EME - EMCOR Group: Good Growth Prospects But Expensive (Rating Downgrade)

2023-05-09 15:22:55 ET

Summary

- Revenue should benefit from robust RPOs and resilient end-market demand.

- The margins should benefit from pricing actions to mitigate inflationary pressure and easing supply chain constraints.

- Premium valuation keeps me on the sidelines.

Investment Thesis

EMCOR Group (EME) is poised to benefit from the healthy Remaining Performance Obligations (RPOs) and good end-market demand. There are several secular trends like the onshoring of supply chains and domestic capacity expansion under the CHIPS and Science Act 2022, good demand for hyperscale data centers and building automation, etc. which should drive revenue growth in the future. The margin should benefit from good project execution, a favorable product mix, pricing actions to mitigate inflationary pressure, and easing supply chain constraints.

I last covered the stock in November when I gave it a buy rating . The stock is up ~14% since then and has outperformed the broader markets. However, after this outperformance, the company's stock is currently trading at a premium valuation compared to its five-year forward average P/E. While the company's prospects look favorable, the premium valuation suggests that these prospects are already getting priced in at the current levels. Hence, I am moving to a neutral rating.

EME's Q1FY23 Earnings

In the last week of April, EME reported better-than-expected results for the first quarter of FY 2023. Sales for the quarter stood at $2.89 billion, which represented an 11.6% YoY increase (organic growth of 10.1%), and exceeded the consensus estimate of $2.87 billion. The EPS increased by 66.9% YoY to $2.32, compared to the consensus estimate of $1.83. Despite persistent inflationary and supply chain challenges, the consolidated operating margin expanded 150 bps YoY to 5.4%, contributing to the improvement in EPS for the quarter.

Revenue Analysis and Outlook

In Q1 2023, EME's revenue growth was driven by good execution across all segments, a contribution of $35.2 million from a recent acquisition, and strength in retrofit markets with a focus on energy efficiency and indoor air quality.

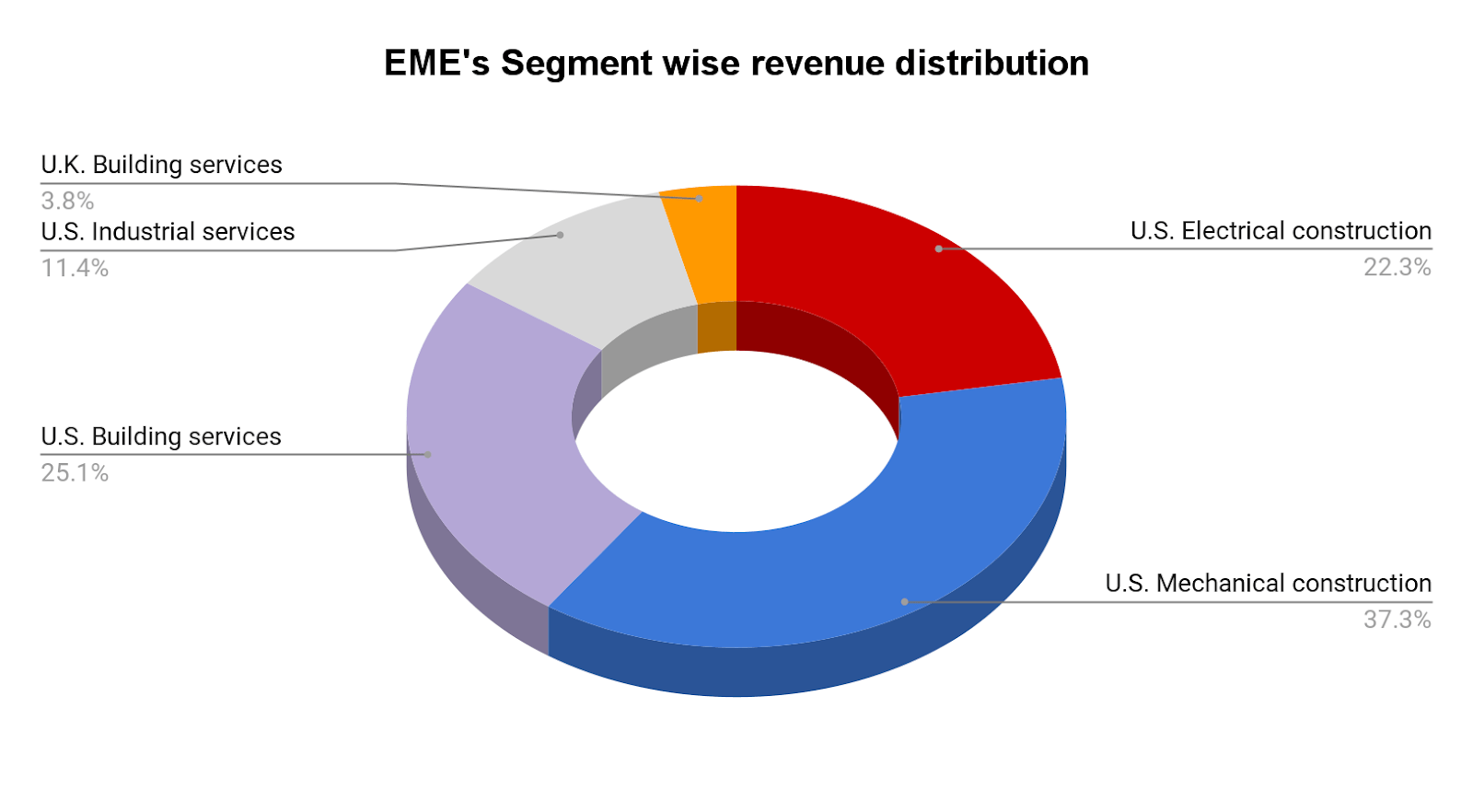

The U.S. Mechanical Construction segment grew 8.7% YoY to $1.08 billion, driven by strong demand in high-tech manufacturing, particularly in the areas of semiconductors and EV value chain, as well as continued demand for data centers.

The U.S. Electrical Construction segment grew 23.5% YoY to $644.7 million, driven by acquisitions and increased project activity within the network and communication, healthcare, manufacturing, and hospitality and entertainment market sectors. This more than offset revenue declines in the transportation and traditional commercial sector.

The U.S. Building Services segment saw revenue increase by 14.1% YoY to $725.4 million, primarily driven by growth within the mechanical services division. The U.S. Industrial Service segment saw modest growth of 6.5% YoY, despite headwinds from ongoing volatility in the broader oil and gas industry. The steady resumption in demand for its field services offering, increase in new-built heat exchange orders, and growth in its cleaning and maintenance within shop service operations more than offset the headwind.

Overall, the total U.S. operation grew 12.9%, driven by strong growth across all major segments. However, the United Kingdom Building Service segment revenue declined 15.7% YoY to $110.9 million, primarily due to unfavorable exchange rates resulting from the weakening of the pound sterling.

Emcor's Segment Revenues (Company data, GS Analytics Research)

{kind=link}

Looking ahead, the company's revenue this fiscal year should benefit from strong RPO levels and strength in its end markets. In Q1 FY23, RPOs were up 32% Y/Y to $7.9 billion indicating strong underlying demand for the company's services and giving good visibility on future revenue growth.

In terms of end market demand, the company is benefiting from several secular tailwinds. The company's network and communication business is benefitting from increased demand for hyperscale data centers which should continue for the next several years. Further, the company should benefit from high-tech manufacturing projects related to semiconductors and EVs, EV Value chain, and batteries. The trend towards onshoring supply chain and domestic capacity expansion should also benefit the company's revenue in the coming quarters. Moreover, the additional investments driven by the CHIPs and Science Act which encourages U.S. manufacturing should add to this demand. Last year, companies like Micron ( MU ) and Qualcomm ( QCOM ) announced ~ $50 billion in additional investments under this act.

In the U.S. Building Service segment, supply chain issues, and challenges still exist, with long lead times and unreliable delivery schedules for finished systems such as switchgear and HVAC equipment. However, the situation is getting incrementally better and the company continues to adapt and improve planning to reduce disruptions. Strong demand for Building Automation and Control solutions, as customers seek ways to improve energy efficiency and/or indoor air quality of their facilities, coupled with many companies focused on reducing their carbon footprint, should make this business an area of continuing demand for EME, benefiting the company's revenue in the coming years.

EME holds a well-balanced portfolio of businesses with the ability to provide Electrical and Mechanical construction, retrofit, and repair service technical labor and solutions across diverse non-residential market sectors in U.S. and U.K. geographies. This, along with a good product mix and well-executed project delivery in this ongoing challenging operating environment, makes me optimistic about the company's longer-term revenue growth prospects.

Margin Analysis and Outlook

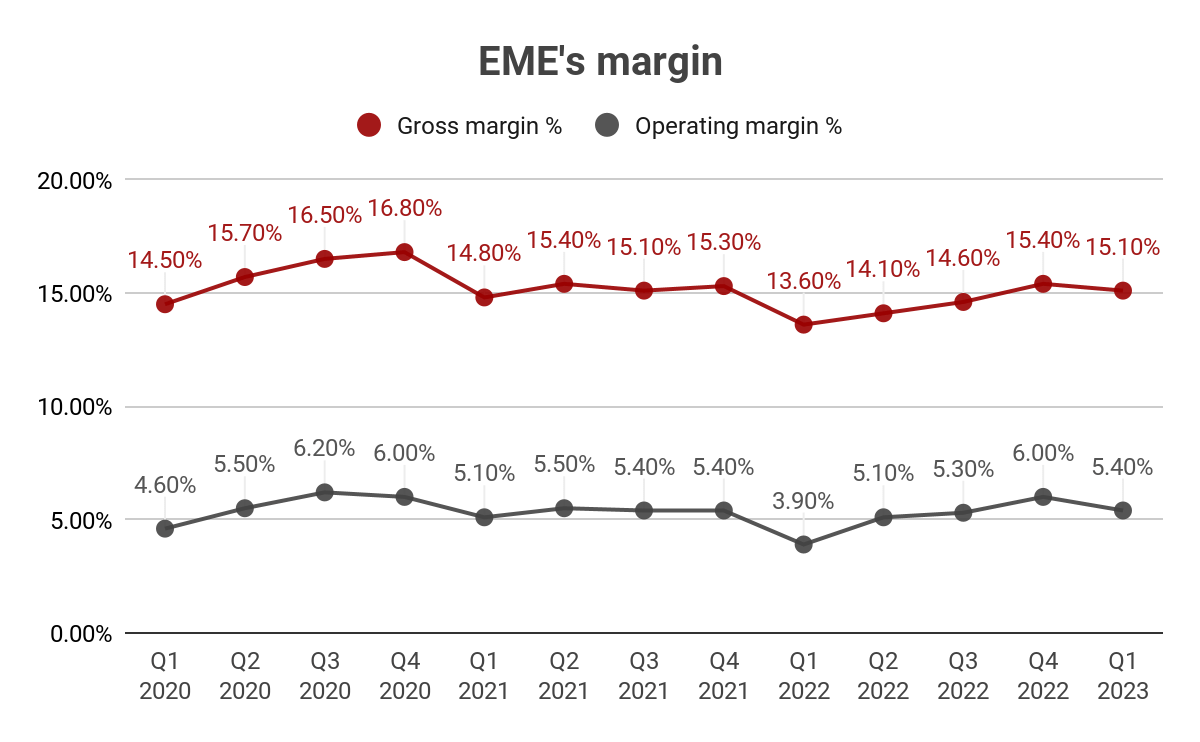

The company achieved a Y/Y expansion of 150 bps in its gross margin, which reached 15.1% in Q1 2023. This can be attributed to good execution, a favorable mix of businesses, and easing comps. Consolidated operating margin also expanded by 150 bps, due to the same reasons.

Segment-wise, the U.S. Electrical construction segment showed the most significant improvement, growing 250 bps Y/Y to 6.3% in Q1 2023, thanks to a favorable revenue mix and easy comps due to the negative impact of supply chain disruptions in 2022. Meanwhile, the Mechanical construction segment improved to 8% from 5.9% in the prior year, driven by good project execution, a better revenue mix, and improvements in the supply chain and commodity pricing environment. The U.S. Building Service segment increased by 140 bps Y/Y, while the U.S. Industrial segment only saw a modest 20 bps growth. In contrast, the U.K. Building Service segment experienced a 320 bps Y/Y margin contraction and margins fell to 4.9% in Q1'23 due to unfavorable comps resulting from the benefits of a successful project closeout in the prior quarter.

Emcor's margins (Company data, GS Analytics Research)

{kind=link}

Looking ahead, the supply chain situation has improved slightly in the recent quarter and is expected to continue to improve as equipment availability increases. Coupled with ongoing pricing adjustments to mitigate inflationary pressure, these factors should more than offset headwinds for the rest of 2023, resulting in margin expansion.

The company was able to adapt well to less-than-optimal environments in the last couple of years and execute well. So, with supply chain and inflationary headwinds easing, I am expecting execution to improve further. Along with normalizing demand, this should help the company achieve margin expansion in 2023 and beyond.

Valuation and Conclusion

The company's stock is currently trading at a forward P/E of 16.97x FY23 consensus EPS estimates of $9.81, which is a premium to its five-year average forward P/E of 15.65x. Even based on the FY24 consensus EPS estimate of $10.70, the company's P/E is 15.56 which is almost in line with its historical averages. In the coming years, the company's revenue should benefit from resilient end markets and secular tailwinds from the increasing demand for data centers and government stimulus in the form of the CHIPS and Science Act.

Margin prospects also look good given the company's excellent execution, easing supply chain constraints and pricing actions to mitigate inflationary pressure. However, the premium valuation of the stock indicates that these positives are already getting reflected in the current stock price. Hence, I am moving to a neutral rating on the stock.

For further details see:

EMCOR Group: Good Growth Prospects But Expensive (Rating Downgrade)