PKB - EMCOR Group: Things To Consider Ahead Of The Upcoming Earnings Event

2023-10-25 16:38:23 ET

Summary

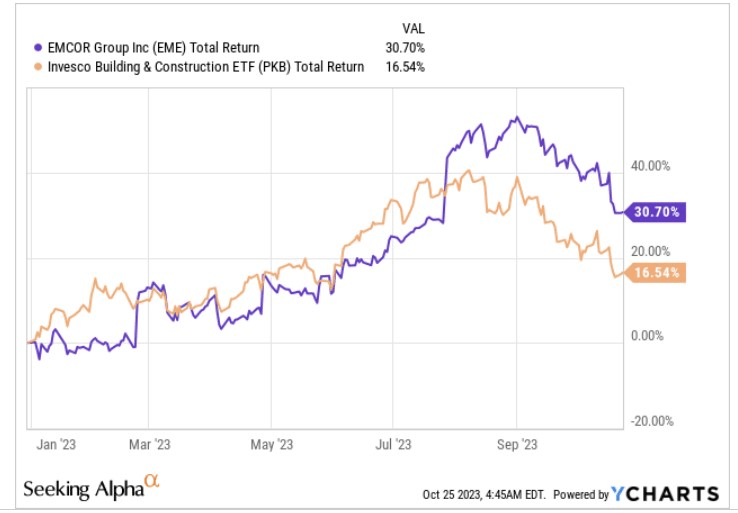

- Emcor Group's stock has performed well in 2022, delivering a 31% return and outperforming a building and construction ETF by almost 2x.

- We have a catalyst on the anvil with Q3 results due to be announced on October 26.

- We pick out some of the key themes to watch out for.

- We also touch upon earnings revisions and current valuations.

- We close with some thoughts on the technicals.

Introduction

The stock of EMCOR Group ( EME ), a mid-cap specialty contractor with particular expertise in the fields of mechanical and electrical construction, has enjoyed a fine 2022; on a YTD basis, the stock has delivered 31%, almost twice as much as its peers from the Building and Construction universe.

{kind=link}

Soon enough, the stock may likely make another big move, one way or the other, with the Q3 earnings report due to be published on the morning of the October 26. Here are a few important things for investors to consider ahead of the key event.

Key Earnings-Related Considerations

EME’s earnings track record over the last two years has been quite heartening to watch; over the last eight quarters, it has missed street estimates only once (in Q1-22). Crucially note that over the last couple of quarters, the degree of earnings beat has come in at a hefty percentage of over 25% on average. This probably tells us that the consensus is yet to get a solid grip on some of the recent positive changes taking place in this business and industry.

Seeking Alpha

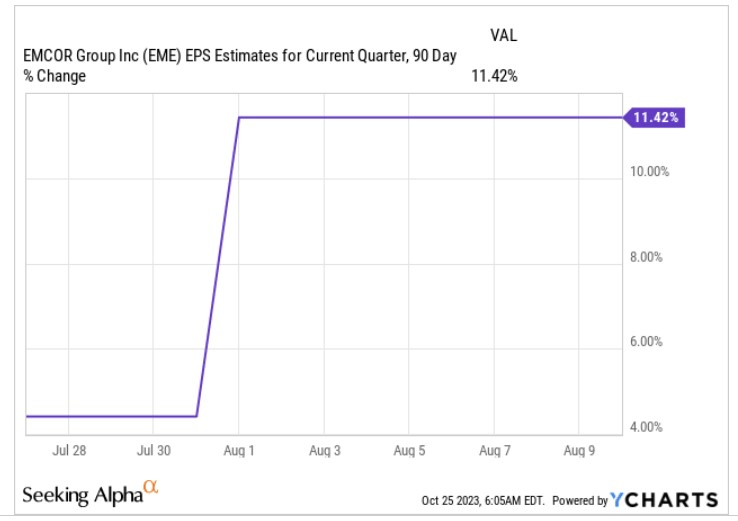

Looking ahead to Q3, the key headline numbers to watch will be an expected EPS figure of $2.68 , and expected revenue of $3.11bn. We’d imagine it would take something special for EME to come up with another +25% EPS beat, as it looks like over the past three months, consensus has already lifted its EPS estimates by over 11%. Given the magnitude of these sell-side EPS upgrades, investors would be advised not to expect too many fireworks.

{kind=link}

It's also worth remembering that during the Q2 event, management had also lifted the FY EPS guidance range from previous levels of $9.25-$10 to $10.75-$11.25; basically, at this mid-point of those ranges, the implied guidance lift is around 13%.

In that regard, even if the actual Q3 numbers are roughly on par with consensus numbers, there’s potential for EME management to drive through further upward revisions in the FY numbers as current consensus expectations for the whole of FY23 (even after the recent Q3 upgrades) are still over 2% lower than the upper end of the guidance provided in Q2.

Having said that, investors are advised not to expect the moon with forward guidance, as the forward-looking ABI index (a useful leading indicator for non-residential construction activity by 9-12 months), recently dropped to its lowest point since December 2020. Backlogs have also come off in a big way from peak levels of 7.2 months seen last year in Q1-22.

One key variable to note will be the growth of EME’s RPO (Remaining Performance Obligations) as it helps provide some perspective on the future revenue visibility. The RPO diminishes as work gets completed and revenue is recognized whilst it goes up when EME garners new contracts. In fairness, EME has done reasonably well to maintain a book-to-bill ratio of over 1x for multiple quarters, but one does wonder if this could drop off soon enough, given the slowing pace of the YoY RPO growth (Q2 vs Q2). In Q3, EME will come up against a high base where last year’s RPO growth came in at an impressive pace of 32%!

EME Quarterly reports

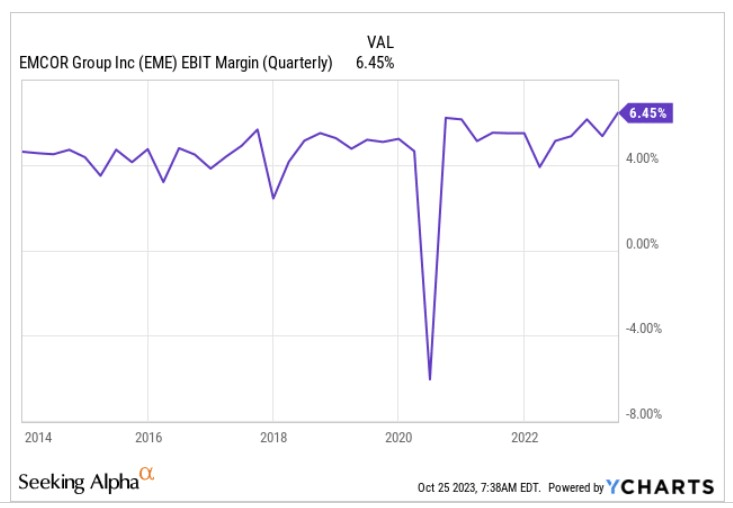

As far as margins are concerned, note that this is not an innately high-margin business (see image BELOW), but yet still, the company delivered record EBIT margins in Q2 ( 140bps YoY improvement), and sounded optimistic about this trend carrying on as they seek to generate better SG&A leverage through H2. Much of this is driven by a better service mix, in Q4 a more normalized fall season should help as well.

{kind=link}

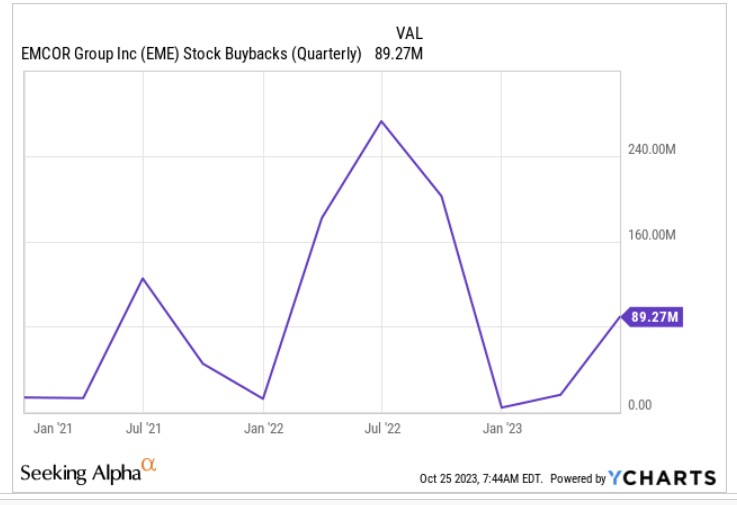

On the capital allocation front, we have been enthused to note that EME has been gradually scaling up its buyback spend over the past two quarters (it only spent ~$4m in Q4-20), but we wouldn’t necessarily expect this trend to have continued into Q3, given that they would have deployed a healthy chunk of cash to acquire the energy efficiency specialist ECM Holdings at the start of Q3 (the acquisition sum was not disclosed). For context at the end of Q2, EME still had authorization to indulge in $284m of buyback spend.

{kind=link}

Valuation Considerations

Investors largely gravitate to EME because it is expected to be one of the key beneficiaries from the ongoing reshoring momentum ( 83% of NA manufacturers are likely in the midst of reshoring their supply chains), EV infrastructure, and steps to beef up the domestic grid. However, at some stage one also has to ask if a lot of the positive expectation has already been baked in, and also ponder if the price has gone too far. We’d be inclined to go with that view.

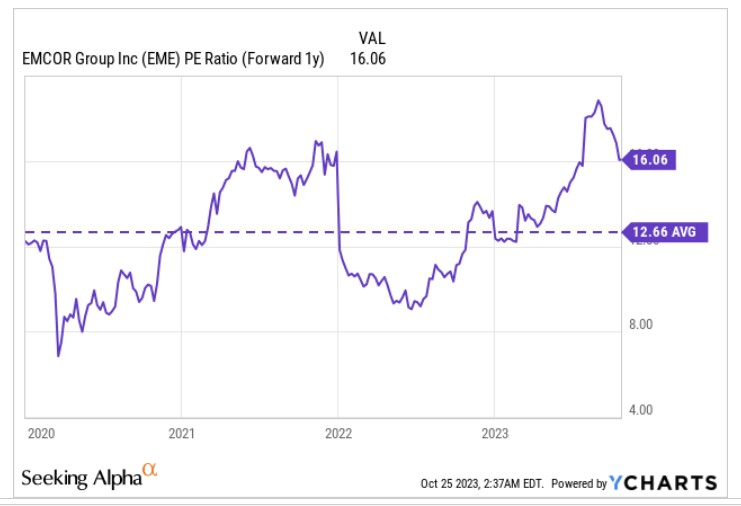

FY23 has been a stellar year for EME and sell-side analysts have made upward revisions to the tune of 15% already across the last six months. Things don’t end there, and even next year’s estimates have been scaled up by a healthy rate of 13% over the past six months. All in all, despite these strong upgrades, note that YCharts estimates imply that EPS growth in FY24 will come in at only 9% YoY (an expected EPS of $12). Given that you’ll likely only get single-digit-earnings growth, it feels a bit much to shed out a forward P/E (based on the FY24 EPS) of 16x. Crucially, also consider that this P/E translates to a relative premium of 26% over the stock’s 5-year average multiple.

{kind=link}

Closing Thoughts- Technical Considerations

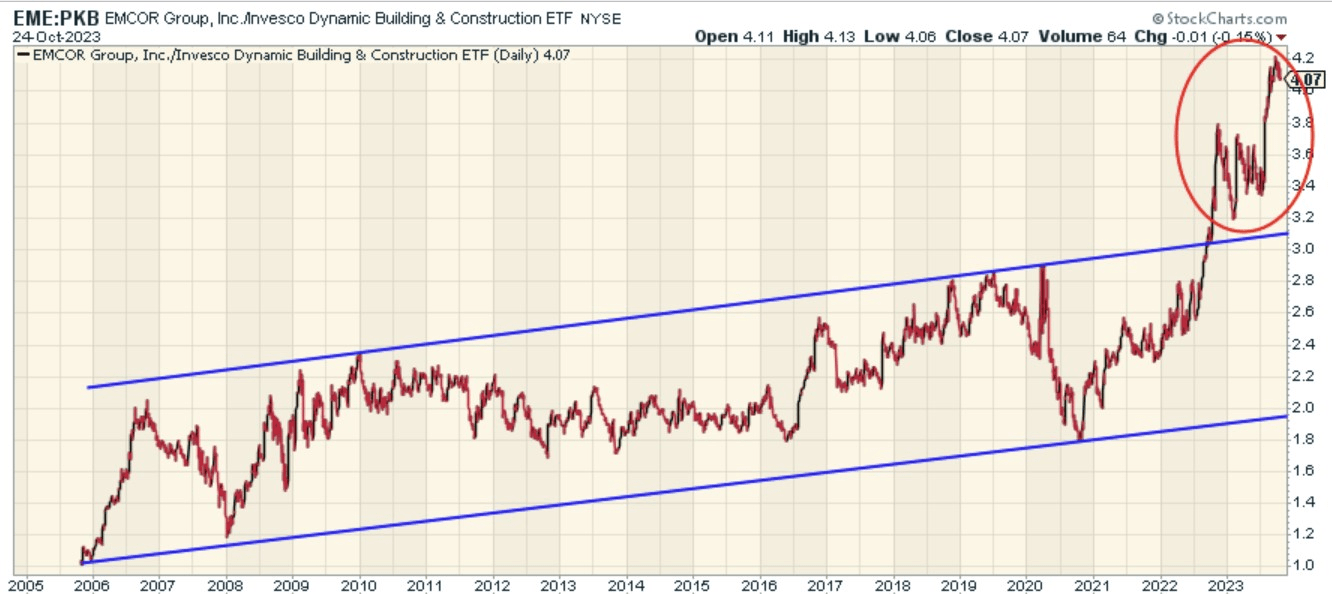

The chart below helps ascertain if EME could potentially serve as a useful rotation option for those interested in the US building and construction universe.

{kind=link}

Well, based on the imprints seen here, that’s not something we could advocate for now. From 2006 till mid-2022, we can see that EME had been gaining steady clout versus its peers, with a gradual increase in the relative strength ratio. However, note that even though this ratio moved up over time, it did so within the boundaries of a certain ascending channel. However, since the second half of 2022, this ratio has just gone ballistic, and is currently at around lifetime highs, which certainly dampens the rotational prospect.

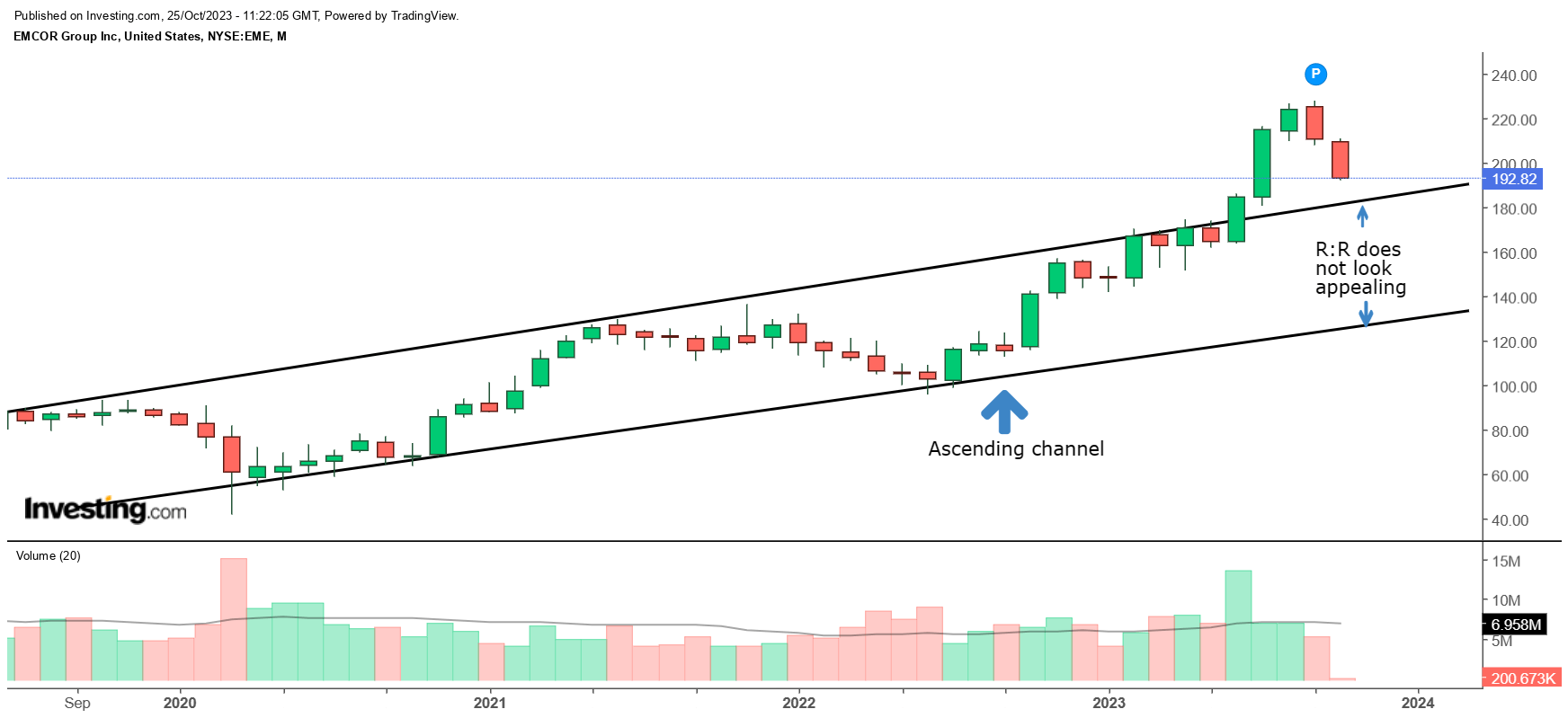

Then if we switch focus to EME’s own weekly price imprints we can see similar patterns of an ascending channel, but here the breakout took place at the start of June; in recent weeks the euphoria appears to have given way to a pullback. Now, based on how Q3 results go, we could see the stock slump back to its old channel, build a base just outside the channel, or kickstart another leg higher. Either way, given where valuations are, we are not prepared to be bullish on EME at this stage and would prefer to review it if it drops back into the old channel.

{kind=link}

For further details see:

EMCOR Group: Things To Consider Ahead Of The Upcoming Earnings Event