THQQF - Electronic Arts: High Quality Revenue Model

2023-04-01 00:07:53 ET

Summary

- Electronic Arts Inc. is a global company that creates, markets and publishes games.

- EA has done a fantastic job of monetizing its IP, allowing the business to generate outsized returns through recurring revenue.

- The company has market-leading IP while expanding into key growth areas such as Mobile gaming.

- Profitability is far in excess of EA's peers, with the company having the capacity to generate >30% EBITDA-M and >20% FCF conversion.

- Our valuation suggests upside, with strong buybacks and dividends possible in the coming decade.

Investment thesis

The gaming industry is highly attractive due to the growth we have seen historically and the ability of companies to generate accretive gains due to improving economics. Electronic Arts Inc. ( EA ) looks to be a leading business in this industry, with the key characteristics to generate outsized returns. Our analysis will look to assess this, considering the key success factors and financial performance of the business.

Company description

Electronic Arts Inc. is a global company that creates, markets and publishes games, content, and services for game consoles, PCs, and mobile phones.

Its portfolio includes games from diverse genres, such as sports, racing, first-person shooter, action, role-playing, and simulation, under popular brands such as Battlefield, The Sims, Apex Legends, and Need for Speed. In addition, the company licenses games from other entities, such as FIFA (Soon to be ending), Madden NFL, UFC, and Star Wars.

Share price

EA's share price has grown rapidly in the last decade, gaining over 450%. This has been driven by rapidly improving financial performance and improving KPIs. EA has been leading the market in the monetization of games, allowing the business to produce accretive gains.

Monetization

In recent years, EA has been transitioning its business model from one-time game purchases to a recurring revenue model based on in-game purchases and subscriptions. The best example of this is FIFA Ultimate Team, where players can open "packs" containing players, with gamers encouraged to keep opening packs until they get the best players. The company's live services and esports initiatives have been critical in driving this transition, with the nature of their gaming titles perfect to allow for the execution of monetization. It would be far more difficult to monetize a story-based game in this fashion, which gives EA an advantage compared to many of the other publishers.

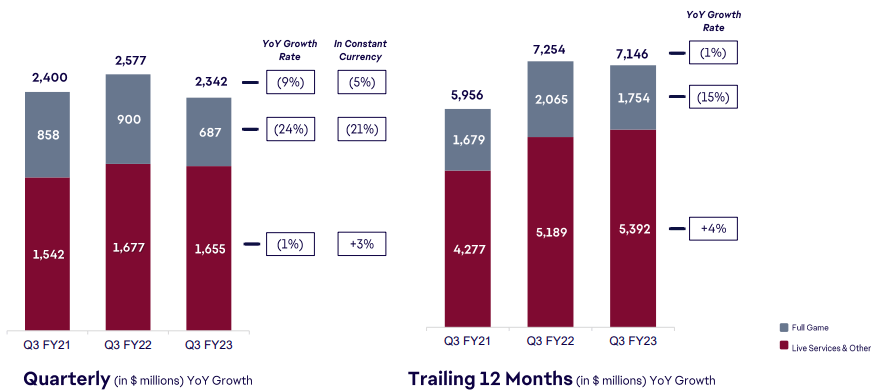

From a financial perspective, the traditional full game model was to spend a large amount of money upfront marketing and building the game, with the hope of success producing gains above cost. This is similar to the movie industry. It creates far more risk for the company and only produces returns at a single point per consumer. This was especially unfortunate as many console gamers are purchasing games secondhand, resulting in no money going to the publisher. The financial benefit of a subscription model/in-app purchases is that the publisher can continue to monetize a game that is already built, with minimal marginal cost. This is highly accretive, allowing the business to earn outsized returns per consumer. Our view is that EA is the most progressed in this respect, with FIFA leading the charge. In the LTM period, EA generated $5,392M from its live-service segment, representing 75% of revenue.

We should acknowledge that many consumers are not a fan of this model. Further, it has been suggested that this is predatory, targeting children who are not aware of the gambling-like nature of these systems. For this reason, there has been some political pressure to ban/limit the ability of publishers to implement these in their games. The UK Government has found that it is linked to gambling , although has stated it will not be banned. Our view is that this may be the biggest risk for EA, should legislation begin to limit the scope for monetization.

Franchise model

Another important characteristic of EA is its portfolio of games. The company has a wide range of franchise-based games, such as FIFA, Battlefield, and Madden. The benefit of these games is that they are not built from scratch but incrementally developed with every new release. Further, each new iteration builds on the marketing and image of the last, generating improving market awareness over time. This again is a highly accretive model as it means game development and marketing investment is far lower than it would need to be had the game been a new IP.

Mobile gaming

The mobile gaming market has seen significant growth in recent years, with more consumers playing games on their smartphones. This trend has been led by the improvement in technology, allowing for better games to be run, as well as a greater desire for convenient short-term enjoyment.

According to market research firm Newzoo , the mobile gaming market is valued at $92.2BN, accounting for 50% of the total video game industry revenue. EA has looked to exploit this segment, expanding its mobile gaming portfolio with the acquisition of Glu Mobile for $2.1 billion . This acquisition will allow EA to develop its gaming exposure in line with its traditional releases, increasing its total addressable market.

From a financial perspective, the scope for gains is similar to the live-service discussion above, with mobile apps filled with in-app purchases. The mobile phone monetization model is arguably more aggressive than EA's traditional games.

{kind=link}

Financial analysis

EA's financial performance (EA)

{kind=link}

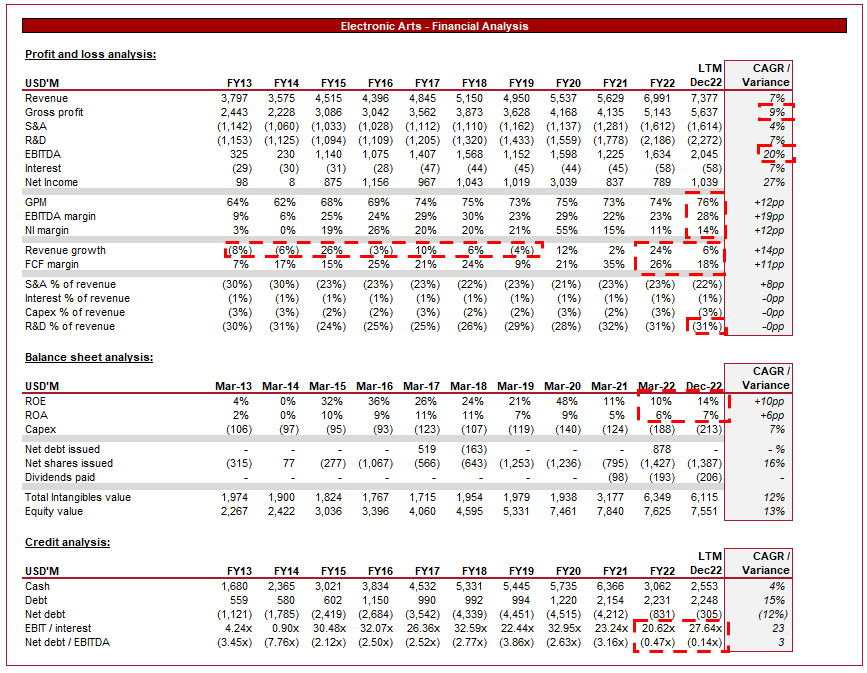

Presented above is EA's financial performance for the last decade. We can summarize it as incredibly impressive, marrying growth with margin expansion.

Revenue has grown at a CAGR of 7%, driven primarily by growth in their key franchise titles, alongside the release of new games such as Apex Legends and Star Wars. As the below illustrates, not only is the live service segment the larger of the two, but it is also the more resilient. With softening economic conditions, it is not surprising to see demand softening. Despite this, YOY growth is still present, while full-game sales have declined.

{kind=link}

EA has seen its GPM improve across the historical period, gaining 12ppts. in 10 years. This is a highlight of the accretive nature of live services, illustrating the games EA has made as it transitioned to a greater amount of revenue from this segment.

S&A expenses have grown at a rate of 4%, far lower than revenue. This is a reflection of their strong IP, allowing the business to be conservative with its marketing investment as a means of driving revenue. In my opinion, many individuals will purchase the new FIFA every year with no hesitance. This is the advantage of Franchise based games. EA purchased Codemasters several years ago, giving them several premier racing titles, including Formula One, allowing them to expand the franchise IPs they have.

On a normalized basis, the company is able to generate an EBITDA margin of over 25% and a FCF conversion in the region of 20%. This is a market-leading return, which will allow for healthy consistent distributions to shareholders.

Moving onto the balance sheet, we see the improving returns reflected in the increasing ROE. This has dipped in recent years due to the accumulation of cash but Management has increased their distribution to shareholders, including initiating dividends.

Despite the growth and distributions, EA remains well capitalized, with a net debt position of $(305)k. This will allow the business to further conduct M&A if required.

Overall, we are very impressed with EA's financial performance. The company has grown into a SaaS-like business, with market-leading profitability metrics.

Outlook

Analyst target (TIkr Terminal)

{kind=link}

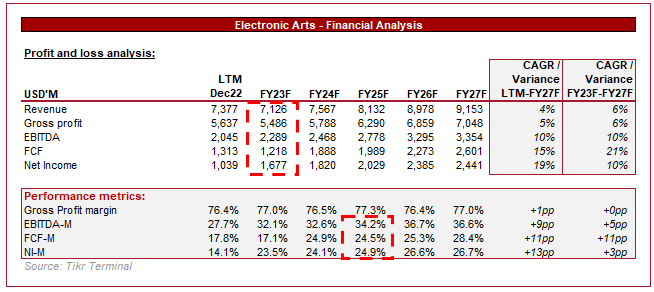

Presented above is Wall Street's forecast for EA's coming 5 years.

Analysts are expecting revenue growth to remain in excess of 5%, following a soft FY23. We concur with this view, as live service produces outsized returns as the gaming industry continues to grow as impressively as it has.

Analysts are highly bullish from a margin perspective, expecting the company to see a noticeable expansion in both EBITDA and FCF margins. These are levels the company has achieved in the past, although not for an extended period. Our view is that these are levels that EA could achieve but would like to see further evidence before considering them likely. If EA was to achieve these levels in conjunction with 5%+ growth, a >25x EBITDA multiple would be reasonable.

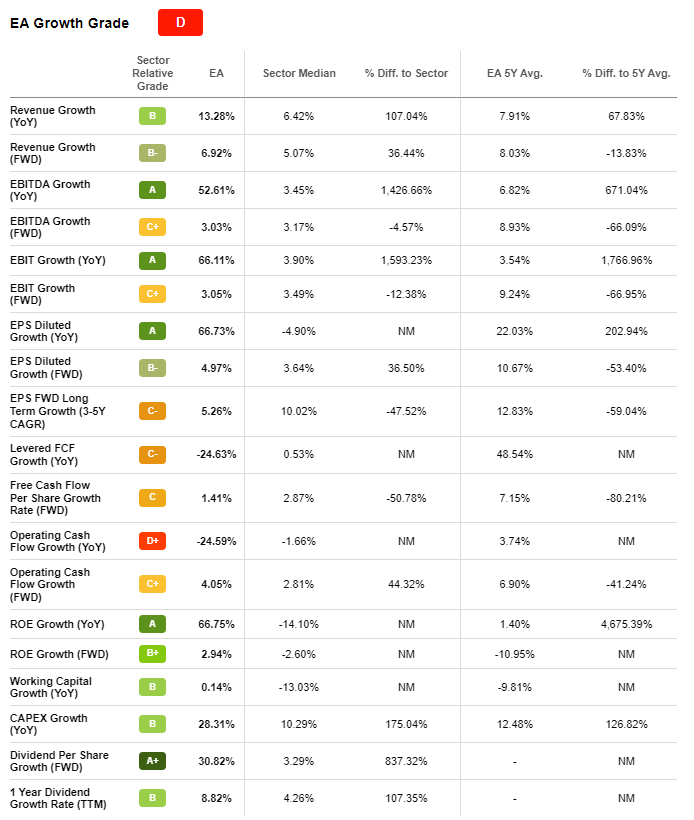

Peer group comparison

Profitability grade (Seeking Alpha)

Presented above is Seeking Alpha's profitability rating, comparing EA to its sector peers.

As we mentioned previously, the company is generating market-leading profits, which is perfectly illustrated above. EA's GPM is over 50% greater than the sector median, with this flowing down to EBITDA, which is equally outperforming.

{kind=link}

From a growth perspective, EA scores less well. This is a reflection of its relative maturity when compared to other peers. Additionally, many in the industry are active in the M&A market, resulting in large inorganic growth. Despite this, EA scores very well in key metrics, such as revenue growth (both Y/Y and forecast), EBITDA growth, and EPS.

EA's economic resilience is reflected in the EPS growth, with the sector experiencing a decline.

Valuation

EA Valuation (Seeking Alpha)

EA's valuation reflects its impressive financial metrics. The company is trading at a premium to the majority of its peers, with an LTM EBITDA multiple of 15x and a P/E ratio of 20x.

Our view is that premium companies deserve a premium valuation. Rarely does the profitability of EA has come at a discount.

With EA producing far superior profitability, we have conducted a DCF valuation to calculate an absolute valuation.

Our key assumptions are:

- Revenue growth of 2% in FY23F, followed by growth between 4-6%.

- FCF conversion improving from 17% to 21%, conservatively below analyst forecasts.

- EBITDA growth exceeding revenue but again more conservative than analysts are forecasting.

- Perpetual revenue growth of 3%, a discount rate of 9%, and an exit multiple of 15x.

Based on this, we derive a current upside of 10%, which is below analysts, who are targeting 18%. With tough economic conditions, EA's relatively sticky financial performance should allow the business to outperform, placing greater value on this 10% target.

Final thoughts

EA is fundamentally a highly attractive business. The company's key strengths are its franchise focus, monetizability, and marketing-leading IPs. These strengths reduce the key risks in the gaming industry, that being the reliance on full game sales while being positioned perfectly to exploit the biggest opportunity, which is the ability to continually upsell over time. From a profitability perspective, EA may be the best business in the gaming industry. Our view is that strong investor distributions will follow in the coming years, which will return alpha over many of its peers.

The gaming industry is highly attractive and we believe most investors should have some exposure if they are seeking outsized returns in the coming years. We have already covered Take-Two Interactive ( TTWO ) and Embracer Group ( THQQF ), considering them both a buy.

For further details see:

Electronic Arts: High Quality Revenue Model