THQQF - Embracer Group: Forging An Ecosystem Of Gaming Products

2023-04-08 06:18:28 ET

Summary

- Embracer Group invested and spent massively on acquisition sprees with the ambition of establishing an effective ecosystem of gaming products.

- This ambition is costly and the company has accumulated a massive amount of debt in pursuit of such ambitions.

- The company is still able to handle its debt servicing obligation and is cash rich, meaning the ambition of creating such an ecosystem appears to be still on track for now.

Investment Thesis

Embracer Group AB (THQQF) is operating with a primary strategy of massively acquiring other smaller gaming companies and assets with the end object of establishing an effective ecosystem of gaming products. Such a strategy is ambitious and forward looking but in terms of execution, the chances of succeeding at a global level are not overwhelming for a relatively small company like THQQF.

The company is accumulating a large amount of long-term debt. While the company is still able to handle the debt servicing obligations in the near-term, it's long-term capability to pay off all these debts eventually is questionable.

In spite of having a loss making the bottom line in the latest financial year, the company is still rich in free cash flow which may help to mitigate some of the risk associated with its high debt volume.

Company Overview

Embracer Group AB serves as the parent company for a collection of businesses helmed by entrepreneurial leaders who specialize in developing games for PC, console, mobile, board games, and other related media. The company boasts a vast collection of over 850 franchises that are either owned or controlled.

With a global presence, the company operates through 12 operative groups, including THQ Nordic, Plaion, Coffee Stain, Amplifier Game Invest, Saber, DECA Games, Gearbox Entertainment, Easybrain, Asmodee, Dark Horse, Freemode and Crystal Dynamics.

In addition, Embracer Group owns approximately 135 game development studios.

Income Statement Analysis

Income statement from Seeking Alpha :

{kind=link}

Generally, THQQF enjoyed a consistently rising revenue trend since 2013. The cost of revenue has been kept low such that the trend of rising top line trickled down to its gross profit.

Its operating income was also rising consistently until 2022 and the latest TTM period, which saw the company's bottom line dipping into the negative territory for the first time. Notably, the negative operating profits are caused by the 2 massive cost items of Selling General & Admin Expenses ("S&M") and Depreciation & Amortization ("D&M").

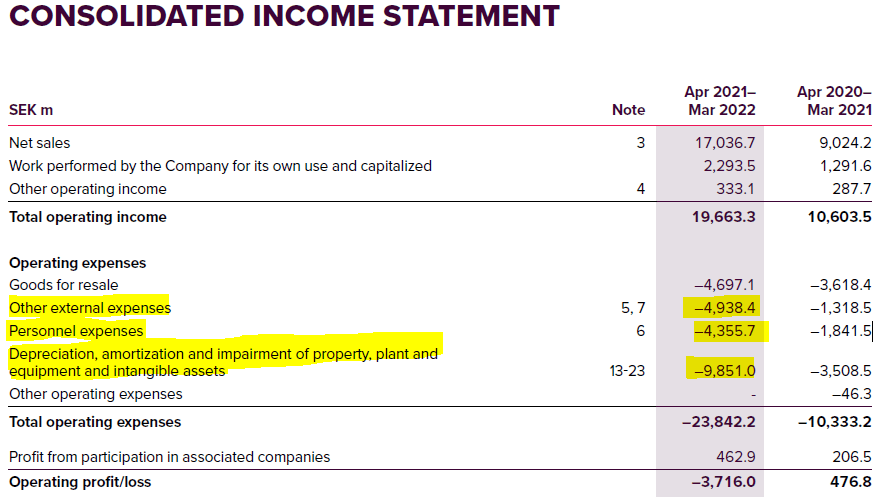

If we infer from the company's 2022 annual report , we understand the greatest increase in expenses comes from hiring (personnel expenses), the purchase of assets (property, plant, equipment, etc), and "other external" expenses:

{kind=link}

Going into the details, we understand the company spent a large amount on acquisitions of other companies. With a larger workforce from the new companies, personnel expenses increase in tandem. Amortization and depreciation of the acquired assets, including additional S&M costs required to strengthen the capabilities to monetize these assets under a new company also contributed to the operating costs:

Net Sales and Earnings (Company website)

In summary, the company's strategy right now appears to be massively acquiring new companies and their assets with the aim of building an "ecosystem" (as mentioned in the annual report).

{kind=link}

A successful ecosystem of entertainment products can create a very strong network effect which is very good for the growth of THQQF. In another article , I described how a Chinese gaming company might be able to do that as well. However, in my opinion, despite the appealing upside potential, the probability of success in creating such an ecosystem is relatively rare and only successfully executed by a handful of bigger companies.

Investors should ask themselves whether THQQF has what it takes to become one of just a few companies to create a successful ecosystem to benefit massively from the network effect.

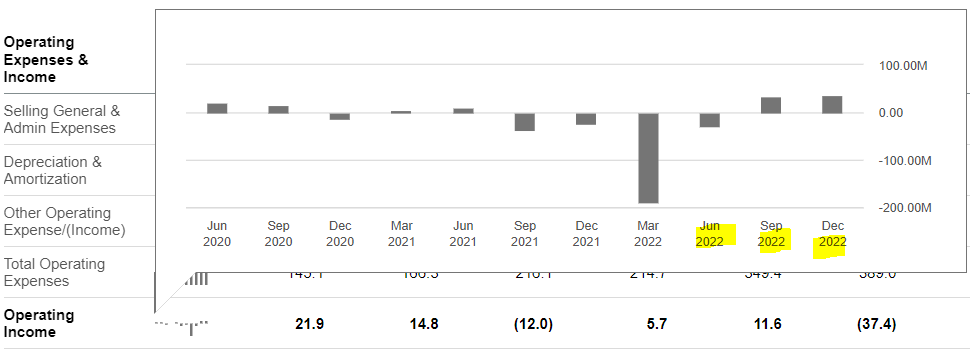

In spite of my skepticism, I am encouraged by the observation that in the last 3 quarters, the bottom line of THQQF appears to have improved remarkably. The operating losses appear to be largely under control, and THQQF has returned to profitability for the last 2 quarters.

{kind=link}

Investors should observe whether these quarterly profits are sustainable enough to produce a profitable annual profit in 2023 and remain profitable in subsequent years.

Balance Sheet Analysis

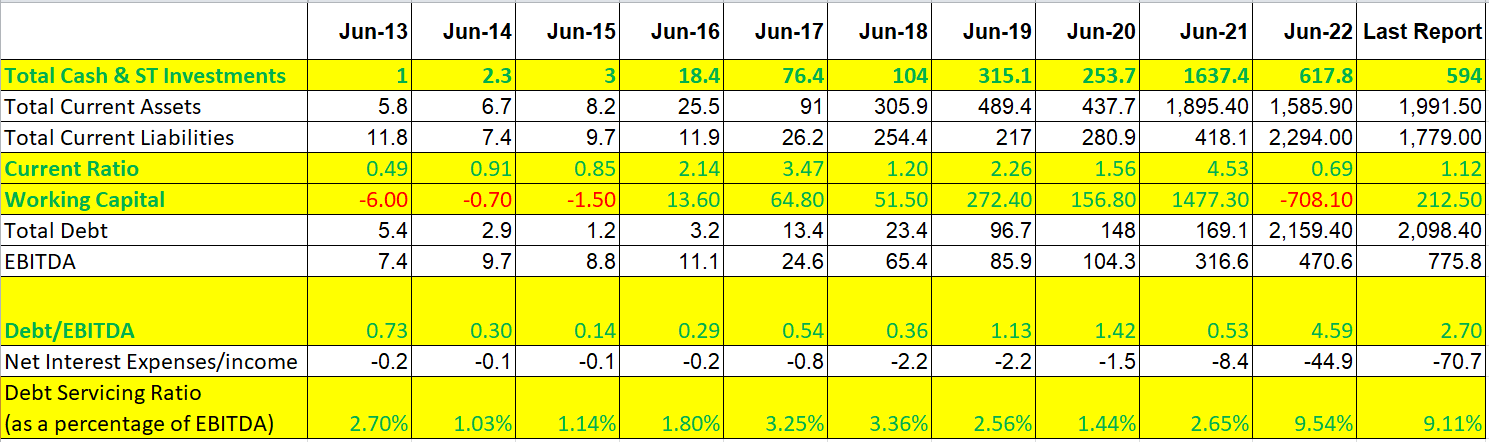

Let's move on to the company's balance sheet :

{kind=link}

Here are some observations:

- The company has had a healthy and progressive accumulation of cash on the balance sheet since 2013.

- The working capital has been positive since 2016 and remains so only until 2021.

- The latest year of 2022 saw the company accumulating an enormous level of debt, resulting in an overall working capital falling into the negative territory for the first time since 2015.

- If we put the debt volume into perspective, it is more than 4 times its EBITDA. In my opinion, a debt/EBITDA ratio of more than 3 is considered unhealthy.

- The silver lining is that while incurring a huge amount of debt, THQQF has always been able to comfortably service the interest incurred on its debt for the last decade. The amount of interest expense incurred is consistently lower than 10% of its EBITDA. In my opinion, a value that is lower than 30% is considered low and sustainable.

The main issue with the company's balance is the company's huge accumulation of liabilities which currently sits at about $708M more than its total current assets. This is largely contributed by the debt line items on the balance sheet.

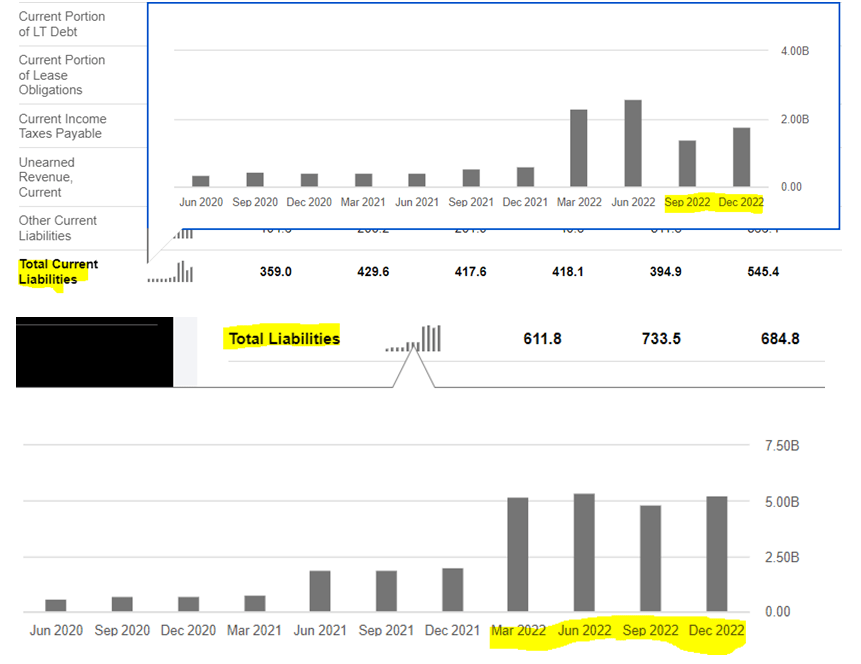

From a quarterly perspective, while it is encouraging to note that the short-term "current liabilities" has decreased significantly, investors should note that the "total liabilities" (including long-term liabilities) of the company remain high:

{kind=link}

From the annual report, we understand that this is due to the company refinancing its short term debt and converting it into long-term ones:

Annual Report (Company Website)

THQQF's debt has to be paid off "eventually". For now, the company decided to kick the can down the road. Investors should ask themselves: Is the company capable of repaying these debts eventually ?

As mentioned in the previous section, the capital raised from these debts is mostly used in acquiring revenue-generating companies and other assets. They are not used for paying off recurring operating expenses. Hence, if the investment in these acquisition sprees paid off, leading to greatly improved bottom-line margins in the long run, it is possible that the company is still able to pay off these debts eventually.

Cash Flow Analysis

Let's move on to the company's cash flow statement .

{kind=link}

Here are some observations:

- Earlier, we discussed the company's accounting losses are primarily due to "D&A" and "S&M". Hence when the non-cash item of D&A is added back into its operating cash flow, THQQF is observed to be very cash rich.

- The CAPEX of the company is increasing but the amount is still small compared to its operating cash flow, resulting in an overall very positive FCF.

- The FCF has been increasing by double-digits in percentages almost every year. On average, since 2014, the CAGR is about 100%.

Although the company is currently loss-making in accounting terms, the cash-rich profile of THQQF suggests the company is still managing its cash flow effectively.

Valuation

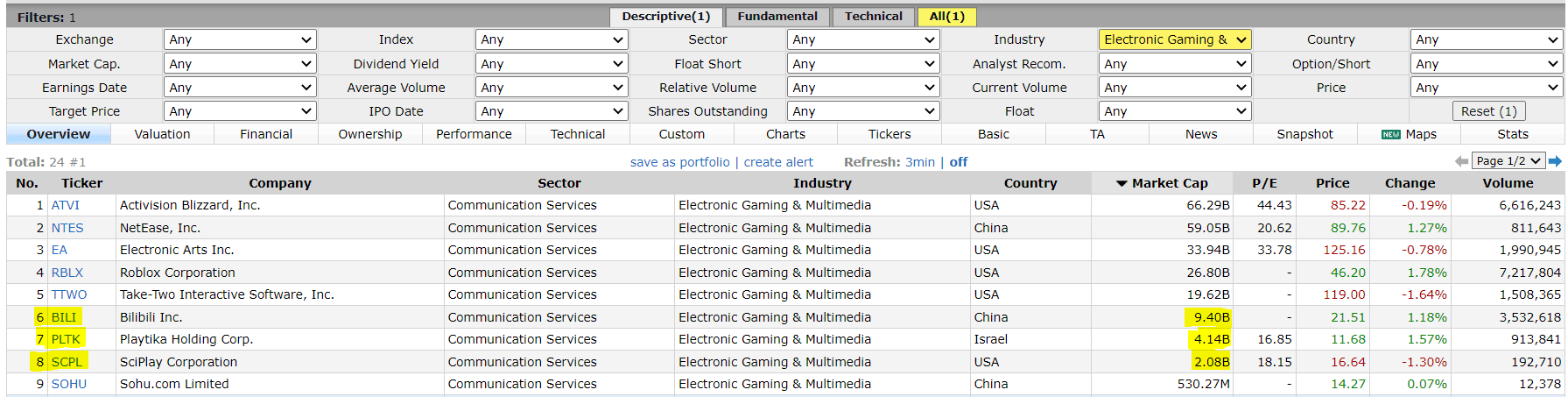

According to Seeking Alpha , the market cap of THQQF is currently $5.46B (in USD). From Finviz , the below highlighted 3 gaming companies have a similar market cap.

{kind=link}

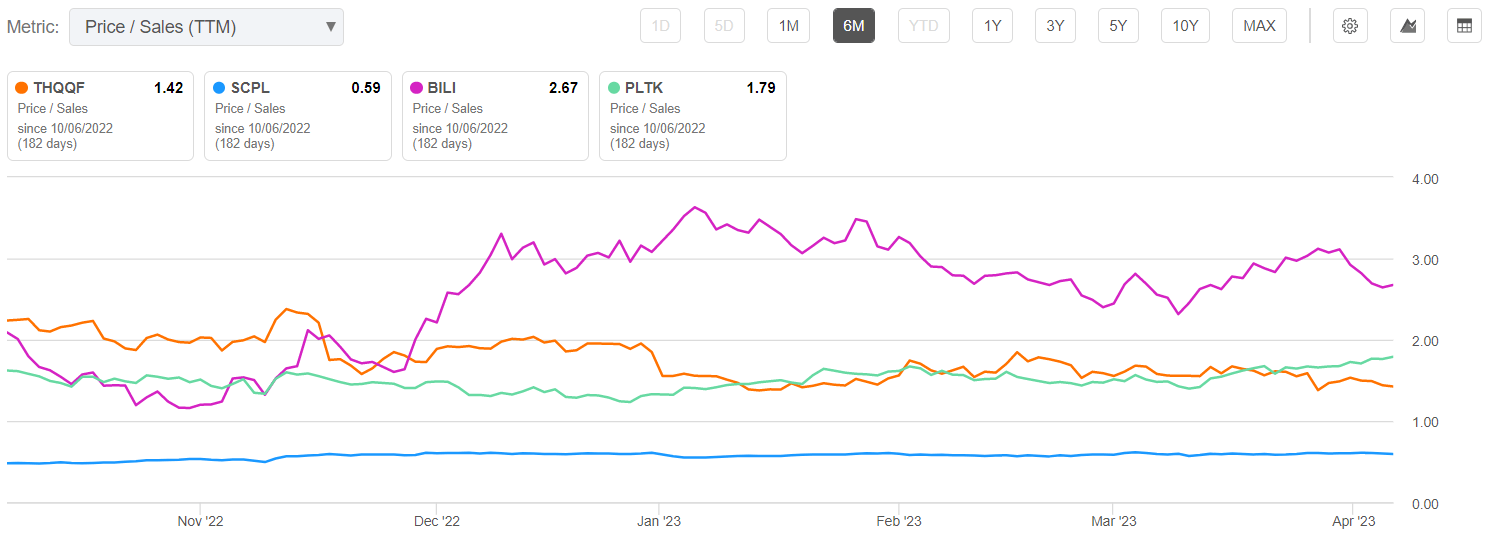

We will compare THQQF's valuation with these peer companies. Since the company is still loss-making at the bottom line, we will compare using the Price/Sales ("P/S") ratio:

{kind=link}

From the graph, we can observe:

- The P/S value fluctuates in a range between 0.5 and 3.0

- SCPL is the most undervalued on the comparison list with a P/S of 0.59, which is near the bottom fluctuating range.

- THQQF, with a P/S of 1.42, appears to be fairly valued (residing in the middle of the P/S range).

The company may be fairly valued with respect to the peers in the comparison list but it is actually a relatively small company in the overall gaming industry. From Finviz, we can observe that THQQF is nowhere near the size of the top 5 players by market cap.

As such, investors should demand a higher margin of safety which means I will not regard this current fair value as a buy signal.

Risk

THQQF has invested tremendous resources to embark on a massive acquisition spree, resulting in the accumulation of a huge amount of long-term debt. This risk is mitigated by the observation that the company's debt servicing obligations are still manageable when compared to its EBITDA.

Investors should observe whether the debt profile gets out of control in the long run.

Conclusion

The company is currently loss-making in accounting bottom line and sustains a huge amount of liabilities which are largely contributed by its debt volume stated in the balance sheet.

However, we noted that it is still generating cash on a consistent basis, and the debt servicing obligations are still manageable.

Despite acknowledging that the balance sheet is experiencing strain, we hold the belief that the situation is reparable and can be improved, especially if the long-term ambition of creating a gaming ecosystem of products is materialized. This is after considering that the capital used is channeled toward forward-looking acquisitions that have the upside potential to greatly improve the company's bottom-line performance in the long run.

Still, the high debt profile of THQQF presents a relatively significant risk that should not be ignored. Investors should take this into consideration when deciding whether to invest in THQQF.

For further details see:

Embracer Group: Forging An Ecosystem Of Gaming Products