WES - EMO: This CEF Has Strong Fundamentals And An Attractive Discount

2023-10-10 09:19:26 ET

Summary

- ClearBridge Energy Midstream Opportunity Fund specializes in investing in midstream corporations and energy infrastructure companies, providing access to master limited partnerships in tax-advantaged accounts.

- The fund boasts an 8.60% yield, comparing well to other energy infrastructure funds.

- The fund's recent performance has been better than the S&P 500 Index, with investors making a significant difference in returns.

- The fund is positioned to benefit from strong mid-to-long-term fundamentals for crude oil.

- The fund's distribution should be reasonably secure and it is trading at a massive discount on net asset value.

ClearBridge Energy Midstream Opportunity Fund Inc. (EMO) is a closed-end fund that specializes in investing in various midstream corporations, master limited partnerships, and other energy infrastructure companies. This makes this fund one of the few ways to easily include master limited partnerships into a tax-advantaged account, such as most individual retirement accounts. The fund also provides investors with a respectable way to achieve a high level of income from their assets, as it boasts an 8.60% yield at the current price. This may not seem impressive compared to some other funds, but it is important to keep in mind that this one is not a fixed-income fund, as most high-yielding closed-end funds are. As such, we should compare its yield to other energy infrastructure funds, and it compares reasonably well here:

| Fund |

| Current Yield |

| ClearBridge Energy Midstream Opportunity Fund |

| 8.60% |

| First Trust Energy Income & Growth Fund ( FEN ) |

| 9.42% |

| First Trust MLP & Energy Income Fund ( FEI ) |

| 7.95% |

| Kayne Anderson Energy Infrastructure Fund ( KYN ) |

| 10.36% |

| ClearBridge MLP & Midstream Fund |

| 9.01% |

Thus, we can see that the ClearBridge Energy Midstream Opportunity Fund compares reasonably well to its peers in terms of yield. This should prove to be at least satisfactory to most income-focused investors.

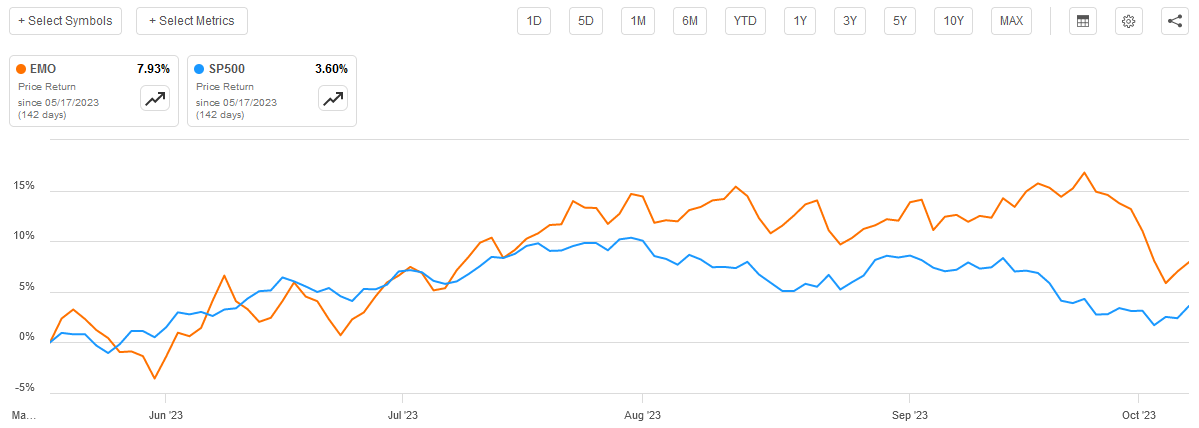

As regular readers will likely recall, we last discussed this fund in mid-September, although that article was exclusive to subscribers and trial members. The last article that I published on this fund publicly was released on May 17, 2023. That was well before energy prices started to tick up in mid-July, so there have obviously been quite a few changes to the market in which this fund primarily invests. We can actually see this by looking at the fund's performance, which has been substantially better than the broader S&P 500 Index ( SP500 ) since that article was published:

{kind=link}

The difference becomes even more stark when we consider the fact that this fund pays out a substantially higher yield than the S&P 500 Index, which provides a boost to its overall investment return. When we consider this distribution, investors in the ClearBridge Energy Midstream Opportunity Fund have made 12.26% over the past five months, compared to 3.60% for investors in the S&P 500 Index. That is a pretty significant difference in results. Fortunately, there are some reasons to expect that this fund will continue to deliver very strong performance going forward, although perhaps not quite that strong.

There have naturally been other changes to this fund beyond simply the improvements in the macroeconomic environment that we need to discuss in this article. Most importantly, the fund released an updated financial report that we can discuss. Therefore, let us investigate and see if this fund could still make sense for an income-focused portfolio today.

About The Fund

According to the fund's website , the ClearBridge Energy Midstream Opportunity Fund has the primary objective of providing its investors with a very high level of total return. This makes sense because this is a common equity fund, which is immediately apparent in the fact that 98.06% of the fund's assets are invested in common equity:

CEF Connect

As I have pointed out in numerous previous articles, common equity is by its very nature a total return vehicle. After all, investors typically purchase common equity because they want to receive an income in the form of dividends or distributions as well as benefit from capital gains as the issuing company grows and prospers with the passage of time.

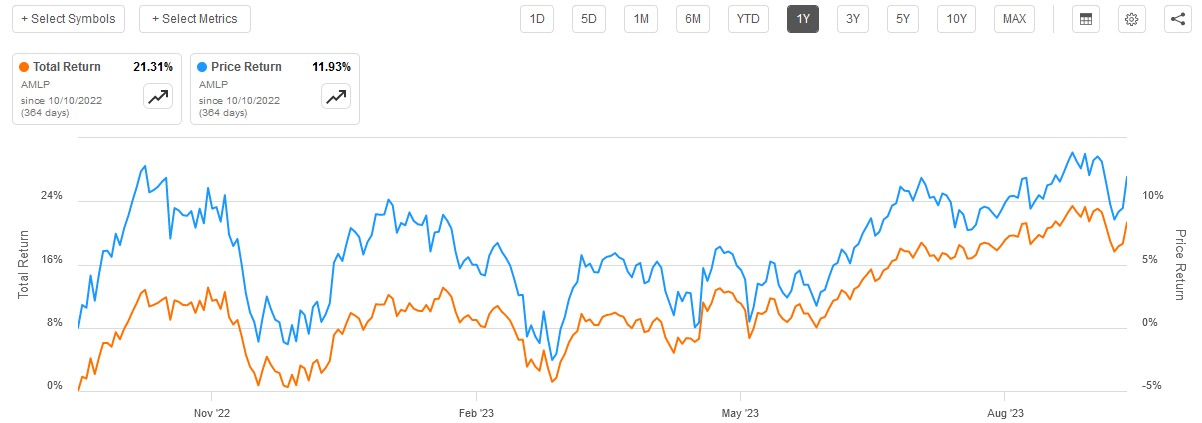

In the case of midstream companies and partnerships, a substantial portion of the investment return comes in the form of distributions and dividends. We can see this by looking at the price return against the total return of the Alerian MLP Index ( AMLP ), which primarily tracks midstream partnerships. Here are the comparison figures for the past year:

{kind=link}

As we can see, the shares of the index fund only appreciated by 11.93%, but investors in the fund actually realized a 21.31% gain on their investment. This implies that just under half of the total return that midstream partnerships provided to their shareholders during the past year was in the form of direct payments. In many years, the percentage of the total return provided by the distributions is higher than this. As such, we can assume that a substantial percentage of the total return of the ClearBridge Energy Midstream Opportunity Fund will be in the form of distributions from its assets as opposed to simple equity price appreciation.

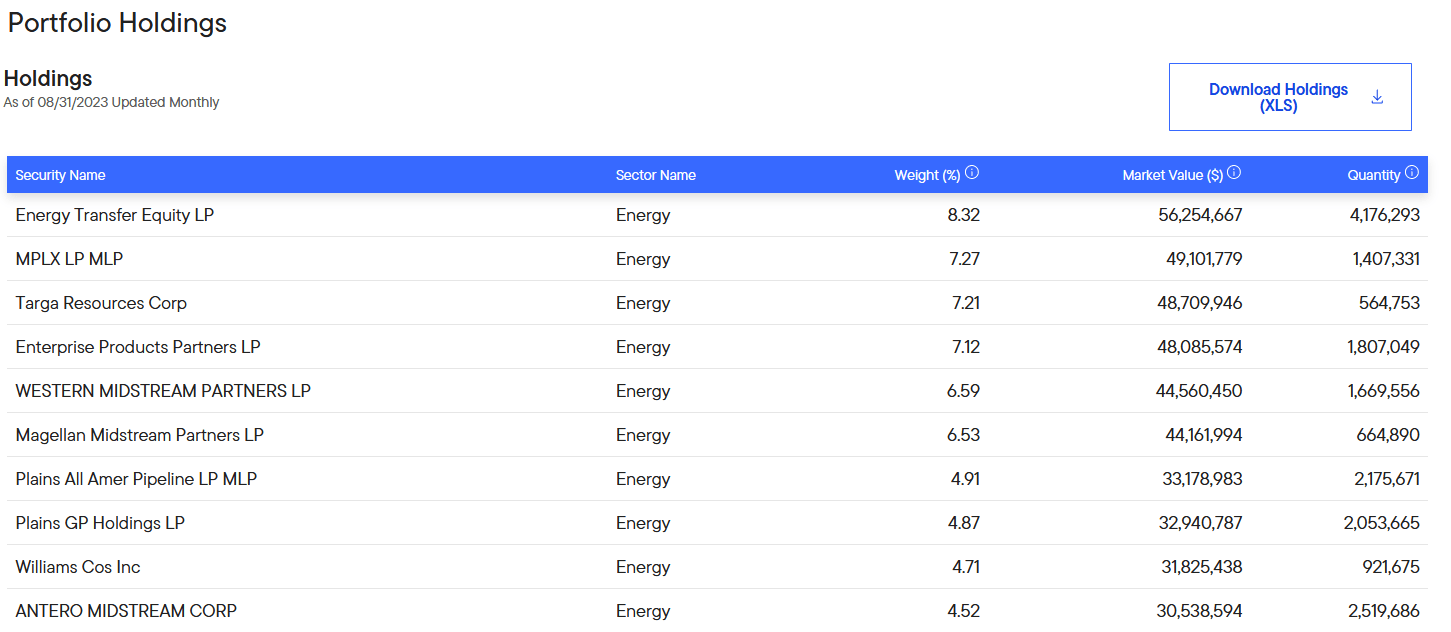

As regular readers are no doubt well aware, I have devoted a considerable amount of time and effort to discussing various midstream corporations and partnerships over the past several years. These reports were published both on my Investing Group and on the main Seeking Alpha site. As such, most readers should be familiar with the largest positions in the fund. Here they are:

{kind=link}

I have discussed all of these companies except for Western Midstream Partners ( WES ) and Plains GP Holdings ( PAGP ) over the years. However, Plains GP Holdings is simply the general partner and manager of Plains All American Pipeline ( PAA ), which I have discussed quite often. As such, it should be quite familiar to most readers. Indeed, all of these companies should be reasonably familiar. That is nice because I should not have to point out that many of these are among the best companies in the industry.

There is almost certainly one major change to this list that has occurred within the past few weeks, however. That is Magellan Midstream Partners, which recently completed a pending merger with ONEOK ( OKE ) and is no longer an independent company. As such, it is quite likely that ONEOK has probably replaced Magellan Midstream Partners since the end of August (the date that the fund last publicly updated its holdings). That is by no means certain, however, and it is possible that the fund sold off the ONEOK shares that it received in the merger in favor of something else. At the moment, we do not know exactly what the tenth company is among the fund's largest positions. This fund has an annual turnover of 60.00%, so it does a fair amount of trading, and it is certainly possible that it sold off the ONEOK shares.

In a few recent articles, I have pointed out that there are signs that the American economy may be starting to slow down. For example, we are starting to see consumers beginning to get tired of their post-pandemic spending spree and cutting back. Citibank reported that consumer spending on credit cards fell 11% in September, which represents the fifth consecutive monthly drop and the largest so far. When we consider that this period included the "back to school" season (typically a fairly large event for retail spending) was weaker than normal this year and prices have certainly not declined, this is a very clear sign that one of the last bastions of economic strength has crumbled. Fortunately, the companies in which the ClearBridge Energy Midstream Opportunity Fund invests are highly unlikely to be affected by economic weakness. This is due to the business model that these companies employ, which I discussed in a previous article:

In short, a midstream company enters into long-term contracts with its customers. Under the terms of these contracts, the midstream company moves a customer's hydrocarbon products through its network of pipelines and other infrastructure. In exchange, the customer compensates the midstream company based on the volume of resources that are transported, not on their value. This provides a significant amount of insulation against volatile energy prices.

This business model works so well to protect these companies against economic problems that even the COVID-19 lockdowns in the Spring of 2020 had no impact on most of their cash flows. While we did see several of these companies reduce their distributions in response to that event, that was simply because the capital markets did not want to touch anything related to the oil and gas industry. These companies simply cut their distributions in order to pay off their debt and become self-financing. As I have pointed out in many previous articles though, their cash flow was almost completely unaffected. It seems likely that the same would be the case in another economic downturn, such as what might be coming. As we will see in a moment, energy prices could increase going forward, which would put further pressure on consumers.

Oil Price Fundamentals Update

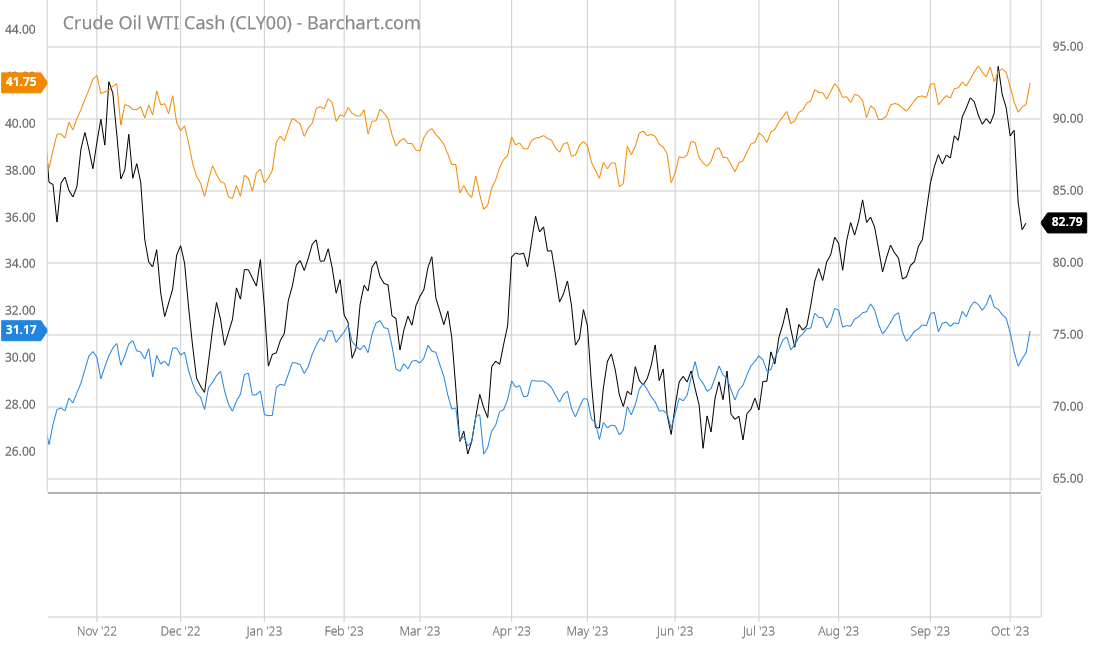

As we already saw, the cash flows of the midstream companies in which the ClearBridge Energy Midstream Opportunity Fund invests are not significantly impacted by energy prices. If they were, then these companies would not have handled the COVID-19 lockdowns as well as they did. However, their equity prices do still correlate with oil prices to a certain degree. It is not a perfect correlation, but we can still see one in this chart:

{kind=link}

This chart shows the spot price of West Texas Intermediate crude oil against the Alerian MLP Index in orange and the ClearBridge Energy Midstream Opportunity Fund in blue over the past twelve months. We can see that crude oil prices are much more volatile, but for the most part increases in crude oil prices caused the price of both the fund and the index to increase and vice versa. Thus, the fundamentals of energy prices are still relevant to our discussion of this fund as an investment.

Fortunately, the fundamentals of crude oil right now are very positive primarily because energy companies in aggregate have been underinvesting in productive capacity since 2015. There are several reasons for that, including various parties in the market refusing to provide energy prices, investor aversion towards fossil fuels, government incentives meant to promote renewable energy, and various other things. As a result of this underinvestment, crude oil production is not likely to be as high as it would have been had suitable amounts of capital been invested. This poses a problem because most sources right now expect that crude oil demand will not drop off nearly as rapidly as environmental activists and politicians believe. The truth is that renewable technology is nowhere near where we need it to be in order for it to work as a suitable replacement for hydrocarbons.

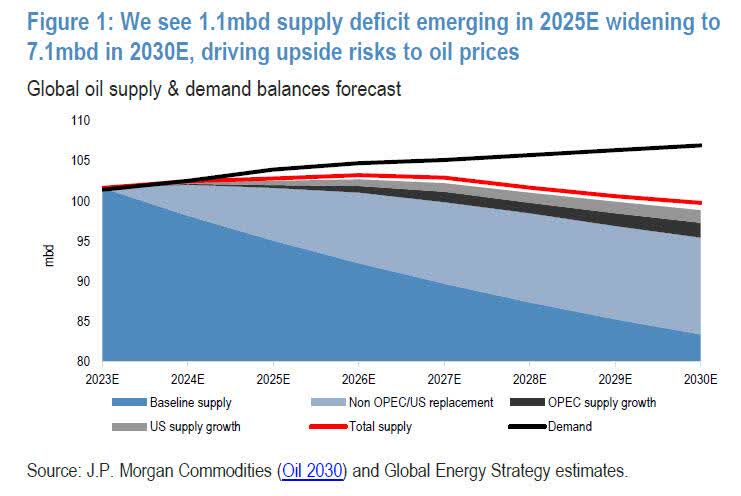

As a result, the production of crude oil is likely to be lower than demand over the coming years. JPMorgan Chase recently predicted that the global demand for crude oil will be 1.1 million barrels above the production level by 2025 and 7.1 million barrels above the production level by 2030:

{kind=link}

The Organization of Petroleum Exporting Countries recently made similar statements. The organization's World Oil Outlook stated that the energy industry needs to invest approximately $14 trillion into upstream, midstream, and downstream capacity by 2045 in order to avoid a catastrophic energy shortage. That is, to put it mildly, highly unlikely to happen considering that many politicians and activists are trying to curtail investment into productive capacity.

There may be some readers who point out that the Organization of Petroleum Exporting Countries is simply talking up its own book with its statements about a mid-term shortage of oil. That is certainly possible, but private companies such as JPMorgan and Moody's are saying the exact same thing. Thus, it is something that we can probably take seriously.

The laws of supply and demand imply that a shortage of crude oil would have the effect of raising crude oil prices. As we have already seen, there appears to be a correlation between the price performance of midstream companies, the ClearBridge Energy Midstream Opportunity Fund, and crude oil. Thus, there is reason to believe that this situation will have a positive effect on the share price of this fund over the mid-to-long term.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the ClearBridge Energy Midstream Opportunity Fund is to provide its investors with a high level of total return. In order to accomplish this, the fund invests primarily in midstream companies and partnerships. These are companies that deliver a significant percentage of their total return in the form of direct payments to the shareholders. As a result, they tend to have high yields. For example, the Alerian MLP Index yields 8.13% at the current price. The ClearBridge Energy Midstream Opportunity Fund collects these distributions and pays them out to its own shareholders along with any capital gains that it manages to realize. As such, we can assume that this fund would have a fairly high distribution yield itself.

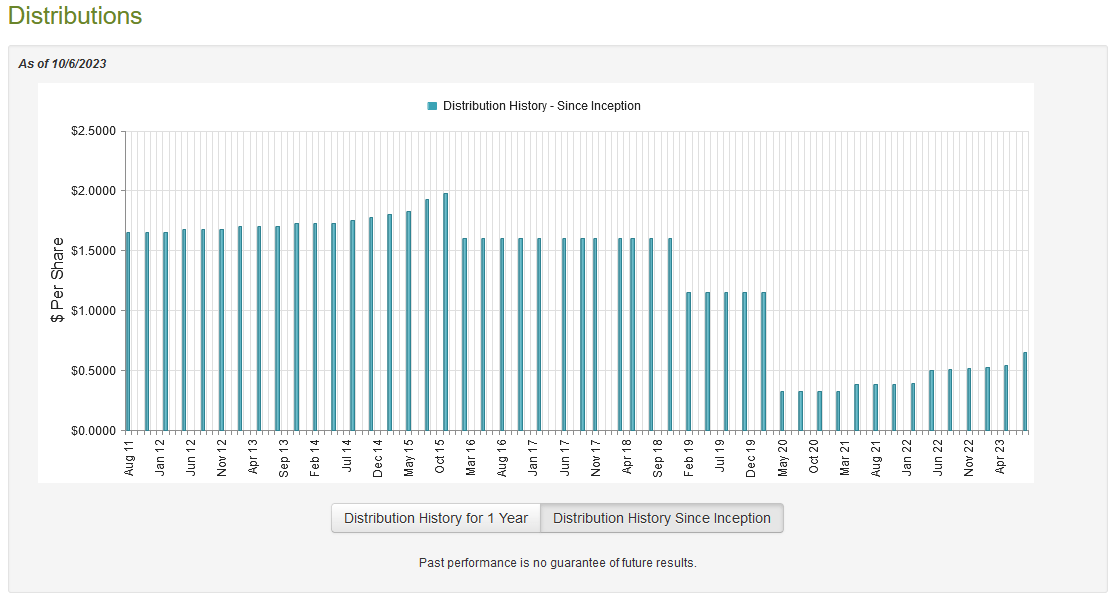

That is certainly the case as the ClearBridge Energy Midstream Opportunity Fund currently pays a quarterly distribution of $0.65 per share ($2.60 per share annually), which gives it an 8.60% yield at the current price. This is a very reasonable yield for a fund like this and it is sufficiently high to appeal to any income-focused investor. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years. As we can see here, it has had to make a few large cuts over its lifetime, although it has generally been boosting its distribution since 2020:

{kind=link}

The fact that the fund has not obtained a perfect track record with its distribution could be something of a turn-off to investors who are seeking a safe and consistent source of income to use to pay their bills or finance their lifestyles. However, as I explained earlier in this article, several midstream companies cut their distributions in 2020 despite their cash flow remaining stable. In addition, companies in the industry saw their equity prices collapse. These two factors reduced the amount of money coming into the fund and forced it to take substantial unrealized losses. Thus, it makes sense that the fund had to cut in response to these events. Fortunately, we can see that it has been increasing its distribution now that the sector has largely recovered.

Naturally, though, anyone who purchases the fund today will receive the current distribution at the current yield and will not be adversely affected by the distribution cuts that the fund was forced to impose in the past. As such, the biggest concern for investors today is how well the fund can sustain its current distribution. Let us investigate this.

Fortunately, we do have a fairly recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is a newer report than the one that we had the last time that we discussed this fund, which is quite nice to see. After all, during the first half of this year, crude oil prices were generally much lower than they were in either 2022 or recently. This weighed somewhat on midstream stocks and likely made it much more difficult for the fund to earn capital gains than it experienced in 2022. This report will thus show us how the fund performed in such an environment, and seeing how a management team handles a challenging environment is a very important part of determining its overall skill. After all, anybody can make money in a raging bull market.

During the six-month period, the ClearBridge Energy Midstream Opportunity Fund received $23,247,909 in dividends and distributions along with $178,049 from the money market funds storing its cash. The fund reported no interest during the period. One characteristic of midstream partnerships is that their distributions are not considered to be income to the fund, so the fund only had a total investment income of $4,936,584 during the period. This was not enough to cover the fund's expenses, and it ended up reporting a net investment loss of $5,316,691 over the course of six months. Obviously, that was nowhere near enough to pay any distribution, but the fund still handed out $13,682,401 to its shareholders. At first glance, this is almost certainly going to be very concerning.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distribution. For example, the fund received $18,787,159 in distributions from master limited partnerships during the period. That money was not considered to be income for tax purposes, but it still represents money coming into the fund. The fund also might have been able to get some capital gains that can be paid out. Unfortunately, it was not successful at this task as it only reported net realized gains of $8,290,562 but this was more than offset by $42,384,338 net unrealized losses. Overall, the fund's assets declined by $56,823,422 after accounting for all inflows and outflows during the period. Thus, it failed to cover its distributions overall, which is worrying. However, the fund's net assets were still up over the trailing eighteen-month period. In short, the fund made enough money over the course of 2022 to cover all of its distributions for that year and make up the difference for the first half of 2023. Thus, the distribution is probably reasonably safe right now, especially considering that the past few months have given it the possibility of having more gains.

Valuation

As of October 6, 2023 (the most recent date for which data is available as of the time of writing), the ClearBridge Energy Midstream Opportunity Fund has a net asset value of $34.97 per share but the shares only trade for $31.17 each. As such, the fund's shares are currently trading at a 10.87% discount on net asset value. This is a very large discount, although it is nowhere near as attractive as the 12.91% discount that the shares have had on average over the past month. As such, it might be possible to obtain a better price by waiting a bit. However, realistically a double-digit discount is generally a reasonable price to pay for any fund, so the current price is probably acceptable if you want to own some shares.

Conclusion

In conclusion, the ClearBridge Energy Midstream Opportunity Fund is a reasonable way to play the midstream exposure without having to worry about the tax problems that can come along with owning master limited partnerships. This fund is structured as a corporation, so it handles all the tax issues on the fund level. The fund has delivered a respectable performance over the past several months, as it has beaten the S&P 500 Index, and it seems likely that it will continue to do so due to the strong mid-term fundamentals for energy. The valuation is also reasonable right now. The biggest problem here is that the fund failed to cover its distribution during the first half of the year, but due to the very strong performance that it delivered in 2022, it is not straining to maintain the distribution. Overall, this fund might be worth considering for a portfolio today.

For further details see:

EMO: This CEF Has Strong Fundamentals And An Attractive Discount