OPRT - Elevate Credit: High-Probability Merger Arb

Summary

- Definitive merger arb offering 19% annualized returns.

- Online-based subprime lender Elevate Credit is getting taken private by one of its creditors at $1.87/share.

- I expect ELVT’s shareholders to approve the merger given consideration’s large premium, fair valuation of the target as well as the company’s worsening operational performance.

This is a definitive merger arb with a high probability of successful closing. The spread is quite tight, however, given expected closing within this quarter the IRR might be substantial. Meanwhile, the downside might be protected by previous acquisition interests by other third parties.

Online-based subprime lender Elevate Credit ( ELVT ) is getting acquired by alternative debt-focused asset manager Park Cities Asset Management in a $67m transaction. Transaction consideration is $1.87/share in cash. Merger spread used to stand at minimal levels upon the announcement only to widen to around 6% since mid-December despite no transaction-related news. The spread has slightly contracted and now stands at 4%. Having said that, this spread translates to 19% annualized returns assuming merger closing in Q1'23 which is in line with the company's estimates.

{kind=link}

The merger will require regulatory approvals and a nod from ELVT's shareholders. While approval from regulators is likely a formality given tiny transaction size, shareholder approval is also unlikely to be an issue. ELVT's management owns 10% of the company, 7% of which is expected to be rolled over into the acquiring entity. I expect the remaining shareholders to likewise support the transaction:

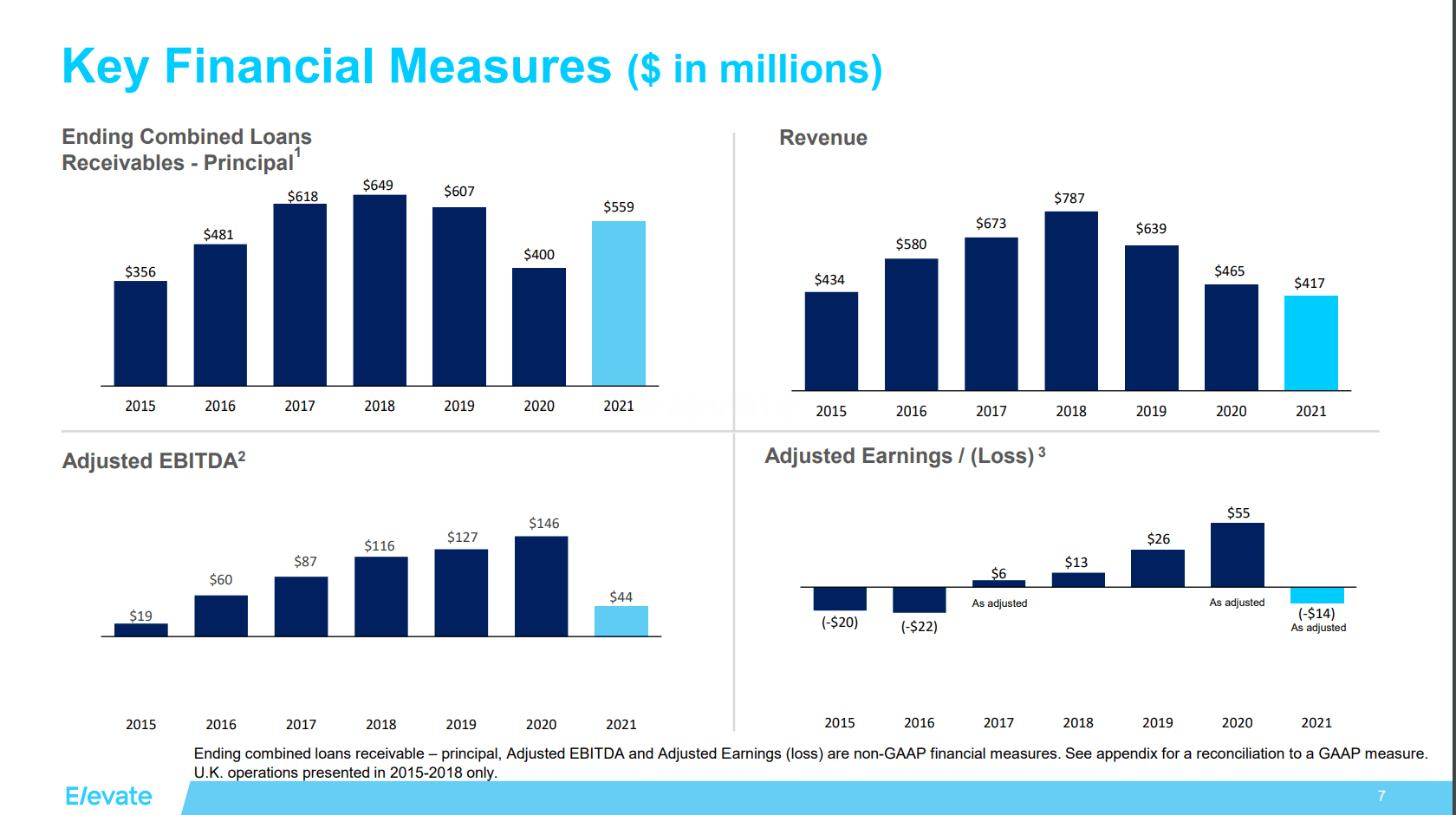

- Given macroeconomic headwinds and potential upcoming refinancing at much higher rates, the merger seems to make sense for the target company. The acquisition offer comes in light of ELVT's deteriorating operational performance in recent years amid a series of broader macroeconomic headwinds. Firstly, the COVID-induced stimulus payments in 2020 and 2021 as well as eased monetary policy have significantly reduced credit demand from credit-constrained customers. Not surprisingly, ELVT's combined loans receivables, revenue, and adjusted EBITDA all declined substantially in 2020-2021 compared to 2017-2019 levels. Secondly, the business has been impacted by significant macroeconomic headwinds since last year, including severe inflation. This has forced the company to tighten new loan underwritings as well as led to increasing charge-offs on previously issued loans. For reference, new customer growth rate was lower by 60% YoY as of Q3'22, meanwhile, TTM revenues and EBITDA have both stood materially below historical levels at $497m and $23m respectively. Lower loan volumes are complemented by borrowing/liquidity issues the company might be likely to face. While the majority of ELVT's debt has a fixed interest rate, the company's management has highlighted that most of the debt matures in Jan'24 ($519m out of $562m in total debt).

Elevate Credit Q4'21 Investor Presentation.

{kind=link}

- The merger seems to value the target quite fairly. At the offer price, ELVT fetches 0.35x P/B (5% EBITDA margins) - in line with where a similar-size ($184m market cap) and -margin peer Oportun Financial (NASDAQ: OPRT ) is currently trading. Larger online-based subprime lenders trade at much higher multiples, including Curo Group (NYSE: CURO ) and Enova International (NYSE: ENVA ) - both trade at 1.1x-1.2x. However, these competitors have maintained much stronger post-COVID operational performance while boasting higher TTM EBITDA margins (14% for CURO and 26% for ENVA). Another data point is Enova's acquisition of On Deck Capital in Jul'20 in a transaction that valued the target at 0.4x P/B.

- Park Cities' offer comes at a 69% premium to unaffected share price levels. While ELVT is still valued significantly below share price levels seen prior to mid-2022, shareholders might not oppose an acquisition proposal at such a sizable premium.

The risk of the buyer walking seems quite low here. Despite recent slowdown, it seems that ELVT's performance going forward might materially improve given significant growth runway. ELVT is an online-based loan provider in an industry which has seen decreasing yet still sizable market share of legacy physical-based competitors, such as Check Into Cash and Advance America (also referred to as payday loan providers). For reference, ELVT's larger competitor ENVA currently has only 1-2% market shares in the US subprime ($30bn TAM) and near-prime ($28bn) consumer loan markets. Another important aspect is that ELVT's management expects a recessionary environment to eventually increase demand for the company's products given tightening of credit supply from prime lenders. From ELVT's CEO during Q2'22 earnings call :

What we saw historically in recessionary-like times is prime lenders are seeing to tighten up fast and loosen up slow. And so that makes higher credit quality consumers down into the space where we operate and the banks we work with operate. So it creates a unique opportunity. We see a little bit higher credit quality consumers come in the space that we can work with and lend to. And just recently, if we look at our FICO score distributions of applicants coming to the door, we are starting to see that already. So I think it gives us the opportunity to take a very broad market already and see that somewhat expand as more prime consumers are squeezed out of the prime market into our market.

Park Cities Asset Management (PCAM) is an alternative credit manager focusing on private lending across specialty finance and fintech sectors. PCAM has provided two debt financing facilities for ELVT - for corporate purposes and for one of the company's credit products - since Oct'21. Notably, Park Cities was interested in acquiring the company during 2019-2020, albeit PCAM did not make any proposal back then. Nevertheless, it appears that PCAM is familiar with the Elevate business' dynamics and is now able to acquire it at an opportunistic time.

Interestingly, prior to agreeing to a buyout by Park Cities, ELVT attracted buyout interest from numerous other potential acquirers. Merger proxy mentions contact with 15 third parties by Sep'22, with five of them entering into confidentiality agreements. Most notably, just a couple of weeks before the current definitive merger agreement in Nov'22, an undisclosed strategic player ("Party B") submitted a proposal valuing the target at $1.81/share (70% in cash/30% in stock). This suggests that in the unlikely case of the current deal breaking, there would be a non-zero probability of this party as well as other potential acquirers stepping in.

It is worth noting that the setup is not risk-free by any means. There is a possibility of the macroeconomic environment worsening significantly, thus pushing PCAM out of the deal. Moreover, an economic recession could put off any other potential acquirers if the current buyer PCAM were to walk away. The downside to pre-announcement levels is sizable at 41%. Meanwhile, share prices of ELVT's peers have fluctuated since the merger announcement, including ENVA (+4%), CURO (+23%) and OPRT (-14%). Assuming ELVT's share price would move in line with OPRT's, the downside would stand at 49%. Therefore, while I consider a deal break scenario unlikely, investors should size their positions appropriately and, if needed, purchase put options here.

Business

Elevate Credit provides online credit solutions for credit-constrained customers, with more than $10bn in loans originated to date. ELVT's main products include installment loans, lines of credit and credit cards. In addition to operating as a state-licensed lender, the company is also a service provider to FDIC-regulated banks whereby ELVT licenses its technology platform as well as credit/fraud scoring models to other banks.

In response to macroeconomic headwinds, the company initiated a number of measures, including furloughs (25% of the workforce in Q3'22) and other cost savings initiatives as well as reduction in loan originations.

Worth noting that ELVT has repurchased $53m worth of the company's stock (more than 30% of outstanding shares) since 2020.

Conclusion

ELVT presents an interesting short-term merger arb opportunity. The merger is highly likely to be approved by ELVT's shareholders whereas the buyer PCAM does not seem likely to walk away from the deal. Given expected closing in Q1'23, the situation currently offers a 19% annualized return for event-driven investors. Having said that, the potential downside is significant here and investors should thus size their positions appropriately.

For further details see:

Elevate Credit: High-Probability Merger Arb