IVSBF - Electrolux: Unlocking Potential Amidst The Midea Rumors - Is It Time To Invest?

2023-06-05 18:56:57 ET

Summary

- Electrolux has faced challenges such as squeezed margins and decreased sales volumes but has initiated cost reduction and turnaround programs to improve performance.

- The projected growth possibilities indicate a medium-risk, low-reward scenario, and competition may restrict expansion opportunities.

- Investor AB, the company's largest owner, is likely not willing to sell its stake in Electrolux at this stage, and the rumors of a potential bid from Midea have largely been extinguished.

Introduction

According to analyst Karri Rinta at Handelsbanken, Electrolux ( ELUXY ) is an attractive and “easy target” for the relatively larger Chinese industry peer Midea. Yet, is Investor AB ( IVSXF ), the largest owner, willing to sell at this stage? And what are the prospects of the company on a stand-alone basis?

Electrolux is a global appliance company offering products such as refrigerators, freezers, washing machines, ovens and any relevant home utilities. In 2019, it was decided that Electrolux professional, the business unit with more industrial appliance products were to be spun-off from Electrolux and is now a separate stock listed entity. Since then, Electrolux has a more specific target group: the end consumer. They strive after continuous sustainable innovation within the three areas: taste, care and wellbeing. This is done by developing products that are more resource efficient and facilitate for the user to optimize and use the product sustainably like developing smart washing programs with lower temperatures and reduced water consumptions, refrigeration solutions that help reduce food waste and new launches of equipment with less CO2 emissions. Furthermore, they develop products with a circular mind; offering recycled or recyclable appliance materials and more sustainable packaging. In the annual report 2022 they describe their innovation process related to their strategy for profitable growth through innovation and efficiency:

"By leveraging our scale through global innovation processes and modularized product architectures we have the ability to rapidly and efficiently bring attractive products to the market that meet the needs and desires of our targeted consumer groups. Digitalization and automation are additional important elements in providing cost-competitive products with high quality."

Recent Company Concerns

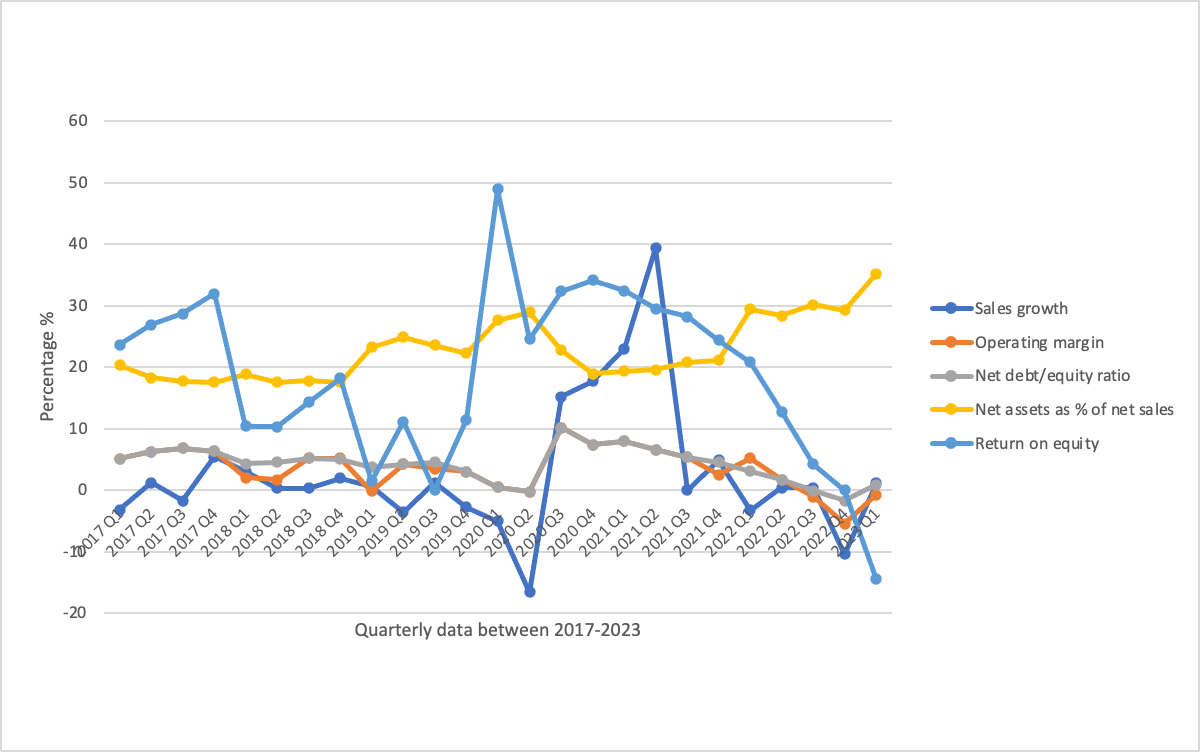

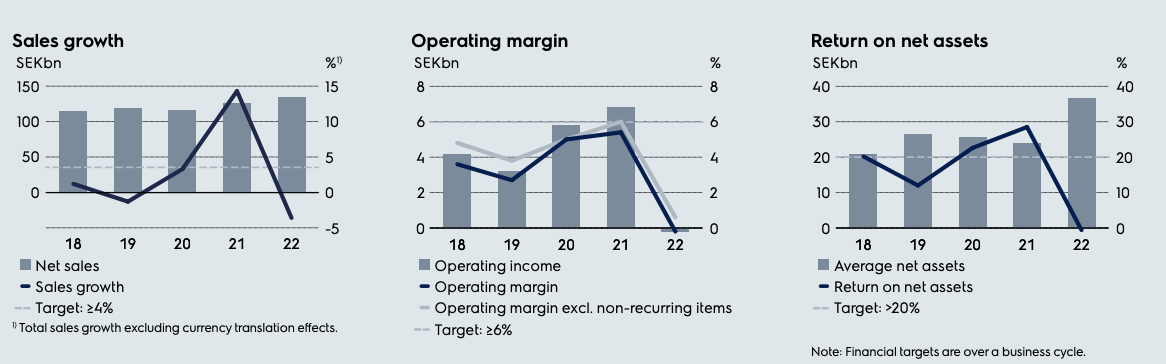

Nonetheless, the company has suffered lately from squeezed margins and lowered sales volumes following a turbulent time with supply shortages and decreased demand arguably catalyzed by the post-pandemic interest hikes. As a cyclical business, this headwind comes into effect quickly. Yet the ambition is to reach operating margins of more than 6%, return on net assets of at least 20% and sales growth of 4% annually over a business cycle - a long-term view needed for this type of business.

{kind=link}

{kind=link}

But, it appears management believes that the cyclical nature of the business is not a good enough excuse for poor performance, subsequently Electrolux has initiated a group-wide cost reduction and North America turnaround program in September to reduce their cost base: “A successful implementation of the Group-wide cost reduction and North America turnaround program will be our number one priority for 2023.” As they expect a decrease in cost with an excess of SEK 7bn once fully implemented and for the full year of 2023 a positive year-over-year earnings contribution of SEK 4–5bn - adjusting for this while keeping all other 2022 values constant, would turn Electrolux profitable again with an operating income of about 185M and a net profit of around 142M. Electrolux has made large investments in the past, and made strategic decisions related to the exit of Russia in 2022 relating to a divestment expense of SEK 350M and a future closure of Nyíregyháza factory in Hungary resulting in a non-recurring item of SEK -561M in 2024 in Q1 2023. While these adjustments may offer some unleashed potential to not only get back to profitability but also to grow the business, there is high uncertainty regarding the actual outcomes of all these factors, therefore I present a more nuanced scenario estimation below in my projection scenarios.

Projected Growth Possibilities

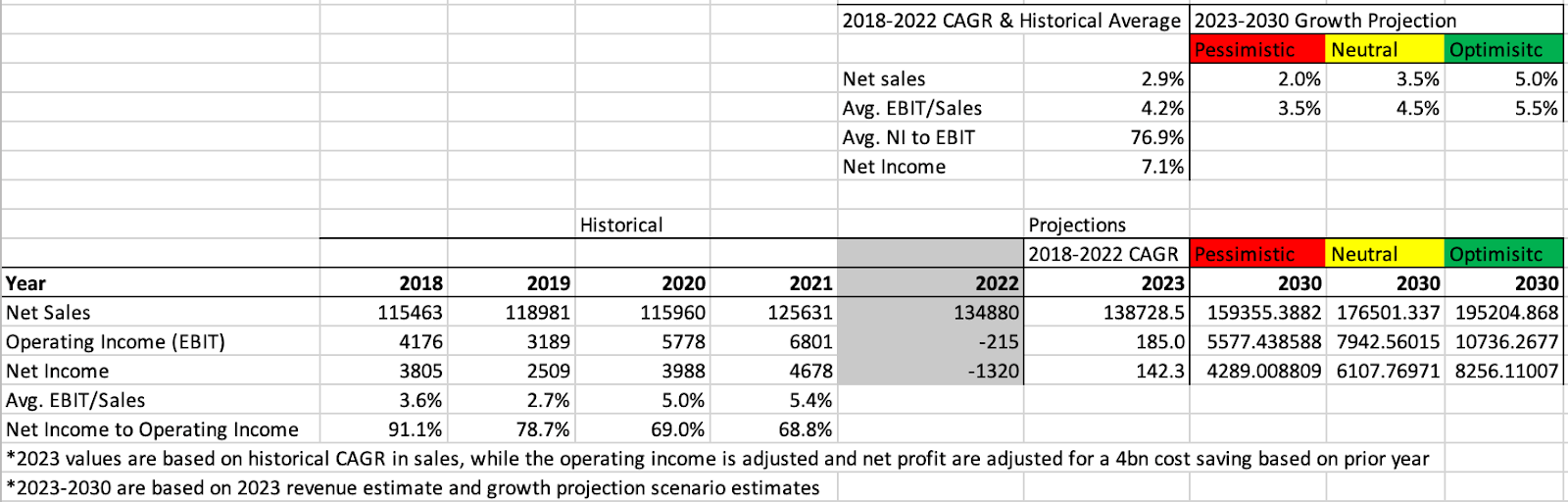

Below is a growth projection sensitivity scenario for the coming seven years. I believe it is reasonable to assume that this incumbent can grow sales at an annual rate of 2-5% per year and achieve an EBIT margin of 3.5-5.5%, which is based on its four year prior historical performance. As we can see, Electrolux experienced a significantly unprofitable year in 2022 due to several non-cash, non-recurring items that are mentioned above and also due to the after-shock of a high demand cycle in 2021. During Covid, the company was not able to ship finished goods due to the supply chain mess. So, once these conditions eased Electrolux was finally able to send goods which is the reason for the companies high sales growth in 2021 & 2022. However, the company sees difficulty ahead due to the pent-up demand waning away.

{kind=link}

Given the sales and EBIT/sales assumptions hold, I expect the company's net income to lie between 4.2 billion SEK and 8.2 billion SEK. The true outcome will likely vary significantly based upon where 2030 finds itself within the cyclical sales cycle. ELUXY is currently selling for a 42 billion SEK valuation at the time of this writing, therefore an optimistic scenario implies that the company is trading at a favorable valuation whereas the pessimistic scenario does not imply so.

To expand, this relatively conservative picture is pointing at a medium risk to return, and a low reward case. While the company may experience a financial turnaround with continuous growth and rebound profitability, it is facing competition that may restrict its already limited expansion scope (the company is exiting countries such as Russia and Hungary rather than entering new countries) although there is still market share to win in the main markets. Nonetheless, Electrolux experienced a relatively weaker demand in 2022 across basically all markets; besides a double-digit decline in Latin America it also saw a decline in Europe (excluding Russia) of -10%, and a decline of -6% in the US. However, in Asia and Africa a slightly positive trend in demand was seen despite the inflation and weaker macro sentiment.

Industry Dynamics

Electrolux is not alone. In its 2022 annual report , Bosch stated that:

"The Consumer Goods business sector suffered from the steep drop in demand for home appliances and power tools. Along with the end of the extraordinary boom that prevailed during the height of the coronavirus pandemic, increasing consumer reticence due to higher energy prices and to the general cost of living is likely to have an effect."

On the other hand, several of Electrolux’s competitors are operating in various business areas, which is somewhat of a hedge to the cyclical nature of home appliances, which may be advantageous both for cross-business synergies in R&D as well as constant revenue streams reducing the risk. But over-diversification also leaves the company less focused, which may be a strategic advantage to Electrolux, a company that has maintained its reputation as a leading home appliance firm. With that said, one may question if the size and the cash reserves will suffice to make the necessary investments to keep up with the rapid changes in the market due to digitalization or whether the prior investments they argue have been made will yield the expected returns. Yet this is the plan as they are in the final stage of executing a SEK 8bn re-engineering investment focusing on modularization and automation of selected production facilities in Europe and the Americas. In the Electrolux annual report it is clearly communicated that investments in digitalization are important to manage sourcing, supply chain and logistics efficiently and meet customer demands through interactions by modularized products, flexible product offerings and production efficiency gains. Now, with these risks mentioned, Electrolux may not be the most lucrative investment case on a stand-alone basis. However, if a public bid is made by Midea, one might expect a positive reaction - but how likely is it?

Midea Rumors Extinguished

Little is known about the Midea offer and whether or not Investor is ready to give up its long-held ownership in Electrolux that dates all the way back to 1956 Håkan Lindgren: Wallenberg archive. DI, 2023 explains that the Investor, owning 18 percent of the capital and 30 percent of the votes in Electrolux, is not willing to let Electrolux go as of yet. According to Affärsvärlden sources claim that Electrolux and the investor believe the preliminary bid set by Midea, although offering a significant premium, was undervaluing the company.

My partner and I were present at the Investor AB shareholder meeting, where we heard management shake off any possibility that they sell their large stake in Electrolux. Rather, the investment company is focused on delivering value with the cost saving initiatives mentioned earlier. It is unreasonable to expect that they are pushing for large cost-cutting initiatives to then directly sell the company, but perhaps we can expect Investor AB to sell at a later stage after these initiatives have taken hold? Altogether, considering that Investor AB is a proud long-term owner of primarily Swedish companies it is not likely that they will sell any time soon especially if the bidding price is considered too low. Hence, the rumors have been to a large extent extinguished.

Concluding Remarks

In conclusion, Electrolux, a global appliance company, has faced challenges in recent times, including squeezed margins and decreased sales volumes. However, the company has initiated cost reduction and turnaround programs to improve its performance. The projected growth possibilities indicate a medium-risk, low-reward scenario, and competition in the industry may restrict expansion opportunities. Despite these challenges, Electrolux has maintained its reputation as a leading home appliance firm. The company's largest owner, Investor AB, is likely not willing to sell its stake in Electrolux at this stage, and the rumors of a potential bid from Midea have largely been extinguished. Overall, while Electrolux may not be the most lucrative investment case on a stand-alone basis, its focus on cost-saving initiatives and long-term ownership by Investor AB suggest a commitment to delivering value in the future. Given that the company can likely turn the operations around, I believe investors will be substantially rewarded, but since this is uncertain I rate the company a Hold for the time being.

For further details see:

Electrolux: Unlocking Potential Amidst The Midea Rumors - Is It Time To Invest?