ELMD - Electromed: Reiterating Buy With Sales Rep Conversions Driving Top-Line Growth

Summary

- Solid Q2 result with upsides versus consensus at the top and bottom lines.

- Sales force increase converting to further sales growth with >$950,000 in revenue/rep this quarter.

- Reiterate buy with revised price target to $15.

Investment Summary

Following my last publication on Electromed, Inc. ( ELMD ), the stock has caught a tremendous bid and rallied ~36% to the upside at the time of writing. The report, titled "SmartVest Clearance Adds Alpha Opportunity" made several arguments around the company's SmartVest system and how the recent 510(k) clearance had opened up the gate for investors to position against a name that is innovating in the high-frequency chest wall oscillation ("HFCWO") domain. As a reminder, the company is honing its focus for the SmartVest on the bronchiectasis and chronic obstructive pulmonary disease ("COPD") treatment markets. For a full analysis on each disorder, plus the underlying growth forces in the market, check out the deep dive I performed in the last publication.

{kind=link}

Turning to the company's Q2 FY 23numbers , it was equally as pleasing to see upside surprises at the top and bottom lines, especially in the current macro-climate. Several mid-term growth drivers were observed throughout its quarterly numbers and this was supported by constructive forward-looking language from management on the earnings call . Here I'll run through all of the moving parts from the ELMD's Q3 earnings and tie this back to the original buy thesis. Net-net, I reiterate ELMD stock as a buy and have revised the 20 23price target to ~$15, eyeing a strong performance from the company this year.

Unpacking ELMD's Q2 FY 23numbers

Before scrutinizing the financial performance, I'd suggest there's three key growth drivers in ELMD's flywheel to grasp first. Specifically:

- Referrals. The company noted that referrals continued accelerating YoY, indicating that efforts to expand its sales force headcount is generating a strong ROI on the human-capital investment. As such, with 48 sales reps, up from 44 last quarter [and a fully staffed reimbursement team], ELMD is efficiently converting referrals into approvals and shipped product. It therefore met its previous goals of getting 48 reps in the first place. More importantly, the increase in rep-count means that each sales rep has less area to covered, and can therefore drive sales concentration without having to distribute their efforts across as large of an area. Looking at the productivity, revenue per rep came in to $927,000 per rep, up 415bps from $890,000 sequentially and well within the target range of $850,000–$950,000/rep. I'd opine this is a good springboard in commercializing the new ClearwayVest looking ahead.

- Clinical trial momentum. ELMD's multi-site outcome study looking at the SmartVest's treatment for bronchiectasis patients is at a 37% enrolment [n=37/100], and an additional site has been approved to increase the pace of enrolment. In extension, ELMD's bronchiectasis quality-of-life ("QoL") outcome study analysis is also entering its final stages, and the QoL outcome study with COPD patients will be presented at the American Thoracic Society ("ATS") 2023 International Conference in May.

- The DTC model to increase volume. It is driving unit volumes and new users through prescribers [mainly pulmonologists treating bronchiectasis] forms the crux of ELMD's 3-pillared set of growth initiatives. The benefit of this model is seen in that it enables an accelerated uptick in new user accounts with the more providers under the company's wings, where the efficacy and patient response can do the talking as to results, so to speak. Consequently, there's a dual incentive for both the pulmonologist and for the patient, and we've seen this kind of model work well in device prescription as the tail of asset returns can lengthen extensively as the 'installed' patient base begins to grow.

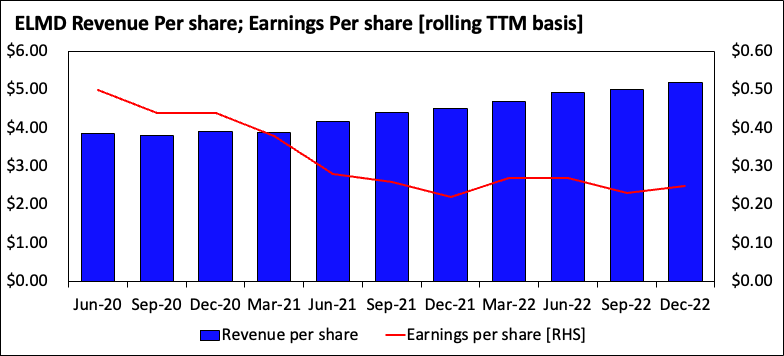

Now turning to the numbers. ELMD reported quarterly net revenues of $11.7 million, a 15% YoY increase. Growth was underscored by a 14% YoY increase in Homecare revenue, which totaled $10.7 million, made possible by the increase in referrals and supported by the sales force expansion discussed earlier. Moving down the P&L, it clipped operating income of $1.27mm, a YoY growth route of 18%, spurred by the revenue growth. It pulled this down to earnings growth of 16% to $977,000 or $0.11 per share.

Fig. (1)

Note: All figures shown in Per Share basis [Revenue per share ; Earnings Per Share] (Data: Author, using data from ELMD's SEC Filings)

{kind=link}

Looking to its quarterly homecare distributor revenue, it clipped a 13% YoY decrease to $336,000. More importantly to this analysis, however, it's important to explain that distributor sales can exhibit notable fluctuations in quarterly revenues. Looking at its YTD growth [i.e., Q1 and Q2 FY23] it has come to, 64% at the midpoint of its full-year FY 23guidance in this domain. Moreover, it recognized institutional revenue of $589,000, representing a 77% YoY increase for the quarter. Upsides here were seen chiefly on the back of increased capital sales to its institutional customer network. Ex-U.S. revenue was also $72,000, which decreased by 42% YoY for the quarter as expected from prior guidance.

Turning to the marginal analysis, ELMD's gross profit for the quarter increased to $8.7 million on a 74% margin, down ~300bps YoY. This was largely expected given the inflationary pressures compressing margins for input and manufacturing costs on revenues. Further, it recognized this in higher shipping expenses to expedite its inventory purchases. Noteworthy, management said the cost of revenues improved substantially up towards the c.75%+ mark towards the back end of the quarter. It also saw a ~12% headwind at the SG&A line with total OpEx of $7.4Bn for the quarter. However, its again important to realize the 12% gain stemmed primarily as a result of the investment into growing the salesforce headcount and reimbursement departments, and are therefore an investment into future growth in my estimation. Further, a breakdown of ELMD's working capital and fixed asset base is observed below. The company is well capitalized to continue operations with a current ratio of 5.7x and no debt on the balance sheet.

Fig. (2)

Data: Author, with data from ELMD's Q2 FY 23 10-Q

Valuation and conclusion

The stock is trading at a reasonable premium at 22x forward EBITDA but this mightn't be the best way to value the stock given it's got some time before it really starts driving profitability down the P&L. It trades at an attractive 2.5x forward sales, meaning we'd expect ELMD's top-line to expand by this much over a predefined investment horizon [say, 5 years] if paying that multiple today. I do believe the company can reach this level of growth over that time frame, and therefore believe the company is fairly priced at this mark. Last report I laid out the bottom-line growth assumptions into FY25, with a $0.26 EPS estimate for this year [see: last publication, Exhibit 5, " ELMD's FY23–25E' growth assumptions" ]. Following the results, I see no change to this growth trajectory. Hence, I'm revising the price target higher to $15.34, eyeing a strong bottom-line growth period into the next 2-years.

Net-net, each of the factors discussed here support a continued buy rating for ELMD. The company continues advancing on its growth route, and market adoption of its SmartVest continues to demonstrate as an ongoing alpha opportunity, also reflected in the stock's price action into the new year.

Key risks

As a footnote, the major risks to the buy thesis include the following factors:

- ELMD is a small-cap and its share price can undergo large price swings. This is a key market risk.

- When investing in small-cap stocks, fundamentals can become widely disconnected from technicals. Hence, this could nullify the buy call.

- If the company doesn't adhere to the forward EPS estimates, this could result in a re-rating to the downside.

Investors should understand these risks in full before committing to any long position in ELMD.

For further details see:

Electromed: Reiterating Buy With Sales Rep Conversions Driving Top-Line Growth