WMB - EMO: A Solid Midstream CEF Trading At A Huge Discount

2023-05-17 13:03:01 ET

Summary

- Midstream partnerships have long been an excellent investment vehicle for anyone seeking income due to their high yields and general stability.

- ClearBridge Energy Midstream Opportunity Fund invests in a portfolio of these companies that includes most of the best companies in the industry.

- The EMO closed-end fund has somewhat underperformed the Alerian MLP Index, but it includes corporate entities that the index does not, so has a diversification advantage.

- The EMO fund yields 7.83% at the current price, which is easily sustainable.

- The fund is currently trading at a very attractive price.

For many years now, midstream master limited partnerships have been some of the favorite investments of income-focused investors. This makes a lot of sense because these companies are almost perfect for those looking to generate income from their assets. After all, these companies enjoy remarkably stable cash flows that can be paid out to investors. When we combine this with the fact that many of these companies have relatively low growth rates, the yield is usually a high percentage of the unit price because the market assigns them very reasonable multiples.

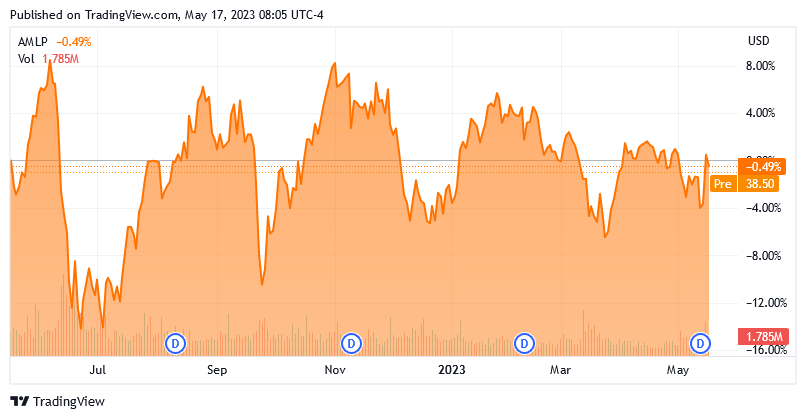

We can see these high yields reflected in the fact that the Alerian MLP Index ( AMLP ) currently yields a whopping 8.89% over the past year. It has also given a very respectable performance in a challenging market environment:

{kind=link}

Although the index has been down slightly over the past year, the total return is sharply positive because of the high yield. In fact, its total return is quite a bit higher than the S&P 500 Index (SP500) because of this yield. Master limited partnerships also enjoy tax benefits with respect to their distributions, as all distributions are taxed as a return of capital until the total distributions received exceed the investor's purchase price. Thus, taxes are usually deferred for several years after you purchase the investment, and even after that period has ended, you are still only taxed at the capital gains rate. This is something that will undoubtedly be appealing to any investor.

Unfortunately, there are a few problems with master limited partnerships as investment vehicles. The biggest of these is that due to their inherent tax advantages, it is difficult to include them in a retirement account or other tax-advantaged vehicle. In fact, having one in your retirement account could expose you to tax liability on behalf of your retirement account! In addition to this problem, it can be difficult to put together a diversified portfolio of these assets without having access to a considerable amount of capital, but that is not a problem that is unique to master limited partnerships.

Fortunately, there are some ways to solve these problems. One of the best ways is to purchase shares of a closed-end fund, or CEF, that specializes in investing in midstream companies. These funds are not really well followed in the investment media, so unfortunately most people are not going to be very familiar with them. However, they offer investors an easy way to acquire a portfolio of assets that can usually deliver a higher yield than any of the underlying assets possess. This second characteristic is something that might be very attractive to income-focused investors.

In this article, we will discuss the ClearBridge Energy Midstream Opportunity Fund ( EMO ), which is a closed-end fund that is in this category. As of the time of writing, it boasts a respectable 7.83% yield, which is admittedly lower than the index but is still more than sufficient for most income investors. We have discussed this fund before, but a few months have passed since that time, so obviously several things have changed. This article will focus specifically on these changes, as well as provide an updated analysis of the fund's financial condition. Therefore, let us investigate and see if the EMO fund could be a good addition to your portfolio today.

About The Fund

According to the fund's webpage , the ClearBridge Energy Midstream Opportunity Fund has the stated objective of providing its investors with a high level of total return. This is not surprising, since this is the objective that most master limited partnership closed-end funds have. After all, these funds typically invest in common equity securities issued by midstream companies, and this one is no exception. As we can see here, the fund's portfolio is entirely invested in common equities, with only a very small amount of cash:

CEFConnect

The reason that the fund's focus on total return is unsurprising is that common equity securities are by their nature a total return vehicle. After all, investors typically purchase these securities because they want to earn an income through the distributions and dividends that the issuing companies pay out, as well as benefit from capital gains as the companies grow and prosper. In the case of midstream companies, most of the total return comes in the form of direct payments to investors via either distributions or dividends. This is because midstream companies in general tend to be relatively low-growth entities, so investors cannot count on the capital gains that companies in high-growth sectors deliver. Thus, a midstream company compensates by paying out a high proportion of its cash flows to the investors. This allows them to deliver a reasonable total return even in the absence of growth.

After all, there are midstream partnerships that yield over 10%, such as Crestwood Equity Partners LP ( CEQP ), which is in the same ballpark as the S&P 500 Index's historic total return. The advantage here in favor of the midstream company is that you receive your return as cash and do not have to sell your assets if you want to spend money, as you would with most other common equities. There is also nothing stopping you from reinvesting the distribution in the same or a different company if you want to continue to build your assets.

In the introduction to this article, I stated that one of the appealing things about midstream companies is that they typically enjoy remarkably stable cash flows over time. This is due to the business model that these companies employ. A midstream company will enter into long-term contracts under which it agrees to transport a customer's hydrocarbon resources, such as crude oil or natural gas, through its infrastructure of pipelines and storage assets. In exchange, the customer compensates the midstream company based on the volume of assets that are transported, not on their value. This provides a great deal of protection against changes in resource prices, which is something that could be important today.

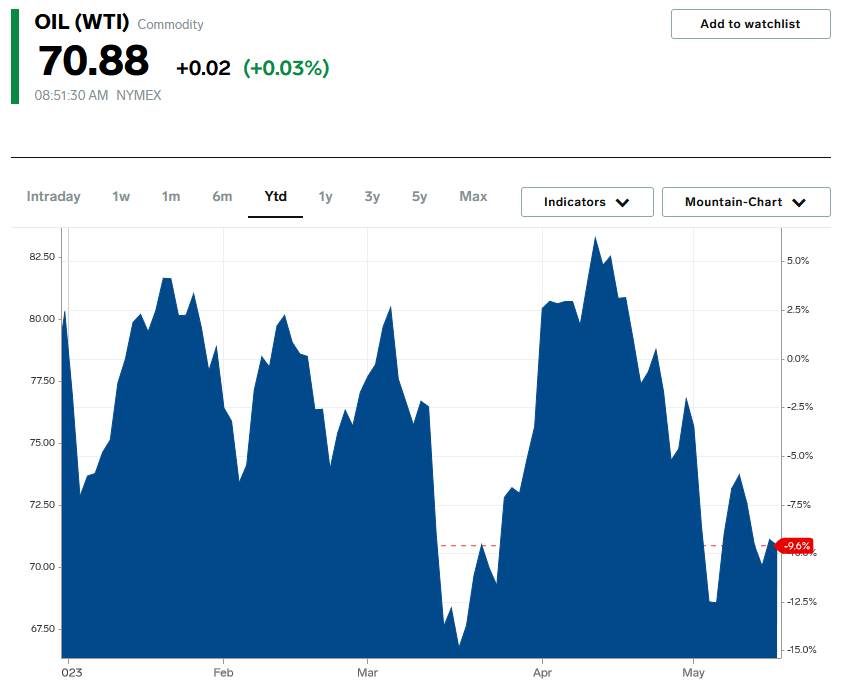

As I mentioned in a recent blog post , natural gas prices have fallen substantially year-to-date due to a supply glut that was triggered by an unusually warm winter and the temporary shutdown of a major export facility. Crude oil prices have also fallen on recession fears, as indicated by the fact that West Texas Intermediate crude oil is down 9.60% year-to-date:

{kind=link}

As I pointed out in numerous previous articles, most midstream companies were minimally affected even by the steep collapse in energy prices that occurred back in April 2020. It is highly unlikely that the cash flows of any of them will be very affected by today's market action. With that said, the price of the common units will be impacted, which only increases the yield. As income investors, we should welcome this, since we receive the majority of our returns through the distributions and dividends paid by the midstream companies. Those are unlikely to be cut due to the cash flow stability of these companies, so we should not have to worry too much.

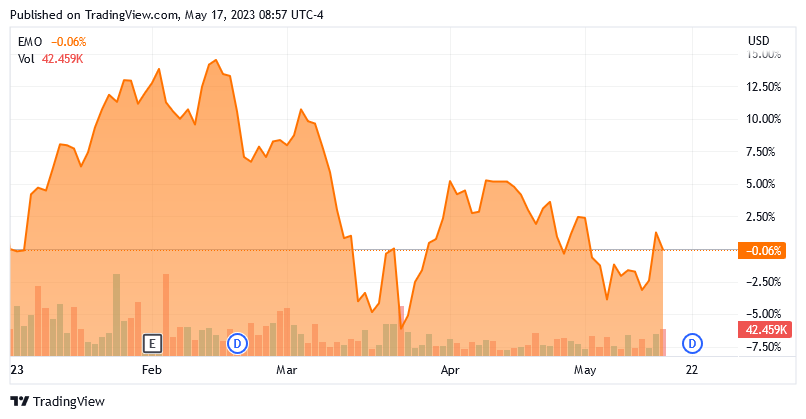

Despite the year-to-date weakness in energy prices, the ClearBridge Energy Midstream Opportunities Fund has held up surprisingly well. As we can see here, the fund's shares are only down 0.06% year-to-date:

{kind=link}

The fund has therefore had a positive total return over the period since the distributions that it has paid have more than offset this slight decline. The fund's webpage unfortunately does not include year-to-date performance, but it does show that the fund has delivered very positive total returns over the past one and three-year periods:

{kind=link}

The three-year period is not necessarily a good period to use to judge the fund's past performance. Three years prior to April 30, 2023, was the worst market for anything related to traditional energy that we have seen in a generation, and so anyone that bought then would have made fantastic total returns as the market rebounded following the end of the pandemic-driven lockdowns. It is very unlikely that we will experience such a perfect buying opportunity again in our lifetimes. The fact that the fund performed much better than the S&P 500 Index over the past year is inspiring, though.

As my regular readers are no doubt well aware, I have devoted a considerable amount of time and effort to discussing midstream corporations and partnerships on this site over much of the past decade. As such, the largest positions in the fund will likely be familiar to most readers. Here they are:

CEFConnect

I have published articles on nearly all of the companies on this list over the past few years. In fact, the only companies here that I have never discussed are Western Midstream Partners ( WES ) and Plains GP Holdings ( PAGP ). However, Plains GP Holdings is just the general partner for Plains All American Pipeline ( PAA ), which I have discussed numerous times. As such, it will probably be reasonably familiar to most readers. The remainder of these are certainly going to be familiar, which is nice as most of these are among the best companies in the sector. In particular, MPLX LP ( MPLX ) and Enterprise Products Partners L.P. ( EPD ) have been two of my top picks for several years, and their most recent results have not changed this conviction. Magellan Midstream Partners, L.P. ( MMP ) has recently been in the news due to an impending acquisition by ONEOK, Inc. ( OKE ), which will remove it from this list and almost certainly replace it with ONEOK. That is not a problem, as the combined company will probably be stronger than Magellan Midstream Partners is alone. Unfortunately, ONEOK is a corporation, so the acquisition will remove some of the tax benefits that the fund currently receives.

ClearBridge Energy Midstream Opportunity Fund's largest positions are the same as they were the last time that we discussed the fund, although the weightings of many of the companies have changed considerably. This could be caused by one company outperforming another in the market though and is not necessarily a sign that the fund has traded or exchanged any positions. For example, Magellan Midstream Partners has delivered a very positive performance ever since the announcement of the ONEOK acquisition that would have increased its weighting in the absence of any intervention by the fund's managers.

The fact that the largest positions in the fund have remained pretty similar over the past few months could lead one to believe that the fund has a very low turnover rate. However, this is not the case as the fund had a 60.00% annual turnover in 2022, which is about the average for an equity closed-end fund. The reason that this is important is that it costs money to trade stocks or other equities, which are billed to the shareholders of the fund. This creates a drag on the fund's performance and makes the job of the fund's managers more difficult. After all, management must generate sufficient returns to cover these extra costs and still provide a return that is acceptable for the fund's shareholders. There are very few management teams that manage to achieve this on a consistent basis, which is one reason why most actively managed funds fail to beat their benchmark indices.

As we saw earlier, this fund has underperformed the Alerian MLP Index over the past year, so it is certainly not an exception to this rule. That is unfortunate, as this fund does have a few advantages over the index, such as the fact that it can include a few companies that the index cannot because they are structured as corporations. The Williams Companies ( WMB ) is a great example of a very good midstream company that the index cannot include. Those investors that want the diversification that the fund can offer must settle for lower returns due to the higher costs of this fund, and that is a disappointment.

Leverage

In the introduction to this article, I stated that closed-end funds have the ability to employ certain strategies that boost the effective yield of their portfolios. When we consider that midstream companies and partnerships already have some of the highest yields in the market, this is something that can very quickly prove to be attractive. One of the strategies that the ClearBridge Energy Midstream Opportunities Fund employs to accomplish this task is the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase the common equity of midstream companies. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not have too much leverage because that will expose us to too much risk. I generally like a fund's leverage to be less than a third as a percentage of its assets for this reason. As is the case with most midstream closed-end funds, this one satisfies this requirement as its levered assets comprise 32.63% of the portfolio as of the time of writing. This is higher than many of the fund's peers possess, which is unfortunate, but it is still an acceptable level that should represent a reasonable balance between risk and reward. Overall, the ClearBridge Energy Midstream Opportunity Fund's leverage should not be anything that we really need to worry about.

Distribution Analysis

One of the biggest reasons why investors purchase midstream companies is because of the high yields that these entities usually possess. As already mentioned, the yield of the Alerian MLP Index, which only includes midstream master limited partnerships, is 8.89% as of the time of writing. That is higher than most other indices. The ClearBridge Energy Midstream Opportunities Fund invests in these companies and then applies a layer of leverage in order to boost its effective portfolio yield. As such, we might expect that the fund will have a very high yield.

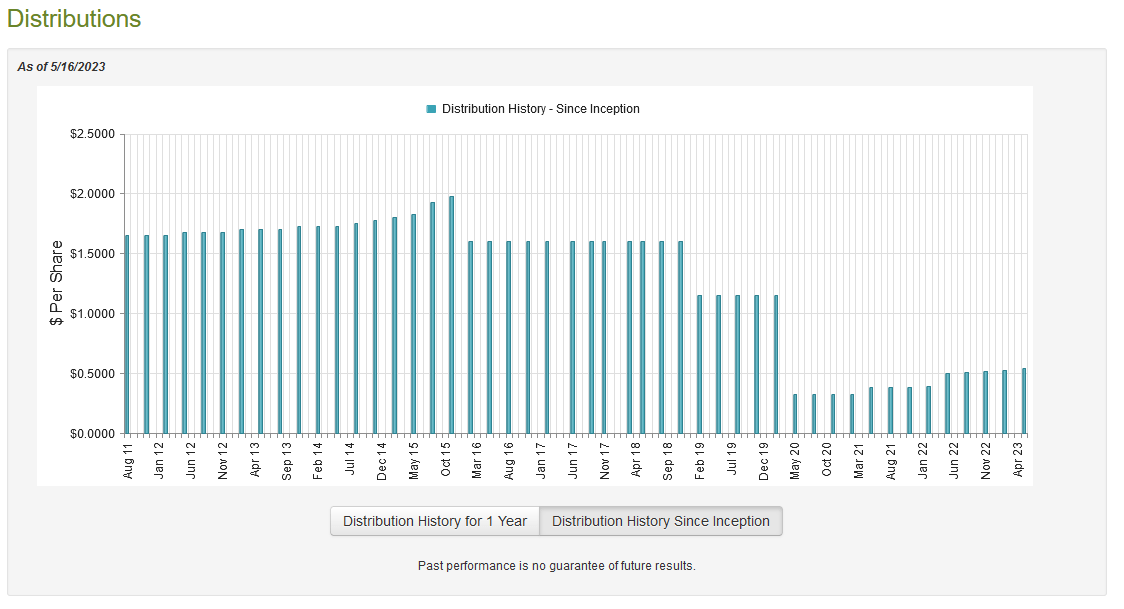

This is certainly the case, as the ClearBridge Energy Midstream Opportunity Fund pays a quarterly distribution of $0.54 per share ($2.16 per share annually), which gives it a 7.83% yield at the current price. That is certainly a reasonable yield for any income-seeking investor, although it is not quite as high as the index. Unfortunately, the fund has not been especially consistent with its distribution over the years:

{kind=link}

This history will likely prove to be rather unappealing to anyone that is seeking a consistent and secure source of income that can be used to pay their bills or finance their lifestyles. However, it is not unexpected as the midstream sector suffered through two crises over the period in question. The first came in the middle of the decade when Saudi Arabia attempted to bankrupt the American shale industry by artificially holding crude oil prices down. The second crisis was the COVID-19 pandemic, which crushed crude oil prices due to a steep decline in demand.

Although the cash flows of the companies in the fund were largely unaffected by either of these events, they still cut their distributions to strengthen their balance sheets as the market was generally unwilling to provide any needed capital. As such, the fund's income declined, and it was forced to cut its own distributions to weather the environment. That is all in the past though and anyone buying today will receive the current distribution at the current yield. As such, the most important thing is the fund's ability to maintain its distribution at the current level.

Fortunately, we have a reasonably recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on November 30, 2023. As such, the report will not include any information from the past few months, which is unfortunate as it would be nice to see how well it performed in the face of the year-to-date weakness that we have seen in the energy market. However, we still have enough to see how much it profited in 2022, as the energy sector substantially outperformed anything else last year.

During the full-year period, the ClearBridge Energy Midstream Opportunities Fund received $40,761,780 in dividends and distributions, along with $101,727 in interest on the cash that it had during the period. A sizable percentage of the money that the fund received came from master limited partnerships and so was not considered to be income for tax purposes. As such, the fund only reported a total investment income of $7,911,597 during the period. It paid its expenses out of this amount, which left it with a negative $5,597,287 available for shareholders. Obviously, this is nowhere close to enough to pay any distributions, let alone the $24,902,723 that the fund actually paid out in distributions over the year.

However, the fund has other means through which it can obtain the money needed to cover its distributions. For example, it received $32,580,668 in distributions from the master limited partnerships in its portfolio that were not included in net investment income. That alone was sufficient to cover the net investment loss and the shareholder distributions with money left over. This money can be considered capital gains if the fund sells the partnership units. The fund had $54,149,128 net realized gains and $97,845,488 net unrealized gains during the period.

Overall, ClearBridge Energy Midstream Opportunity Fund's net assets increased by $114,293,511 over the course of the year despite paying its distributions and buying back some of its own shares. Clearly, the fund easily delivered a performance that was strong enough to cover the distribution. Therefore, we do not have any reason to be concerned about the safety of the distribution today.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the ClearBridge Energy Midstream Opportunities Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are buying a fund's assets for less than they are actually worth. As is the case with most midstream funds, that is the case today. As of May 16, 2023 (the most recent date for which data is available as of the time of writing), the ClearBridge Energy Midstream Opportunities Fund had a net asset value of $32.87 per share but the shares only traded for $27.63 each.

That is a 15.94% discount to the net asset value at the current price. While this is not as good as the 16.48% discount that ClearBridge Energy Midstream Opportunity Fund shares have had over the past month, it is still a very respectable discount that represents an attractive price at which to purchase the fund.

Conclusion

In conclusion, midstream master limited partnerships and midstream companies enjoy stability and high yields that make them an excellent investment vehicle for anyone that desires to earn an income from their portfolios. The ClearBridge Energy Midstream Opportunities Fund provides a reasonable way to add these companies to a retirement or other tax-advantaged account while avoiding the inherent problems that come with adding partnerships to these vehicles. The fund's portfolio appears to be reasonable and has delivered a very strong performance over the past year. When we combine this with an attractive valuation, ClearBridge Energy Midstream Opportunity Fund might be worth considering this fund today.

For further details see:

EMO: A Solid Midstream CEF Trading At A Huge Discount