KEYS - Emerson Puts NI In Play As It Looks To Continue Its Growth Transformation

Summary

- Emerson has gone public with its desire to acquire T&M company NI at $53/share.

- NI has thus far rebuffed Emerson, but recently announced a "strategic review" process that could bring it to the negotiating table.

- Expanding into T&M is consistent with Emerson's stated goals of transforming itself into a higher-growth industrial company leveraged to drivers like automation, electrification, and software.

- I believe a price closer to 18x '23 EBITDA could get a deal done; derisking a self-improvement plan for NI shareholders, but creating both opportunities and risks for EMR.

“I shoulda taken the money” Nick Chinlund as Toombs; The Chronicles of Riddick (2004)

After years of seeing NI ( NATI ) (previously known as “National Instruments”) management coming up short of their own self-improvement targets and lagging rival Keysight ’s ( KEYS ) share price performance, I can understand why Emerson ( EMR ) would take its proposed acquisition of this test & measurement (or T&M) straight to the shareholders in the hopes of applying some pressure to the board to come to the bargaining table. Were Emerson willing to pay a high-teens EBITDA multiple, I think it would be foolish of them not to seriously consider an offer.

For Emerson, this looks like a logical, if risky, expansion into a high-value adjacent market. Expansion into T&M, particularly on the development/validation side and with meaningful controller and software capabilities, is not only consistent with Emerson’s relatively recent investor day presentations, but also in keeping with management’s goal to shift its focus to higher-growth, higher-value products and services. I do think there’s a deal to be done here, but Emerson’s willingness to pay steep multiples to build its “Industrial 2.0” portfolio (including software and automation assets) does at a minimum increase the pressure on management to execute on these opportunities.

The Proposed Deal

After some rumbling in the media and trade journals, as well as NI announcing a “strategic review on January 13, Emerson went public on January 18 with its interest in acquiring NI, announcing a $53/share bid that values NI at around $7.4 billion. Emerson chose to go public after initially making an unsolicited $48/share bid in May of 2022 and having no success in trying to engage the board in M&A discussions since then.

At $53/share, Emerson would be offering a little more than 15.6x my FY’23 EBITDA estimate, and I would argue that based upon prior transactions in the T&M space, NI’s margins/returns, and the potential for self-improvement at NI, this is really just an opening bid.

As far as commentary from both companies goes, NI has played it relatively cool and has spared us all the performance theatre and pearl-clutching hysterics of pretending that Emerson’s offer is insultingly low. For Emerson’s part, the press release leans a little heavy on piffle meant to stir up the shareholders, but then I can also understand why Emerson management would be frustrated if NI has refused to have meaningful discussions in the past.

Given that NI has publicly opened the door (the strategic review), there may at least now be a face-saving path for NI’s board to engage in discussions with Emerson, and perhaps other potential suitors.

Why Emerson Would Do This Deal

As I said, T&M is an area that Emerson has targeted as a high-priority adjacency/area of focus, and it fits with the efforts that the company has undertaken to refocus around automation and industrial software. Not only is there leverage here to less-cyclical design/test functions, but also growing recurring software leverage and opportunities to play more directly in secular growth markets like wireless communications (5G/6G), networking (800G and beyond), leading-edge semiconductor production, EVs, and aerospace/commercial space.

NI has a strong presence already in EV/ADAS, including simulation and validation assets, as well as software, and appears to be particularly strong in battery design and test. Given the likely scale of growth in EV batteries over the coming decades, it makes sense to play here, to say nothing of the opportunities in 5G/6G, space, and semiconductors (RF/analog/sensors).

Emerson does have some complementary assets, including Ovation digital twinning and some sensor/controller products, but for the most part this would be a new venture. NI has attractive products like its PXI controller, and I believe there would be multiple cross-selling opportunities here – Emerson could sell more existing automation and software offerings into verticals like autos, aerospace, semicon, and wireless, as well as bring NI’s T&M capabilities into those markets where Emerson has more established presences.

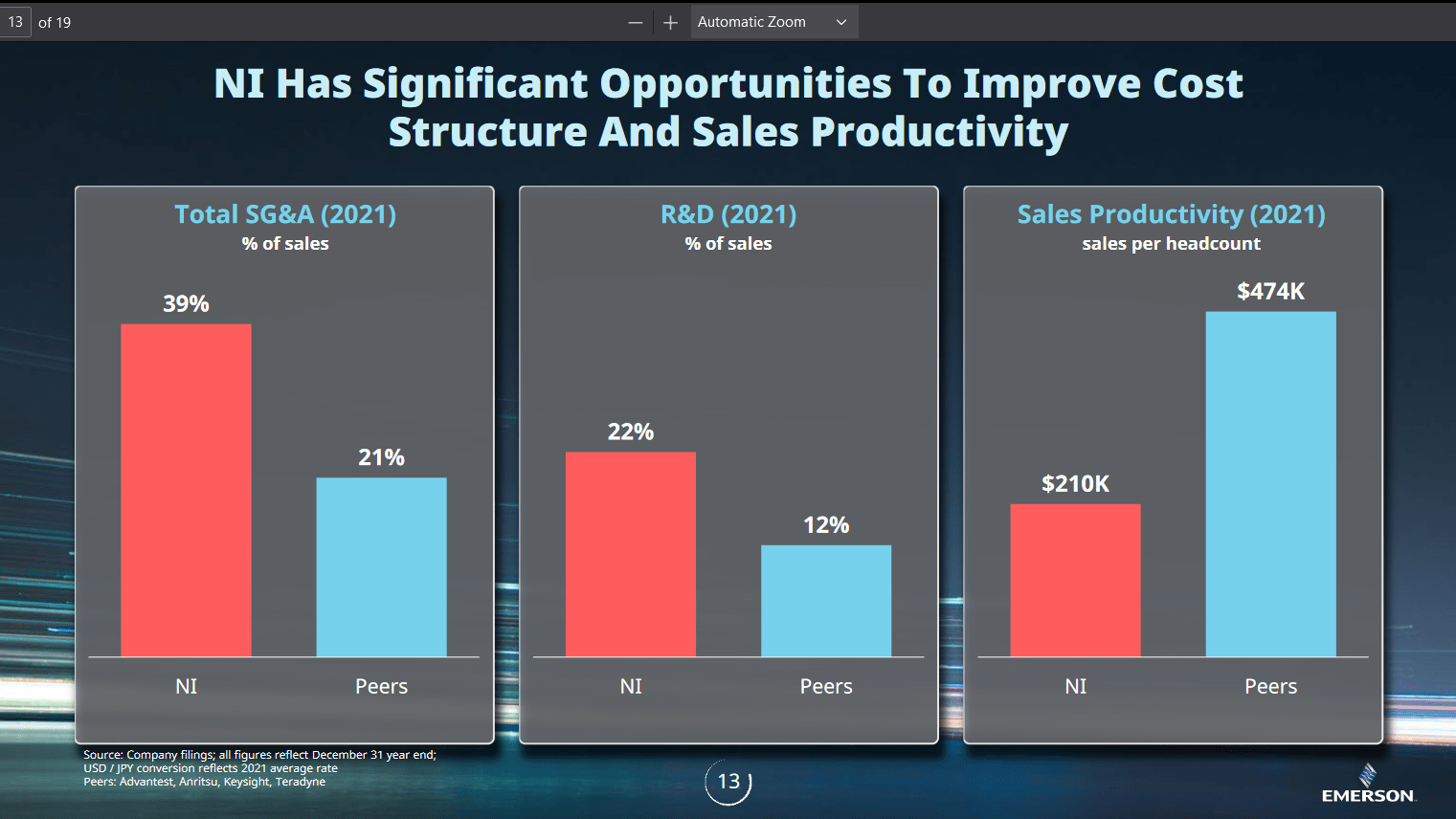

Emerson management has also talked of financial synergies from the deal. To be sure, there is room for meaningful improvement at NI. As highlighted by Emerson in their presentation, NI lags in areas like SG&A and sales efficiency, and their R&D productivity is subject to debate (analyzing T&M companies on R&D/revenue without further context is tricky).

{kind=link}

I’d also note that while Keysight has generated a long-term trailing average FCF margin of 16%, NI’s is closer to 10%. My estimate for EBITDA margin in 2023 is 400bp higher for Keysight, my operating margin estimate is about 600bp higher, and my ROIC estimate is about 15pts higher as well. NI has acknowledged some of these deficiencies in the past and is underway with a multipoint plan to improve (based upon better end-market exposures and go-to-market execution), but management here doesn’t have the greatest track record of hitting its own targets.

One other, somewhat snarky, comment on Emerson’s proposed synergies – while I do see meaningful room for improvement at NI, and I think Emerson management is solid on execution, the lack of engagement and due diligence (Emerson hasn’t been given access to NI’s books) does reduce my confidence in those projections to some extent.

The Outlook

I like Keysight and at the right price I like NI as well – I think electronic design and test systems are a good place to be, and I like the opportunity to not only leverage secular growth trends (data traffic growth, chip complexity, electrification and automation in autos, buildings, factories, et al, and commercial space) but drive value from increased software penetration. Likewise, I think NI has at least in some respects failed to live up to its potential and it’s a logical growth-driven M&A target for Emerson.

If Emerson (or another acquirer) is willing to pay 18x ’23 EBITDA, that’s a deal that I think has to be very seriously considered and weighed against a sober assessment of just how much self-improvement NI can really drive over the next three to five years. Whether 18x is a good deal for Emerson would be the subject of a different article; I think it would likely be a stretch, but it’s hard to buy your way into businesses with compelling long-term prospects at low multiples.

On its own, I’m looking for NI to generate around 8% long-term revenue growth and strong low double-digit FCF growth. I feel like both 8% long-term growth and FCF margin improvement toward 20% give plenty of credit for self-improvement potential, as well as NI’s leverage to attractive secular growth markets (and other drivers like increasing software attach).

On a standalone basis, those cash flow assumptions don’t really drive an attractive DCF-based fair value, but I wouldn’t expect that to be the case given that NI shares are now in play. Likewise, while I think 16x would be a fair near-term standalone EBITDA multiple, I think 18x is probably more appropriate in an M&A context.

The Bottom Line

If I’m right and 18x is a fair price, and somebody is willing to pay that (whether Emerson, Fortive ( FTV ), or some other acquirer), there would be close to 15% upside from here. That’s not too bad, particularly as a deal would likely come within a few months. Absent a deal, I do see some risk here to weaker sentiment around semiconductor demand/volumes in FY’23, as well as a general slowdown in the broader economy and management’s ability to execute on its self-improvement plans.

For further details see:

Emerson Puts NI In Play As It Looks To Continue Its Growth Transformation