ACT - Enact Holdings: Being Shareholder Friendly Offers Upside

2023-06-30 14:03:18 ET

Summary

- Enact Holdings is viewed as a relatively defensive position with well-managed risks and commitment to shareholder interests.

- Recommended as a "buy" for long-term investors.

- The capital allocation framework includes returning at least $250 million to shareholders this year through dividends and buybacks.

In my neighborhood, I've seen more "for sale" realtor signs up in yards that have been there for months, I guess mostly due to the normal seasonal spike in real estate in spring and summer. Anecdotally from my perspective, there is definitely activity going on, in spite of the elevated rates on mortgages over the last year or more. My literal next-door neighbor is trying to sell, and has had several lookers. A house across the street just sold recently to a family moving from another state. In the big picture, housing remains challenged on account of the borrowing costs, but so far there has not been a catastrophic fall out in residential real estate. In turn, the relative health of the mortgage insurance segment has been holding up well, with the shares of some companies doing exceptionally well for their shareholders over the last six months.

When I last wrote a piece focused on mortgage insurer Enact Holdings ( ACT ) in January, the view I wrote-up concluded:

Whether the loss reserve will need to start creeping up again in the current or expected recessionary economic environment will be answered in time, but there is not yet any clear indication of an imminent hard landing. . . I consider Enact Holdings to be a relatively defensive position, with well managed risks and a commitment to shareholders' interests. For long-term investors, I continue to consider it a "buy," although I anticipate there may be more attractive entry points possible in the first half of 2023 while the market digests mortgage numbers that are likely to look abysmal.

Overall, I think that conclusion still holds, and there have been a few dip opportunities to get in at better prices since January, though shares have generally traded in a fairly narrow range. The sector has performed quite well over the last six months, but Enact has lagged well behind its peers in share-price gains.

Enact Holdings, with a market capitalization of $3.98 billion, is one of a handful of publicly traded major providers of this type of insurance that are all of a similar scale; peers include Radian Group ( RDN ) at $3.92 billion, Essent Group ( ESNT ) at $4.84 billion, and MGIC Investment Corp ( MTG ) at $4.40 billion. At a slightly smaller scale is NMI Holdings ( NMIH ), with a market cap of $2.10 billion.

While the shares of these five companies have moved in pretty strong correlation with one another recently, clearly Enact Holdings has been lagging the group.

The mortgage market in 2023 is certainly off to a relatively weak start, with Attom reporting that in Q1 of 2023, only 1.25 million residential mortgages were closed, for $388 billion of borrowing. That represents multi-year lows, and would certainly suggest that mortgage insurers like Enact and its peers were not writing a lot of new policies. Not surprisingly, that has been the case, at least for Enact Holdings. The company wrote $13 billion in new policies during the first quarter, compared to $15 billion in Q4 of 2022.

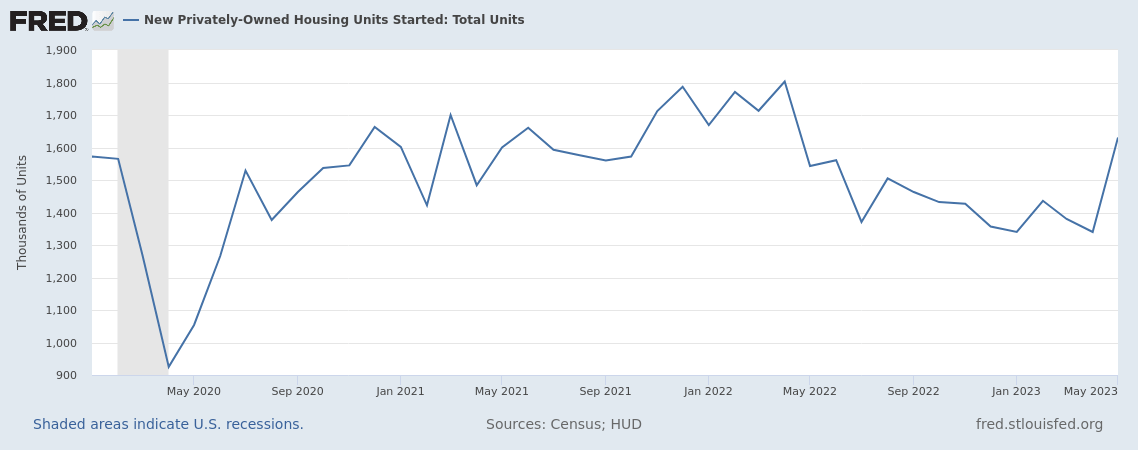

Interest rates are obviously the major contributor to the slowdown, and should a recession eventually come, things could conceivably get worse. However, for the moment, there are signs that home sales are stabilizing as the spring and summer selling season is in full swing. According to the Federal Reserve's data, new housing starts are up, so interest rates have clearly not killed off activity.

New Housing Starts, January 2020 - May 2023 (St. Louis Federal Reserve)

{kind=link}

New starts are at a similar level in May as they were in May of 2021 and May 2022, and recovering from the winter doldrums.

Mortgage Insurance Fundamentals

In the midst of the all data regarding the health of the housing industry, and trying to parse the trends, one can easily get sort of lost in the noise, at least if the objective is trying to come to a conclusion on a possible investment in the mortgage insurance sector. Tuning out that noise that changes so readily from month to month and instead focusing on the fundamentals of the business over the long-term will work out for a better investing decision. So how does a company like Enact Holdings work, fundamentally?

The business model of the mortgage insurance sector, like any form of insurance, is premised on protecting against the risk of an uncertain future. Specifically, those who lend money for the buying of homes want to be protected against loss in the event a borrower does not pay the debt, and borrowers having relatively lowers amounts of equity in their homes involve a greater risk. In the United States, borrowers with less than 20% equity in their homes are generally required to pay premiums for mortgage insurance, typically bundled right into the monthly mortgage payment for convenience but ultimately paid to the mortgage insurer. The insurance company in turn agrees to carry a portion of the risk, and partially protects the provider of the mortgage against losses in the event of a loan default. The insurer uses some of the premiums it collects to fund its own operating expenses, but more to the point, invests the premiums, typically in a conservative portfolio that can reliably fund making payments on claims when they arise. Once a mortgagee has surpassed the 20% threshold, the mortgage insurance requirement goes away, and the premiums are no longer collected.

The sector obviously depends on mortgage volume and home sales for driving new business, but the business that is earned tends to be "sticky" in the sense that an average home buyer paying the monthly mortgage likely does not pay much attention to who is providing the mortgage insurance. Only 3 routine scenarios interrupt the premiums from being received: 1) the borrower's amortization schedule on the loan brings him to the 20% threshold, and the policy is no longer in force, 2) the borrower sells the house (which could potentially generate new business, depending on the buyer's needs and if the seller also proceeds to take on a mortgage to purchase another home), or 3) the borrower defaults and the lender makes a claim on the policy. So long as the premiums are sufficient to operate the company and able to meet future claims, the excess returns above and beyond those needs accrue to the shareholders, whether in the value of the equity, or through dividends and share buybacks.

Enact - Review of Q1

Realizing that Q2 is wrapping up as I write this, the Q1 results are understandably dated already, but provide some context for setting up the rest of the year expectations.

Income from premiums in Q1 was $235.1 million, fairly flat compared to the same period in 2022 of $234.3 million. However, net investment income was up by $10 million year over year, from $35 million to $45 million, which essentially accounts for the total growth in revenue, $280.9 million versus $269.6 million. That difference basically flows through to the net income for the period, ending at $176 million, or $11 million greater than Q1 of 2022. That was enough to improve EPS from $1.01 to $1.08 for the period, as the share count has remained largely unchanged.

Cash from operations suffered from "other liabilities" of $31.6 million, coming in at $119.4 million, considerably lower than last year's $160.8 million. Cash uses in investing were net positive $33.5 million on strong proceeds from the sale of securities, and Enact spent roughly equal amounts on dividends and share buybacks in the quarter, about $22.5 million for both.

The quarter ended with $253 billion of insurance in force, a record high, with low customer churn and adding clients. As an upside to the higher rates for Enact, those homeowners that have locked in low rates over the last few years are now less likely to refinance or sell, which keeps them generally paying Enact's premiums month to month. In fact, according to CEO Rohit Gupta on the quarterly call , nearly all of Enact's insurance in force is with homeowners who are locked into mortgage rates that are at least 50 basis points lower than prevailing rates today, so they generally have no financial incentive to make a change. Overall quality has been good, with a release of loss reserves of $70 million, while still prudently adding to the reinsurance book.

Given the overall environment for interest rates, management is not providing specific guidance for the company's results for 2023. However Mr. Gupta did offer his general outlook on the mortgage origination market a whole for the year, stating (emphasis added and edited for length):

I think I would start off by just saying that we are operating in a dynamic environment when it comes to mortgage rates and impact of mortgage rates on consumers' participation in the purchase market, because majority of our business is tied to the purchase market . So as we think about the year, we still think that this year, 2023, compared to 2022 will be a lower year on purchase originations market. . . So our perspective is . . . closer to where maybe the Fannie Mae forecast is, origination on purchase side being around $1.3 trillion.

So full year expectations on a smaller purchase origination basis is realistically likely to keep some downward pressure on Enact's results, though they are well positioned to weather a slower market. Fitch and Moody's both upgraded Enact to A- investment-grade quality, while S&P upgraded the operating company to BBB+, all recognizing their position of financial strength.

Valuation

While in theory the credit upgrades could be bullish for Enact's equity, clearly the market in the first half of the year has either shrugged off positive news, or else finds something less attractive about Enact than it finds in the other mortgage insurers. But for new investors, that could spell opportunity, if the valuation is attractive enough. Analysts for Bank of America ( BAC ) and KBW have both offered their takes on the sector fairly recently. Bank of America considered Radian (downgraded) and Enact as "holds" and MGIC a "buy," while KBW maintained Enact and MGIC as "outperform," and Radian as Essent were moved down a notch to "market perform."

Overall, I find fairly little differentiation on valuations; most of the sector currently trades at a small discount to book value, with P/free cash flow multiples mostly sitting the around 6.5x - 7.6x range. Radian has long offered the best dividend yield, which remains true even after its price gains.

Mortgage Insurance Valuations (Author's spreadsheet; data from Seeking Alpha)

The potential is there for slight multiple expansion in which the sector trades at more consistently at book value, however that is neither a sustained historical trend, nor does represent much upside from the current valuation. With the market assigning fairly consistent valuations across the sector, none stand out as being particularly undervalued relative to the others.

Enact's dividend lies in the middle, although having increased it dividend by 14% effective with the June 2023 dividend and is planning to return at least $250 million to shareholders for 2023, between dividends and share buybacks. As that amounts to about $1.53 per share, and at the current price of ~$25 per share, that is not a bad 6% return in an otherwise conservative investment. Of the $1.53 per share, $0.64 is in the form of regular dividends, leaving $0.89 per share for buybacks, special dividends, or some combination of both. I think that is where the potential for a good return here and to benefit from the valuation not being stretched.

Conclusion

While I continue to like the sector overall as a conservative play that may offer some growth upside when the housing market accelerates again, but has limited downside due to its pricing power, the benefits of higher rates for generating investment income, and fairly low customer churn while mortgage rates are high. An investment here is most likely to be a sort of slow burner, and I continue to like Enact Holdings personally for its shareholder return plans and a valuation that is reasonable. While I expect the housing market to normalize eventually, I cannot predict how long it will take or what set of conditions it will take to get there, but in the meantime I can sleep well with a small long position in Enact Holdings in my portfolio.

For further details see:

Enact Holdings: Being Shareholder Friendly Offers Upside