EBR - Eletrobras: Still Risky

2023-03-30 22:37:32 ET

Summary

- The Brazilian clean energy giant Eletrobras has seen a sharp dip in price since last November, which comes as no surprise, considering a changed political environment and its weak performance.

- However, there are positives too. Its results can look better in 2023 as drags like one-time costs and deflation related revenue losses disappear. Its forward P/E is attractive too.

- The political risk stays, though. And it would be good to see a turnaround in its numbers before buying it.

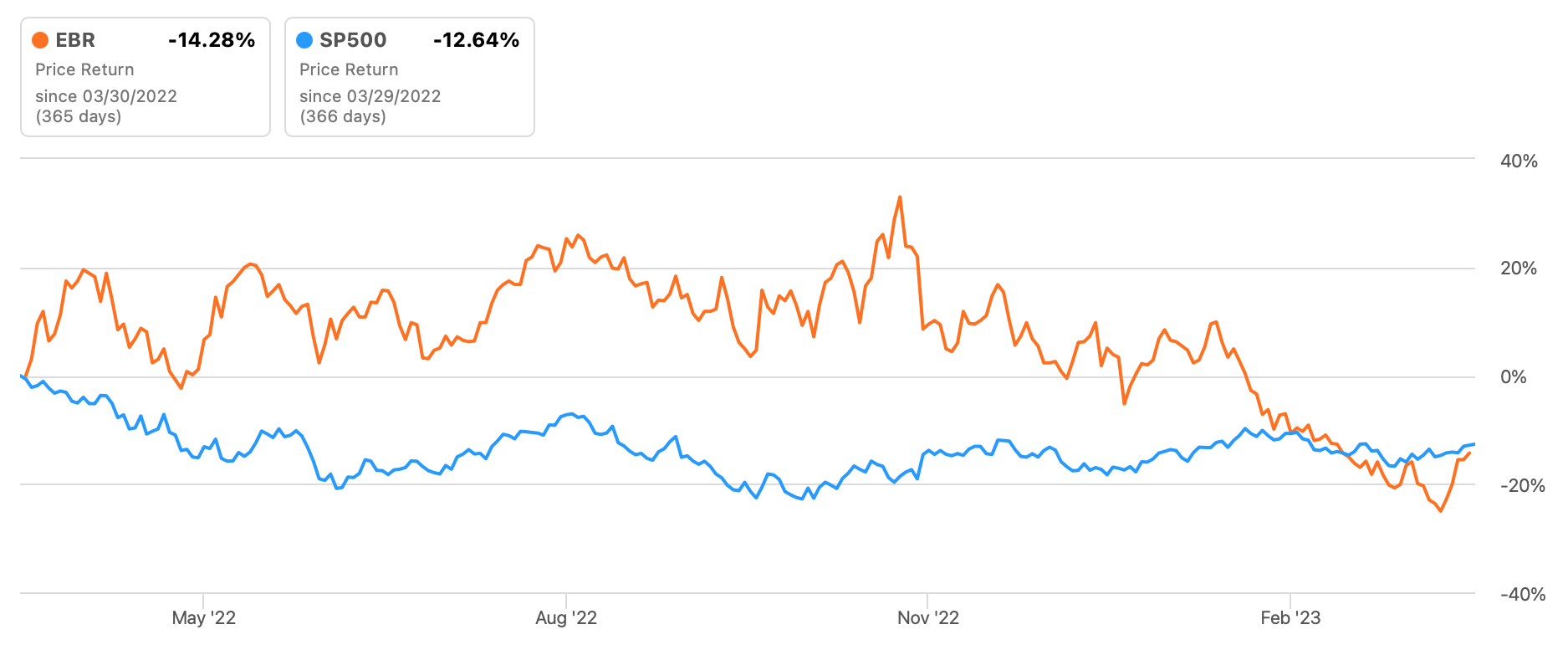

That the Brazilian clean energy utility Eletrobras ( EBR ) has seen a 10.9% price decline year-to-date [YTD] comes as no surprise. My last article on it in early November last year was actually titled " Brace For A Price Decline ”. Since that time, EBR stock price has fallen even more dramatically by 21%. While it would seem like a possible fallout of weak market conditions in general, that is not the reason. The S&P 500 ( SP500 ) has actually shown a 5.8% gain YTD and is relatively unchanged compared to last November.

{kind=link}

The reasons for Eletrobras’s challenged recent performance have to do both with its own financial performance and political conditions in its home country, Brazil. These have clearly towered over its huge potential as a huge clean energy producer, which generates 29% of Brazil's power.

At the time I last wrote about it, my assessment of a price fall was based on its poor performance for the third quarter of 2022 (Q3 2022). Both its revenues and profits had tumbled significantly, adding to the uncertainty already there in Brazil after President Lula of the Workers’ Party came into power.

Poor results

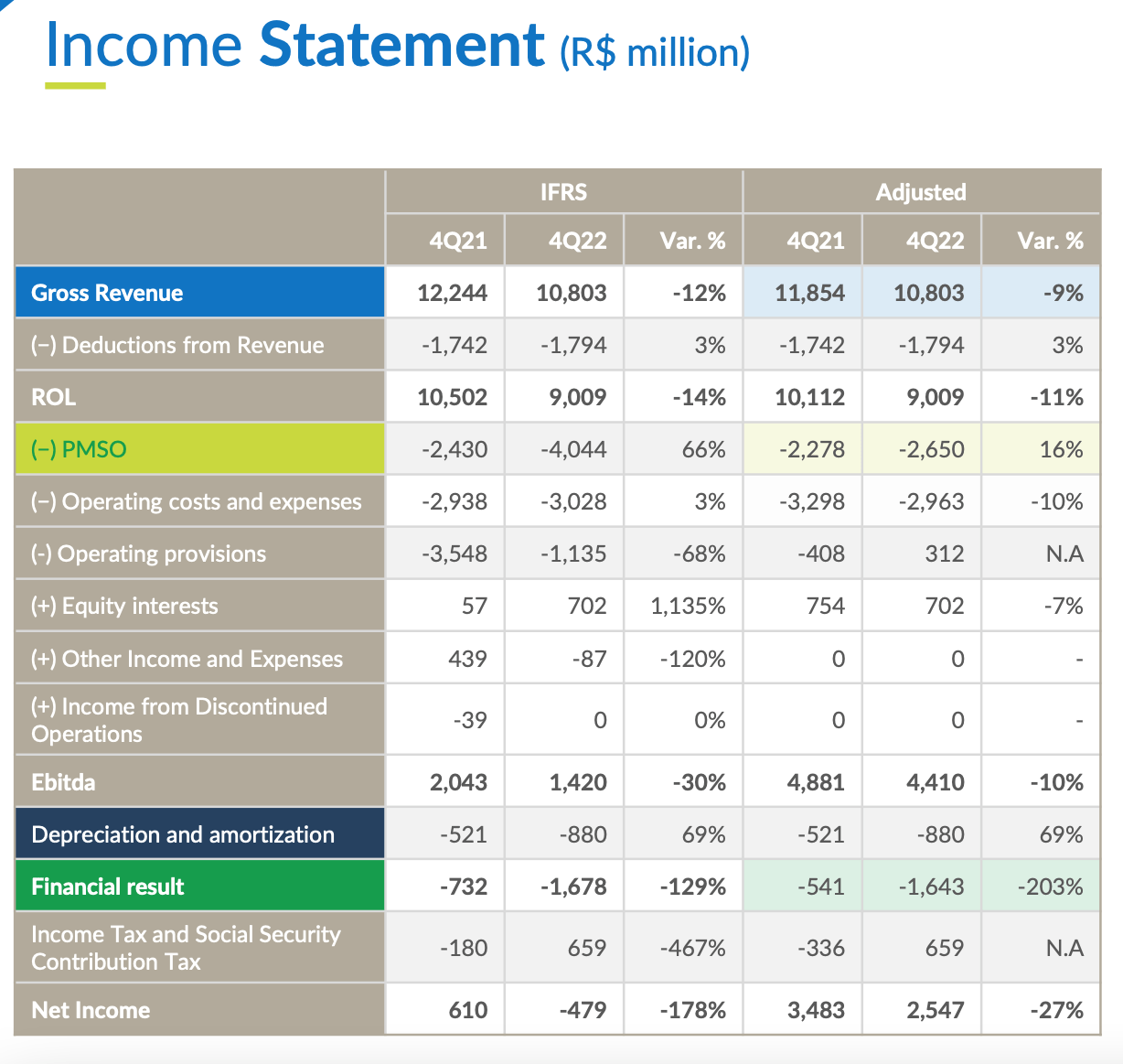

Since then, it has released its Q4 2022 and full-year 2022 results , earlier this month. And they are not any better. Its revenues, EBITDA and net profit declined in Q4 (see table below) and for the full year 2022, its revenues are flat, and its profits have dropped sharply. A number of reasons have led to this poor performance, particularly in Q4 2022.

{kind=link}

One is its Voluntary Dismissal Plan mean to streamline the number of employees on its rolls, which resulted in 2,500 employees signing up in December last year, leading to an expense of BRL1.3 billion (USD 255 million). The company also made provisions for debts owed. Further, it has incurred expenses as it consolidates the indebted SPE Santo Antônio Energia [SAESA], a hydropower plant operator, in which it has a 70% stake. In fact, the SAESA buyout also impacted its Q3 numbers. Eletrobras also points to a reduction in transmission revenues on account of deflation in the country during 2022 as a reason for weaker financials.

Consider the positives

While a weak result is of course no good news for the EBR stock and ADRs, the fact remains that at least some of these costs will not follow it into 2023, like those for the dismissal plan, which was a one-time expense. If just this cost were not there, the company’s net profits would have declined by a much smaller 14% compared to the present 36%.

Further, inflation in Brazil is expected to be higher in 2023, which should also hold its transmission revenues in good stead considering recent tariff revisions. Inflation has already returned to the economy. The acquisition of SAESA could also be a positive down the line as well, though for now, it remains a drag. The only costs that are outright negative are the provisions for loan losses, especially since they have risen significantly by 5x from 2021 to BRL 5 billion (USD 980 million) in 2022.

{kind=link}

Positive forward market multiple

For now though, with declining earnings, its trailing twelve months [TTM] price-to-earnings (P/E) ratio is at 27.9x compared to the 19.9x level for the utilities sector. However, analysts are clearly bullish on the company’s earnings in 2023, with its forward P/E far more attractive at 6.6x compared to the sector at 18.1x.

Persisting political risk

But the political risk to the company stays as real as it did last November. At the time it was privatised in June last year, the now president, Lula, was opposed to it and had even called it a “ crime against the homeland ”. The company, on its part, has measures in place to disincentivise Eletrobras from getting nationalised again.

For any shareholder gaining a controlling stake in the company, a 200% premium needs to be paid. This significantly reduces the chance of any potential buyer’s ability to make gains in any hurry. It also reduces the risk of a government takeover. It also has a 10% voting rights restriction, no matter what the size of the shareholding might be, significantly diluting the purpose of a controlling stake. But that has not stopped speculation of the government’s interference with the company through other means like taxation.

It is no coincidence that the Brazilian stock markets have responded poorly to these election results. The BOVESPA is down by 11% since Lula’s victory. By comparison, the S&P 500 is up by 4% over the same time.

What next?

So, in sum, we have here a company with the potential for a great future. It is a green energy giant, that can do exceptionally well at a time when there is a pressing need to lower carbon emissions and reduce dependence on fossil fuels. But this potential can only be realised in the right environment. At present, there is a political risk to it. Even if the risk does not materialise, the sentimental damage itself can be enough to keep the stock underperforming. And indeed this is visible from the performance of Brazil’s headline stock market index.

It does not help that its recent results have been poor. Possible loan losses and the acquisition of the highly indebted SAESA are a drag on its financials. But there are positives too. Like the possible gains from SAESA when the debt is paid off. Or the improvement in transmission revenues, as the outlook for Brazil’s inflation in 2022 is improved. Analysts too are positive about its earnings in 2023, making its forward P/E quite attractive.

But I am not yet convinced. Also, its price gains of 3.9% over the past five years are underwhelming. At the very least, I would like to wait for another set of results for improvement in its performance. I retain my Hold rating on Eletrobras.

For further details see:

Eletrobras: Still Risky