UBSFF - Embracer Group: Why This Great Company Remains Highly Attractive

2023-08-20 21:14:33 ET

Summary

- Embracer's share price significantly declined following a softening of demand and the collapse of a material several-year partnership.

- Following this, the business has begun a transformation exercise, seeking to achieve efficiency through operational improvement. We believe the scope for gains in margin is high.

- Embracer acquired the Lord of the Rings IP for an attractive price, with markets seemingly distracted by an overarching period of difficulty for the business.

- Embracer remains highly attractive, with a strong catalog of titles, a healthy pipeline, and deep expertise. The gaming industry is also lucrative due to its addictive nature and scope for monetization.

- Embracer is trading at an 80% discount to its peers and over 100% to its historical average. Further, its FCF yield currently sits at 8%. We believe the company is oversold.

Prior and current thesis

We previously covered Embracer Group (THQQF) in Apr-22, stating "Embracer has been quietly acquiring small studios and developers as a means of growing. Management has been extremely successful at incorporating these businesses, and currently has a large pipeline of games under development.

I believe that the fundamentals of this business are extremely strong, with substantial cash flow growth ahead. This will allow the business to grow its bottom line further while also buying back shares. Currently, its stock seems markedly undervalued relative to the growth ahead and so presents an opportunity to generate alpha."

The company has faced numerous setbacks following several negative developments, which we will discuss later. We broadly remain positive, however.

Our current investment thesis is:

- Operational improvements should contribute to margin and FCF improvement, with Management more cognizant of this going forward.

- A softening of its aggressive growth strategy should reduce shareholder dilution, improving investor returns.

- The acquisition of the Lord of the Rings IP has significant upside potential which investors have not priced in.

- The fundamentals of the company and industry remain strong. Its wide variety of studios and titles, across platforms, will support growth and consistent financial improvement.

Company description

Embracer Group is a leading global video game holding company headquartered in Sweden. It operates through several subsidiaries and is known for its diverse portfolio of video game franchises (PC/Console games, Mobile games, Tabletop games, and Entertainment).

Embracer is known for games such as Borderlands, Dead Island, Metro, Goat Simulator, Tomb Raider, and Deux Ex, among others.

{kind=link}

Development of the business (Embracer)

Share price

Embracer's share price performed well in the lead-up to 2021-2022, at which point the company faced a combination of large-scale share dilution to fund acquisitions and the collapse of a material partnership, turning investors bearish.

Recent developments

Within Embracer's Q4'23 report, Management stated " Late last night, we were informed that one major strategic partnership that has been negotiated for seven months will not materialize ". Deals fall over regularly, why was this such a big deal? Well according to Management " The specific deal included more than $2bn in contracted development revenue over a period of six years " ( Q4 Investor Report ). This represents 53% of its LTM Revenue... from one partnership.

In conjunction with this, the business faced a broadly difficult year, " adversely impacted by game delays, weaker consumer demand and lackluster reception for certain notable releases ".

These two factors contributed to an over 50% decline in the company's share price, as Management and investors retreated from the prior outlook of the company.

This has been incredibly disappointing and is likely a reflection of naivety among Management. The reliance on this deal in strategic decision making assuming it would close without due protection is inexcusable. Management was likely led into a false sense of security by the fact the counterparty was Savvy Games Group, a company that owns 7.85% of Embracer ( Source: TIKR Terminal ) and is backed by the Saudi PIF (which funded Embracer in 2022).

This contributed to a change in Management's strategy, with a new focus on operational improvement in response to this lost revenue. The broad objective is to:

- Generate Opex improvements and reduce Capex investment - This has involved a reduction in projects, as well as the closing of studios.

- Capital allocation - Identification of divestment opportunities, as well as consideration of increased external financing of projects and a global review of the company's existing pipeline.

- Efficiency improvements - New processes for game investment and development.

According to Lars " I have a high degree of confidence that this entire process is going to easily translate into better product selection that’s more profitable and that gives us a greater opportunity for growth in the future, and that helps to leverage the IP that we own within our organisation. "

Overall, this could be a blessing in disguise for investors... hear me out. Embracer has been full of potential while only providing short-term pain for investors, as its dilutive and aggressive M&A strategy contributed to poor share price performance and messy financials. Now that Management is forced to optimize the business, we will finally see its financials cleaned up, dilution slow, and margins improve. This should allow its fundamentals to be on full display, contributing to improved investor sentiment.

Further, it's likely to light a fire under Management, reminding them that they have a duty to the company's shareholders first. What we mean by this is that the company is likely bloated, as evidenced by the haste to reduce projects/studios. A slightly more "corporate" attitude to managing this business could help improve performance.

We would be comfortable seeing growth slow to <10% if EBITDA-M moves to >20-25% alongside consistently strong FCFs. A few years following this, its M&A strategy could commence again.

Hidden within all of this noise was a shrewd transaction that is a reminder of what Management's key strength has been, the identification of opportunities. In Aug-22, Embracer acquired the entertainment rights for The Lord of the Rings and The Hobbit IPs. In Feb-23, it further announced that it had an agreement in place with Warner Bros. to collaborate on multiple feature films.

This has the potential to be massive for the company, particularly because Amazon ( AMZN ) is pushing its TV heavily, even developing a LOTR MMO (which is part of a deal with Embracer). With the success of Game of Thrones, the Witcher Series, and others, there is clearly strong demand for high-fantasy. If developed well, the potential is significant.

Not only this but Embracer paid only $395m for the rights, which include worldwide rights to films, games, board games, merchandising, theme parks, and stage productions. By contrast, Amazon paid $250m for just the TV show.

Financial analysis

{kind=link}

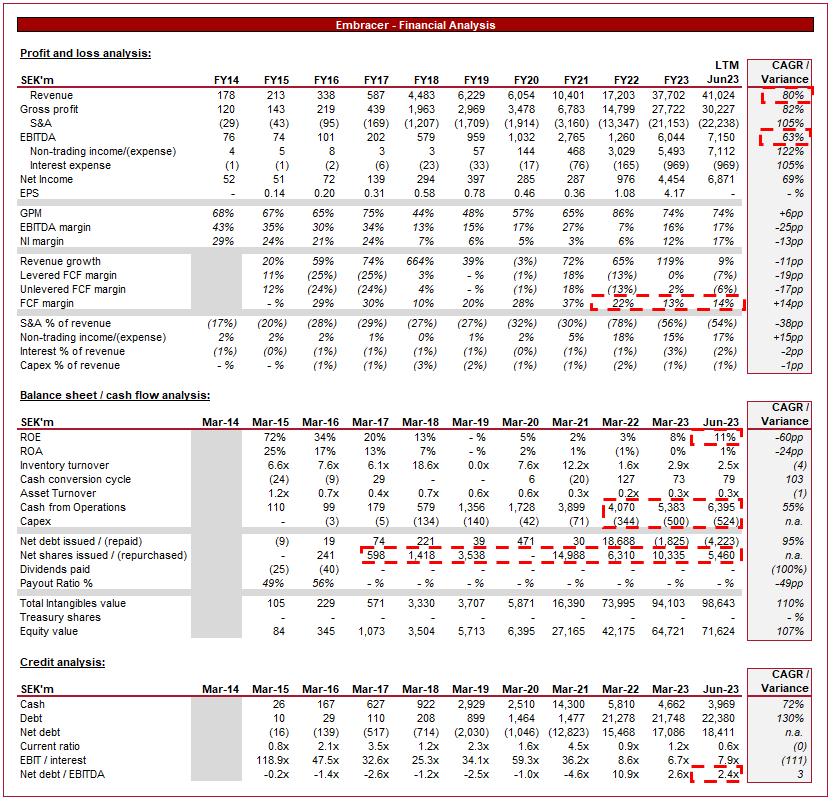

Embracer financials (Capital IQ)

Presented above is Embracer's financial performance in the last decade.

Revenue & Commercial Factors

Embracer's revenue has grown at a CAGR of 80% in the last 10 years, with 3 successive fiscal years of growth in excess of 50%, underpinning the strong performance.

Business Model

Embracer's subsidiary companies develop and publish a wide variety of games, including AAA titles, indie games, and mobile games. This diversification helps the company cater to different segments of the gaming market, maximizing its broader reach and earning potential.

Further, this allows the business to partake in industry trends, such as the current popularity of mobile gaming, driven by consumers seeking convenient entertainment and the improvement in mobile technology.

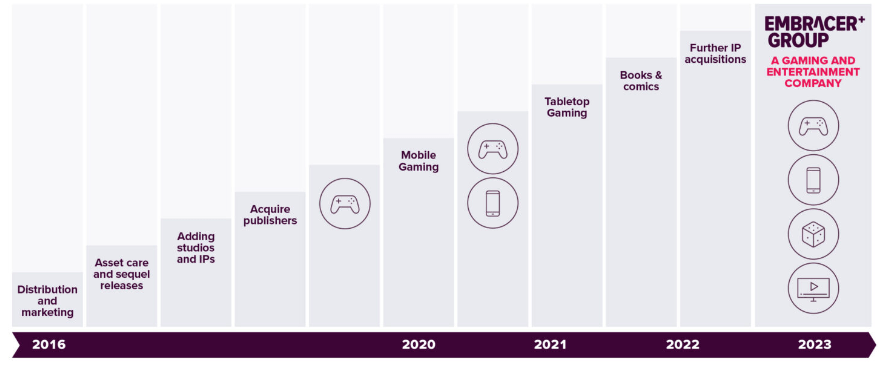

Embracer follows an aggressive acquisition strategy, acquiring successful video game development studios and publishers around the world, materially propelling its growth trajectory. The company places a strong emphasis on owning valuable IPs, utilizing M&A for this.

A nuance to this approach is Management's approach to financing acquisitions, with shares issued aggressively and cash utilized. This has allowed the business to finance consistent transactions but is not necessarily investor friendly.

Embracer invests heavily in, and culturally encourages, innovation and the development of new ideas beyond their current IP. The company has sought to develop a culture of passion towards gaming, rather than an underlying corporate attitude. We have critiqued this above partially, but more so toward Management than the studios.

Embracer maintains a decentralized structure, allowing its subsidiaries to operate with a degree of autonomy, and helps keep the corporate focus away from the developers. This approach fosters creativity and innovation within the individual studios, contributing to minimal disruption post-transaction. We believe this has been an incredibly successful strategy for the business and is a key reason why it has managed to keep teams motivated following buyouts.

Embracer's management team has a history of fostering growth within the subsidiaries, contributing to the company's overall success. The light-touch approach, ability to share competencies between teams, and strong due diligence to identify targets have allowed for consistency with results.

Competitive Positioning and Gaming Industry

The video game industry has experienced significant growth, driven by a number of factors. The continued incorporation of digital technologies in society, as well as greater access to digital devices globally are two key reasons. Further, from a psychological perspective, they are highly addictive and for many, provide an escape/stress relief from the pressures of life. Mobile gaming took this to a whole new level, providing extreme convenience and leaning further into the addictive nature of human behavior.

Embracer has expand its library of titles through additional content, utilizing downloadable content ((DLC)), future sequels, and in-game purchases. This has been a popular trend within the gaming industry, particularly in the development of in-game purchases. This is because it de-risks the gaming industry while significantly improving returns. Historically, the industry incurred development costs before releasing a game for a point-in-time purchase. Now, businesses can continue to monetize games for an extended period of time, maximizing their return per user (and reducing the downside of the second-hand games industry).

While we very much like Embracer's portfolio of games, there are two key weaknesses we see relative to its peers (many of which are larger). Firstly, the company lacks a definitive mainstream title (Think GTA, Mario, Pokemon, Minecraft, etc.). Borderlands, Tomb Raider, Metro, Saints Row, and Deux Ex have all had the potential to reach blockbuster success but slightly fall short. This puts the business at a disadvantage to the likes of Take-Two ( TTWO ) and Ubisoft ( OTCPK:UBSFY ). Secondly, Embracer lacks the lucrative profile of having an annually-releasing franchise, where only incremental development costs are required to drive significant returns. Examples of this include EA Sports FC (and other Sports Titles), Call of Duty, etc. This puts the business at a disadvantage to the likes of EA ( EA ) and Activision Blizzard ( ATVI ).

Q1 results

Q1 (Embracer)

Presented above is Embracer's most recent quarterly results.

Embracer's revenue has grown impressively in the last quarter, with YoY growth of 47% but importantly, organic growth of 20%. Further, EBIT has exceeded this level, allowing for margin improvement.

Despite this, the business is still in the process of integrating acquisitions and dealing with the current financial strain from issues faced in the prior year and the current restructuring process.

Balance sheet & Cash Flows

Embracer has historically avoided the use of debt, although was forced to in FY22. Management is currently seeking to rapidly deleverage, although we note the current level is at the top-end of sustainable (Interest at 3% of Revenue and an interest coverage ratio of 7x) if the business was forced to carry this.

Outlook

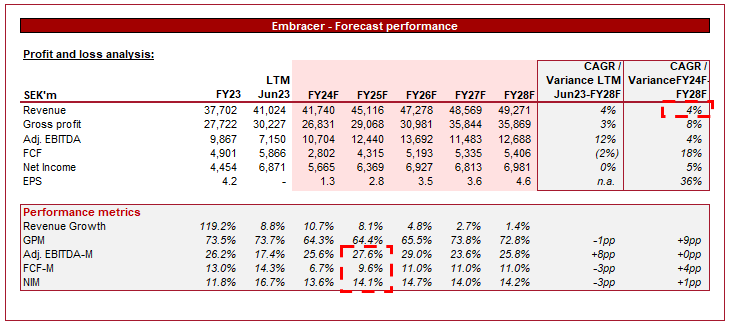

{kind=link}

Outlook (Capital IQ)

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting mild growth in the years to come, with a CAGR of 4% from FY23. This is a reflection of the change in approach going forward, with more conservative financial investment and a focus on operational optimization. Despite this, we believe the company's organic trajectory alone should support HSD, particularly with a strong pipeline (which we concede has likely peaked in the near term).

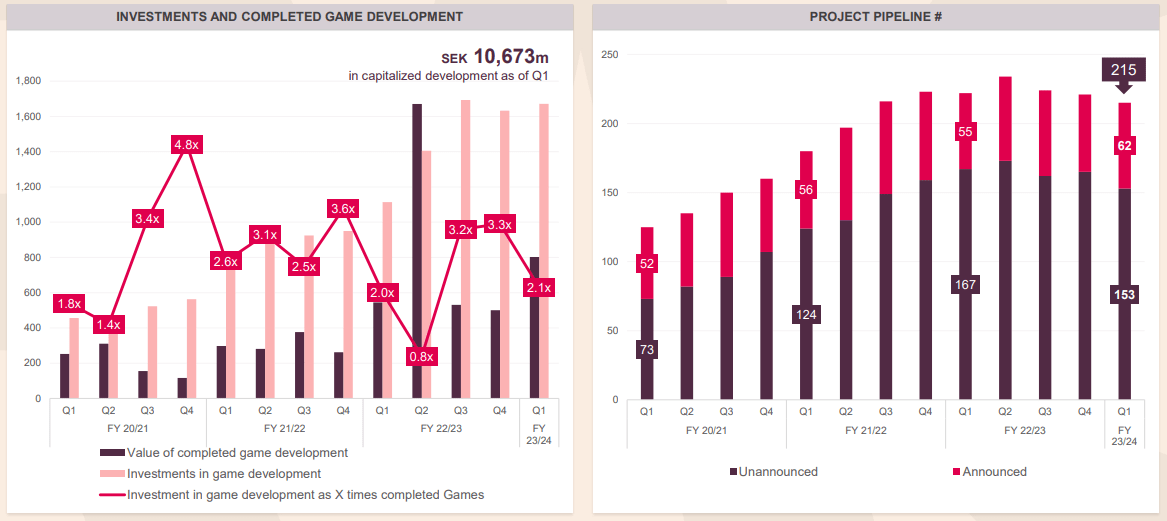

{kind=link}

Pipeline (Embracer)

Embracer's margins have been fairly erratic during the historical period, muddied by the various acquisitions conducted. With operational improvement underway, we expect definitional EBITDA to more closely align with Adj. EBITDA in the coming years.

Industry analysis

Interactive Home Entertainment Stocks (Seeking Alpha)

Presented above is a comparison of Embracer's growth and profitability to the average of the Interactive Home Entertainment industry, as defined by Seeking Alpha (11 companies).

Embracer's performance relative to peers is difficult to judge given the impact of growth. What is more important to consider is how the business is positioned in the years to come and how lucrative the industry is (and thus why we are so bullish).

Its peers have grown revenue at low double-digits, while profitability growth has slightly lagged this. Further, the industry boasts impressive margins and a ROE in excess of the long-term growth rate. Embracer is not a gulf away in margins while our revenue expectation of HSD organic growth is likely comparable, also.

Analysts are expecting Adj. EBITDA-M to land at 25-30%, which implies a definitional EBITDA of 20-25%. This would put the business at parity.

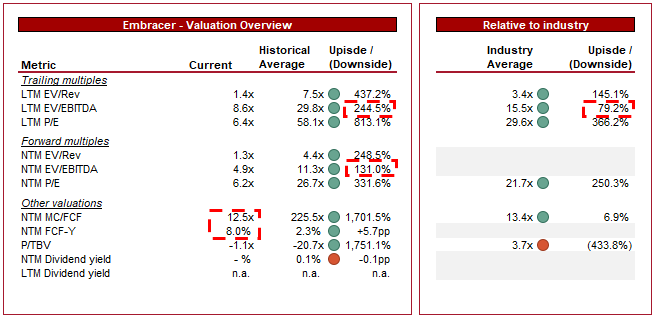

Valuation

{kind=link}

Valuation (Embracer)

Embracer is currently trading at 9x LTM EBITDA and 5x NTM EBITDA. This is a discount to its historical average.

A key consideration, beyond fundamentals, commercial considerations, and financials, is dilution. Investors hate dilution and the fear of this will continue to dissuade investment, contributing to an inherently baked-in discount.

A discount to its historical average is likely warranted, as this would adequately reflect the change in trajectory and issues faced in the last 2 years.

Further, a discount to its peers is also justifiable, primarily due to the execution risk of financial improvement in the coming 12-36 months, as well as the lack of blockbuster titles that many of the peer group hold.

Investment in this stock requires a long-term outlook and willingness to ride potential dilution, fluctuations in share price, and a non-"Wall St." attitude to running a business.

Embracer is owned and run by Lars Wingefors (20%+ ownership and rising with significant purchase). Although Lars has made mistakes, we continue to subscribe to the theory that well-run owner-led businesses will outperform.

Final thoughts

Embracer is a great business in our view, even if some of the decisions and outcomes of the last year would make any sane person doubt this. The company has been beaten down but we must remember, the future revenue lost is already offset by the decline in share price. We believe this will be a blessing in disguise for Management and contribute to more shareholder-friendly decisions going forward.

We continue to rate this stock a buy, although soften the rating due to the execution risk associated with margin improvement and maintaining a healthy level of growth.

For further details see:

Embracer Group: Why This Great Company Remains Highly Attractive