EMF - EMF: Trade The China Re-Opening Via This EM Equity CEF

Summary

- Templeton Emerging Markets Fund is an EM equity closed-end fund.

- Chinese equities make up around 27% of the fund, followed by South Korea and Taiwan at 17% and 14%, respectively.

- The fund focuses on large capitalization stocks.

- The fund is trading with an -11% discount to net asset value.

- This article covers CEFs.

Thesis

Templeton Emerging Markets Fund (EMF) is an EM equity closed end fund. The vehicle invests in large capitalization stocks that are issued by corporations incorporated in an EM jurisdiction. As per its literature:

The fund seeks long-term capital appreciation by investing, under normal market conditions, at least 80% of its net assets in emerging country equity securities.

Chinese equities make up around 27% of the fund, followed by South Korea and Taiwan at 17% and 14% respectively. The issues associated with de-listing fears for Chinese ADRs are well documented, but these have been mitigated by the recent developments which has seen the relevant U.S. regulatory bodies having gained access to the necessary information. We are of the opinion that China understands its need to be able to access international capital markets when needed, via the NYSE, and thus will ensure that door stays open.

Technology and financials are the top sectors in the fund, accounting for over 50% of the holdings. From a performance standpoint the fund beats a plain vanilla ETF in the space, namely iShares MSCI Emerging Markets ETF ( EEM ). EMF does what it is supposed to do - takes EM equity exposure and transforms it into dividends with a slight outperformance versus a plain vanilla instrument, even after fees are priced in. However, the asset class as a whole is likely not properly compensating an investor for the risks taken. As it stands, EMF has posted an annual total return under 2% with a 21 standard deviation on a decade long window. That is disappointing, and makes it a cyclical instrument in our mind. Not a buy and hold. The fund's Sharpe ratio which is virtually zero, is reflective of this setup - not enough return to justify the volatility here.

EMF is best to be traded as a recovery asset class. From that angle the blood-letting we have seen in 2022 would indicate a good set-up for 2023. An informed reader is reminded that JP Morgan called Chinese equities un-investable earlier this year. We believe EMF is going to post a 10% plus total return figure in 2023 on the back of China re-opening and the recession finally getting fully priced in. Long term however this CEF is not a true buy and hold, especially from a risk/reward lens.

Analytics

AUM: $0.18 bil

Discount to NAV: -11%

Z-Stat: 0.8

Yield: 10%

St Dev: 21

Sharpe Ratio: 0.01

EMF Holdings

The fund has a China-centric allocation in its current format:

Country (Fund)

Over 27% of the portfolio is allocated to equities that are incorporated in China. South Korea and Taiwan come next with a 17% and 14% respective allocation. From a sectoral standpoint technology is the main portfolio concentration:

Sectors (Seeking Alpha)

The top 3 sectors account for over 60% of the fund's holdings. From an individual name standpoint we recognize most of the top names in this CEF:

Top Names (Fund Fact Sheet)

The fund is composed of large capitalization stocks mainly:

Market Cap (Fund Fact Sheet)

These are multinational, large, well known corporates, that just happen to come from an EM jurisdiction. The issues associated with Chinese ADRs listed in the U.S. are well documented, but we feel this is not a hot topic anymore, with the audit committee now finally having access to the requested information.

Performance

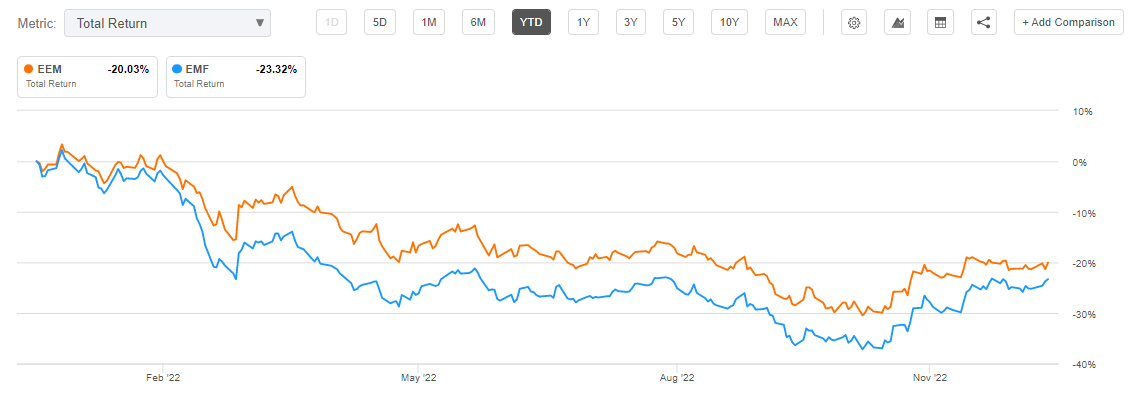

The fund is down -20% on a year to date basis:

{kind=link}

We are comparing the CEF's performance with a plain vanilla ETF, namely the iShares MSCI Emerging Markets ETF ( EEM ). The two structures have similar compositions from a geographic standpoint and an underlying company capitalization size.

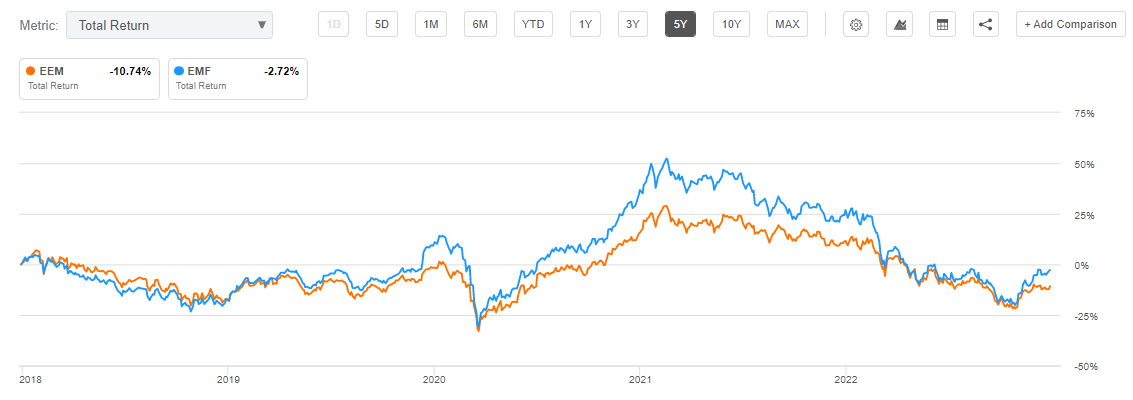

On a 5-year timeframe EMF outperforms:

{kind=link}

We can note that the CEF had a long time-frame during 2020/2022 when it was significantly ahead of the ETF from a total return perspective. As a reminder, the total return figures are the correct ones to look at here since CEF distribute capital gains via dividends. Just comparing prices would always put a CEF structure at a disadvantage.

We can observe the same dynamic on a 10-year basis as well:

{kind=link}

However, both funds are not very exciting from a total return perspective. Annualized total returns come at sub 2%, with a 21 standard deviation. Too little of a reward for a high volatility product.

Premium / Discount to NAV

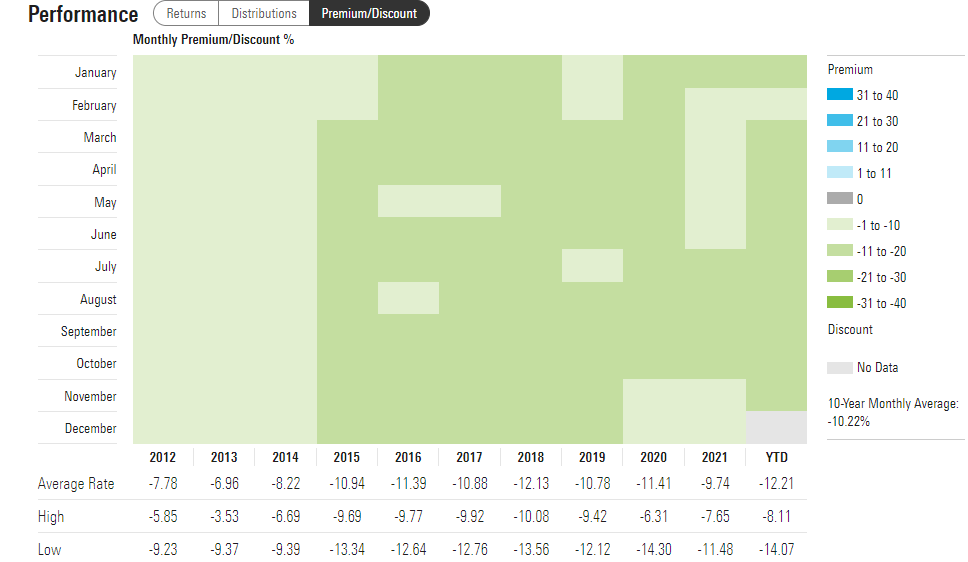

This fund has always traded with a discount to net asset value:

Premium/Discount to NAV (Morningstar)

{kind=link}

The current discount is pretty much in line with the average historical ones. We are of the opinion that the meager results displayed by this asset class are responsible for the CEF's market value being under its NAV. We usually see this for underperforming asset classes. Do not expect this fund to suddenly move to being flat to NAV from a market pricing perspective.

Conclusion

Templeton Emerging Markets Fund is an EM equity closed end fund. The vehicle invests in large capitalization stocks from emerging market jurisdictions. Currently, Chinese equities make up around 27% of the fund, followed by South Korea and Taiwan at 17% and 14% respectively. The fund is trading at an -11% discount to net asset value, but this level is in the middle of its historic range. EM equities have been an underperforming asset class, with EMF posting a sub 2% annualized total return in the past decade. EMF does beat a plain vanilla ETF in the space, but exhibits cyclical returns (i.e. not ideal as a true buy and hold vehicle). The CEF does what it is supposed to do in terms of transforming EM equity exposure into dividends, and in our mind will have a 10% plus total return in 2023 as China re-opens and the current recession gets fully priced in.

For further details see:

EMF: Trade The China Re-Opening Via This EM Equity CEF