AQN - Emera: Dividend Freeze Would Actually Be The Best Outcome

2023-06-17 22:25:11 ET

Summary

- Emera's debt load is getting too high.

- All 3 rating agencies have a negative outlook on their rating.

- This is a dangerous path into a recession and changing the dividend growth plans would be very helpful.

All values are in CAD unless noted otherwise.

When regulatory authorities determine the rate to be charged by a utility provider, that company is known as a cost-of-service rate-regulated utility. The rate zeroed upon compensates the utility for it the expenses (excluding interest and income taxes) it incurs to provide reliable service to its customers. Additionally, it includes a little somethin somethin which forms the return on investment for the utility and its shareholders. This portion of the rate is often called return on equity. This rate setting provides the utility visibility into future earnings and provides reliable cash flow which facilitates better planning. Often times this also enables the company to consistently increase dividends to its shareholders. Its not all sunshine and roses though, and we shall see that later in this piece.

Often, not all, but a significant portion of company's assets fall under the regulatory purview discussed above. Headquartered in Halifax, Nova Scotia, Emera Incorporated ( OTCPK:EMRAF ) ( EMA:CA ) is one such utility. It owns and operates electric and gas assets in Canada, United States and the Caribbean, majority of which are regulated.

{kind=link}

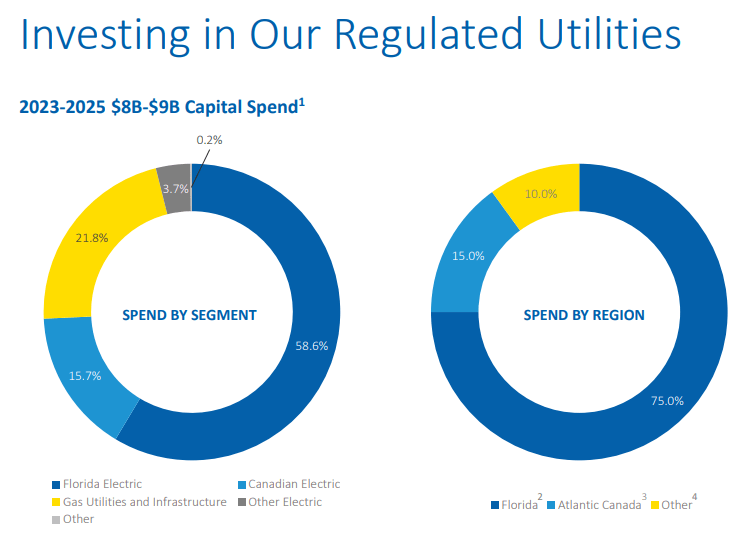

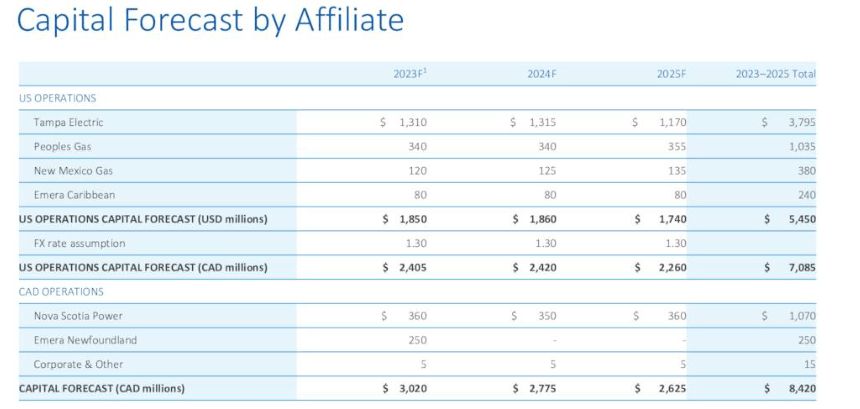

Ongoing capital expenditures or capex are not uncommon for utilities and Emera is no different. The company has $40 billion in total assets and expects to spend another $8-$9 billion in capex over the next three years, with most of it concentrated in Florida.

{kind=link}

The focus on Florida is based on the customer growth trends seen in 2022 and to have the infrastructure to reliably meet the higher energy demands. Emera expects that this capex endeavor will result in a 7%-8% rate base growth and 4%-5% dividend growth over the same time period. The company already has 16 years of consecutive dividend increases, and expects to continue that trend at least for the next three. At 69 cents/quarter and current price, the stock yields a little over 5%. Not shoddy at all when compared to its peers.

Prior Coverage

Estimated debt to EBITDA of 6.4X, capex plus dividend payout in excess of free cash flows, along with downgrades from credit agencies from stable to negative outlook (still investment grade) were reasons enough to place us in the bear camp the last time we covered this stock. There was no way we would advocate buying this one for 18X earnings that it was trading at the time. We had a price target of $45 with an explanation in the conclusion to that piece.

Some investors may assume that Emera has room considering that both Fitch and S&P are two notches above junk. That does give it some time, but we have to put our weight behind Moody's here and think the Baa3 (one step above junk) with negative outlook, is more representative of the risks. We are issuing a Sell rating here and expect the combination of these headwinds to warrant a dividend freeze, large equity issuance and a move to 15X normalized earnings. That gets us to about $45 CAD per share.

Source: Emera: Don't Chase That Yield

While it has not beaten the broader market, the stock has performed decently since then.

Seeking Alpha

Our prior article was based on the Q3-2022 data. Let us review the recent numbers and elaborate on the reasons for our current sentiment.

Q1-2023

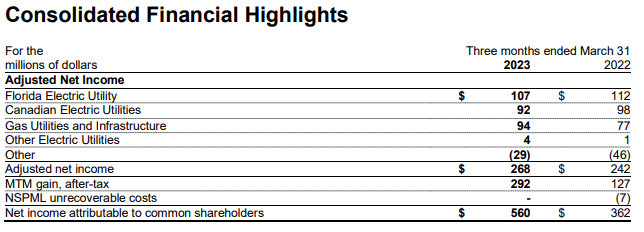

While Tampa/Florida Electric and Canadian Electric enjoyed the boost from higher rate base, it was more than offset by higher operating and interest expenses. Perhaps the straw that broke the Canadian side's back was also the provision for the $10 million in penalty pertaining to renewable energy standards, that Nova Scotia Power had to recognize in the quarter. The company intends to appeal the penalty caused by delays in commissioning and ongoing testing.

{kind=link}

While higher interest expense was experienced across the board, the new base rates and asset management agreement that helps create value from unused capacity, helped the gas segment outperform the prior year numbers. The trading and marketing arm also continued to perform well. Even excluding the star of the show, mark to market gains of $292 million, the earnings per share or EPS increased year over year by 7.60% from 92 cents to 99 cents.

{kind=link}

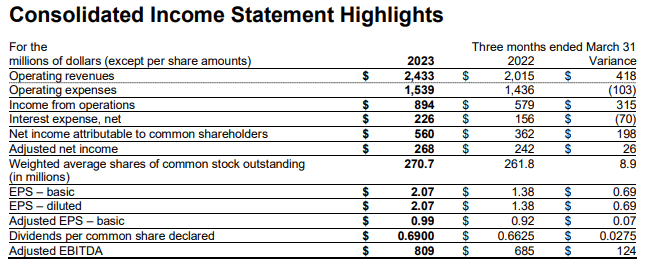

Before we break out the bubbly though, take a note that the year over year interest expenses increased by close to 50% due to higher rates and debt levels. This does the impossible, it makes the 22% year over year increase with saw in Q4-2022 seem like the good old days. The debt plus interest obligations for the remainder of 2023 at the end of Q1 were $1,214 million.

Q1-2023 MD&A

If you combine this information with their cash flow statement and their capex plans you get a picture of Emera increasing debt load faster at a time where their interest costs are ballooning rapidly.

Q1-2023 MD&A

Capex does slow down in 2024, but it will remain rather high nonetheless.

{kind=link}

Debt should increase by at least $1.0 billion in 2023 and a similar amount in 2024. The hope is that the debt to EBITDA can be forced down as base rate increases flow through. While the rating agencies still have this company as investment grade, we had discussed the downgrade from a stable to a negative outlook in our previous piece . Emera's management does not expect that to change anytime soon and said as much in the earnings call ( emphasis ours ).

Maurice Choy

Thanks. And maybe just a quick follow-up. Your expectation of how the rating agencies will respond to these? And any recent engagement with them about changing the outlook back to stable.

Greg Blunden

Yes, I mean that's an ongoing conversation, Maurice. I mean, generally, they look through the fuel cost recovery side of it. So, looking through maybe the cash flow perspective, but I think it's -- they're fairly consistent across the board. They don't normalize for the associated debt with respect to those fuel cost recoveries.

Obviously, with the majority of our under recoveries in 2022 of Tampa Electric and now having regulatory approval for that. That's helpful, seeing an accelerated recovery of those costs, which does mean we're reducing our debt.

So, given that they don't normalize for the debt, that will certainly be a positive. But having said all of that, I'm not anticipating that we'll see a shift back to stable outlooks anytime soon.

Valuation and Verdict

With the stock price higher than when we last wrote on it, and there is no corresponding positive change in terms of leverage and interest expense. While the growing dividend may have the income crowd interested, we do not believe it is sustainable, despite what the management noted in the Q1 report.

Emera has provided annual dividend growth guidance of four to five percent through 2025. The Company targets a long-term dividend payout ratio of adjusted net income of 70 to 75 per cent and, while the payout ratio is likely to exceed that target through and beyond the forecast period, it is expected to return to that range over time.

Source: Q1-2023 MD&A

We do not think Emera will be able to carry out its capex plans and sustain the dividend growth without getting further into the bad books of the rating agencies. As opined back in December, something has got to give. The company will have to revise its dividend growth plan to the downside or to bring the dividend crowd to a stunned standstill by freezing dividends for the next few years alongside doing a massive equity issuance. Of course companies including utilities, sometimes learn the hard way as we saw with Algonquin Power & Utilities Corp. ( AQN ) where red flags were visible for a long time before they actually were forced to cut. We continue to rate this a Sell.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Emera: Dividend Freeze Would Actually Be The Best Outcome