NONOF - Eli Lilly: Does 'Miracle' Weight Loss Franchise Justify Rising Price Tag?

2023-07-24 15:08:24 ET

Summary

- Eli Lilly and Company's share price won't stop climbing on the promise of its "miracle" diabetes and weight loss drug, Tirzepatide, and franchise.

- The share price is +25% so far this year, and +425% over a 5-year period. Lilly is now the world's most valuable Pharma.

- Tirzepatide may win its approval in weight loss this year, where it will take on Novo Nordisk's wildly successful Wegovy.

- There is a very good chance tirzepatide will become the best-selling drug of all time globally. The market opportunity is practically unheard of.

- There are still plenty of obstacles to overcome however - in this post I run readers through the potential pitfalls of tirzepatide and calculate a target price using forward revenue projections and DCF.

Investment Overview

Just over 6 weeks ago, in a post for Seeking Alpha , I discussed how Eli Lilly and Company ( LLY ) had assumed the mantle of being the world's most valuable pharmaceutical company, despite being nowhere near the biggest revenue driver, and far from the most profitable.

Pfizer ( PFE ), for example, earned nearly >3.5x more revenue than Lilly in 2022 - $100bn, to Lilly's $28.5bn - yet its market cap valuation is $205bn, which is less than half Lilly's valuation of $440bn.

Johnson & Johnson ( JNJ ), the company Lilly briefly replaced at the top of the valuation table, earned net income of $17.9bn last year - nearly 3x more than Lilly. Lilly's dividend yield of <1% is the lowest in the Big Pharma sector - the average payout yielding ~3%.

As I discussed in my last note however, Big Pharma valuations are rarely based on actual performance today, but perceived performance tomorrow. Indianapolis-headquartered Lilly is thought to have developed - in the form of its Glucagon-like Peptide-1 ("GLP-1") receptor agonist pipeline - a diabetes and weight loss franchise with the potential to deliver the industry's all-time biggest selling drug.

Tirzepatide is already approved by the FDA to treat Type 2 diabetes, under the brand name Mounjaro. It is expected to be approved to treat weight loss/obesity before the end of the year in both the U.S. and Europe, after results from the drug's Phase 3 SURMOUNT-2 study revealed the drug achieved an average 15% weight loss in adults, versus 3.2% achieved by patients taking a placebo.

I explained in my last note that, as large a market as Type 2 diabetes is - ~37m people in the U.S. alone are diagnosed with the condition in the US, and Lilly's list price for Tirzepatide is estimated to be ~$13k, creating a theoretical market opportunity of ~$450bn - the weight loss market is far larger. According to the World Health Organisation ("WHO"), 650m people globally are obese, and 1.6bn people are overweight.

In short, the potential of Tirzepatide - a drug that works by binding to both the GLP-1 and GIP receptors, responsible for controlling your appetite, and literally making patients feel more full - is mind-boggling. And it is not just Tirzepatide that Lilly is working on - there are 2 other drugs in the company's pipeline that could be as effective, or perhaps even more effective.

Retatrutide, nicknamed "Triple G" because it combines glucagon receptor agonism with GIP and GLP-1 receptor agonism, recently achieved 17.5% mean weight reduction in a Phase 2 study of >330 patients, meeting all primary and secondary endpoints, whilst orforglipron, a once-daily oral nonpeptide GLP-1 receptor agonist (tirzepatide and retatrutide are self-injectable therapies), has achieved 14.7% weight reduction at 36 weeks in overweight or obese adults in its own Phase 2 study.

These are momentous data readouts - better than anything that has come before, with the possible exception of Novo Nordisk's semaglutide - already approved in Type 2 Diabetes ("T2D") as Ozempic, and in weight loss as Wegovy. Ozempic drove ~$8.6bn of revenues in 2022, and the demand for Wegovy has been so great, there is currently a global shortage of the higher dose formulation.

Both Lilly and Novo Nordisk stock has bucked the trend of underperformance by large Pharma companies in 2023 - Lilly's share price is up by 44% so far this year, and by >420% across the past 5 years. Novo Nordisk stock is up by 21% so far this year, and by >230% over 5 years.

Conservative estimates around tirzepatide sales suggest the drug could achieve peak sales of ~$25bn per annum in T2D alone - Lilly itself hasn't volunteered a figure, but management has pointed out that obesity-related complications and comorbidities cost the US government upwards of $1 trillion per annum. My own personal belief is that the franchise could drive revenues per annum >$80bn.

As such, it is not hard to understand why Lilly's share price has been soaring. Equally, it is not surprising to see people questioning whether a $440bn market cap valuation - which implies a price to earnings ratio based on 2022 earnings ratio of >70x - at least twice as high as the next Pharma - and price to sales ratio of 14x - at least 3 times as high as the next pharma - is going too far.

Is Lilly's Soaring Valuation Justified? Let's Start With Donanemab

Tirzepatide is undoubtedly one of the most-hyped drugs in recent memory. Its potential is so significant, it has even cast a shadow over another breakthrough drug that Lilly has just released pivotal trial data for.

That drug is donanemab, Lilly's Alzheimer's Disease ("AD") therapy. Last week, Lilly revealed the results from its Phase 3 TRAILBLAZER-ALZ 2 study, which showed, according to a press release:

Donanemab significantly slowed cognitive and functional decline for amyloid-positive early symptomatic Alzheimer's disease patients, lowering their risk of disease progression.

Additional subpopulation analyses presented live showed that those study participants at earliest stage of disease had even greater benefit, with 60% slowing of decline compared to placebo.

Donanemab attacks the clumps of amyloid beta protein that build up in the brains of Alzheimer's patients, and successfully removes them. When approving Biogen ( BIIB ) and partner Eisai's (ESALF) drug lecanemab (under the brand name Leqembi) which has a similar mechanism of action ("MoA"), the FDA made it clear that it considers removal of amyloid plaque to be a surrogate endpoint for AD drugs.

With donanemab also showing a clinical benefit in its pivotal study, the drug seems highly likely to be approved, even with a somewhat troubling safety profile. Cases of Amyloid-related imaging abnormalities ("ARIA"), a side effect of the drug that can cause nausea and dizziness, and in more serious cases, swelling of the brain ("oedema"), were experienced by 37% of patients in the donanemab arm of the study, versus 15% in the placebo arm. Overall death in the donanemab arm was 1.9%, versus 1.1% in the placebo arm.

The slowing of cognitive decline experienced by patients using donanemab - and lecanemab - has been hailed as a major breakthrough, although neither drug remotely resembles a cure for the disease, and it is even unclear if those caring for patients will be able to see any noticeable effect or improvement in patients.

Donanemab is an important drug and an important step forward in the battle against Alzheimer's, and it will likely be a major revenue driver for Lilly, perhaps even generating sales in the double-digit billions annually. But make no mistake, tirzepatide is the drug driving Lilly's share price higher and higher.

Talking Of Alzheimer's - Could Tirzepatide Flop On Safety Concerns, Like Biogen's Over-Hyped Aduhelm?

When Biogen's first AD drug Aduhelm was approved - controversially - by the FDA in June 2021, the company's share price leaped from ~$265, to ~$395 overnight - a gain of ~50%, which represented an increase of >$20bn in Biogen's market cap.

Some of the forecasts for that drug were almost as high as those quoted for tirzepatide - but Aduhelm was associated with adverse safety events, overpriced by its developers, at >$45k per annum, and failed to secure reimbursement from the Centers for Medicare and Medicaid Services ("CMS") outside of clinical trials, before being shelved altogether. Today. Biogen's share price trades at a similar price to the pre Aduhelm approval spike, even with the successful approval of lecanemab.

Is there any prospect of tirzepatide suffering a similar fate to Aduhelm?

Although the long-term effects of using tirzepatide have not been completely established, it does come with side-effects - gastrointestinal, cardiovascular, renal, dermatologic, hepatobiliary, ocular, endocrine and pancreatitis complications have all been reported in clinical trials - the available data suggests most side-effects are mild in nature.

The "miracle" T2D / weight loss drug appears to be safe for most patients to use, although Mounjaro does come with a boxed warning - as it has been found to cause dose-dependent and treatment-duration-dependent thyroid C-cell tumors in rats.

Arguably, the biggest safety issue to have come to light so far in relation to GLP-1 agonists involves customers who cannot gain access to Novo Nordisk's semaglutide turning to compounding pharmacies to buy ready-made compounds, which may well be risky. A cynic might also suggest it is very much in Lilly and Novo Nordisk's interests to prevent patients accessing their drugs via any other supplier.

One other concern could be related to mental health. The European Medicines Agency recently announced it is:

reviewing data on the risk of suicidal thoughts and thoughts of self-harm with medicines known as GLP-1 receptor agonists, including Ozempic (semaglutide), Saxenda (liraglutide) and Wegovy (semaglutide).

The review was triggered by the Icelandic medicines agency following reports of suicidal thoughts and self-injury in people using liraglutide and semaglutide medicines. So far authorities have retrieved and are analysing about 150 reports of possible cases of self-injury and suicidal thoughts.

This is an important dimension of safety that is difficult to judge as there has never before been a weight loss drug as effective as GLP-1 agonists appear to be. Sometimes referred to as the "Hollywood Drug," some high-profile figures have suggested that Novo Nordisk's Wegovy has not worked for them, whilst others have bought into the hype, with the likes of Elon Musk praising Wegovy use as integral to his own weight loss.

This has helped create massive global demand for semaglutide and caused a global shortage of the drug - and a moral headache. Celebrities singing the praises of these drugs could lead to a global sense of "FOMO" (fear of missing out) and damage the self-esteem of people whose mental health is linked to their weight.

Additionally, the use of semaglutide and tirzepatide off label to lose weight could result in there being not enough supply to treat diabetics, whose need is more urgent.

Can Lilly Create Enough Tirzepatide Product To Meet Demand?

In Q123, Novo Nordisk announced that sales of Ozempic were ~$2.9bn- up 46% year-on-year - and sales of Wegovy were $679m - up 225% year-on-year. Wegovy sales would likely have been much higher had it not been for supply shortages experienced by the company.

For Lilly's part, the company reported Mounjaro sales of $569m in Q123 - up from $279m in Q422 - a figure which set analysts pulses racing, given the drug was only approved in May 2022.

Speaking at a Goldman Sachs healthcare conference in June, Lilly's Chief Financial Officer ("CFO") Anat Ashkenazi revealed that the company had completed its regulatory submission for tirzepatide in weight loss, and thanks to a Priority Review Voucher ("PRV"), expected to receive an approval in this indication before the end of 2023.

Apparently, Mounjaro is already being prescribed off-label for weight loss, and as I discussed in more detail in my last note, tirzepatide, thanks to its dual action, which has earned it the nickname "twincretin" (incretins are hormones that augment the secretion of insulin), is tentatively expected to emerge as the superior alternative to semaglutide. Lilly itself is confident, and its SURMOUNT-5 study will directly compare the 2 drugs.

Analysts have forecast that Mounjaro alone will generate >$26bn in annual revenues by 2030, and with weight loss, as discussed, representing a far larger market, where demand has already outstripped supply, it is hard to put a number on the kinds of annual revenues tirzepatide could drum up in its second indication.

For good measure, the drug is also likely to be approved in non-alcoholic steatohepatitis, another "holy grail" indication in which no other drugs are approved, and revenues in the double-digit billions, if approved, are virtually guaranteed.

With all that said, Lilly can only sell whatever quantities it can produce, and management is desperate not to experience the shortages suffered by Novo Nordisk. Lilly is spending $1.7bn on a facility in North Carolina, Ashkenazi told the GS conference, but quickly realised that it would need more:

That facility is progressing well, and we should be launching out of that facility -- or not launching, selling out of that facility this year. So it's on track to what we said previously. But we knew that this was probably not going to be sufficient. It's a very large site with multiple lines. So we broke ground last year, mid last year.

On a second site in North Carolina in Concord, a couple of hours drive from the first site, equally large site as well, another over $1 billion investment, but we knew that's not going to be sufficient.

So we have three more sites we're starting. One is an API site in Ireland, which we just broke ground on. And I think you already know, we have large presence in Ireland. And then two new sites in Indianapolis, not all of them for the incretin portfolio, but we looked at the broader portfolio that we have. And we felt that we needed that capacity to be available. So almost $4 billion of investment in just North of Indianapolis for additional manufacturing capacity.

By my count that is 5 new sites dedicated to producing tirzepatide, which uses the same auto-injector pens as the rest of Lilly's diabetes franchise, e.g. Trulicity, Emgality. The total investment of ~$6bn into new manufacturing plants is peanuts compared to expected sales of tirzepatide, and allows Lilly to control production as opposed to using contract manufacturing organisations, the strategy that has not worked out so well for Novo.

For further comfort, Ashkenazi told the conference attendees that "whenever we see us launch in a market, you should feel confident we're going to be able to support that market", and also made the point that the company would not be using PRV - which can shorten the FDA's review period from e.g. 18 months, to just 6 - if it did not feel it could meet demand for tirzepatide in weight loss.

Reimbursement Issues

Although the above-mentioned Aduhelm and tirzepatide are 2 very different drugs, there is another element of the former's commercial failure that could also affect the latter.

In the U.S. today, the CMS does not provide reimbursement - i.e., the process by which low and middle income patients can access more expensive drugs, with CMS funding the majority of the cost - for any weight loss drugs. Mounjaro has a list price of ~$1k per month, likely meaning the majority of patients will need some form of reimbursement if Lilly charges the same for the obesity version of the drug.

One study has suggested that if 10% of people in the U.S. with obesity covered by Medicare were prescribed with "a brand name semaglutide," the cost would be in the region of $26.8bn. The author of the study told Beckerspayer.com:

When we look at outcomes relative to costs, in the short and long term, the price of semaglutide simply does not align at the moment with the added benefit over previous generation anti-obesity medications

Presumably, the same would also be true for tirzepatide, and tirzepatide will likely be a life-long treatment, making it potentially prohibitively expensive for not just the CMS, but private insurers also, who often look to the CMS when making their own reimbursement decisions.

Celebrities and higher-earners may not bat an eyelid at paying ~$12k per annum for a drug with proven weight loss capabilities, and if, for argument's sake, 5m people were to do so each year - ~1.5% of the U.S. population - the drug could still earn $60bn per annum for Lilly.

That figure may or may not be realistic, however, so doubtless Lilly will consider it vitally important to secure reimbursement. Big Pharma companies, it is well known, have very powerful lobbies, and last week a group of U.S. senators reintroduced a bill that will allow Medicare recipients to receive reimbursement for weight loss drugs - apparently, it is the seventh time the bill has been introduced since 2012.

Pharmas have a habit of eventually getting their way in such matters, although the government secured a notable victory last year with the introduction of the Inflation Reduction Act ("IRA") that gave it a say in drug pricing for the first time, and prevented Pharmas from raising drug prices faster than the rate of inflation. Unsurprisingly, several prominent pharmas have opted to sue the government as a result - although Lilly is not yet one of them.

Ultimately, the CMS decision on whether to reimburse for weight loss drugs could be worth as much as $25bn per annum to Lilly, if not more.

A Fairweather Discounted Cash Flow Valuation of Lilly's Business

As suggested when covering donanemab, above, Lilly has more to offer than its diabetes/weight loss franchise. Its oncology division drove $5.7bn of revenues last year, and 3 potential "blockbuster" drugs - i.e., capable of driving >$1bn revenues per annum - have recently been, or will be, added to the portfolio.

Those three are Retevmo, approved last year for metastatic solid tumors with a rearranged during transfection ((RET)) gene fusion, Pirtobrutinib, approved in January for relapsed or refractory mantle cell lymphoma ((MCL)), and Imlunestrant, a breast cancer therapy still in late stage clinical studies.

Neuroscience division revenues - $3.5bn in 2022, will likely grow substantially thanks to donanemab, and a second AD drug in development, remternetug, while the immunology division - 3.3bn of revenues in 2022 - will grow thanks to 2 new drugs, lebrikizumab, and mirikizumab, that could drive combined revenues >$6bn in time.

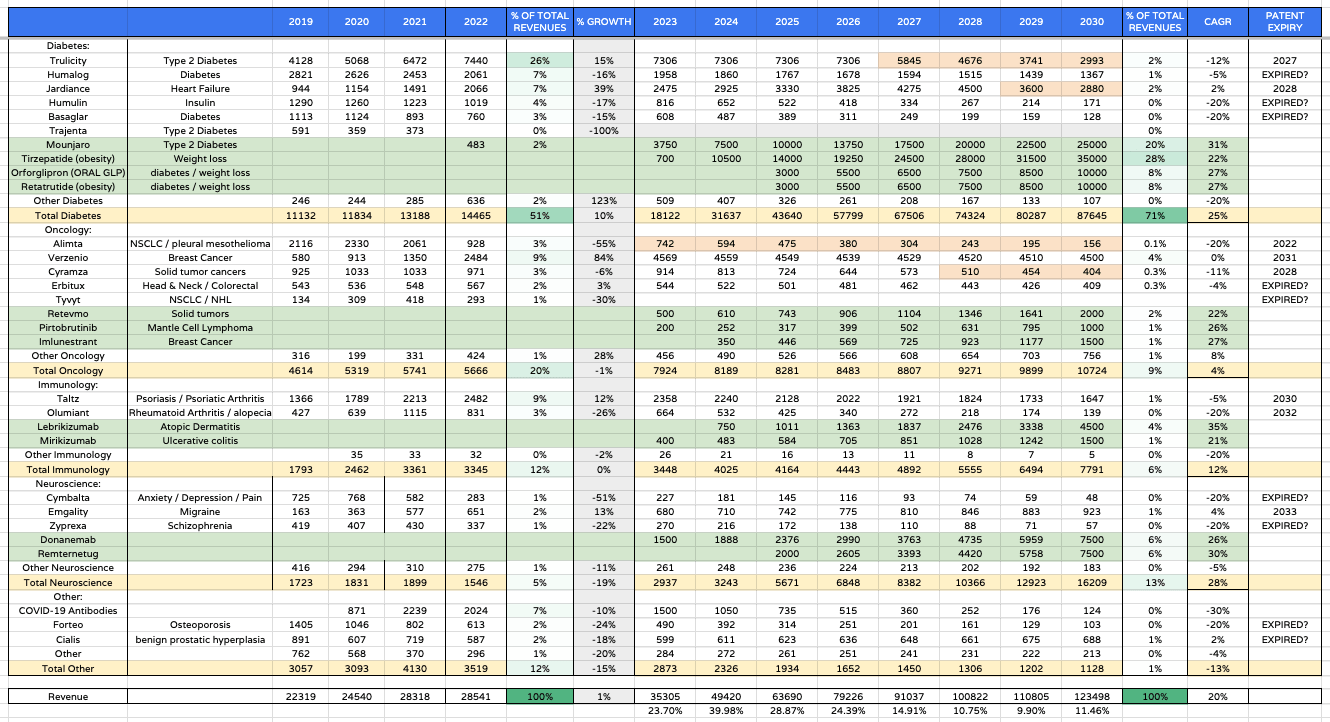

Lilly forward product revenues (my table and assumptions)

{kind=link}

In order to try to assess if Lilly stock is genuinely worth $465 per share - its current traded price - or more, or less, I created a table of product-by-product revenues forecasts as above.

This is an optimistic table in which peak GLP-1 franchise revenues in 2030 are $80bn, with the next generation drugs retatrutide and orforglipron approved and generating double-digit billion revenues.

By 2020 I also have the oncology division delivering revenues in the double-digit billions, and the neuroscience division >$16bn per annum. In this optimistic scenario Lilly's revenues in 2030 exceed $120bn, which would be a record for a Pharma. The compound annual growth rate for revenues is an almost unheard of (for such a large company in such a competitive industry) at 20%.

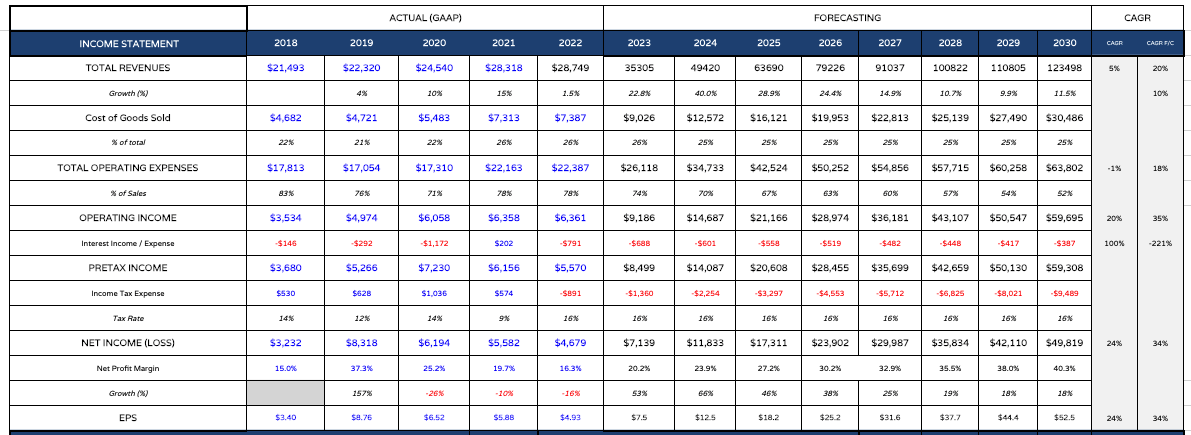

Lilly - forecast income statement (my table and assumptions)

{kind=link}

I take these revenue figures and plug them into a forecast income statement, as above. Note I also substantially reduce operating expenses as a percentage of revenues over time, to just over 50% by 2030, and also reduce interest expense - if these projections were accurate, Lilly may have generated >$200bn in cash by 2030 - an astonishing figure! In the above table, EPS reaches >$50 by 2030 - a forward price to earnings ratio of ~9x.

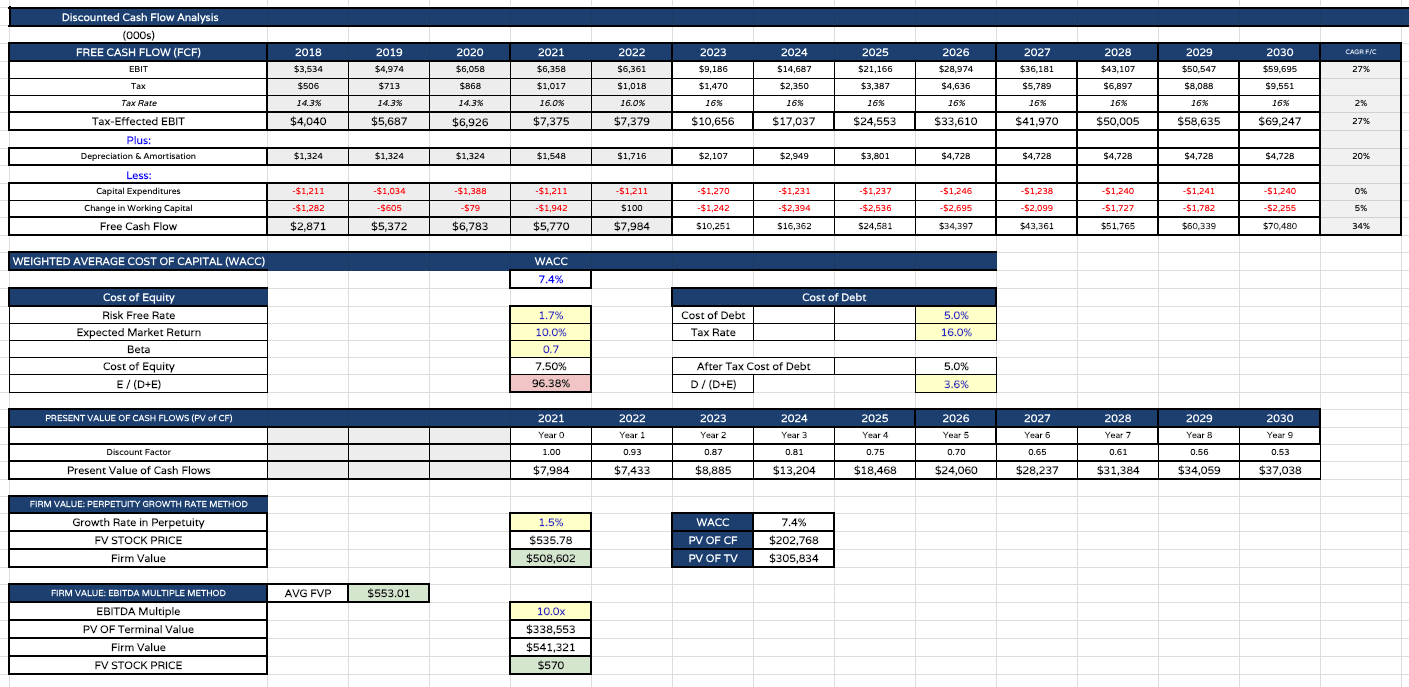

Lilly DCF price analysis (my table and assumptions)

{kind=link}

Finally, I present my discounted cash flow ("DCF") analysis and price targets - $535 per share based on the perpetuity growth rate method, and $570 based on the EBITDA multiple method.

Note the weighted average cost of capital is only 7.4%. I usually use a WACC of 10% when completing DCF analysis on large Pharmas, but I am reducing Lilly's beta, anticipating the company outperforming even while economic conditions are harsh and providing industry-wide headwinds, and the expected market return, for the same reasons.

My final price target - in this optimistic scenario - is the average of the 2 calculations - or $553 per share.

Concluding Thoughts - Over-Hyped, or Under-Valued? The Jury Remains In Session - But The Bull Case Can Still Be Made

Lilly, and Novo Nordisk (NVO), exist in a parallel universe to the rest of the Big Pharma industry at the present time, their share prices climbing while the others fall, and make no mistake, this is entirely down to their diabetes/weight loss franchises, and more specifically, semaglutide and tirzepatide - 2 products the market believes are nothing short of revolutionary. But is the market right?

In this note I have highlighted some practical issues that must be overcome in order for Lilly to justify its current sky high valuation and status as the world's biggest Pharma by market cap.

Secure an approval for tirzepatide in weight loss. Ensure there is sufficient supply to meet demand. Ensure the long-term safety profile is proven and address issues around off-label use and mental health implications of using the drug. Secure reimbursement for weight loss from CMS.

A final important point to consider is patent protection - how long can Lilly reasonably expect to have exclusivity in these markets? It could be 10-15 years, and after that, the weight loss empire would crumble under the weight of generic competition, with franchise revenues likely falling at >25% per annum.

As mentioned in my intro, with many hurdles to be overcome, it is not surprising there is bearish sentiment on Lilly and disbelief that the company warrants its current valuation. Take away tirzepatide, and Lilly's valuation likely falls by 50% or more overnight, just as Biogen's did with Aduhelm.

Bulls, on the other hand, have every reason to believe Lilly's share price can climb even higher, based on an objective assessment of the market opportunity. My price target implies Lilly's share price may be as much as 15% undervalued.

The implications of a successful, safe, weight loss drug addressing a market of ~2bn people worldwide are mind-boggling, to the extent that Lilly becoming the first ever $1 trillion dollar market cap pharmaceutical company does not even seem too outlandish.

There are plenty of reasons why we will never see such a high valuation, as discussed, but I personally believe Lilly is capable of getting over half way there, and quite likely beyond $600bn, although it may not stay there for long, with so many "unknowns - known and unknown" - in play.

For further details see:

Eli Lilly: Does 'Miracle' Weight Loss Franchise Justify Rising Price Tag?