DRVN - Emeth Value Capital H2 2023 Letter

2024-02-11 05:45:00 ET

Summary

- One of the great challenges in public markets investing is that the feedback loop between process and outcome can at times be painfully long.

- Mathematically, over the extreme long run, an investment in a stock earns the return of the business that underlies it.

- It seems that in a market that is prone to irrationality, starting from a baseline of rationality can be a dangerous proposition.

{kind=link}

Foreword

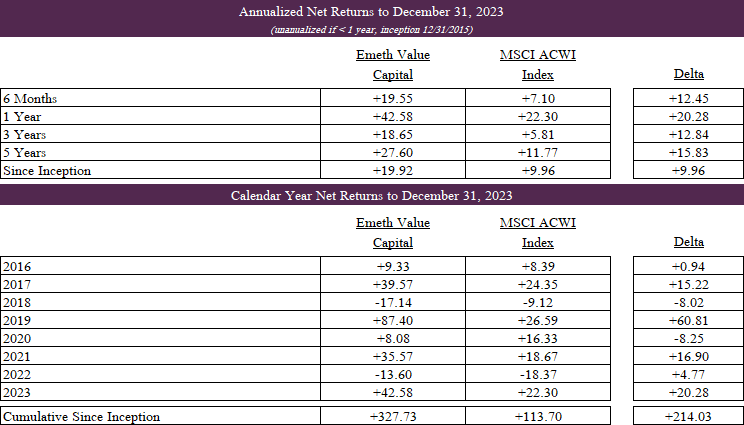

I intend to share the updated results at the outset of each letter. It is worth reiterating that I ascribe little significance to short term results. I look out many years when making investments for the partnership and believe our results are best weighed using a similar time horizon.

A Dangerously Reasonable Price

I've made the comment before that the value investing industry has had irreparable damage and is unlikely to recover in a material way. But the corollary of that is that value investing for those that remain, I think is an extraordinarily exciting time. Let me explain the way that I would have tended to look at things a long time ago, which our business was buy things that are sort of cheap, figure out that they are going to be a bit better than the world generally understands, and wait. So the very simple math is if a stock is $10 and the world thinks it's going to earn a buck, and you think it's going to earn $1.15… and you wait for a year and they've made $1.15 instead of a buck and now it looks like they'll earn $1.35 the following year, and you get a 13x multiple on the $1.35 and you paid a 10x multiple on the $1, then you've just made 60-70% over 18 months. Now, if you play out that same story today, it's an 8x multiple instead of 13x, and at the end of that 18 months you'll have made 6% on you money not 60%. The problem is those fundamental buyers simply aren't there anymore, they've been turned passive. So, where does that leave us and how have we adjusted our strategy? What we're doing now is we're saying, what do we have to do to make a good return if a tree falls in a forest and nobody is there to hear it? You have this enormously bifurcated market, there is a wasteland of companies where literally nobody's paying attention and nobody's following. So, instead of buying at 10x earnings because you think earnings are going to be x in the future, you can buy that same type of situation at 5x earnings, and at that point what others think matters less. If companies are taking the vast majority of that earnings yield and giving it back to you in dividends or buybacks, this has to work itself out over time in a favorable way.

You have to build a portfolio of companies that are so cheap and so unloved it will be difficult to lose. (David Einhorn)

One of the great challenges in public markets investing is that the feedback loop between process and outcome can at times be painfully long. We know, mathematically, that over the extreme long run an investment in a stock earns the return of the business that underlies it. However, in practice, the journey rarely feels so consonant. One of the principal reasons for this is that in the initial stages of compounding, when an investment's growth is still somewhat linear, stock performance is far more influenced by multiple expansion or contraction rather than fundamental performance.

Consider a hypothetical investor who pays a market multiple, or 16x, for stock in a company they believe can sustainably compound earnings at twelve percent per annum; in other words, a reasonable price for a business that grows at double the long-term market average.

{kind=link}

While oversimplified, one way we can frame the process-outcome disconnect is as a measure of time. The graphic above calculates how many years of compounding are "lost" based on certain levels of growth and multiple compression. If we assume our hypothetical investor's analysis is flawless, and that indeed the business does compound earnings at twelve percent per annum, the result is that more than six years of compounding would be erased if the multiple falls to 8x....

Emeth Value Capital H2 2023 Letter