EEX - Emerald: New Consumer Live Events And Economies Of Scale Imply Undervaluation

2023-08-21 10:42:40 ET

Summary

- Emerald is a B2B trade show company in the United States.

- The company's business model is based on connections, content, and commerce, with a focus on trade shows, conferences, digital spaces, and e-commerce platforms.

- Emerald's financials show strong liquidity and a focus on organic and inorganic growth, with potential for stock repurchases and the use of digital tools.

Emerald Holding, Inc. ( EEX ) may obtain significant revenue traction and cash flow growth thanks to the recent consumer live events, NBA Con and the popular Overland Expo series. Also, with highly positive trends in both attendees and pricing as well as recent financing received, I believe that there is significant optimism around the business model of EEX. Even taking into account risks associated with the total amount of debt or failed M&A integration, I think that EEX is trading quite undervalued.

Business Model

Emerald is a B2B trade show company in the United States. Its business is based on three key elements: connections, content, and commerce. The base of operations is given by the organization of fairs, conferences, digital spaces for interaction between businesses, live events, content creation, insights for different industries, digital tools, and e-commerce platforms among others.

From its founding to date, Emerald has achieved more than 20 acquisitions of other key players in the B2B trade show market, which is a highly fragmented market in the United States.

The company divides its business model into four reportable segments: commerce, design, creativity, and marketing others and those of corporate activity. The latter is an exclusive segment for the financial situation of the company and its management. The segment of others is for the provision of minor services in the generation of events and interaction platforms for business developers.

The strong points in this aspect are the commercial segment and the design and marketing segment. Both cases deal with the organization and production of events, but with small differences. The commercial segment specifically targets licensing, merchandising, retail distribution, and marketing coverage that enable professionals to make decisions based on reliable information and understanding of consumer demands. The design and marketing segment is dedicated to the production of events that include a wide variety of participants from different industries, with the aim of connecting professionals with new products, and other businesses.

In addition to these trade shows, Emerald also offers the creation of content and the administration of digital media aligned with the interests of each of the fairs and their main themes. Ultimately, the company has a management service and digital merchandising and e-commerce solutions for fair participants.

I believe that it is a great moment to review the financials of Emerald, not only because of the current valuation, but also because of the recent earnings momentum. In the most recent quarter, management noted that scalability and efficiency are expected to bring substantial revenue growth in this year and the next.

The strong recovery in live events is continuing to drive double-digit growth at Emerald, with highly positive trends in both attendees and pricing. The work we’ve done to drive scale and efficiency by centralizing key functions and investing in our technological capabilities has made Emerald a powerful platform for both internal and external growth. By leveraging the investments we’ve already made, we expect to continue to drive both substantial revenue growth as well as meaningful margin improvement in this year and next. Source: Quarterly Press Release

Balance Sheet

As of June 30, 2023, the company reported cash and cash equivalents of close to $204.7 million, trade and other receivables worth $92.2 million, prepaid expenses and other current assets of $17.6 million, and total current assets close to $314.5 million.

Non-current assets include intangible assets worth close to $189 million, goodwill of about $553.9 million, right-of-use lease assets close to $11.1 million, and total assets of $1.072 billion.

The ratio of current assets/current liabilities is larger than 1x, so I believe that liquidity does not seem a problem right now. The asset/liability ratio is also close to 2x, which means that the balance sheet is quite solid.

Source: 10-Q

The list of liabilities does not really seem worrying. The largest liabilities are accounts payable worth $50.2 million, deferred revenues of close to $162.4 million, contingent consideration worth $0.5 million, and term loan of $398.9 million. Finally, with deferred tax liabilities worth $2.6 million and right-of-use lease liabilities close to $10.6 million, total liabilities are equal to $647.6 million.

Source: 10-Q

The total amount of debt is not small, so investors may need some more information about the loans. As of June 30, 2023, the company reported a loan facility worth $403 million with interest of about 10.2%. With this in mind, I assumed a cost of capital of 11%, which I believe is conservative.

Source: 10-Q

Competitors

Competition is high and fragmented, with around 9,400 fair organizing companies participating in the market. Companies with a similar infrastructure and positioning are Reed Exhibitions, Informa Exhibitions, and Clarion Events. The competition varies according to the type of industry that participates in the fairs and exhibitions, and in more than one case, the subsidiaries that organize these events are created by industry associations, with which it is difficult to overcome their attendance and participation. In addition, Emerald's online platform competes with other companies that offer similar software and services in that field.

DCF

Among the new information that investors may need to know, there is the new Extended Term Loan Facility for close to $415.3 million. In my view, even if the financial conditions received were not much better than in the past, more financing means, in my view, more confidence. As soon as shareholders learn that the company received more money from debt investors, equity investments may become more interesting.

On June 12, 2023 , our wholly-owned subsidiary, Emerald X, Inc. The aggregate outstanding principal amount of the Extended Term Loan Facility was approximately $415.3 million as of June 30, 2023. The Term Loan Amendment also replaced the interest rate applicable to the term loans with a rate equal to, at the option of Emerald X, (i) the Term Secured Overnight Financing Rate plus 5.00% per annum plus a credit spread adjustment of 0.10% per annum or (ii) an alternate base rate plus 4.00% per annum. Source: 10-Q

The company is primarily focused on generating organic growth by understanding and leveraging the drivers for increased exhibitor and attendee participation at trade shows and providing year-round services that provide incremental value to those customers.

With many years in industry, under my financial model, I assumed that Emerald acquired sufficient know-how to help clients generate incremental sales and expand their brand’s awareness in their industry. I believe that Emerald’s trade shows will help clients connect and develop relationships, which will most likely drive high recurring participation among exhibitors. In sum, recurrent participants will most likely enhance future FCF generation.

Also, with the previous experience of the company in the M&A markets and the fact that the trade show industry appears highly fragmented, I assumed that Emerald will most likely be able to acquire new businesses. In my view, inorganic growth may bring further FCF margin driven by economies of scale.

The trade show industry is highly fragmented, with the four largest companies, including Emerald, comprising only 9% of the wider U.S. market according to the International Globex Report 2022. This has afforded us the opportunity to acquire other trade show businesses, a growth opportunity we expect to continue pursuing. These acquisitions may affect our growth trends, impacting the comparability of our financial results on a year-over-year basis. Source: 10-Q

I would also be expecting further repurchase of stock in the coming years if the stock remains at the current price mark. In this regard, it is worth noting that Emerald acquired a significant amount of shares in the past, which may enhance the demand for the stock, and lower the cost of capital in the coming years.

In October 2022, our Board approved an extension and expansion of the share repurchase program, which allows for the repurchase of $20.0 million of the Company's common stock through December 31, 2023. We did not repurchase any shares of our common stock during the three months ended June 30, 2023. There was $3.0 million remaining available for share repurchases under the Share Repurchase Program as of June 30, 2023. Source: 10-Q

I also assumed that the use of digital tools and data-focused solutions will most likely accelerate the creation of leads, and may help allocate resources. Management did mention some of these new tools in the last quarterly report, and I saw that virtual events are expected to grow at close to 21% from 2020 to 2026.

Leveraging our shows as key market-driven platforms, we combine our events with effective industry insights, digital tools, and data-focused solutions to create uniquely rich experiences. Source: 10-Q

The global virtual events market is worth $75.21 billion in 2020 and is predicted to grow at a CAGR of 21.89 per cent to $366.5 billion by 2026. Source: Virtual Events Market | Size, Share, Growth | 2022 to 2027

Finally, I believe that the recently announced new consumer live events and Elastic e-commerce software suite will most likely serve as cash flow catalysts in the coming years. The following lines were found in a recent press release.

Our recent expansion into consumer live events, including NBA Con and the popular Overland Expo series, is helping to unlock new audiences for Emerald that will complement our core B2B portfolio. In addition, our investment into value-add products like our Elastic e-commerce software suite is driving ever greater value for our customers, which we expect to become a meaningful contributor to our strong cash flow generation over time. Source: Quarterly Press Release

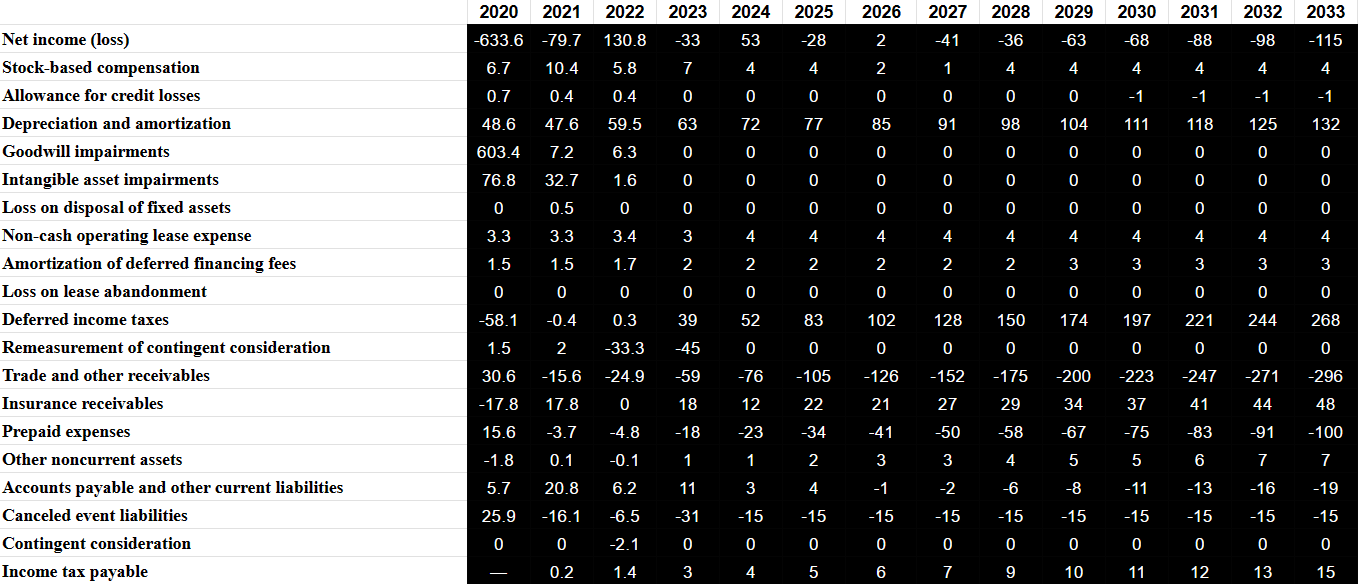

Considering the previous assumptions, I designed a DCF model from 2023 to 2033, and I used numbers that were close to the figures reported by the company in the past. I made forecasts for the next ten years. Most LBO and cash flow models these days include estimates of about ten years.

Source: Ycharts Source: Ycharts

{kind=link}

{kind=link}

My financial model included 2033 net income of about -$115 million, stock-based compensation close to $4 million, 2033 allowance for credit losses of -$1 million, depreciation and amortization worth $131 million, and non-cash operating lease expense of about $4 million.

Also, with amortization of deferred financing fees worth $2 million, deferred income taxes worth $268 million, insurance receivables close to $47 million, and prepaid expenses of -$100 million, I assumed accounts payable and other current liabilities worth -$19 million, canceled event liabilities of -$15 million, and income tax payable of $14 million.

{kind=link}

Besides, with deferred revenues worth $121 million, operating lease liabilities close to -$17 million, and other noncurrent liabilities of $30 million, 2033 CFO would stand at $59 million. Finally, if we also assume purchases of property and equipment of close to -$7 million, 2033 FCF would be close to $52 million.

{kind=link}

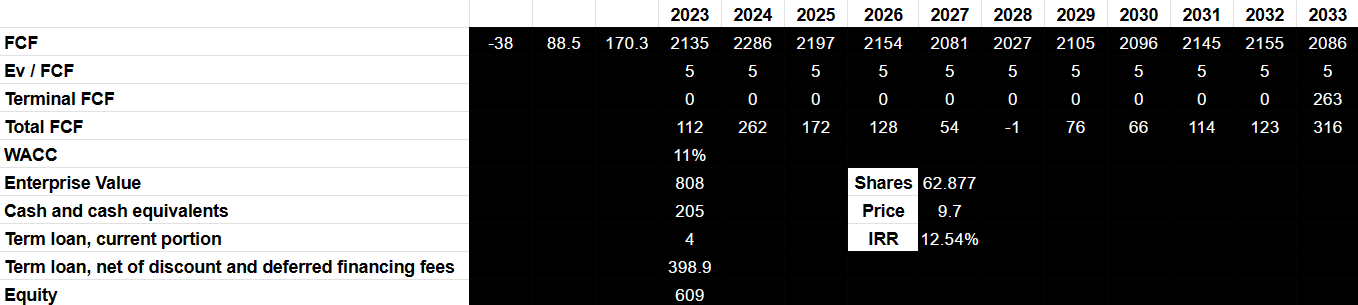

If we assume a conservative EV/FCF close to 5x and a WACC of 11%, the enterprise value would be close to $807 million. Now, using the cash and cash equivalents reported in the last quarter of $204.7 million, current term loan of $4.2 million, and long term loan of $398 million, the implied equity stands at about $609 million. Using the current stock price and the implied fair price obtained of close to $9.7 per share, I obtained an internal rate of return of about 12.54%.

{kind=link}

Risks

Currently, the historical nature of B2B fairs is changing due to two fundamental factors: the consequences of the covid pandemic, which significantly reduced attendance at face-to-face events, and the growing offer of digital options that replace such types of events. The projection is that this trend will continue to deepen. Although it means a risk factor for the company, recent strategies for the development of digital offers and solutions may be a way to overcome them.

When it comes to operational risks, the inability to read market trends or bring major players from each industry to your shows can be a risk factor. Mainly, it must be considered that 25% of the company's annual sales are concentrated in the 5 main fairs it organizes. This lack of diversification could have consequences in the future.

Another relevant factor is that Emerald, during December 2022, ceased to be considered a start-up, which will lead it to incur higher costs, and the inability to manage this may affect the company's activities. In this sense, the management of the integration of future acquisitions that are a key part of the development strategy for Emerald represents another latent factor.

Ultimately, the company reports an inconsistent situation in its financial debt that could complicate access to future lines of credit or financing, and this factor together with the growth of the costs of ceasing to be a start-up may lead to reorganization of the business structure or generate cuts in some areas of the business.

My Takeaway

Emerald recently announced expansion into consumer live events, such as NBA Con and the popular Overland Expo series, which may serve as revenue catalysts in the coming years. Besides, management also announced highly positive trends in attendees and pricing as well as recent financing, which may enhance demand for the stock. I did find certain risks with regard to the total amount of debt, lower demand for trade shows, or failed M&A attempts. With that being said, I believe that Emerald appears quite undervalued.

For further details see:

Emerald: New Consumer Live Events And Economies Of Scale Imply Undervaluation