ENTA - Enanta: Deep Dive Reveals No Changes To Growth Headwinds

2023-06-23 16:14:00 ET

Summary

- Enanta Pharmaceuticals faces challenges due to lack of profitability and sales growth, as well as unwise R&D investments.

- The company's royalty structures are attractive but do not mitigate downside factors, leading to a neutral investment view.

- Enanta's current valuation and lack of positive sentiment make it difficult to recommend a buy.

- Net-net, reiterate hold.

Investment Summary

Following my neutral rating on Enanta Pharmaceuticals, Inc. ( ENTA ) in December, the company has sold off to now trade at 52-week lows. The December publication identified a number of critical facts that needed addressing to satisfy investment–grade criteria, whilst highlighting the positives. To name a few:

- Lack of equity risk premium exhibited from fundamental, economic or valuation-based factors.

- Potential value to be obtained with the company's royalty agreements (there has been an update on this in Q1).

- Initiation of SPRINT phase 2 trial to advance the EDP-235 formulation, where 200–400mg dosage was to be determined.

- Unsupportive valuations trading at 60x forward EBITDA at the time.

There have been several updates to the critical facts within the investment debate that need discussion. However, there is insufficient mitigating evidence against a hold rating on ENTA in my informed opinion. This report will cover all of the updated moving parts in the ENTA investment debate. Net-net, reiterate hold.

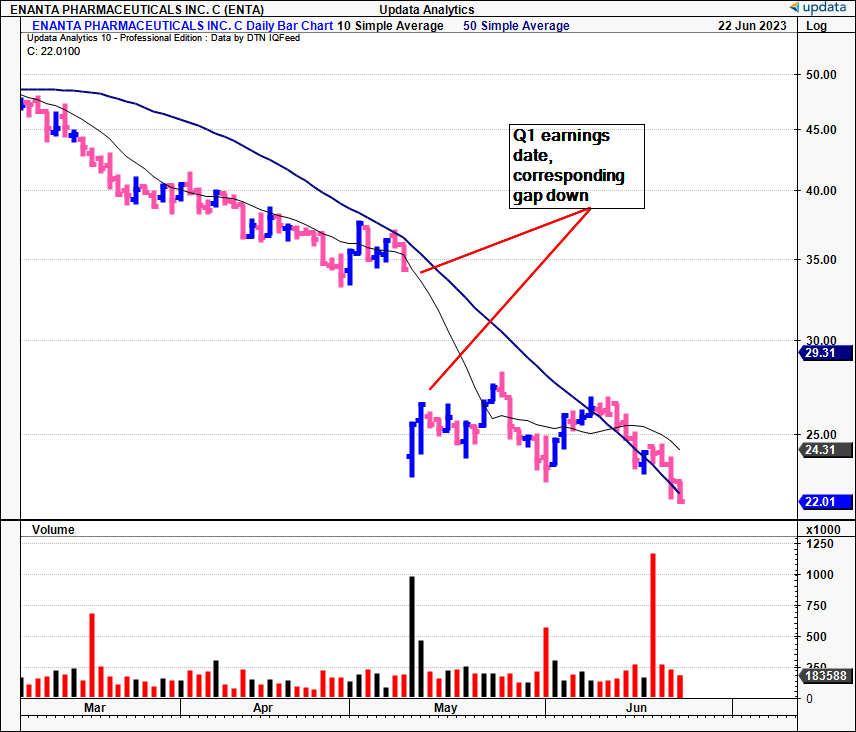

Figure 1. Selloff after Q1 FY'23 numbers, indicating expectations

{kind=link}

Critical facts in the ENTA hold thesis

There are a number of additional contributing factors feeding into the ENTA investment debate, as mentioned. These consolidate into fundamental, sentimental and valuation-based domains.

1. Fundamental factors

ENTA booked $17.8mm in Q1 turnover . Most of the clip was generated from royalty revenue earned on AbbVie's global MAVYRET net product sales, under the royalty structure. I discussed this at lengths in the last publication. Importantly, management said that patient volumes were down YoY and this could be a headwind to sales growth moving forward.

Speaking of sales growth, it hasn't been a standout feature in the ENTA story thus far, evidenced by the following record:

Table 1. ENTA long-term revenue, R&D investment record

Data: Author, ENTA SEC Filings

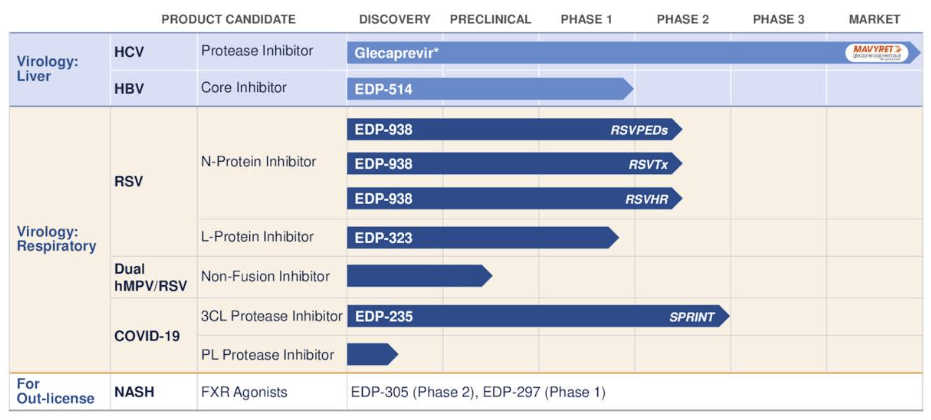

Key to the debate is the company's R&D investments that is used to fund clinical programs and convert clinical assets into intangible ones on the balance sheet. Adjustments to GAAP operating income must therefore be made. Doing this, you see the rapid decline in operating earnings on an annual basis into 2023, where 2023 is presented in the TTM. This is despite the R&D investment increasing from $40mm to $158mm over this time. The firm's entire pipeline is observed in Figure 2.

Figure 2.

{kind=link}

The following points are relevant on the company's newly obtained royalty structure:

- The firm announced a significant royalty sales transaction with OMERS that captured investors' attention in Q1.

- This transaction involved the sale of 54.5% of the company's future global royalties earned on net sales of MAVYRET from July 2023 until June 2032, with payments capped at 1.42x the final purchase price.

- The acquired ––OMERS–– paid the company $200mm upfront, providing the firm with an additional source of non-dilutive financing.

- Furthermore, the company retains 45.5% of all royalties until the cap is reached. After this point, 100% of all further royalties will revert to the company.

- This is a bullish tailwind that must be recognized, and certainly adds a layer of balance to the investment debate.

Moving down the P&L , it lost ~$3mm at the G&A line given frictional costs tied to growth, and clipped $4mm in adj. operating income, when adjusting for the $43.5mm R&D investment of the quarter. It recognized a net loss of $37.7mm. It's worth noting that the firm's current position is supported by its approximately $225mm cash reserves, along with the $200mm in cash received from the royalty sales transaction. Hence, there is no drains or pulls on liquidity– just a lack of operational growth.

2. Sentimental factors

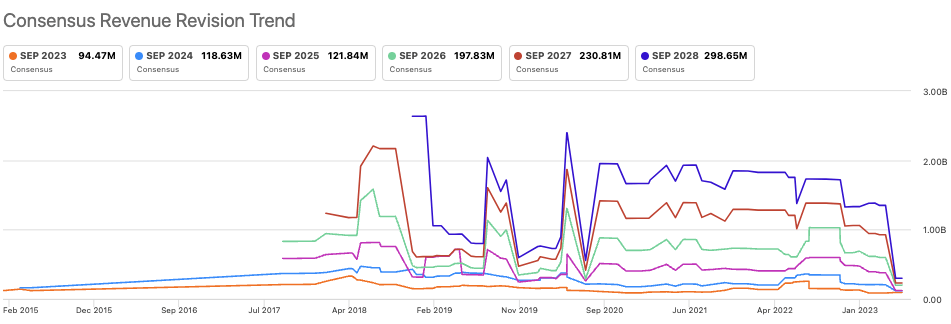

Current investor sentiment is a critical aspect to consider in the debate here. The lack of positive sentiment poses difficulties to ENTA re-rating in my opinion. Note, this sentiment is influenced by the absence of catalysts, which can be discerned through the analysis of sell-side analyst ratings.

Figure 3.

{kind=link}

In the last 3 months, there have been five revisions down each for turnover and earnings, leading to a more bearish sell-side. Consensus expects growth of 9% in FY'223, increasing to 25% in FY'24, which confirms a neutral view.

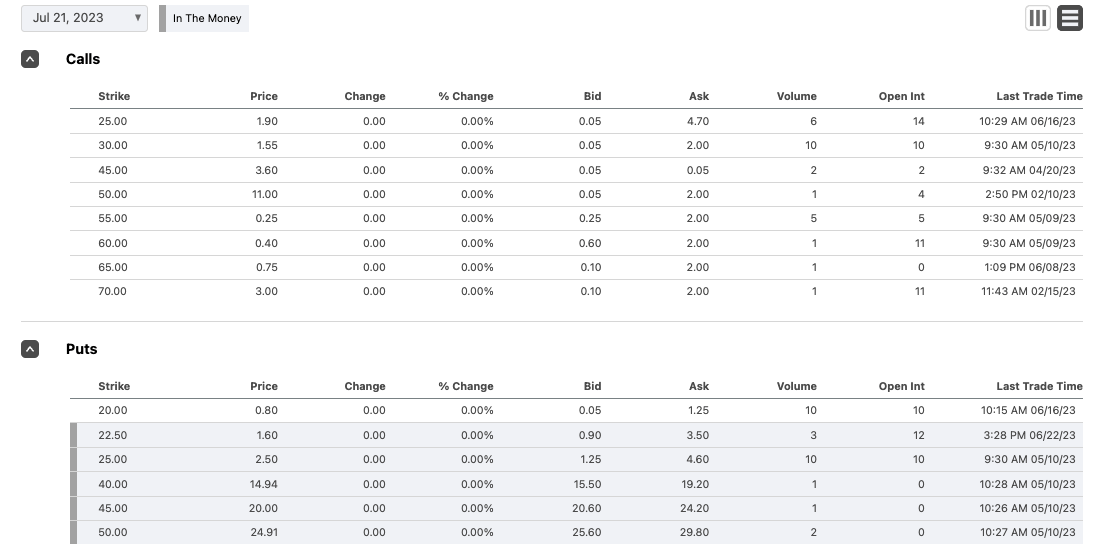

Moreover, options positioning is currently neutral, with investors positioned on both sides of the chain, ranging from strikes on calls of $25 to puts as low as $20. This could be a result of hedging activity or strategies applied to play the sideways trend. Nonetheless, there is no bullish action in the money, highlighting the opinions of those with money at risk. This further supports a neutral perspective.

Figure 3a. ENTA options chain, in the money, July 2023 expiry

{kind=link}

Finally, the downward momentum and price action are indicative of sentiment as they capture all the drivers "in the price". The fact that ENTA trades below all moving averages implies that expectations are "below average". In the absence of positive sentiment, it would be difficult to recommend a buy, as it would be a contrarian stance not backed by fundamental data. If the latter were true, it would be a different story.

3. Valuation factors

Investors are selling ENTA stock at 5x forward sales, which is 20% above the sector. In my opinion, based on the factors discussed here, I do not believe ENTA objectively deserves to trade above the sector. There are many high-quality names that warrant this amongst ENTA's peers, but not the company itself.

Consensus expects $94.5mm in turnover this year and I am comfortable with this number. This calls for 9-10% growth and looks overly priced at the 5x forward multiple. In that vein, it appears the market has priced ENTA correctly given the available data. On my analysis, there doesn't appear to be a disconnect in fundamental or sentimental factors to the valuation. At 5x sales on $94.5mm, you get to $22 as well. Hence, this also supports a neutral view.

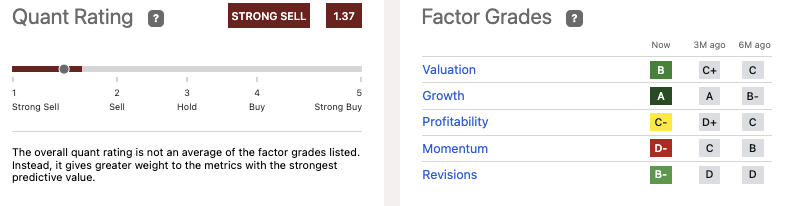

I would also urge investors to pay very close attention to the quant systems' "strong sell" rating on ENTA. These are not to be ignored. Whilst there is some positives in a few of the sections ––growth, for example–– the calculus involved in setting the quant rating is not constructive on the stock. I would suggest this also supports a neutral view. In the absence of quality earnings data, objective findings are of the utmost importance to form an investment view. In that vein, with the quant's system at a sell, this supports my rating.

Figure 4. ENTA quant grades

{kind=link}

Discussion

To say it's been a challenging few years for ENTA shareholders would be an understatement. Fundamentally, the case is blurred, leading to a pessimistic sentiment, and these factors combined aren't conducive to the firm trading higher. One of the main points is the destruction in profitability and sales growth. As mentioned, one of the key facts is the monetization of the company's R&D investments. Given the upscale in investment compared to the reduction in income, it would tell me the capital has been spent unwisely, on unprofitable clinical programs that have consumed exorbitant amounts of capital.

This is telling for what to expect moving forward. The company's royalty structures are definitely attractive– but do nothing to mitigate the downside factors. As such, there is a lack of available evidence to warrant a re-rating. This, combined with the lack of sentiment, corroborates the fact investors are unlikely to pay a higher market value in my view, and thus I cannot urge readers to buy the stock when there are a multitude of selective opportunities available within the latest market rally.

In that vein, based on the culmination of data presented here, I reiterate that ENTA is a buy. This is a name that I will be closely monitoring in the coming months to see what to do next. The quant system has it at a strong sell, and that's not to be ignored in my view. Net-net, rate hold.

For further details see:

Enanta: Deep Dive Reveals No Changes To Growth Headwinds