ENGGF - Enagas Has More Upside Than Snam

Summary

- Looking at the numbers, Snam is a safer company compared to Enagas (based on credit metrics and Regulatory Asset Based evolution).

- Snam offers the best opportunity to capture EU hydrogen growth.

- However, Enagas has a compelling valuation with a 10% dividend yield (the Italian player already paid the interim).

Here at the Lab, we very much like comps analysis, and recently, we scrutinized Generali vs Allianz and FormFactor Vs. Technoprobe. Based on the stock price developments, our insights were positive and we achieved interesting returns. Today, we will focus our attention on Enagás (ENGGF) (ENGGY) versus Snam (SNMRF). Last year, our internal team analyzed Enagás' strategic plan for 2022-2030, while Snam just announced a new plan update for the next five years.

These are Snam's 2022-2026 strategic plan objectives and we will compare them with our Spanish pipeline operator.

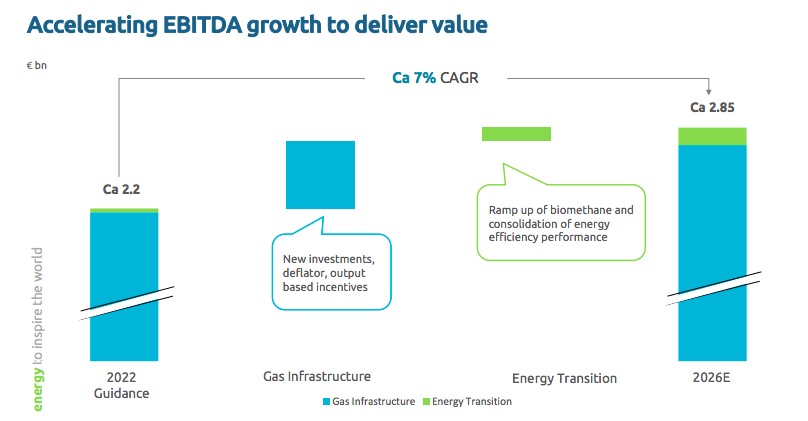

Snam's total investments will reach €10 billion (+23% compared to the €8.1 billion of the 2021-2025 plan), mainly for the commissioning of two FSRUs, the update cost on the Adriatic Line construction, and new storage facilities. According to the plan, RAB will grow by more than 5% on average per year (from +2.5%) with an EBITDA estimate CAGR of 7% in the same period (from the previous +4.5%) and a net income growth forecast of 3%. These numbers already incorporated the higher financial charges due to the increase in interest rates which are assumed at a 2% average (versus the 1.1% in the previous plan). Looking at Enagás, the company will invest €2.7 billion by 2030, and if we consider the European REPowerEU, we arrive at a figure of approximately €4.8 billion. Regarding the P&L, Enagás expects lower growth compared to Snam. Indeed, EBITDA estimates are for a 2% increase on a yearly basis until 2026, and then a higher forecast of 4% between 2026 and 2030.

{kind=link}

Snam EBITDA growth

Source: Snam's new strategic plan

What is key to emphasize is also the fact that the Italian player network is ready to transport hydrogen, while Enagás will need new CAPEX and we might expect limited reductions in its pipeline.

Enagas CAPEX plan

Source: Enagás 2022-2030 Strategic Plan

Going to the shareholder's remuneration, as for the dividend, Snam's minimum growth is envisaged at 2.5% for previous years and was also extended to 2026. In particular, Snam established that for the 2022 financial year, a total dividend of €0.2751 per share may be distributed in 2023, of which 40% as an interim dividend (€0.11 per share, yield of 2.20 %) with a payment expected today, while the remaining 60% is for June. Enagás confirmed its dividend policy and the company will increase its DPS by just 1% in 2022 and 2023 and maintain a flat dividend of €1.74 per share until 2026.

{kind=link}

Snam DPS increase

Enagas DPS increase

Regarding the financial structure, Snam's debt is expected to rise to €18 billion in 2026, and the company will maintain credit ratios consistent with current creditworthiness and a mix of fixed and variable debt of approximately 2/3. Snam's debt duration is higher than Enagás (5.7 years vs 4.3 years) and financial cost is lower (1% vs 1.7%).

Conclusion and Valuation

Here at the Lab, we continue to reiterate our overweight rating on Snam and our target price of €5.3 per share (the company is currently trading at €4.7 per share). Also, we continue to see the Italian player as the best-positioned European stock to capture hydrogen growth as part of the net zero decarbonization process. However, Enagas offers a higher upside on the stock price appreciation and a better dividend yield. In detail, the Spanish operator still trades below a 15x price-earnings ratio, and below 11x 2023 expected EBITDA. Enagás offers a 10% dividend yield compared to Snam at 5.6%. Our buy target rating is also supported by our previous publication thanks to 1) 6 regasification plants that could manage 40% of the total gas capacity in continental Europe, 2) renewable & hydrogen infrastructures, and 3) the Italian opportunity with a possibility to double the TAP pipeline .

For further details see:

Enagas Has More Upside Than Snam