ENGGY - Enagas Is Still A Buy

Summary

- Supportive developments from affiliates.

- Asset rotations reduced EM exposure (and earnings volatility), and Enagas increased its equity stake in TAP.

- The dividend payment was once again confirmed, and so was our valuation.

Here at the Lab, in 2022, we have intensively covered the Spanish gas operator in the past and we recently performed a comps analysis between Enagás ( OTCPK:ENGGF ) ( OTCPK:ENGGY ) and Snam ( OTCPK:SNMRF ), providing further insight to support our buy rating target. As a reminder, Enagás has a compelling valuation and is yielding more than 10% (at today's price). In addition, its asset base could manage 40% of the total EU gas capacity and this is also coupled with the possibility of doubling the TAP pipeline .

Our readers know that we are surprised to see a minus 20% in stock price decline since our publication called Enagás Is Playing A Crucial Role In The Energy Crisis ; however, investments in hydrogen and renewable infrastructures, the RePower Act, and further asset rotation with disinvestment in EM & investment in developed countries (lowering Enagás earnings volatility) will support the company going forward.

Before commenting on the company's Q4 and FY results, and to support our investment thesis, we would like to emphasize Enagás' latest developments:

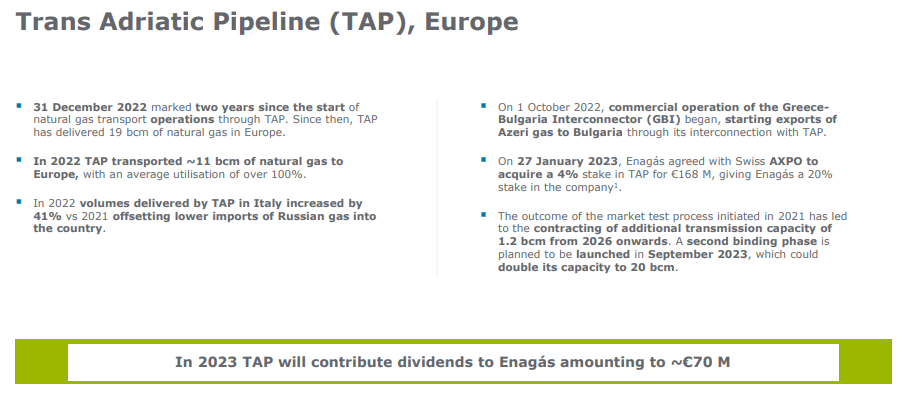

- Mare Evidence Lab's supportive buy points were affiliates with higher dividend contributions. Enagás reached a 39% net profit from equity stake investments confirming the positive trajectory achieved in the past. These performances were delivered despite the ongoing asset rotation. In detail, we should mention that a 45.4% stake in GNL Quintero was sold with a capital gain of €135 million, and in January 2023, the Spanish player purchased an additional 4% stake in TAP from AXPO for a total consideration of approximately €168 million. Thus, Enagás increased its equity participation to 20% and more importantly is expecting a 2023 dividend contribution of around €70 million (Fig 1);

- Still related to TAP, a second expansion phase is expected to be launched in Sept 2023. This confirms our previous insight for a capacity expansion which was already well detailed in our article called Positive News Ahead. TAP's final shareholding agreement is now well balanced with an equal shareholding structure of 20% for all the partners involved;

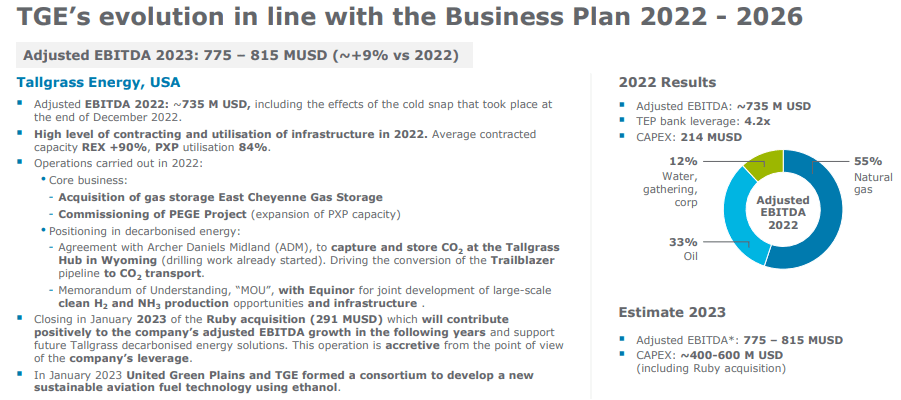

- In the US, Tallgrass Energy is proceeding with its 2022-2026 strategic plan and its utilization rate reached an average contracted capacity for the Pony Express and the Rockies Express pipeline of 84% and >90% respectively (Fig 2).

- In mid-January, Enagás also announced its intention to cancel €75 million investment for a fifth of the capital of the BBL gas pipeline.

{kind=link}

Fig 1

{kind=link}

Fig 2

The company's gas demand evolution, which includes both national consumption and exports to Europe, grew by 4.4% in the year just ended. However, this amount contains a double reality. While exports through international connections (France and Portugal) and LNG refills (with their final destination in Germany and Italy) increased, Span consumption was substantially lower than in 2021 with a minus -21%, both due to lower industrial demand and the government's savings and efficiency measures taken at B2C level. On the other hand, gas burning for electricity generation marked a new maximum since 2010, after increasing by almost 53% due to higher electricity exports to France and Portugal, and the drought, which sank hydro generation production.

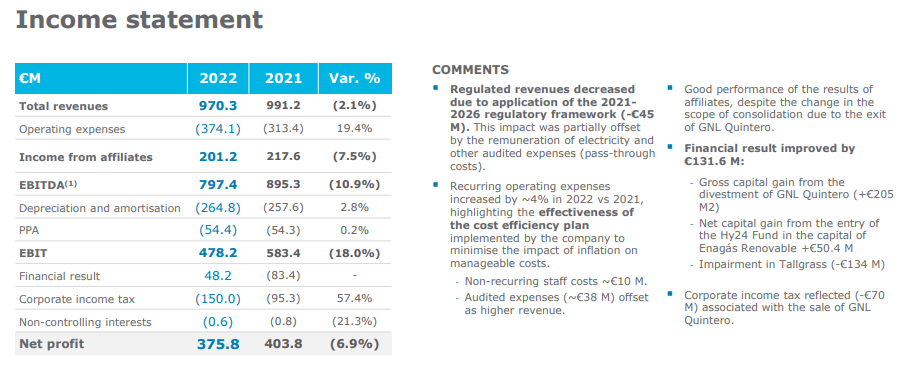

Checking our previous coverage, we are not surprised to see that the company saw its regulated income fall by almost 2% (with a minus €45.1 million) due to the framework regulation application for the period between 2021 and 2026.

- Cost-Cutting Advances And Affiliate Income Continue Enagas Earnings Development

- Enagas Sees Remuneration Reductions, But Still Offers Inflation Protection And Opportunity In Hydrogen

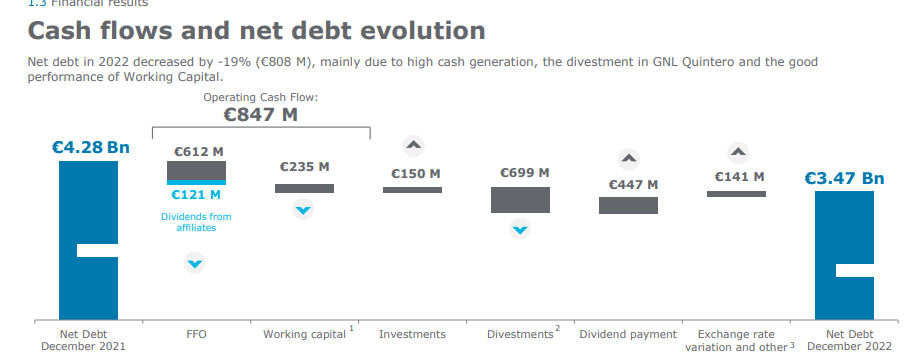

EBITDA then reached €797.4 million and was reduced by 10.9% compared to the previous year (Fig 3). Aside from the reduction due to regulatory change, the company was not able to offset some inflation pressure costs. Going down to the P&L analysis, the financial results reached a plus €48.2 million thanks to the asset rotation (GNL and Enagás Renewables sales) and were able to offset a negative one-off impact of €133.8 million due to Tallgrass Energy impairments. Despite a lower EBITDA, the operating cash flow was 14.5% higher than the previous year and the company managed to reduce its debt (Fig 4). This was mainly due to positive working capital evolution and a solid FCF generation. At the bottom line, if we consider Enagás' previous indication, we see a net profit down by 6.9% on a yearly basis; however, it was above management targets.

{kind=link}

Fig 3

{kind=link}

Fig 4

Conclusion and Valuation

Dividend indications were left unchanged, confirming the company's future projection that guarantees a 1% increase in the dividend in 2022, and an additional increase to €1.74 for 2023. Given the geopolitical situation, the Spanish gas system has positioned itself as an entry point to Europe. In 2022, the company had a supply portfolio from 19 different origins, one of the most diverse in Europe, and unloaded 338 LNG ships up by 30% compared to the previous year.

After months of a total slowdown in Spain's gas consumption, Enagás is already seeing a " strong recovery " in the quantities consumed by the secondary sector and gas consumption is returning " to pre-war levels ". For 2023, and despite this acceleration in industrial consumption, Enagás expectations are set for a 2% plus, and taking into consideration, the regulatory framework, we estimated a net profit of €320 million - 15% less than in 2022. As already anticipated, affiliates' dividends will then increase Enagás accounts. On a negative note, before the results, BlackRock decided to lower Enagás equity investments from 1.07% to 0.97%. This operation notified on February 10th has been carried out through a British fund and represents its biggest downward position. Despite that, we decided to confirm our buy rating and even apply a Dividend Discount Model, with Enagás DPS policy (constant at €1.74 per share) and a discount & growth rate of 8% and 1% respectively, we derived a price target of €24 per share and $12.5 in ADR.

For further details see:

Enagas Is Still A Buy