ERJ - Embraer: Growth Potential But Not So Adequate Financials

2023-09-06 07:37:55 ET

Summary

- Embraer has good prospects for growth due to the aging fleet of commercial and executive aircraft. Apart from that the company is positioned to benefit from the rising defense spending globally.

- Looking at the balance sheet, I am not so impressed. Embraer's liquidity and solvency are not adequate, in my opinion. Similarly mediocre is the situation with the company's profitability.

- The company is priced well below its peers but is overvalued based on DCF calculations.

- I give a hold rating because I like to see the company's management's efforts to improve its balance sheet and profitability.

Thesis

Embraer ( ERJ ) is a leader in its segment for jets with less than 150 seats. The demand for new jets is expected to rise due to the replacement cycle. Embraer is positioned to benefit from that dynamic. Another great advantage is the company's leadership in the executive aircraft segment.

However, Embraer needs adequate liquidity and solvency compared to its peers. Regardless of how bright the future is, the company sooner or later will pass through difficulties. To weather the storm, the business needs liquidity.

Embraer stock is overvalued based on discount cashflow calculations but cheaper than its peers. Despite the industry tailwinds and the company's standing as a leader in the North American market, I give a hold rating.

Company Overview

Brazil has a long history in the aviation industry. Since the beginning of the 20 th century, with Santos Dumont’s aerial adventures, the country has remained a factor in aeronautics. Nowadays, Brazil still holds a leading position in the industry. Embraer is a Brazilian aeronautics company that designs and manufactures commercial, executive, and military aviation aircraft. The company was founded in 1969 and has become one of the world's largest manufacturers of commercial jets with capacities ranging from regional to medium-haul aircraft.

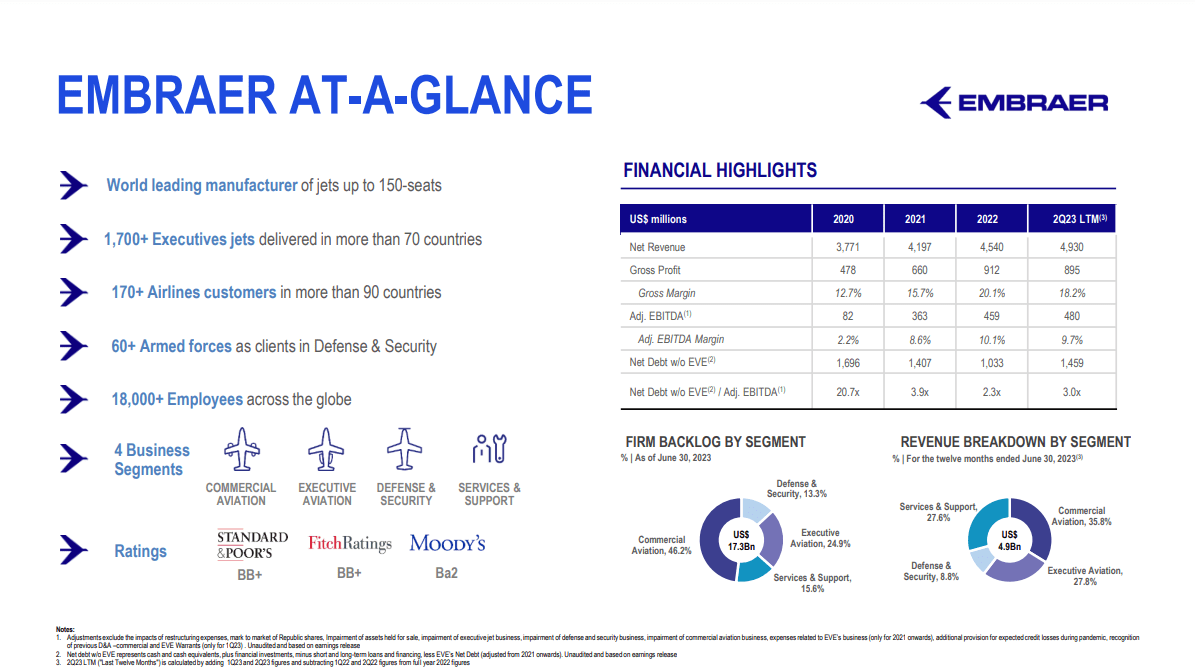

The table from last company's presentation below represents Embraer’s business at a glance:

{kind=link}

The revenue is equally distributed between commercial and executive aviation and services and support. A small part of the revenue originates from defense and security operations. Otherwise, the backlog is concentrated in commercial aircraft, 47%, and executive, 24.9%. The rest is divided between services and support and defense and security segments.

Embraer is widely known for producing the E-Jet series, which includes the E170, E175, E190, and E195 models. These aircraft are commonly used by airlines worldwide for short to medium-haul flights. The table below represents Embraer`s commercial aircraft portfolio:

{kind=link}

Embraer E-Jet E2 Series is the latest generation of Embraer's E-Jet family. It includes three models: E175-E2, E190-E2, and E195-E2. These aircraft offer improved fuel efficiency, lower operating costs, and enhanced passenger comfort. The E2 series focuses on regional and short-haul routes, accommodating varying numbers of passengers.

Its main competitors are Airbus ( EADSY ) and Bombardier ( BDRAF ). However, despite the fierce competition with Boeing ( BA ) and Bombardier in North America, Embraer dominates the market for jets with a 70-90 seat capacity. The company delivers 86% of the jets in that class.

Looking at the past, ERJ's performance is impressive:

{kind=link}

The backlog is the secret weapon of the aerospace industry. The higher, the better. The chart above shows Embraer's ability to keep growing its order book.

We have discussed the supply side, i.e., Embraer portfolio and backlog. However, they are only meaningful if we pay attention to the demand. The latter is a function of the current fleet age and the economic conditions. About the economy, I will go deeper in the section discussing the risks. The table below shows North America's replacement cycle for the next five years.

{kind=link}

Focusing on one type of commercial aircraft provides Embraer with a colossal advantage. The market domination in North America is proof of that statement. The company has a growing backlog, but I expect it to rise further, considering the replacement cycle. The left chart illustrates Embraer's top segment, the regional aircraft. Every year, 70 planes are due for replacement for the next five.

The second largest revenue generator is executive aviation:

{kind=link}

The table above shows the Embraer executive jets portfolio. The company’s focus is on small and medium-sized jets. The latter contributes 60% of the segment sales. Embraer main contenders are Gulfstream and Textron. Gulfstream is among the established companies in the industry. They manufacture only executive jets and dominate medium and large segments.

The model lines are two:

Phenom 100 and Phenom 300 are light jets for executive and private aviation. They offer comfort, performance, and advanced avionics for business travel. Praetor 500 and Praetor 600 are super-midsize jets that offer higher range, comfort, and advanced avionics for intercontinental travel.

The demand for executive jest is projected to grow. More people are getting richer at the highest rate in the history. On the other hand, uncertainty became predominant in economics, finance, and politics. The number of people who can afford to fly private will grow. The chart below shows the expected demand for executive jets:

{kind=link}

The global fleet of executive jets is aging, too. Many aircraft were delivered during the last peak 15 years ago. In the following years, they reach replacement age. I expect the executive segment in the Embraer portfolio to become more critical.

The third segment is the defense and security. The two pillars of the company defense segment are cargo aircraft C390 Millennium and light attach/training aircraft A 29 Super Tucano. Both are widely recognized for their capabilities globally. The image below from the last presentation illustrates Embraer's defense and security segment:

{kind=link}

Globally, defense spending will rise significantly due to the ongoing political fragmentation. The companies involved in the defense industry will benefit greatly. Embraer has a significant advantage because it delivers aircraft for all markets, i.e., NATO and BRICS nations.

Company Financials

The aerospace industry is asset-heavy with high fixed costs. Day-to-day operation consumes the company’s capital at a very high rate. Thus, liquidity and solvency are paramount for those businesses; they are also susceptible to interest rates and oil prices. A financial buffer is a must if the company wants to survive long-term.

Below is a table dissecting Embraer's balance sheet. The data is from the last report, Q2 2023 :

| EBITDA/Interest expense |

| 0.8 |

| EBITDA-CAPEX/Interest expense |

| 0.4 |

| Quick Ratio |

| 0.31 |

| Current Ratio |

| 1.5 |

| Net debt/EBITDA |

| 5.6 |

| Net Debt/ EBITDA - CAPEX |

| 26 |

| Long-term debt/Equity |

| 102% |

| Total debt/Equity |

| 134% |

| Total liabilities/Total assets |

| 75% |

Embraer's liquidity could be better compared to its peers. The table below compares Embraer, Textron ( TXT ), General Dynamics ( GD ) (Gulfstream's parent company), Bombardier and Boeing:

{kind=link}

The covered ratio and quick ratio are the lowest. The company’s solvency is not impressive, too. One positive sign is the lower Long-Term Debt/Total Capital.

Let's look at the company's profitability. The table below illustrates the company's profitability. The data is from the last report, Q2 2023 .

| Free cash flow/EV |

| 5% |

| Sales/EV |

| 54% |

| Gross Margin |

| 18.17% |

| FCF margin |

| 2.35% |

| Backlog |

| $ 8,0 B |

| ROI% |

| 1.98% |

| ROE% |

| (3.82)% |

| Net income per employee |

| $ (5,995) |

The numbers could be better. Regardless of the growing backlog and customer base, the company cannot convert them into net income. Among its peers, it shows the worst results based on ROI, ROE, and FCF margin. A long-term management's ability to grow a company's revenue while maintaining the costs steady makes any business profitable. Embraer's leaders must prove they can turn the company into a profitable enterprise.

Valuation

At this point, I will calculate the intrinsic value of Embraer. For this purpose, I use a 2 Stage Discounted Free Cash Flow Model by Professor Damodaran. For equation inputs, I use his database and Seeking Alpha.

Assumptions and inputs:

- Risk-free rate is equal to the 5Y average of US long-term Government bond Rate - 2.2%

- Risk-free rate is equal to the 5Y average of US long-term Government bond Rate - 2.2%

- Brazil's equity risk premium is 9.6%

- Aerospace and Defense unlevered Beta 0.70

- Embraer Debt to Equity ratio 116%

- Embraer effective tax rate 5Y average 34%

The above parameters are inputs in the following steps:

1. Calculate Levered Beta with the formula below:

Levered Beta = Unlevered Beta * (1+D*(1-T)/E)

2. Calculate the discount rate (discount rate as the cost of equity) using the resulting value for leveraged beta. The formula I use is:

Cost of Equity = Risk Free Rate + (Levered Beta * Equity Risk Premium)

3. Stage 1: I calculate the present value of discounted free cash flows for ten years using 2024 FCF estimates from Market Screener . I assume the FCF will grow at a stable rate of 9.7%.

{kind=link}

4. Stage 2: I calculate the Terminal Value of the free cash flows over ten years at stable growth into perpetuity, g, and the resulting discount rate. Then, calculate the present value of the Terminal Value:

Terminal Value = FCF 2033 × (1 + g) ÷ (Discount Rate - g)

Present Value of Terminal Value = Terminal Value ÷ (1 + r) 10

5. Sum the final results of stage 1 and stage 2. Their sum is called the Total Equity Value (TEV);

Total Equity Value = Present value of next ten years cash flows + Terminal Value

6. Divide the TEV by the total number of company-issued shares. The result is the intrinsic value of the acacia, which I compare against the current market price.

For Embraer, I get the following results:

Levered Beta = 1.16

Discount Rate = 12.9%

Total Equity Value = $ 6,629,000,000

Total shares outstanding = 735,000,000

Intrinsic value per share = $ 9.02

Current market price = $ 15.56 (as of Sept 05, 2023)

{kind=link}

Using EV/Sales and Price/Cash Flow, Embraer is much cheaper than its peers.

Risks

The aviation industry carries three significant risks: economic, liquidity, and operational. Change in the interest rates is a significant economic factor. It affects the company's liquidity risk. The aerospace industry is asset-heavy and requires large pools of capital.

The challenge comes from maintaining ROE higher than the cost of equity while the balance sheet remains liquid. If the price of equity is higher, the company is a capital destroyer. In short, stocks can be profitable due to the predominant narrative. However, in the long term, company fundamentals prevail.

For every business, the operations carry known unknown risks, i.e., idiosyncratic risks. They depend on internal dynamics such as corporate culture, capable leadership, and business processes.

Last but not least is the political risk in Europe. It sounds too distant and has nothing to do with the aviation industry. The transition to clean energy means reducing carbon dioxide emissions. Among the political elite, one of the options on the table is to reduce the number of short-haul flights. That means many inside-country connections might stop existing. If the EU enforces the ban on short-haul flights, the demand for aircraft with less than 100 seats will suddenly plummet. That will cause a significant revenue decline for Embraer because the demand for short-haul aircrafts will drop.

Conclusion

Embraer is a good company operating in a moderately growing industry with mediocre finances. It has a diversified portfolio and is a global leader in regional jets. The prospects for growth are favorable due to the aging fleets of commercial and executive aircraft. On top of that, defense spending will rise notably next year. The company is cheaper than its peers but overvalued based on DCF calculations.

I follow Embraer closely because I believe in the company's potential. However, I will give a hold rating until I see the company's liquidity and profitability improvements.

For further details see:

Embraer: Growth Potential, But Not So Adequate Financials