ENGGF - Enagas: Higher Rates And No Positive Catalyst (Rating Downgrade)

2024-01-17 21:50:30 ET

Summary

- There is uncertainty regarding the GSP arbitration in Peru, and with the ongoing earnings, net debt will likely increase.

- We see no positive catalyst. The H2Med pipeline project is in its infancy period.

- The company's valuation is not justified compared to Snam. With an FCF insufficient to meet DPS, we lower Enagas to a Sell rating.

Here at the Lab, our readers know we have long been on Enagás since 2020 ([[ENGGF]], [[ENGGY]]). Despite that, even with favorable tailwinds and catalysts (1. Cost-Cutting Advances And Affiliate Income , and 2. Enagas Is Playing A Crucial Role In The Energy Crisis ), the Spanish company performed poorly at the stock price level. For this reason, in early August, we decided to move Enagás to a neutral rating with a reduced target price of €16.5.

{kind=link}

Where are we now?

As a reminder, the company operates and owns most of Spain's gas transmission system. These assets are high-pressure pipelines for approximately 11,000km, including underground storage facilities and regasification plants. In our forward-thinking view, we report the following:

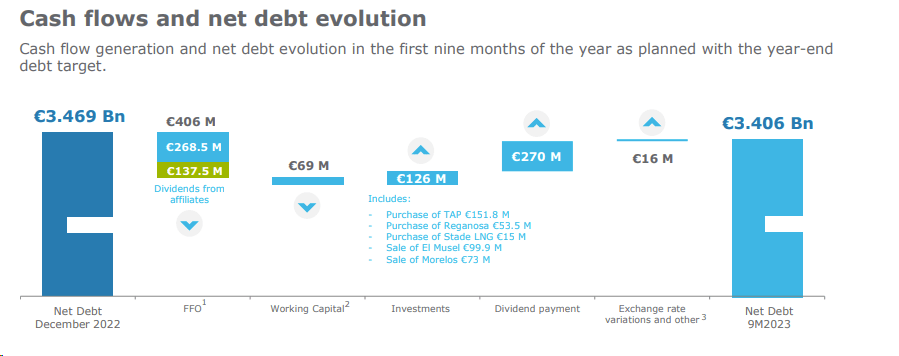

- Enagás' Q3 results met consensus. In numbers, the company narrowed its net income at the guidance top-end, lowering net interest. Despite that, Q3 reported FF0 reached €158 million, of which €28.7 million were in dividends received from equity affiliates. Looking at TAP, the Trans Adriatic gas pipeline provided €42 million in dividends and is likely to achieve its €70 million year-end projection. However, Enagás net debt increased to €3.4 billion from €3.16 billion in Q2 (Fig 1). Here at the Lab, this is not the first time we have reported how the CNMC - Spain’s competition regulator - decided to cut Enagás RAB (Regulatory Asset Based). A shrinking Spanish asset base challenges Enagás core regulated earnings. For this reason, our 2024 sales projection is at €940 million with an adjusted EBITDA of €738 million. With a cash flow projected at €520 million and CAPEX at €335 million, free cash flow cannot meet the dividend per share payment . This results in climbing leverage. Consequently, in our projection, net debt increased on average by €200 million per year;

- We are not anticipating a dividend per share reduction; however, this may happen in the next two years. As a reminder, in 2022, Fitch already downgraded Enagas to 'BBB' with a stable outlook;

- There was no news on the GSP arbitration . The protracted Peruvian arbitration remains share price relevant for the company. This might have a consideration of €463 million in our net debt calculation;

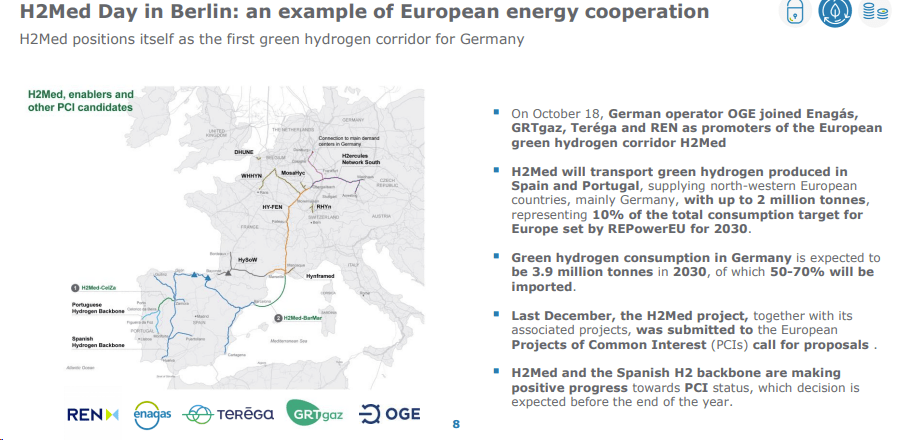

- Even if the company greatly emphasizes the H2Med pipeline project (this is not RAB remuneration), we are more cautious about potential earning pipeline ambitions. This project remains firmly in its infancy period. In the slide below, it is clear that Enagás reports H2Med as an example of EU cooperation (Fig 2);

- Given the incremental debt and higher-for-longer interest rate environment, we anticipated interest expense at 125 million in 2024. Our net income reached €250 million from a projection of €315 million in 2023 (the company's mid guidance - Fig 3), and the EPS moved from €1.2 to €0.96. The company has almost €1 billion in debt to be renegotiated in the next two years. This represents nearly 25% of the total company's debt. A higher net financing cost forecast cannot go unnoticed.

{kind=link}

Source: Enagás Q3 results presentation - Fig 1

{kind=link}

Fig 2

{kind=link}

Fig 3

Conclusion and Valuation

The company is currently trading at an 11% dividend yield, and even if it seems a tasty return, our rating is skewed toward an underperformance rating. As a reminder, Enagás' equity story is challenged as regulated earnings are declining with no view on the Spanish regulators, FCF is insufficient to meet DPS, and the company's leverage is increasing. Here at the Lab, we believe a lower multiple is justified. Enagás trades at a premium to the 2024 RAB estimates, while the Italian operator is at a 6% discount. Enagás' valuation is not justified, and in our view, given Snam's (SNMRF) (SNMRY) superior RAB growth, we prefer the Italian player. In addition, on a 2024 basis, Snam P/E is at 13.5x while Enagás is above 18x. For this reason, we believe the Spanish operator looks expensive. Valuing Enagás with a 2024 EPS of €0.96 in line with Snam P/E valuation, we derive a target price of €12.96 per share from €16.5. Our target is now moved to sell. Upside risks include WACC-RAB rebalance, favorable Peru GSP arbitration, and a lower interest rate environment.

For further details see:

Enagas: Higher Rates And No Positive Catalyst (Rating Downgrade)