TAN - Emeren Group: Pivot Outside China Can Unlock Value

2023-04-04 07:31:30 ET

Summary

- Emeren Group has changed its name from "ReneSola".

- The company is expanding outside of China, targeting new solar development projects across Europe and the U.S.

- An outlook for strong earnings growth in 2023 is bullish for the stock.

Emeren Group Ltd. ( SOL ) recently rebranded from "ReneSola" reflecting a broader focus on renewable energies including battery storage. Indeed, while the bulk of the company's solar power production assets is still in China, the corporate refresh also signifies a global ambition, targeting solar project opportunities in Europe and the U.S.

The company recently reported its latest quarterly results capping off a challenging yet resilient year. Even as shares have underperformed the solar industry over the past year, the attraction here is an outlook for accelerating earnings momentum in a market segment benefiting from several tailwinds. We like SOL with a sense the ongoing diversification outside China should help the company unlock value with a positive long-term outlook.

SOL Earnings Recap

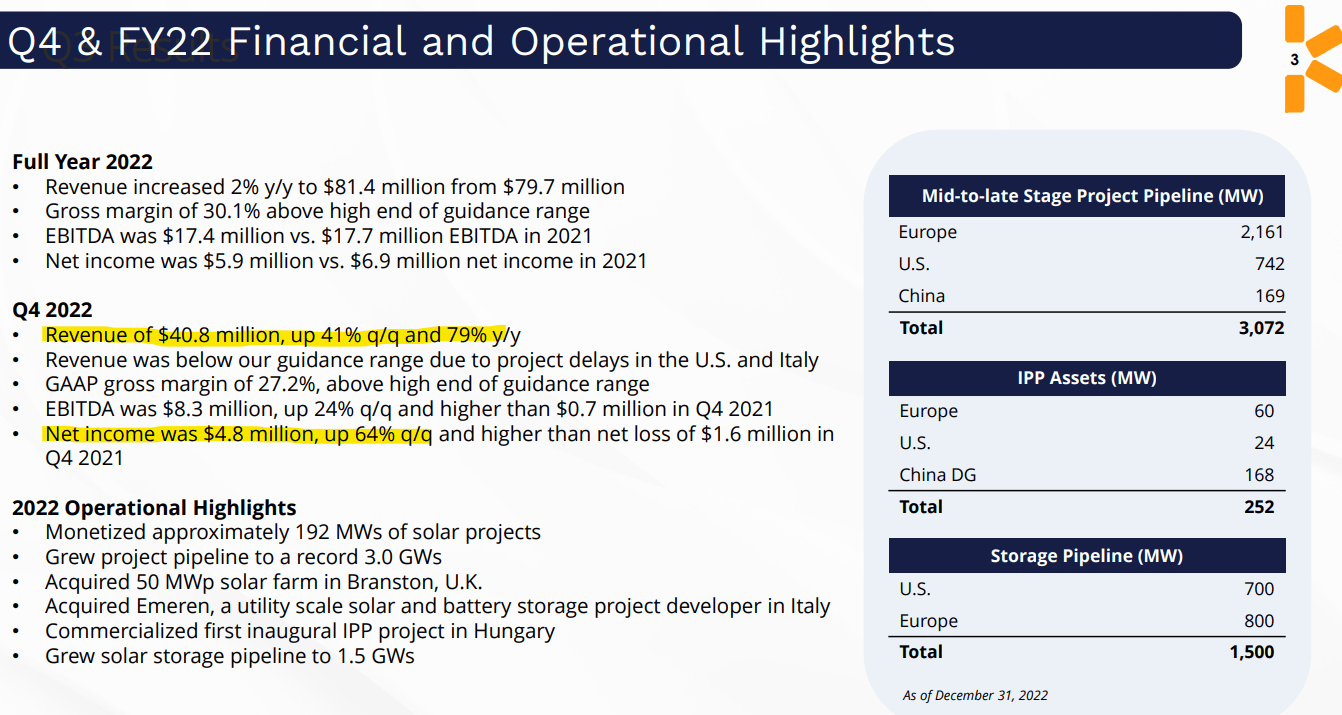

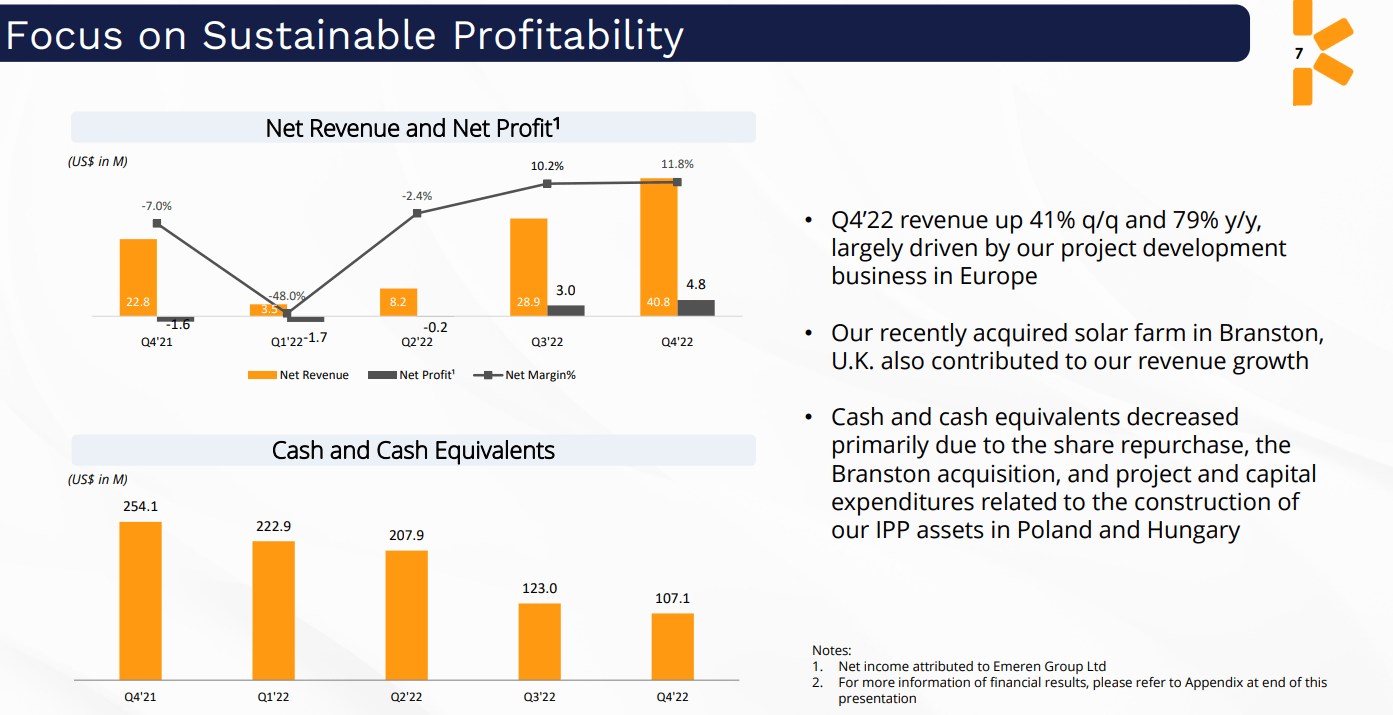

SOL reported Q4 EPS of $0.08 which was $0.01 ahead of market expectations. Revenue reached $41 million, up 79% year-over-year, although slightly below previously issued guidance based on the timing delays of ongoing projects.

For context, revenue and earnings have been volatile over the past year based on themes like supply chain disruptions, inflationary cost pressures, and rising interest rates. Full-year revenue of $81 millio n was up 2% y/y, while 2022 EPS of $0.08 fell from $0.22 in 2021.

Nevertheless, the takeaway here is the stronger second half of the year including the solid Q4 where EBITDA of $8.3 million climbed from just $0.7 million in the year prior. The improving financial backdrop is expected to extend through 2023.

{kind=link}

Operationally, the story has been the growing monetization of solar project deployments, selling 192 MWs in 2022 compared to 128 MWs in 2021. Within this amount, nearly 80% was outside of China in a strategy to diversify the company's global footprint.

The new company name is carried over from the 2022 acquisition of "Emeren", an Italy-based utility-scale solar power project developer and an emerging leader in battery storage projects with over 2.5 GW of projects under development.

The deal worked to expand the company's presence in Europe. That also includes a separate acquisition of a 50 MW solar farm in Branston, United Kingdom which is part of an effort to add an independent power producer ((IPP)) segment, generating stable cash as a complement to the core project sales business. On this point, the company also commercialized its first self-developed and self-constructed IPP project, a 10 MW facility in Hungary.

{kind=link}

We mentioned the shift in strategy as it relates to China. This was a topic discussed by management during the conference call , suggesting a focus on just five providences with the most favorable operating environment compared to a prior effort working in 12 or 13 regions. A plan to sell assets and consolidate the business there is expected to help strengthen the balance sheet following the 2022 European deals.

Overall, there are several moving parts setting up some optimism for a strong 2023. Emeren is targeting 2023 full-year revenue between $140 and $160 million, representing an 84% increase compared to 2022. The company also sees a 2023 net income between $17 and $21 million. At the midpoint, the forecast represents an increase of 222% compared to 2022.

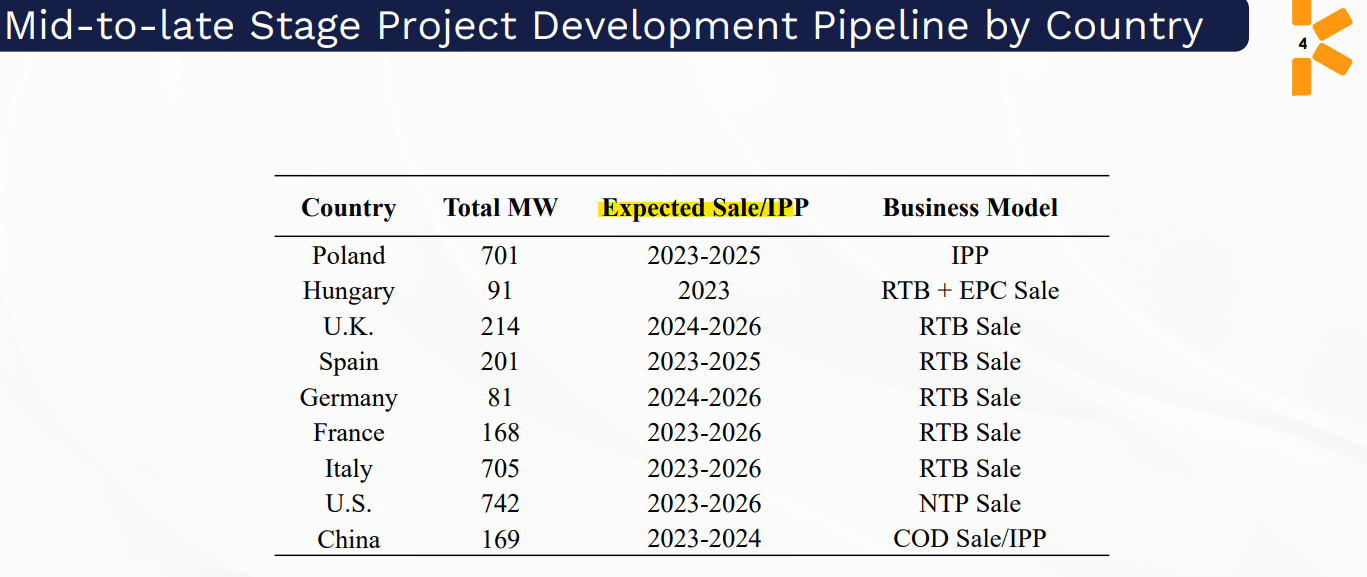

Again, this is based on the ongoing expansion into Europe where the visibility is supported by several mid-to-late stage projects, where 400 to 450 MW are expected to be monetized this year. Going forward, management has a target to monetize a minimum of 500 MW to 600 MW per year beyond 2023.

{kind=link}

Is SOL a Good Stock?

There's a lot to like about Emeren as a high-growth company with overall strong fundamentals. Countries around the world are accelerating the adoption of solar technology, and Emeren is well-positioned to capture demand for new renewable energy projects in an ever-increasing range of applications.

Even though the company faced a rocky last couple of years, the latest trends confirm the financials are finally turning a corner. In this regard, the timing of the corporate refresh and strategy shift into IPP opportunities supports a positive outlook that should also be reflected in generating value for shareholders.

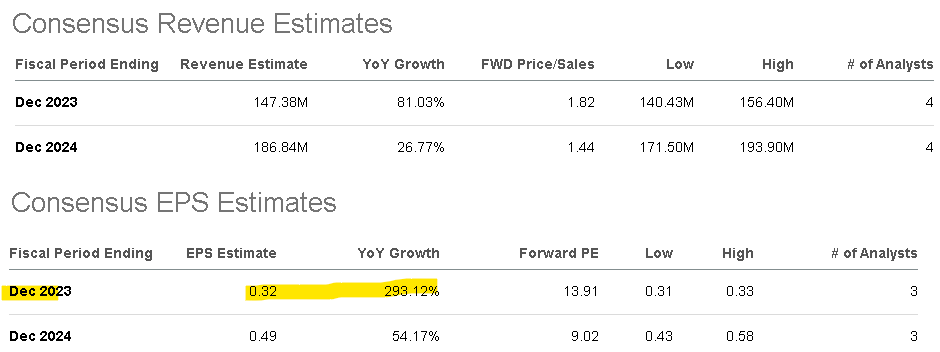

According to consensus estimates, the forecasts for 2023 are in line with management guidance between an 81% revenue growth and a path for EPS to reach $0.32. The momentum is expected to be retained into 2024 with the market penciling in a 27% top-line increase and 54% higher earnings. These are impressive targets and a good starting point for the company to move forward.

{kind=link}

As it relates to valuation, SOL stands out as trading at a deep discount to solar industry peers based on its earnings multiples. The metric we're looking at is SOL's enterprise value to forward EBITDA ratio of 7.4x, significantly below names like SunPower Corp. ( SPWR ) at 18x, SolarEdge Technologies ( SEDG ) at 22x, Maxeon Solar Technologies Group, Inc. ( SHLS ) at 27x, or Sunnova Energy International Inc. ( NOVA ) at 32x.

The explanation here goes back to Emeren's "Chinese" profile with the dynamic of Chinese companies typically trading at a large valuation spread relative to global names. That's also the case with Chinese solar panel manufacturer JinkoSolar Holding Co., Ltd, ( JKS ) trading at a 9.4x multiple.

The key to recognizing is that each of these companies focuses on different segments or levels of the solar supply chain. It's fair that the more "tech" type companies able to generate higher gross margins like Enphase Energy, Inc. ( ENPH ) deserve a premium.

At the same time, the argument we have is that Emeren is simply undervalued and the market has yet to appreciate its increasing exposure outside of China. Looking out over the next 3-4 years, Emeren will likely have a larger presence outside of China allowing its valuation to converge higher with the group as part of the bullish case for the stock.

SOL Stock Price Forecast

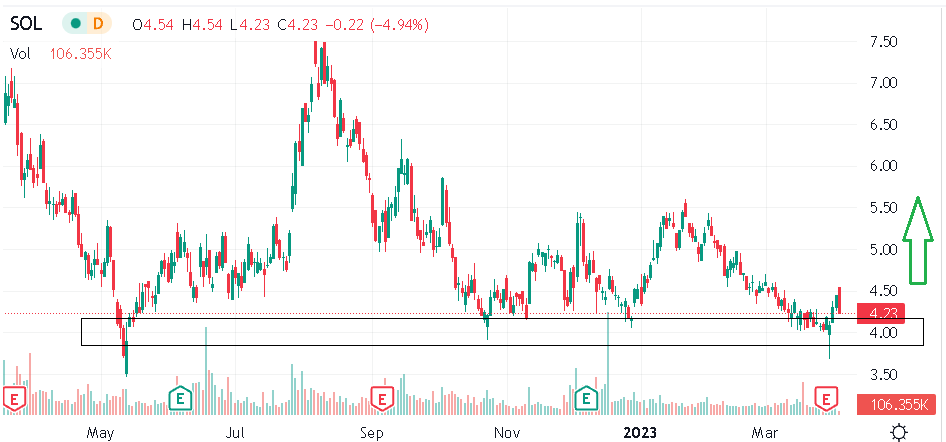

We rate SOL as a buy with a price target for the year ahead at $6.00 representing a 20x multiple on the current consensus 2023 EPS or 10x on an EV to forward EBITDA multiple. In our view, the recent weakness in shares down near their 52-week low offers a good entry ahead of a rebound higher.

In terms of risks, there is a component to underlying project development demand that is cyclical and exposed to broader macro conditions. A deeper deterioration of the economic environment would likely undermine growth projections with potentially weaker-than-expected results would open the door for a leg lower. Monitoring points over the next few quarters include trends in the gross margin and the evolution of the MW pipeline.

{kind=link}

For further details see:

Emeren Group: Pivot Outside China Can Unlock Value