ENGGF - Enagas: Recession-Resistant With A Dependable Dividend

2023-04-20 09:08:06 ET

Summary

- I've covered a fair number of REITs, Financials and Utilities to this day, because I believe these are the best-positioned sectors to outperform.

- Today, I describe in detail how I evaluate whether a stock will do well during an economic slowdown or not, and present my pick for a potential recession.

- The company offers a 9.7% dividend yield, which has been confirmed until 2026.

Dear readers/followers,

Those of you that have been following me have probably figured out by now that my investment strategy is fairly conservative. I don't invest in high multiple growth stocks aiming for the moon, but look for value, income, and safety. There are basically two types of investments I make. First and foremost I look for fundamentally sound and stable companies in sectors I understand and where I can (hopefully) forecast the future better than the masses. I look for these companies with the expectation of generating a reasonably high and dependable dividend yield and ideally one that grows over time. Secondly, from time to time, I dive into a pure value play, usually in a stock that I believe has been unfairly punished by the market and one that I expect to recover over the next 3-5 years.

The reason I mention this is that today I want to present my " Investment idea for the potential recession " which can be interpreted differently by investors. For me and my investment style, this is not about finding a stock that will generate massive returns in case of a recession (I see that as risky and will happily leave that to other authors), but rather about finding a stock with a decent dividend yield that can really be depended upon even during a severe recession and with a stock price which won't suffer too much in the short to medium-term and will likely recover in the long-term. It also helps if we can buy this stock at undervalued levels, creating a sufficient margin of safety. In other words, I'm looking for a stock which will allow investors to weather the storm without affecting their income (and lifestyle) and will allow them to come out ahead on the other side. That's what I'll try to do in this article.

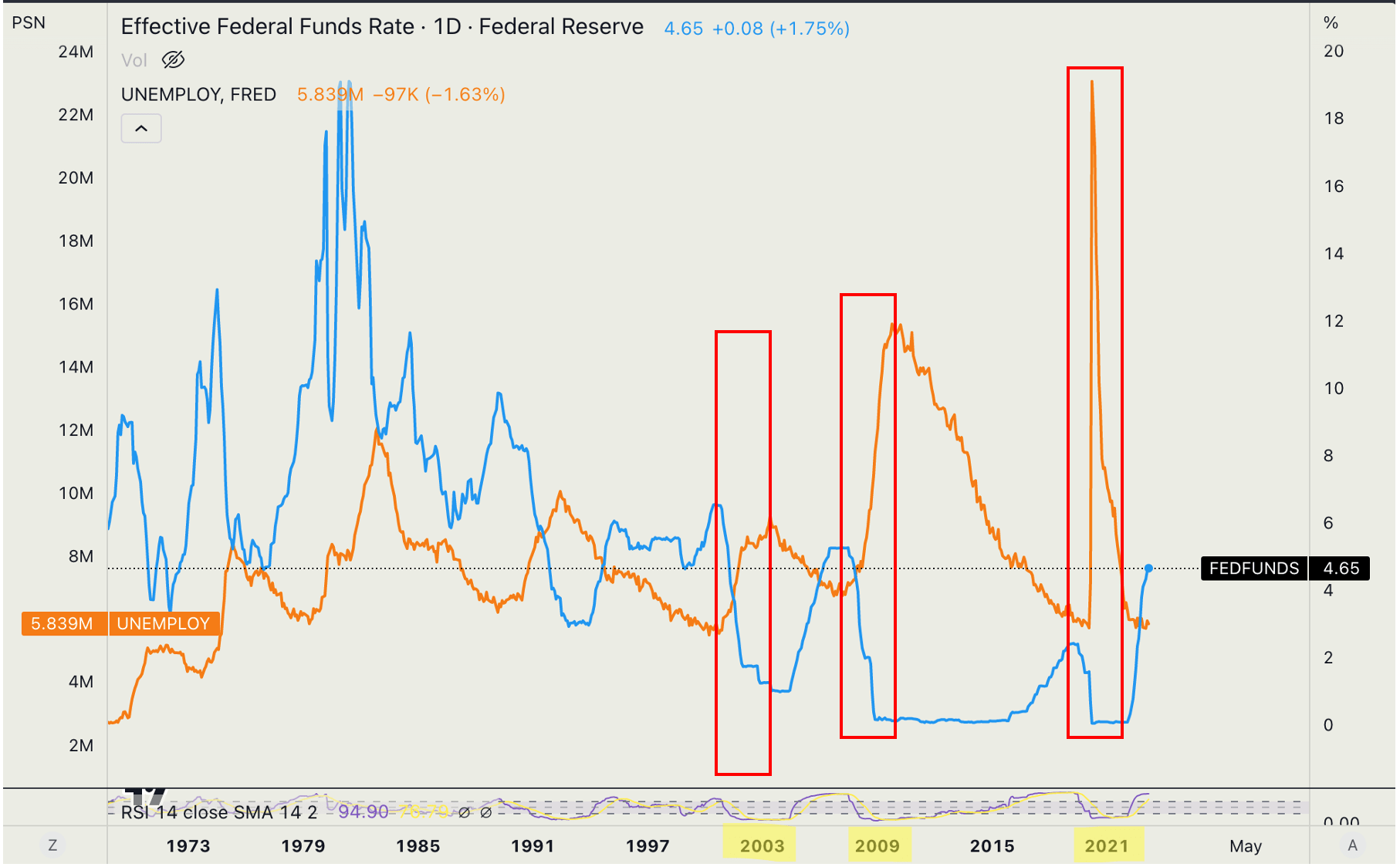

Before diving into the stock itself let's lay out some basic expectations for the potential recession based on history. In the past, every major recession in the US has been accompanied by a steep rise in unemployment (orange line below). Indeed this was the case in the three most recessions in 2001, 2008, and 2020. And although the labor market is still very strong today, we must expect that if we are to enter a severe economic slowdown, unemployment will rise eventually. What has happened in response to this rise in every single case in the past? The Federal Reserve has cut rates in order to stimulate the economy (see blue line below for the Fed Funds rate). This means that for our recession base case, we have to expect a major rise in unemployment and a decline in interest rates which given the current inflation dynamics could spark inflation again. These dynamics play out exactly the same way in Europe as well. Our recession-proof stock pick then has to fulfil three criteria:

- Demand has to be fairly non-cyclical so that it doesn't drop when unemployment rises.

- The company has to have pricing power so that if inflation rises again, it can keep raising prices even into a recession (i.e., it has to offer a necessary product, not a discretionary one).

- We want a company that will benefit from a decline in interest rates so one that has debt or one whose valuation is very sensitive to rates.

Author's analysis on TradingView

{kind=link}

I could find examples of such companies in all three sectors that I'm currently overweight (Real Estate, Financials, and Utilities), but really feel that utilities fulfill these criteria best. That's why today I want to suggest a Spanish natural gas infrastructure player Enagas, S.A. ( ENGGF ) as my pick for a potential recession.

Note: the article discusses the native shares of Enagas that trade under the ticker ENG on the Madrid Stock Exchange. There are also ADRs available under tickers ENGGF and ENGGY .

Enagas overview

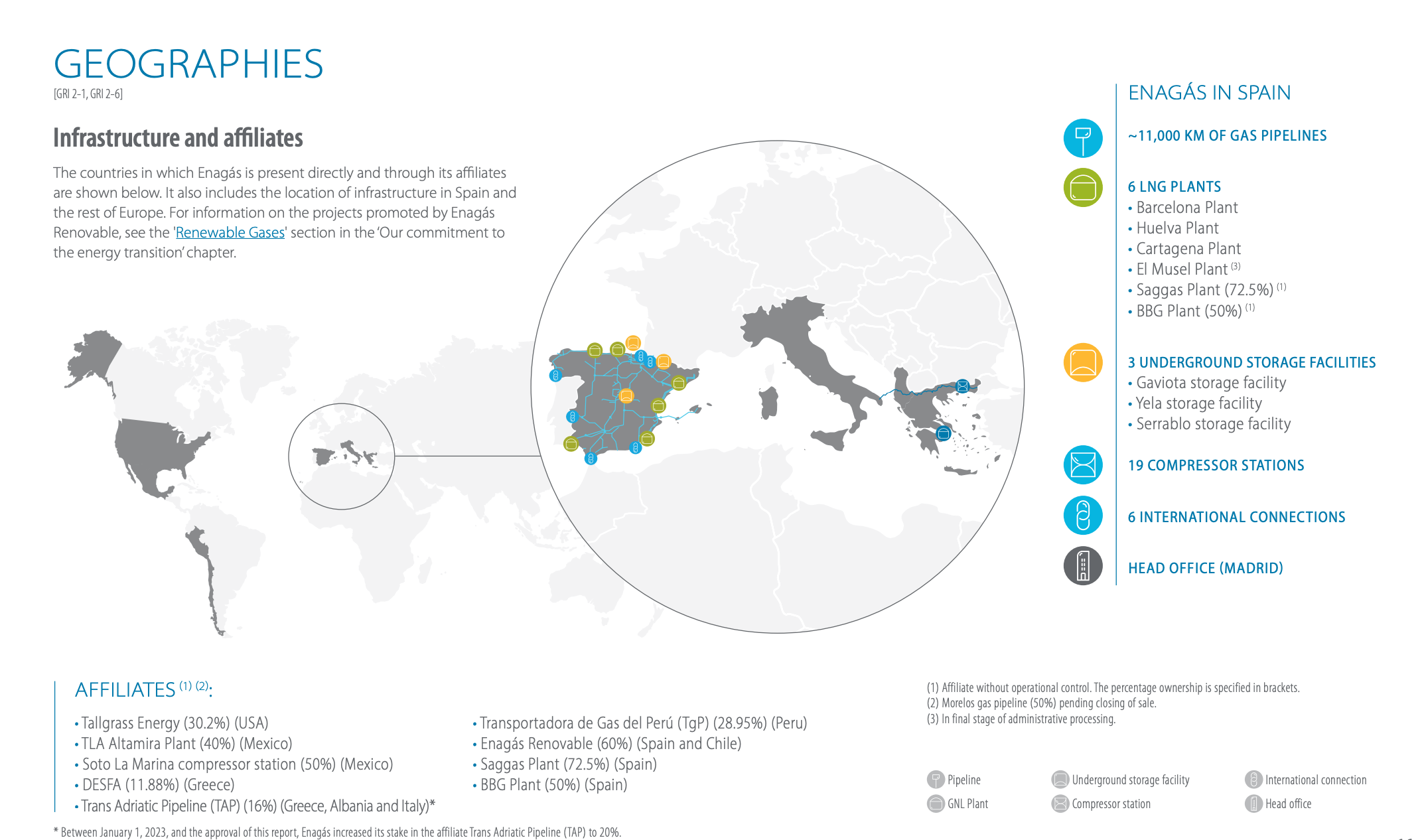

Enagas is a major provider of natural gas infrastructure in Spain where the company owns and operates over 10,000 km of gas pipelines, 3 massive underground storage facilities, 6 large LNG terminals as well international connections to Portugal, France, and Morocco. In addition, the company has stakes in critical infrastructure abroad. This includes a 16% stake in the Trans-Adriatic Pipeline ((TAP)) connecting Turkey with Italy, a 30.2% stake in Tallgrass Energy LP, which owns critical natural gas and oil pipelines in the US and several JV investments in Latin America (Mexico, Peru, and Chile). Enagas is essentially a state monopoly on natural gas in Spain with interesting investments in critical infrastructure across the world. Moreover the company has zero Russia exposure.

{kind=link}

In addition to legacy natural gas infrastructure, Europe has moved forward with their plan to construct a major hydrogen corridor H2Med by 2030, connecting France, Spain, and Portugal. Enagas will be a major player in the development of the project and will play a major role in meeting the domestic hydrogen demand and transporting over 2 Million tonnes of hydrogen to Europe (about 10% of the estimated total demand by 2030). The project is still in the early phases of planning, but Enagas expects significant synergies with its existing business as 80% of the routes coincide with existing infrastructure, and over 30% of gas pipelines have been classified as reusable.

Unfortunately being a monopoly alone won't make Enagas prosper and actually comes with some risks. While the Spanish gas system is geographically very well positioned as an entry point for supplies to Europe, the growth in natural gas demand in Europe has slowed and seems to have peaked in mid-2021 as the continent aims to become greener.

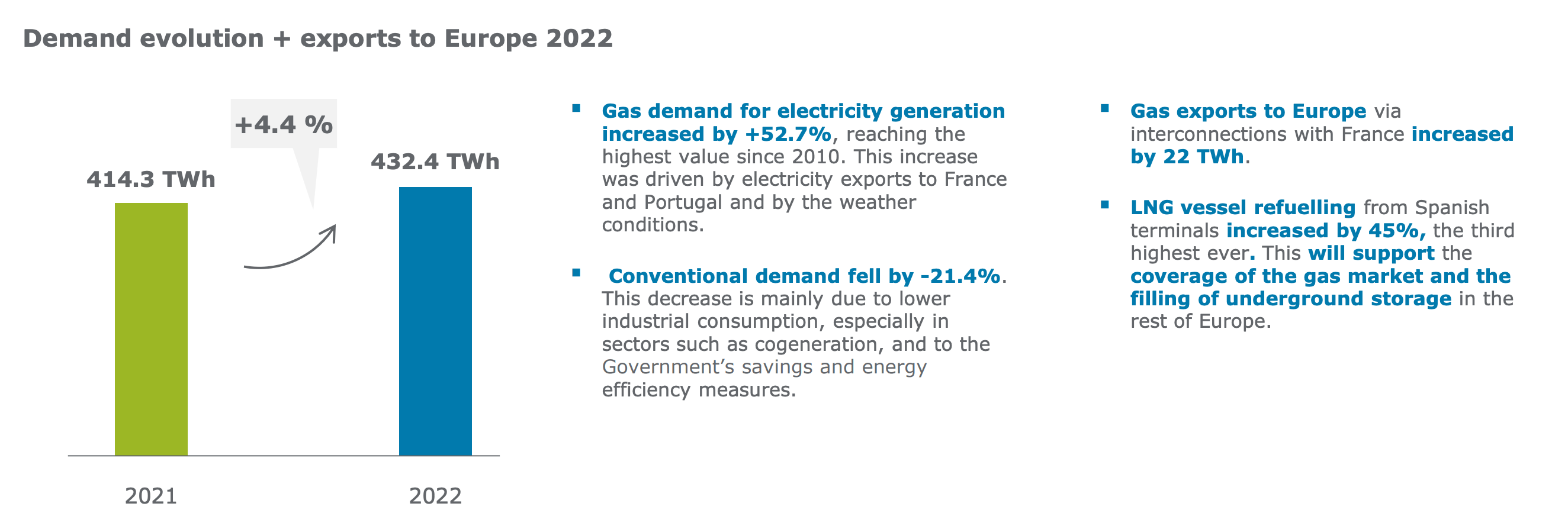

In 2022, Enagas saw a decent 4.4% increase in the volume of natural gas transported. This modest increase was largely driven by exports through international connections and LNG vessel refuelling which grew by 90% YoY. Notably, conventional demand saw a 21% YoY drop, mainly as a result of government efficiency measures.

{kind=link}

Going forward, growth in Spain is likely to be very slow. This is because the EU, including Spain, is pushing for green energy and, as a result, has already announced lower transmission volumes for Enagas. This means that while I don't expect a collapse in revenues, further growth on the old continent is unlikely. This is why the company has tried to expand globally via its JV investments such as the TAP, Tallgrass, and operations in South America. So far, it seems to be working as Tallgrass recorded a solid 9% YoY increase in EBITDA while the TAP saw transmission volume climb by over 40% YoY in 2022.

Growth outside of their legacy market will be really important, especially because the company struggled to keep their margins stable in 2022, as their net income margin decreased from 41% to 39%. This was largely caused by significantly higher operating expenses, although a significant chunk of these were non-recurring staff costs related to terminations and higher audit costs related to regulation. For 2023, management sees keeping operating expenses low as a top priority and so do I.

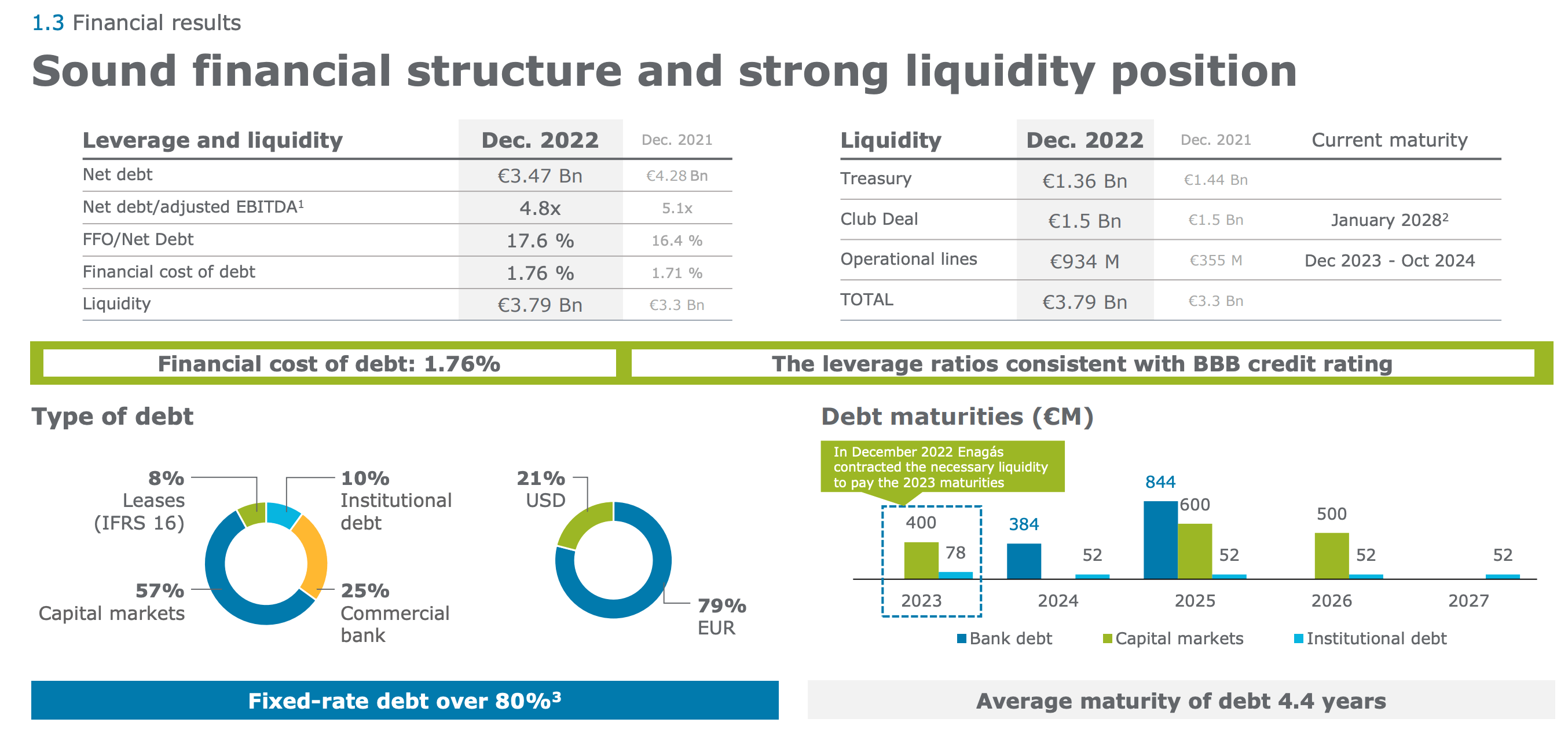

To sum up, the biggest risk for Enagas and us as investors is slow top-line growth and margin compression due to rising costs and (green) regulation and to be fair, this has been the main story for quite a while for Enagas and the main reason why the company no longer generates enough earnings to cover their dividend. That's obviously a red flag especially when you consider that we're essentially buying this stock for its 9.7% dividend yield. There is nothing worse than buying a stock for its dividend only to see it get cut.

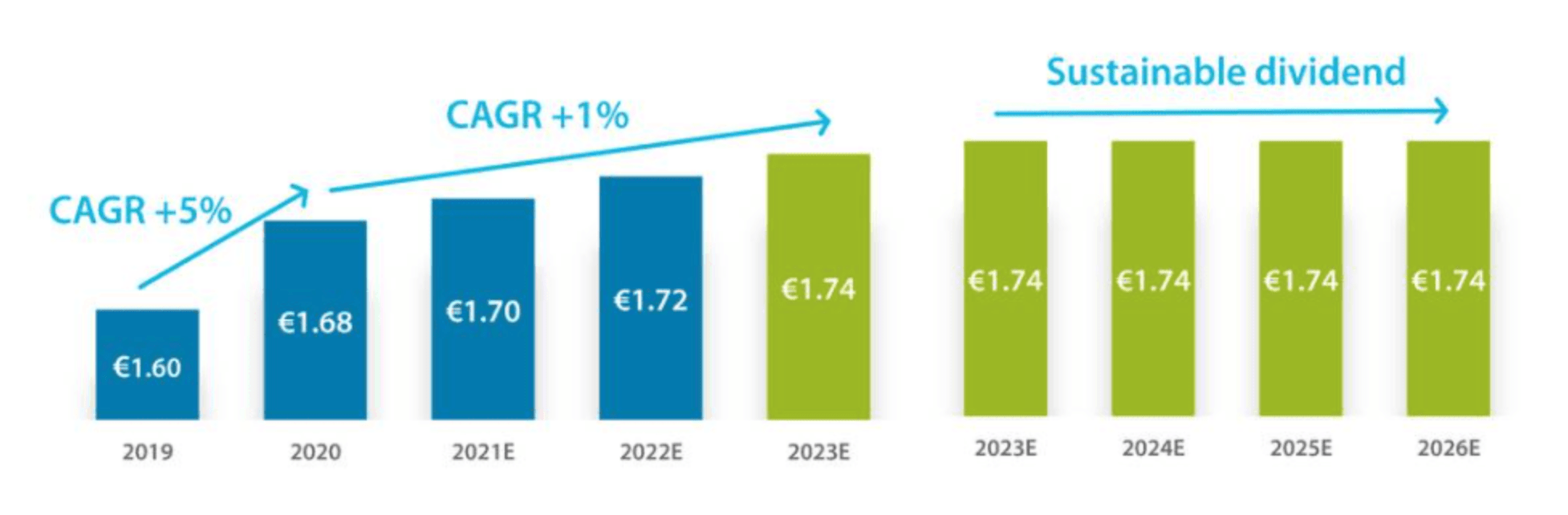

There are, however, a couple of things that are keeping me calm. Firstly, similarly to REITs, for companies like Enagas EPS is arguably not the best measure to compute the payout ratio. Free cash flow is better and in terms of FCF the dividend is actually covered (payout ratio of 80%) and as long as free cash flow remains above EUR500 Million or so the company will be able to cover the dividend with FCF. That seems very doable so far as most forecasts see FCF increasing to EUR600-700 Million by 2025. Moreover, management has already committed to the EUR1.74 per share dividend until 2026, making it quite difficult for them to go back on that promise. Nonetheless, this confirms the fact that the company must find growth outside of Spain in order for the dividend to truly be sustainable long term.

{kind=link}

Before we get to valuation, I want to go back to my recession pick criteria and see how Enagas is doing.

- Non-cyclical strong demand - check. People need gas, the legacy infrastructure in Spain is absolutely critical, and even in case of a severe recession, it's unlikely that revenues would collapse.

- Pricing power - check. Natural gas is not a luxury, it is a necessity. The only limiting factor (and frankly a wild card) in raising prices will be regulation.

- Benefit from a decline in rates - check. The company has a BBB-rated balance sheet with EUR3.5 Billion in debt and while it's true that 80% of it is fixed-rate, the average maturity stands at just 4.4 years. This means that the company refinances often so if rates decline, it will get to refinance at a lower rate. Moreover, lower rates would allow cheaper financing for their international expansion.

{kind=link}

To conclude, I'm fairly confident that Enagas would survive a severe recession, its revenues wouldn't drop too much and it would keep its very high dividend, which currently stands above 9%. That alone is enough to weather a recession, provided we don't overpay for the company today.

Using multiples to value the company is fairly tricky and I think the best way to go here is a dividend discount model. Given the current dividend of EUR1.74 per share and expecting zero growth and an 8% discount rate (in line with returns of an index) I get a price target of EUR21.75 per share (+20% from today). Put another way, using the 8% discount rate, the market is pricing in a dividend cut to EUR1.44 per share, which I simply don't see as imminent. That gives me enough of a margin of safety to buy the stock for the dividend yield and hold it through a potential recession so I rate Enagas as a "buy" here at EUR18.14 per share.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Enagas: Recession-Resistant With A Dependable Dividend