ERJ - Embraer Stock Is A Strong Buy

2023-11-14 14:45:04 ET

Summary

- Embraer S.A. stock has outperformed global markets, gaining nearly 50% since September 2022.

- Commercial aviation deliveries have increased, with a strong book-to-bill expected in Q4.

- Embraer has successfully deleveraged and reprofiled its debt, providing significant upside for the stock.

Since I marked Embraer S.A. ( ERJ ) stock a buy in September 2022, ERJ stock has shown strong outperformance, gaining nearly 50% compared to a <10% return for the global markets. This shows that value is not just locked into the big airplane manufacturers. In this report, I will be discussing the most recent quarterly results and review my rating and price target for Embraer stock.

Airplane Deliveries Continue Positive Momentum

{kind=link}

Commercial Aviation and Executive Aviation are the two most important OEM businesses that Embraer has. So, naturally, we are assessing the delivery profiles of these two segments carefully, also noting that continued OEM production is of key importance to the services businesses which have accounted for a significant portion of the revenues in recent years. Year-to-date, commercial aviation deliveries are up 39 units compared to 27 units last year. While sequentially commercial aviation deliveries did decrease, we do see that the year-to-date numbers showed the increase in deliveries expand from 41% to 47%.

The delivery profile is backloaded, as we see with many aerospace companies, so there is no point in linearizing the deliveries to assess whether the company will hit its delivery goal or not. From demand side, we do see that U.S. carriers are ordering more E175 planes for regional operations which could be seen as an indication that the pilot shortages are somewhat easing, and Embraer expects a strong book-to-bill in Q4 with order inflow exceeding the strong Q4 deliveries. With that in mind, I do believe there are announcements to be expected during the Dubai Airshow which layer on top of a list of potential orders we might be seeing at the show.

Executive Aviation deliveries increased by 14 units or 27%, but somewhat interesting is that Q3 2023 showed a sequential decline, whereas Q3 2022 deliveries showed a sequential increase.

Embraer has maintained the delivery outlook for 65-70 commercial deliveries and 120-130 executive aviation deliveries.

{kind=link}

Commercial revenues grew by 68% year-over-year on a 55% increase in delivery volume. Revenue growth was driven by higher volumes which also drove the gross margins to 6.5% from 5.4% while more E-2 deliveries also positively affected the revenue mix. Executive Aviation sales grew 25% to $339.9 million driven by 43% growth in revenues. The sales growth was slower than volume growth driven by the mix leaning more towards light jets but margins grew to 21.8% from 19.7%. Defense & Security sales grew 40% to due to revenue recognition based on progress and positive pricing adjustments which boosted gross margins from 16.1% to 26%. Services sales grew 24% to $365.8 million. However, due to a different services mix, the gross margins fell from 31% to 24.9% offsetting the top line growth.

Total revenues were $1.284 billion compared to $929 million a year ago, providing a 38% improvement in revenues driven by higher volumes in commercial aviation and executive aviation while defense & security benefited from contract baseline adjustments and revenue associated with progressing completion of contracts.

{kind=link}

The year-over-year figures show that 38% growth in revenues translated to Adjusted EBIT doubling, which in my view shows the positive volume effects and also adjusted EBITDA showed growth in excess of revenue growth demonstrating the positive volume effects. Free cash flow grew from negative $92.4 million last year to $44 million this year. Sequentially, revenues were slightly lower, but the Adjusted EBIT margins were stable while Adjusted EBITDA margins were 90 bps higher. So we do see further improvement in margins even with slightly lower revenues.

Embraer Successfully Deleverages And Reprofiled Debt

{kind=link}

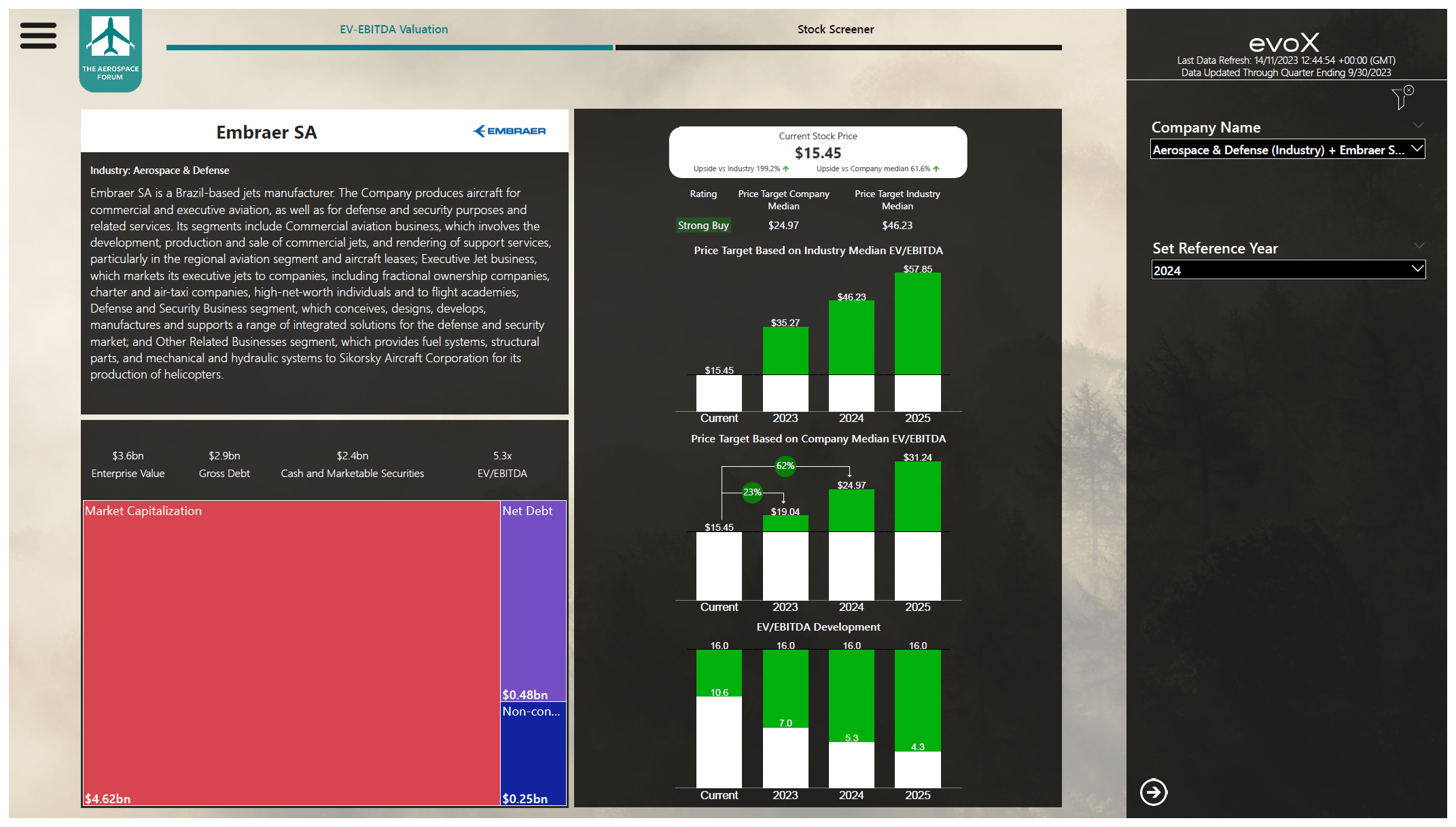

What I like about Embraer is the strong liquidity at $2.4 billion, while its maturing debt until 2026 is minimal providing a lot of padding with the full liquidity covering almost all debt, and with the cash position of $1.5 billion the company can easily cover all debt up to and including 2027. Sequentially, gross debt reduced by $632 million while a better cash position improved the net debt position. Adding a better adjusted EBITDA allowed the company to significantly improve its leverage from 4.8x to 2.5x, and with a strong end of the year expected, I think that leverage will improve even further and could even exceed the 2.3x seen by the end of 2022.

Embraer Stock Has Significant Upside

{kind=link}

Following the release of third quarter results, I have implemented relevant balance sheet data and forward projections for Embraer in my interactive stock screener. For 2023, the EBITDA estimates have remained more or less constant, but free cash flow projections have come down for the year. For the longer term, meaning up to 2025, we see free cash flow projections up 0.8% and EBITDA projections up 0.3% compared to previous estimates.

Parsing the numbers, I have established a $19.04 price target with a strong buy rating, automatically assigned using a score methodology by the stock screener. This provides 23% upside, which admittedly is lower than the 32% upside I saw previously driven by the lower cash flow expected for the year but part of the upside has also materialized.

Given the company’s undervaluation compared to peers and the strong deleveraging path, I feel comfortable with my price target and note that Wall Street analysts even have a higher price target of $20.31. Furthermore, as we are heading into 2024, I believe that the stock price should gradually start reflecting 2024 expected earnings which provides 62% upside from current levels.

Conclusion: Stock Execution Drives Upside For The Stock

Embraer is seeing significant improvements in its commercial and executive aviation deliveries, which drives cash flow on delivery with a significantly backloaded profile and a major improvement in delivery numbers year-over-year. So, the ability to deliver jets and later on harvest services revenues from those jets is improving and the orders for the E175 also can be seen as an indicator that the pilot shortages at U.S. regional carriers is easing slowly but surely, which bodes well for the delivery profile.

From balance sheet perspective, Embraer S.A. has successfully deleveraged and continues doing so while also having reprofiled its debt leaving the company with a very manageable debt maturity profile in the years ahead. All combined, this provides significant upside for the stock and I feel comfortable maintaining my strong buy rating.

For further details see:

Embraer Stock Is A Strong Buy