold Miners Index ( GDX ), evidenced by several names missing production estimates and many having to revise cost guidance upwards due to inflationary pressures exacerbated by labor tightness in prolific regions. Although there were exceptions to the rule, like Lundin Gold ( LUGDF ) and Orla Mining ( ORLA ), Eldorado Gold ( EGO ) was not an exception, revising cost guidance well above its initial outlook ($1,180/oz to $1,280/oz vs. $1,075/oz to $1,175/oz) and missing the bottom end of its FY2022 production guidance of 460,000 to 490,000 ounces. The result was a ~14% decline in production on a two-year basis and a steep decline in margins, with costs likely to come in above $1,215/oz ( FY2020: $921/oz ).

Fortunately, while the headline results might have been less pretty than investors hoped, Eldorado saw meaningful progress across its portfolio. This included successfully financing and green-lighting its high-margin Skouries Project (Greece), exploration success at its Lamaque Mine (Canada), and continued optimization at Kisladag (Turkiye) with higher-capacity conveyors installed and the addition of an HPGR circuit. Just as importantly, it's now lapped its difficult comps. So, with a combination of higher output and a higher gold price, Eldorado should enjoy higher revenue and margins year-over-year as it benefits from easy comps after a tough 2022.

The issue? Much of this positive outlook appears to be reflected in the share price, and the stock has gotten ahead of itself short term. So, while the stock was in a low-risk and buyable position under US$5.60 six months ago, chasing the stock here offers a much less attractive risk/reward setup. In fact, paying up here above US$9.65 is a recipe for potentially being caught in a double-digit drawdown. Let's take a closer look below:

EGO Bullish Rating - July 2022 (Seeking Alpha Premium/Pro)

{kind=link}

Q4 Results

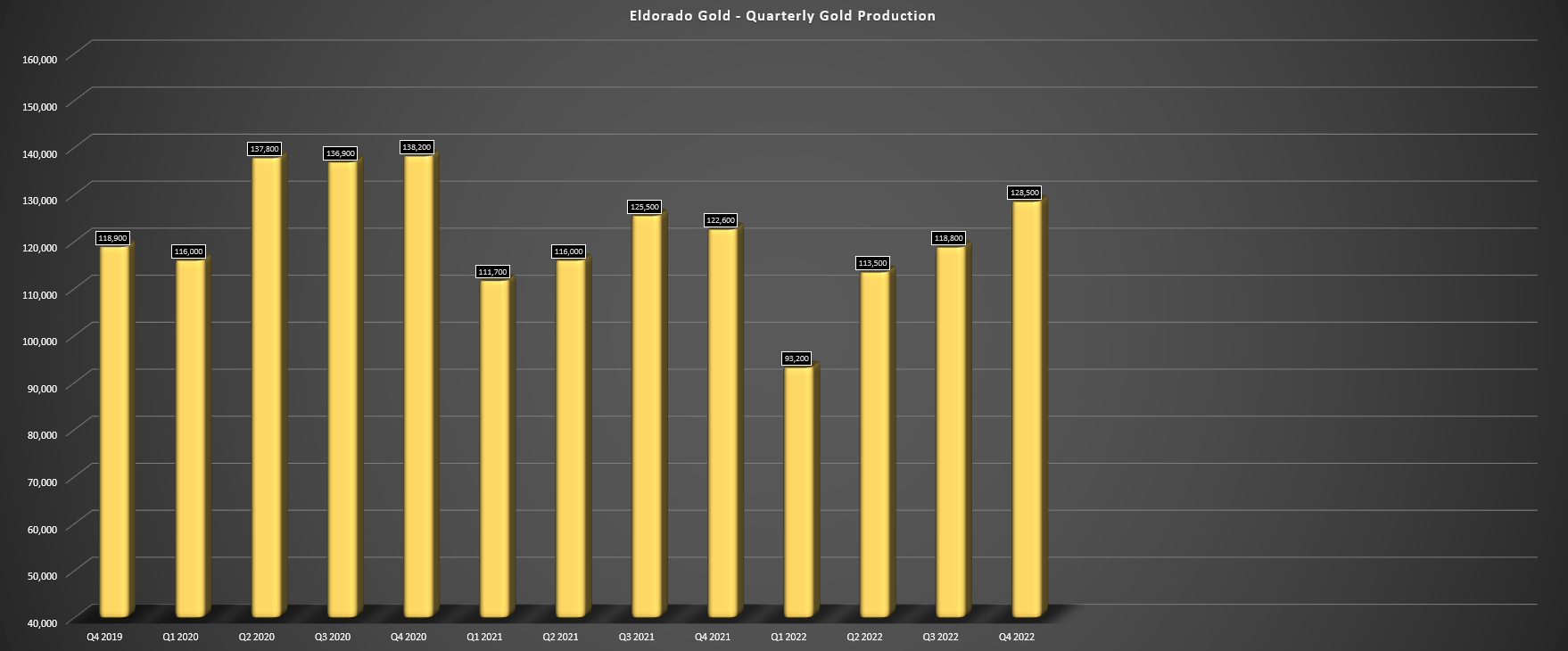

Eldorado Gold released its Q4 results last week, reporting quarterly production of ~128,500 ounces and annual production of ~453,900 ounces. This translated to a nearly 5% increase on a year-over-year basis but a 5% decline on a full-year basis and a nearly 15% decline vs. FY2020 production levels. This was related to a tough start to the year with COVID-19 absenteeism, severe weather in Turkiye and Greece, and a government-mandated power outage that impacted Kisladag. Unfortunately, this slow start to the year couldn't be made up despite a monster quarter in Q4 from the company's Lamaque Mine, and Eldorado came in below the bottom end of FY2022 guidance and saw a more than 4% miss vs. its guidance mid-point (475,000 ounces).

Eldorado Gold - Quarterly Production (Company Filings, Author's Chart)

{kind=link}

Looking at the chart of quarterly production below, the sharp decline vs. 2020 levels might not inspire much confidence, with Eldorado seeing significantly lower production on a two-year basis. However, it's important to note that the company has seen a steady decline in grades at what was previously its most significant contributor, Kisladag, with grades declining from roughly 1.0 grams per tonne of gold in FY2020 to ~0.75 grams per tonne in FY2022. Meanwhile, Olympias has seen a decline in throughput on a two-year basis, and although Lamaque enjoyed record annual production in FY2022 on the back of higher throughput, grades were lower here as well.

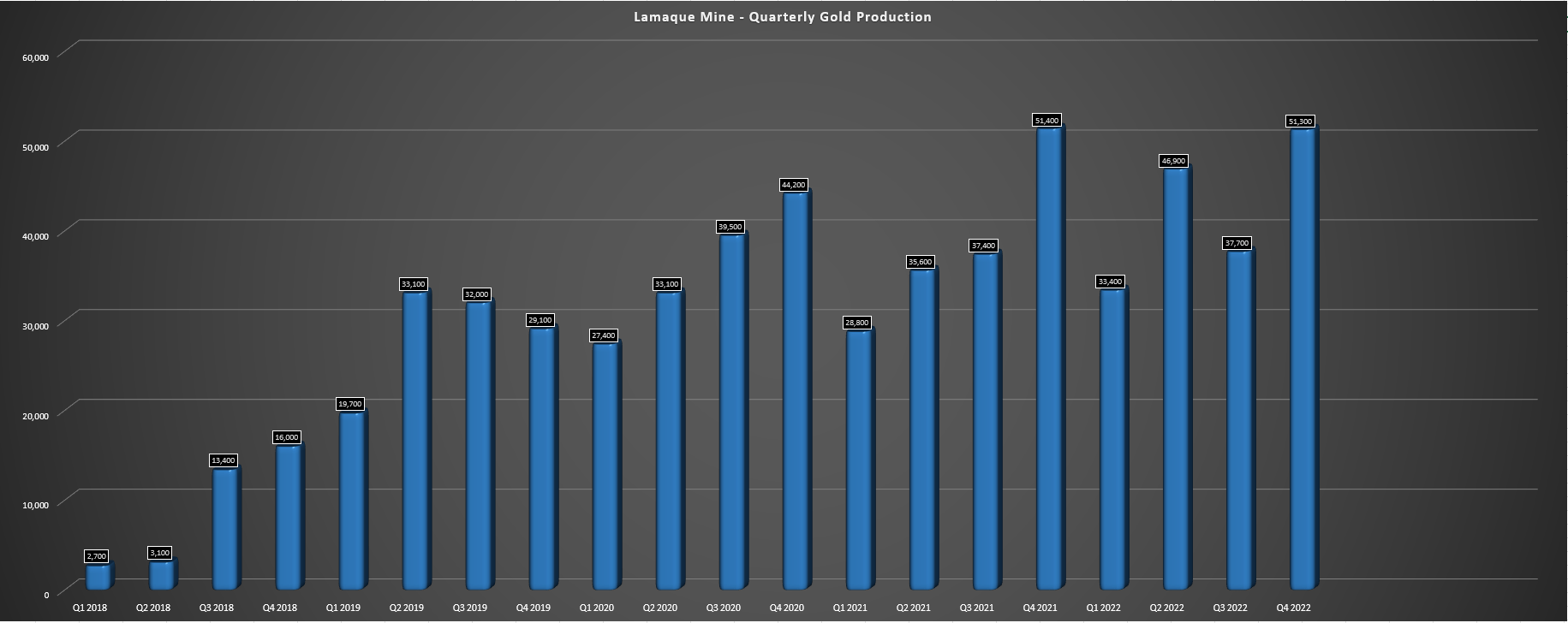

Lamaque - Quarterly Production (Company Filings, Author's Chart)

{kind=link}

While it's easy to be negative on Eldorado if one solely looks at the declining production profile vs. 2020 levels, it's important to note that 2020 was an exceptional year from a grade standpoint, and the company has done a decent job of maintaining production levels given the headwind of lower grades at its two largest assets. Plus, while Kisladag may not see a return to 1.10+ gram per tonne gold grades any time soon as it enjoyed in FY2019 (current reserve grade: 0.68 grams per tonne of gold), Lamaque has a very bright future ahead of it, especially if Ormaque ounces that are much higher grade are moved into the mine plan.

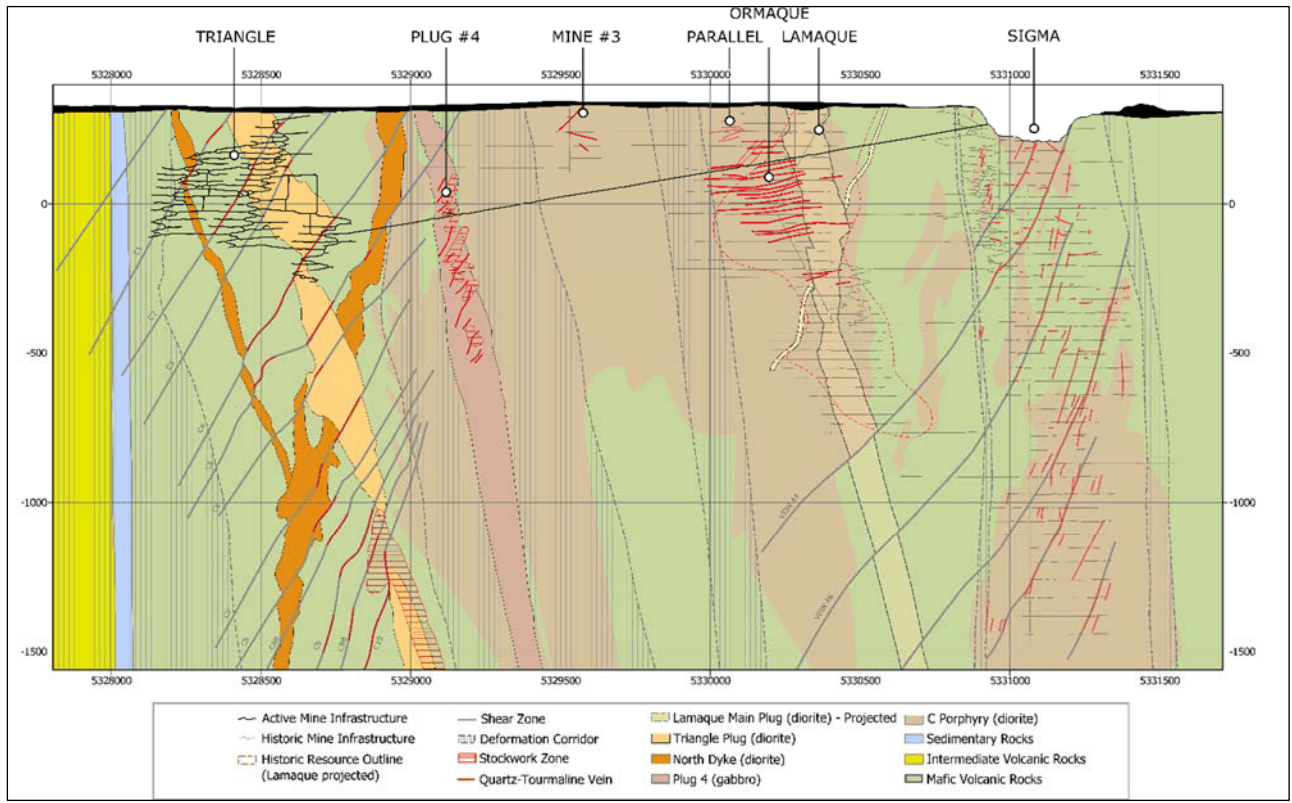

Lamaque Mine & Near-Mine Opportunities (Company Report)

{kind=link}

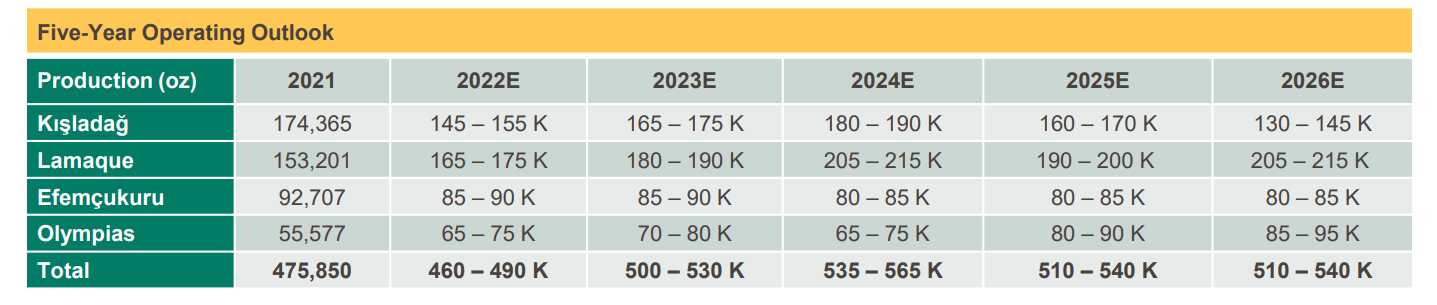

For those unfamiliar, Ormaque is a satellite deposit (1.5 kilometers south of the Sigma Mill and 200 meters east of the new decline) with grades that are well above the reserve grade at 11.0+ grams per tonne of gold. This compares very favorably to Lamaque's current reserve grade of ~6.6 grams per tonne of gold. Both Ormaque and Lower Triangle offer opportunities to significantly extend the mine life at the Quebec asset. So, while 2022 was a record year for Lamaque, with ~174,100 ounces produced, investors can look forward to steady growth in output at this asset based on the guidance of 185,000 ounces in FY2023, 210,000 ounces in 2024, and 195,000 ounces in 2025 (assuming production comes in at the guidance mid-point).

Finally, although Olympias has barely contributed and is by far Eldorado's smallest asset, the company continues to work toward boosting productivity and hopes to increase throughput to 650,000 tonnes per annum, a more than 50% increase vs. FY2022 levels (~400,000 tonnes milled). So, while the polymetallic asset may have a cost profile that leaves a lot to be desired currently (all-in sustaining costs above $2,000/oz), it's worth noting that the mine would benefit significantly from economies of scale in the case of a throughput expansion and its results were impacted by a 13% VAT import charge on gold concentrate into China which was the result of sanctions imposed on Russia that unfortunately diverted planned shipments due to the Russia-Ukraine war.

To summarize, while the FY2022 headline results in the upcoming Q4 report next month may not be easy on the eyes, with AISC likely to come in near $1,220/oz, up 32% from FY2020 levels, there is reason to be optimistic about this story medium-term and long-term. This is because two of its key assets will benefit from economies of scale (Lamaque, Olympias); Kisladag should have a better year with complete optimization work and less impact from fewer tonnes stacked (assuming the weather is cooperative). And most importantly, Eldorado has now green-lighted a transformative asset, its Skouries Project in Greece, which is already ~40% constructed and is expected to have negative AISC on a by-product basis.

Recent Developments & 2023 Outlook

Regarding recent developments, the major development for Eldorado was the €680 million Skouries Project financing and Board approval of the massive project, with an estimated capex bill of ~$845 million. Given that this study was completed more than a year ago, I would not be surprised to see costs come in closer to $900 million, but this is not an issue for Eldorado, which will have a term facility with a €480 million commercial loan, €100 million in funding from the Greek RRF, and a €100 million bridge loan with a blended interest rate near 5% with a 3-year availability and a 7-year repayment.

In addition to Eldorado's available liquidity ($500+ million) and a contingent overrun facility for 10% of capital costs, this gives Eldorado the flexibility to fund the project independently without share dilution, which provides clarity on two critical items regarding going ahead with a project of this size. While the ability to fund this without share dilution will benefit Eldorado's per-share metrics meaningfully, the choice to go it alone will result in meaningful margin expansion and production growth, especially when we compare Skouries estimated negative AISC with Eldorado's $1,100/oz to $1,175/oz cost profile going forward (ex-Skouries). Finally, Eldorado will see a meaningful lift in production, with Skouries expected to be a ~140,000-ounce per annum gold operation (~300,000 gold-equivalent ounces).

The other good news which I discussed previously is that 2022 appears to be a trough for production, and while some producers are up against difficult comps in 2023 after massive years (Lundin, Orla), Eldorado is lapping easy comps. This means it should have no issue posting increases across the board for total production, revenue, and margins, with costs set to benefit from slightly lower oil prices and a much higher denominator. If we combine this with what should be a higher gold price vs. an ~$1,800/oz average price in FY2022, Eldorado should also see meaningful margin expansion. Plus, on a long-term basis, Eldorado has a path to becoming one of the lower-cost producers sector-wide, given that it's bringing a phenomenal asset online by 2026.

Eldorado - 5-Year Outlook (Company Presentation)

{kind=link}

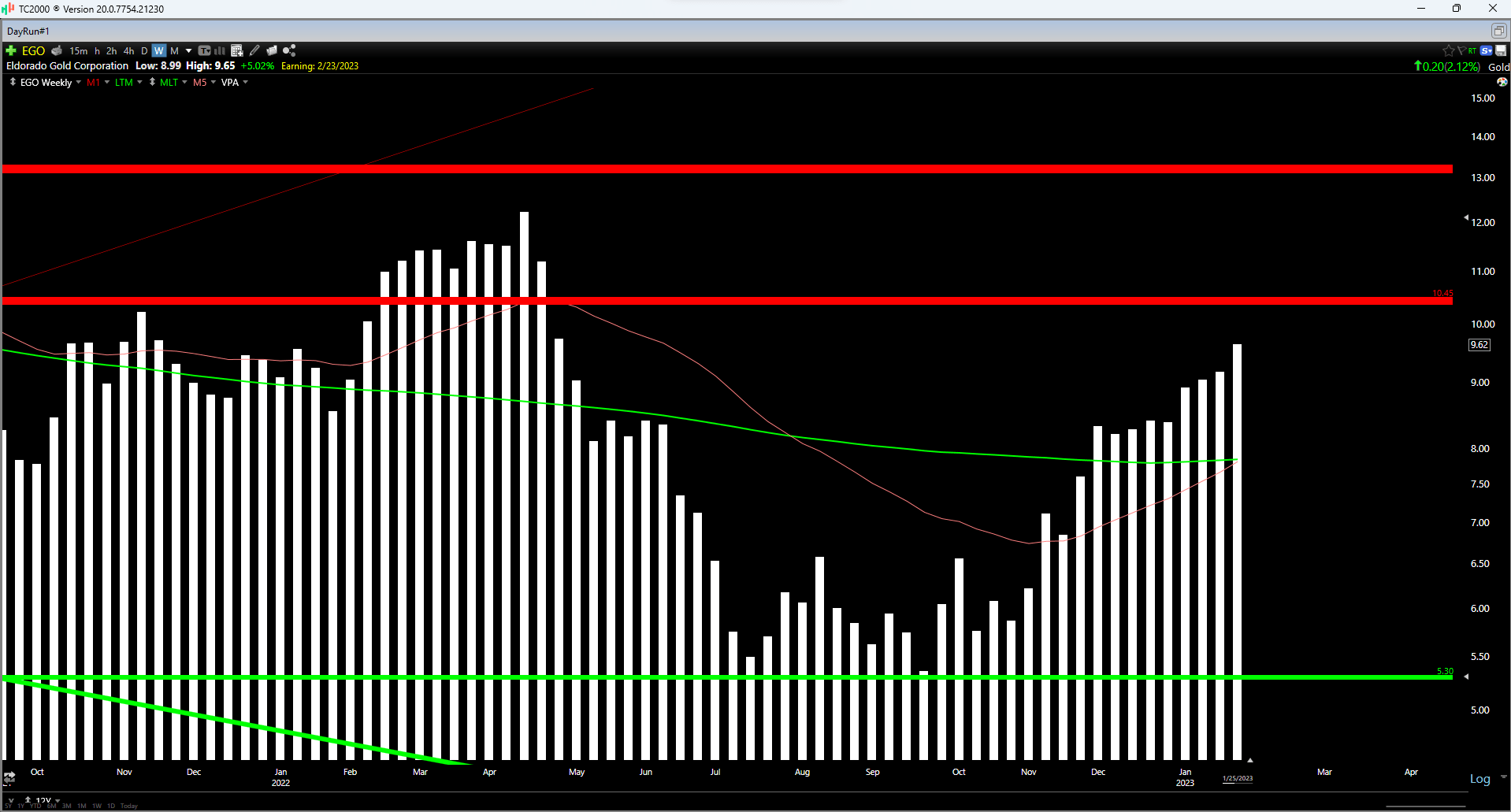

Some investors might argue that this should translate to a premium multiple for the stock, and assuming Skouries can deliver on its estimated production and cost profile, I would not be surprised to see Eldorado command a higher P/NAV and cash flow multiple post-2025 once the asset is in commercial production. However, with at least two years of construction ahead and commercial production not likely until Q4 2025 earliest, it's hard to argue for the stock re-rating this second, and I would argue that a portion of this re-rating has already occurred with the stock now up 90% off its lows in just 85 trading days. Let's take a closer look at the valuation below:

Valuation & Technical Picture

Based on ~189 million fully-diluted shares at year-end 2023 and a share price of US$9.60, EGO trades at a market cap of $1.81 billion and an enterprise value of $2.07 billion. This compares favorably to an estimated net asset value of $2.40 billion (Olympias and Skouries are valued at an 8% discount rate vs. other assets at a 5% discount rate), with Eldorado trading at ~0.74x P/NAV despite conservative metals prices below spot levels and a higher discount rate for two assets in a less proven mining jurisdiction. Using what I believe to be a fair multiple today of 0.90x P/NAV (Eldorado is not yet a low-cost producer, with Skouries being a few years away), I see a fair value for the company of ~$2.11 billion [US$11.16].

Although this points to a 16% upside from current levels, as I have discussed before, I prefer only to start new positions if I am investing at a significant discount to fair value to bake in a large margin of safety. In the case of small-cap cyclical stocks, I require a minimum 40% discount to fair value. This ensures that I have a meaningful enough upside case to my base assumption of where the stock can trade to adjust for the risk of owning a higher-beta and riskier producer vs. more diversified large-cap names like Agnico Eagle ( AEM ). If we apply this discount to Eldorado, the stock would need to decline below US$6.75 to become interesting from a valuation standpoint.

{kind=link}

Obviously, there is no guarantee that the stock will decline to these levels, and unless the gold price falls out of bed, I would be surprised to see a pullback of this magnitude. However, this rigid buying criteria suggests that this is nowhere near a low-risk buy zone for EGO (14% discount to fair value), which is corroborated by the technical picture above. As we can see, EGO is now heading toward a significant resistance level at US$10.45. Worse, it has no strong support until US$5.30 - US$5.60, given that it has not paused to build a new meaningful support level during a near-parabolic ~90% rally. In summary, I believe patience is the best course of action here, and if I were long the stock, I would be taking more profits into strength above US$9.60.

Summary

Eldorado Gold is in the best position it's been in for years, with a cornerstone asset in a Tier-1 jurisdiction enjoying exploration success and a top-10 gold mine from a cost standpoint in the wings and ready to resume construction after a multi-year pause. However, while the investment thesis has undoubtedly improved, the key to outperforming in this sector is buying stocks when they're hated, not chasing them when they're loved and they've already up 90% off their lows. So, while it might be tempting to pay up for Eldorado here and jump on what looks to be a runaway train, I see the reward/risk proposition as extremely unattractive at current levels. Hence, I see the better course of action as being patient for a sharp pullback, and I see this rally as an opportunity to book more profits.

For further details see:

Eldorado Gold: Too Far Too Fast