EA - Electronic Arts: The Recent Drop Created A Good Entry Point

2023-08-20 07:33:21 ET

Summary

- Electronic Arts' stock price dropped after lower-than-expected net bookings in 1Q FY24, but the company's financial results were strong overall.

- EA is set to launch new games, including EA SPORTS FC24 and EA SPORTS NHL24, which could boost net bookings.

- To improve its competitiveness in the gaming industry, EA increased its R&D, sales and marketing, and general and administrative expenses in the past three years.

- EA's gross profit margin is higher than its peers, and I expect its profit margin to improve to the levels it was three years ago.

After Electronic Arts ( EA ), an American video game company, which is the producer of known video games such as FIFA, The Sims, Need for Speed, Battlefield, Madden NFL, Apex Legends, and lots of other video games, published its 1Q FY24 financial results on 1 August 2023, the stock price dropped. EA stock price decreased from $136 on 1 August to $118 on 18 August, down 13.2%, as the company’s net bookings were below expectations (due to underperformance from Season 17 of Apex Legends). EA’s lower-than-expected net bookings in 1Q FY24 can be connected to decreased purchasing power of players (due to inflation), and higher competition in the gaming industry.

From my perspective, the recent drop has made EA attractive, and shortly, its net bookings can increase beyond expectations. Also, EA’s 1Q FY24 financial results can’t be considered as weak. Driven by strong momentum in EA SPORTS global football and Star Wars Jedi: Survivor, the company’s 1Q FY24 quarterly results were strong. Also, the company’s raised the FY24 guidance for its EPS significantly. Electronic Arts is expected to launch EA SPORTS FC24 on 29 September 2023 (see Figure 1). The company claims that EA SPORTS FC24 will improve the in-game realism to a new level, with HyperMotionV being EA’s biggest leap forward in realism to date. Also, EA SPORTS NHL24, which is expected to arrive on 6 October 2023, is claimed to unleash the intensity of Hockey with an all-new exhaust engine and physics-based contact. Overall, the future of the company is bright, and the recent price drop, just made it a buy.

Figure 1 – EA SPORTS FC’s First Ever Cover Star, Erling Haaland.

www.ea.com

Financial and operational results

In its 4Q FY23 presentation, Electronic Arts estimated its 1Q FY24 net revenue to be between $1825 to $1925 million, its cost of revenue to be $350 to $370 million, its EPS to be between $0.98 to $1.14, and its net booking to be $1500 to $1600 million. In its 1Q FY24 results, EA reported net revenue of $1924 million, cost of revenue of $368 million, EPS of $1048, and net bookings of $1578 million, respectively. Also, the company raised the guidance for its FY24 GAAP EPS from $3.30-$3.81 to $3.42-$3.92.

Electronic Arts reported a total net revenue of $1.9 billion (up 9% YoY), and its operating cash flow increased from $(78) million in 1Q 2023 to $359 million in 1Q 2023. In the first quarter of fiscal year 2024, EA’s net bookings increased by 21% YoY to $1.6 billion due to the company continued live services growth and new player acquisition. It is worth noting that EA SPORTS FIFA net bookings in the first quarter of fiscal year 2024 were a record for the franchise. Also, Star Wars Jedi: Survivor is entertaining millions of players globally.

Electronic Arts expects its 2Q FY24 net revenue to be $1825 to $1925 million, and its 2Q FY24 net bookings to be $1700 to $1800 million, higher than in the previous quarter. However, as the company is expected to devote a huge amount of money to R&D and marketing in the following months, its 2Q, 3Q, and 4Q FY24 earnings are not expected to be as high as in 1Q FY24. In the next section, I will explain why this is not a negative thing for the company, and why EA’s decreased price (partly due to its current relatively low profit margins) has created a good entry point.

Valuation

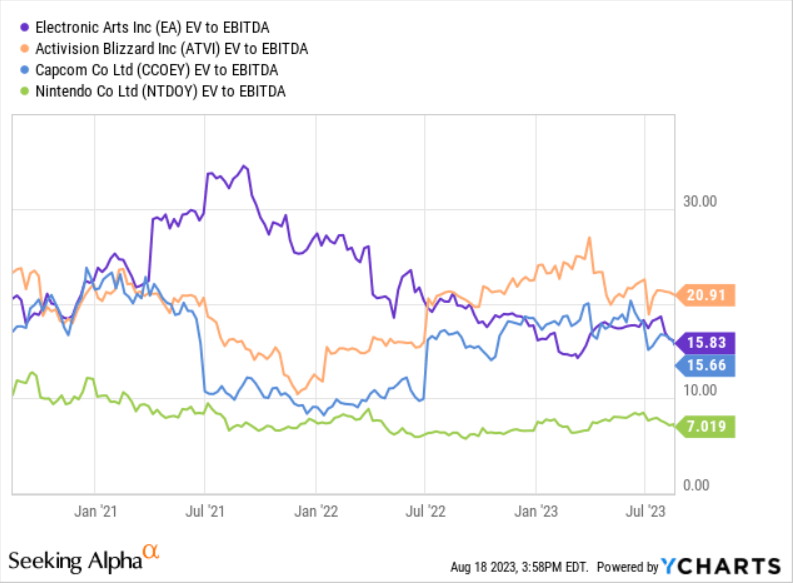

According to Figure 2, EA’s EV-to-EBITDA is lower than the EV-EBITDA of Activision Blizzard ( ATVI ), equal to the EV-to-EBITDA of Capcom ( CCOEY ), and higher than the EV-to-EBITDA of Nintendo ( NTDOY ). We can see that in January 2022, EA had higher EV-to-EBITDA than ATVI. However, as Microsoft announced it has plans to acquire Activision Blizzard for $95 per share, ATVI’s stock price started increasing. The deal between Microsoft and Activision Blizzard is not final yet; however, it is expected to succeed or fail by 18 October 2023. Microsoft believes that a share of ATVI is worth $95. But investors might not have the same view. In another article on ATVI, I explained that if the deal fails, ATVI’s stock price might not decrease as Activision Blizzard will receive a huge amount of money from Microsoft as a break-up fee. My point here is that EA’s lower EV-to-EBITDA (compared to ATVI) does not necessarily mean that EA is undervalued, as there is a good reason for ATVI’s higher price and higher EV-to-EBITDA. Also, we can see that compared to Nintendo and Capcom, EA’s EV-to-EBITDA doesn’t suggest that EA is undervalued. It is worth noting that Nintendo has a market cap of $50 billion, Capcom has a market cap of $9 billion, Activision Blizzard has a market cap of $71 billion, and EA has a market cap of $32 billion. But this is not all you should know about Electronic Arts. There are other things that make EA a buy for me.

Figure 2 – EA’s EV-to-EBITDA vs. peers.

{kind=link}

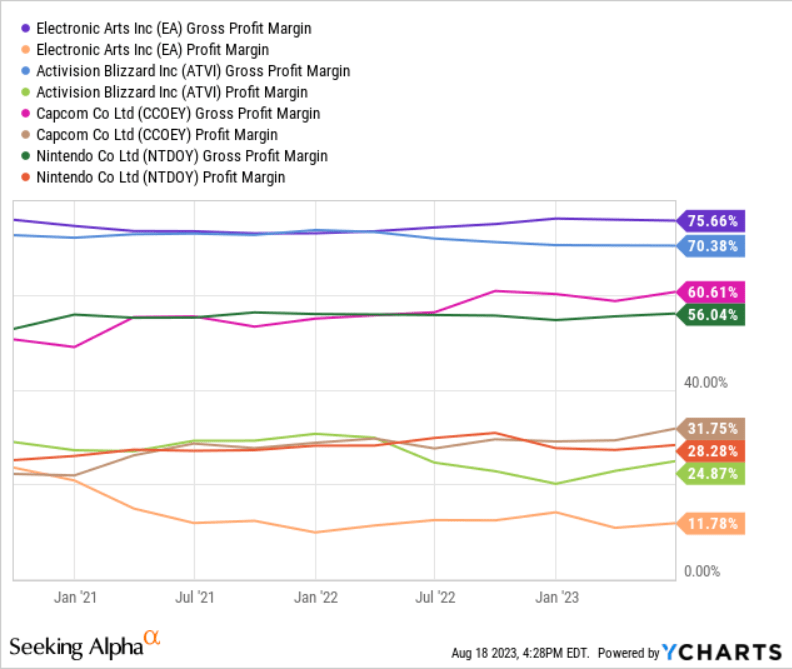

Figure 3 shows that while EA has the highest gross profit margin compared to its peers, it has the lowest profit margin. A higher gross profit margin of EA in comparison to ATVI, CCOEY, and NTDOY simply means that for each dollar that EA expends as cost of revenue, it makes more money than its peers. However, its lower profit margin shows that EA’s operating expenses are significantly higher than its peers. Three years ago, EA’s operating expenses were not as high as they are now. Looking at Figure 3 we can realize that the gap between EA’s gross profit margin and the peers in the second half of 2020 was not as high as it is now. But there is a good reason behind EA’s lowering gross profit margin in the past three years.

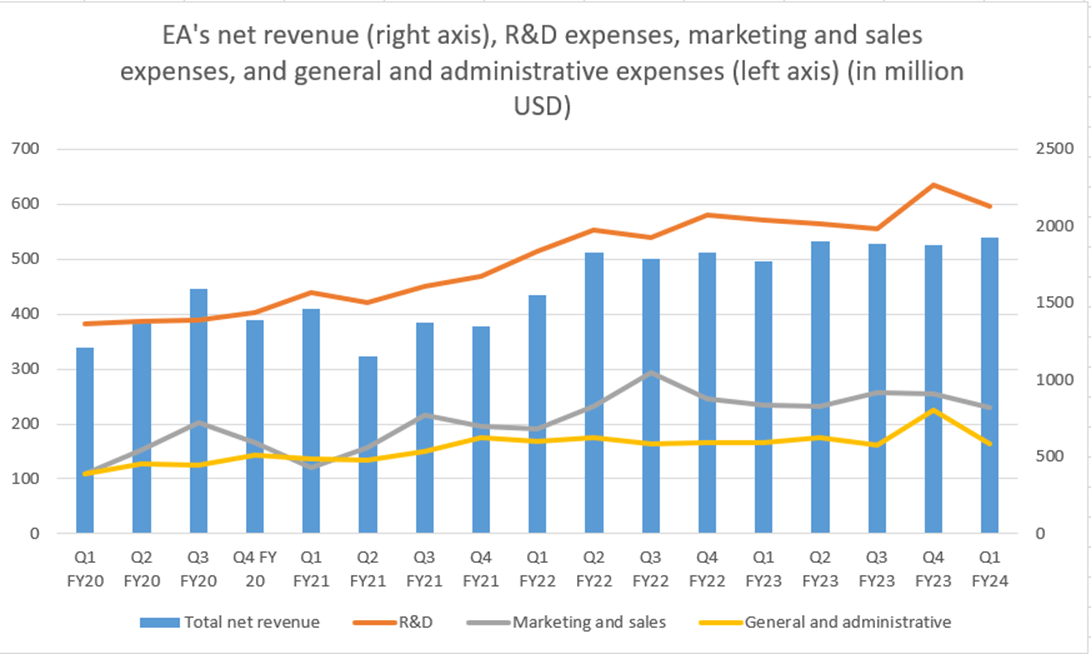

From fiscal year 2020 to fiscal year 2023, EA’s net total net revenue increased with a CAGR of 10.0%, while its R&D, marketing and sales, general and administrative expenses increased at a CAGR of 14.4%. Figure 4 shows that EA’s R&D expenses increased at a significantly faster pace than the company’s net revenue from the first quarter of fiscal year 2020 to the first quarter of fiscal year 2024. All I want to say is that it seems Electronic Arts decided to expend more on R&D to improve the quality of its games, more on marketing to gain the attention of more players and introduce its new games to the world, and more on general and administrative to improve the quality of its human capital.

Thus, with expanding of the global gaming market, shortly, the company’s revenues can increase in a significant way, and EA can have higher gross profit margins. Three years ago, EA had a gross profit margin of about 23%. In a few years, as a result of its recent developments, the company’s gross profit margin can again increase to that level; however, this time, Electronic Arts can be a bigger, more competitive company in the gaming industry. Besides, EA has a free cash flow per share of $1.146, while Activision has a free cash flow per share of $0.714 per share, and Capcom has a free cash flow per share of $0.195, implying that EA is in a better cash position compared to two other giants in the gaming industry.

In the twelve months ending 30 June 2023, Activision Blizzard (with total assets of $28.52 billion) recorded a cash from operations of $2547 million, Capcom (with total assets of $1.49 billion) recorded a cash from operations of $298 million, and Electronic Arts (with total assets of $13.08 billion) recorded a cash from operations of $1987 million. With a cash flow from operations-to-assets ratio of 15%, EA is using its assets to make cash in a more efficient way than Activision Blizzard, which has a cash flow from operations-to-assets ratio of 9%. However, it is worth noting that Capcom has a cash flow from operations-to-assets ratio of 20%. On March 2023, Nintendo had a total asset of $21.5 billion and recorded a cash flow from operating activities of $2400 million. Thus, with a cash flow from operations-to-assets ratio of 11%, Nintendo is not using its assets to generate cash as efficiently as Electronic Arts does.

Figure 3 – EA’s gross profit margin and profit margin vs. peers.

{kind=link}

Figure 4 - EA's net revenue (right axis), R&D expenses, marketing and sales expenses, and general and administrative expenses (left axis) (in million USD).

Author (based on EA's quarterly earnings releases)

{kind=link}

Why I might be wrong?

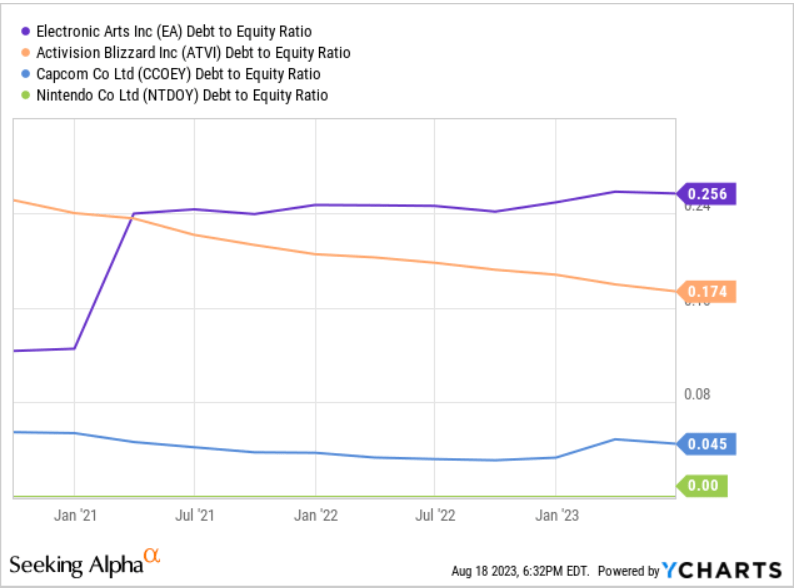

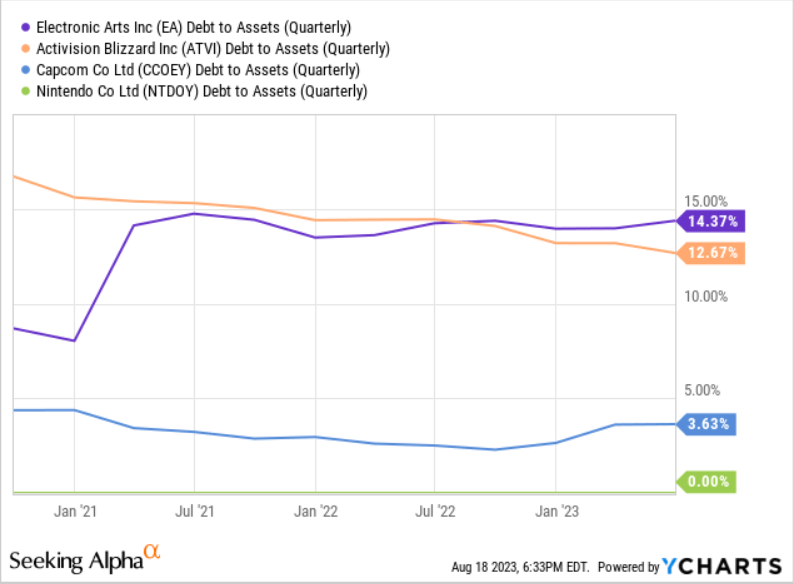

According to Figure 5, EA has a higher debt-to-equity ratio than its peers. Also, according to Figure 6, its debt-to-assets ratio is higher than its peers. It simply means that if the company cannot earn as much as it expects in the future, its relatively higher debts-to-equity and debt-to-assets ratios (in comparison to its competitors) can hurt its financial health, and prevent the company from further developments. The gaming industry is expanding, and every day, more video games can gain the attraction of players. To maintain its competitiveness, EA’s hiked R&D, marketing, and general and administrative expenses in the past three years must turn into more revenues, more net bookings, and more net income. Otherwise, EA may not be able to compete with its Japanese competitors, Activision Blizzard, and other companies like Warner Bros. Games. In another world, as much as EA’s recent expenses can help its financial results to improve, they can put the company in a liquidity crisis if EA’s new developments and games cannot turn into higher net bookings.

Figure 5 – EV’s debt-to-equity vs. peers.

{kind=link}

Figure 6 – EV’s debt-to-assets vs. peers.

{kind=link}

Conclusion

EA stock price dropped in the past few weeks, as the company’s net bookings in 1Q FY24 were lower-than-expected. However, the future of the gaming industry is bright, and EA’s higher R&D, marketing, and administrative expenses in the past three years may turn Electronic Arts into a significantly more competitive company in the gaming industry. EA has more potential to transform each dollar of expense to revenue than its peers, and might be able to improve its profit margin to the levels it was three years ago soon. The stock is a buy.

For further details see:

Electronic Arts: The Recent Drop Created A Good Entry Point